Print

PrintLyuba Goltser and Rebecca Grapsas are Partners and Eleni Samara is an Associate at Weil, Gotshal & Manges LLP. This post is based on their Weil Gotshal memorandum.

Introduction to the Big Three and ESG Guide

The “Big Three” institutional investors, BlackRock, State Street Investment Management and Vanguard, recently released 2026 proxy voting policies and related guidance applicable to US companies. Companies are well-advised to review these policies and guidance in planning for engagement with the Big Three throughout the year and during the proxy season, and in considering environmental, social and governance (ESG) disclosures going forward.

In this Guide, we:

- Provide ESG-focused practical guidance for public companies to consider in light of these policies and guidance. See also our alert, Looking to the 2026 Proxy Season: Key Corporate Governance, Engagement, Disclosure and Annual Meeting Topics.

- Identify changes to the proxy voting policies and guidance of the Big Three on ESG topics for 2026.

- Summarize the expectations of the Big Three as to company practices and disclosures around selected ESG topics, and highlight where failing to meet expectations may result in votes against directors.

Practice Pointers

- Refine Approach to Shareholder Engagement. Companies should review agendas and goals for shareholder engagement meetings, to ensure they reflect shareholder engagement priorities, comply with investor policies around engagement in light of recent Securities and Exchange Commission (SEC) interpretations discussing ownership reporting in the context of seeking to change or influence control, and can address as appropriate areas where the company may not be currently meeting expectations. Companies should ensure that directors and senior management participating in engagement meetings are well-briefed on material ESG-related risks and opportunities, current disclosures and practices relating to ESG topics, and do’s and don’ts of shareholder engagement.

- Identify Vulnerabilities. Companies should review their disclosures and practices in light of the Big Three’s policies and guidance, to help identify where one or more of the Big Three may vote against directors and/or support shareholder proposals. Companies may work with proxy solicitors to determine the expected support of the Big Three and other major shareholders on ballot items, as well as the expected recommendations of proxy advisory firms. To reduce the risk of significant votes against directors, companies should assess director vulnerabilities and may wish to conduct additional shareholder outreach.

- Refresh Materiality Analysis as to ESG-Related Risks and Board Oversight. Given significant recent ESG developments, companies should refresh their materiality analysis relating to ESG-related risks, and how ESG-related risks are integrated into the company’s enterprise risk management framework that facilitates risk identification, assessment, mitigation and monitoring. Companies should also review how the board provides oversight of material ESG-related risks and opportunities, and how this is reflected in board committee charters and related disclosure.

- Enhance Practices and Disclosures if Appropriate. Companies should confirm that the ESG narrative is cohesive across SEC filings, sustainability reports, company websites and other materials. To better reflect Big Three expectations and evolving regulatory developments, in planning ESG disclosures for the year ahead, companies may consider refining disclosure on certain ESG topics, for example:

-

- Refresh risk factor disclosure relating to material ESG topics, and forward-looking statement disclaimers (see our alert)

- Review proxy statement disclosure of board oversight of material risks (see our alert)

- Review company disclosures and initiatives (if any) relating to diversity, equity and inclusion (DEI), in light of continued heightened scrutiny

- Prepare for compliance with California climate disclosure rules, where applicable (discussed in our most recent comprehensive alert), and similar rules that may be enacted in other states

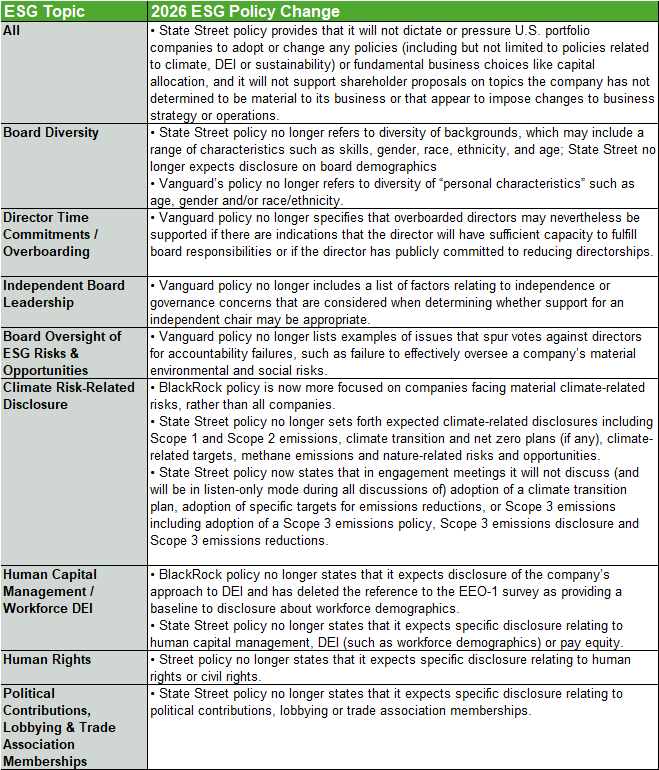

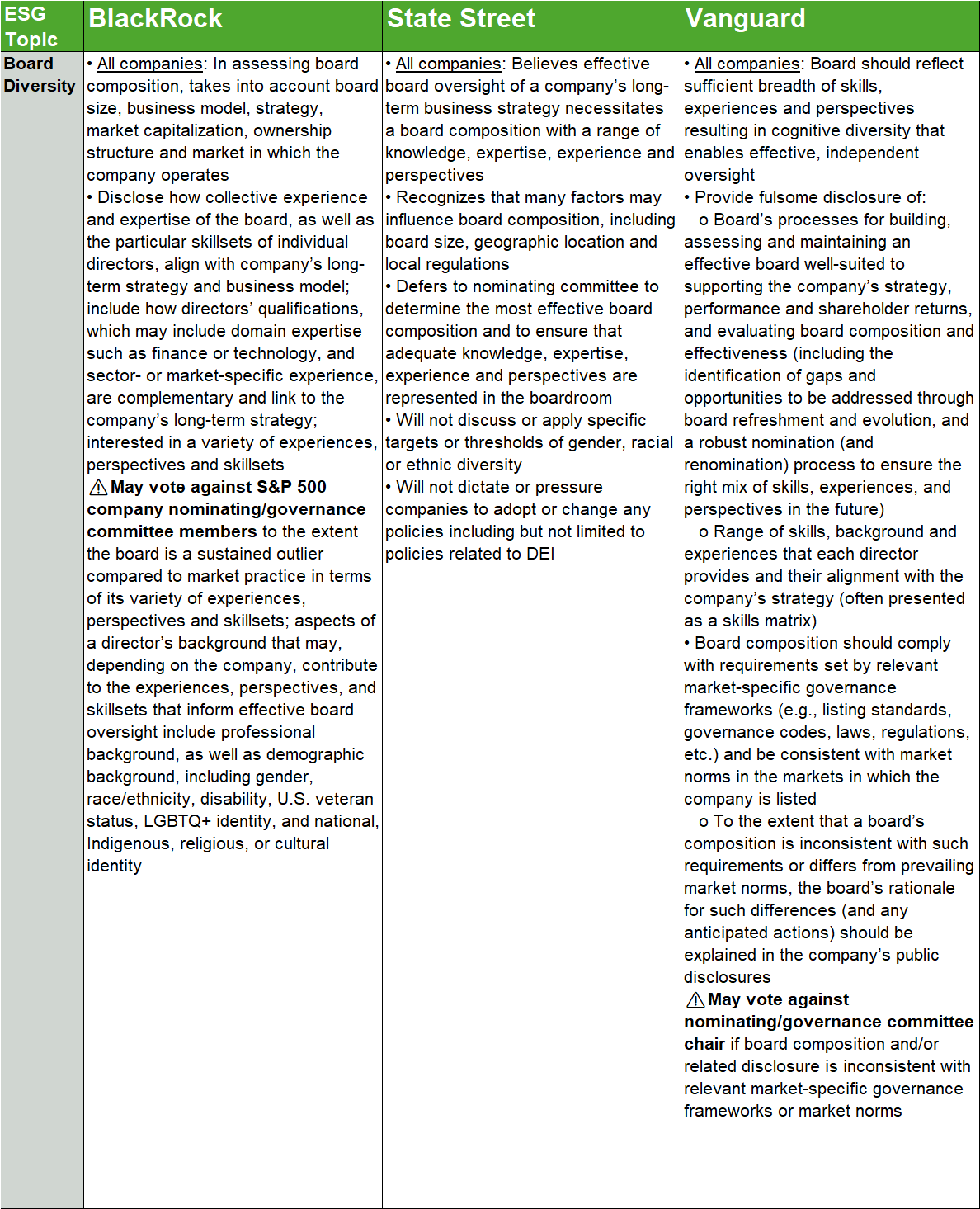

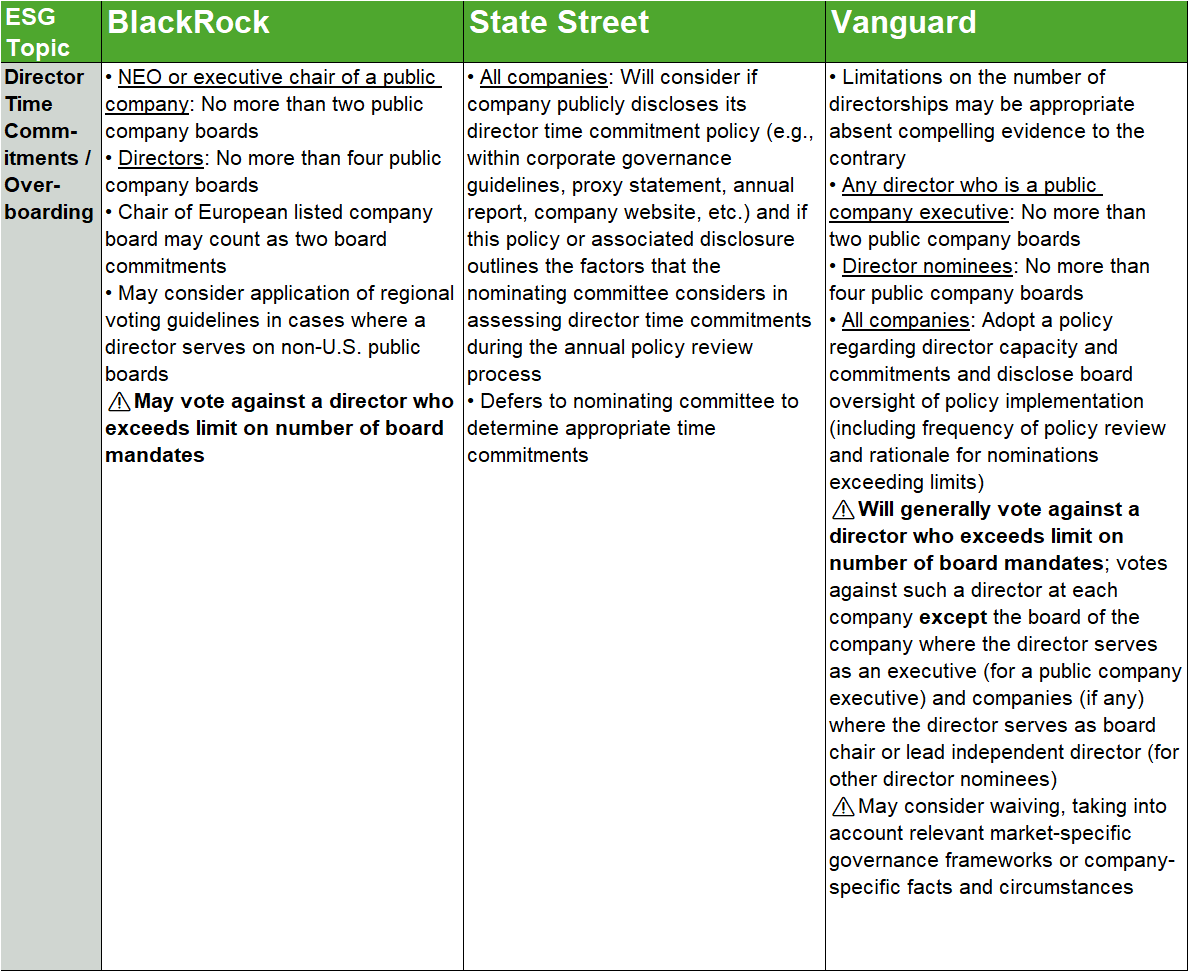

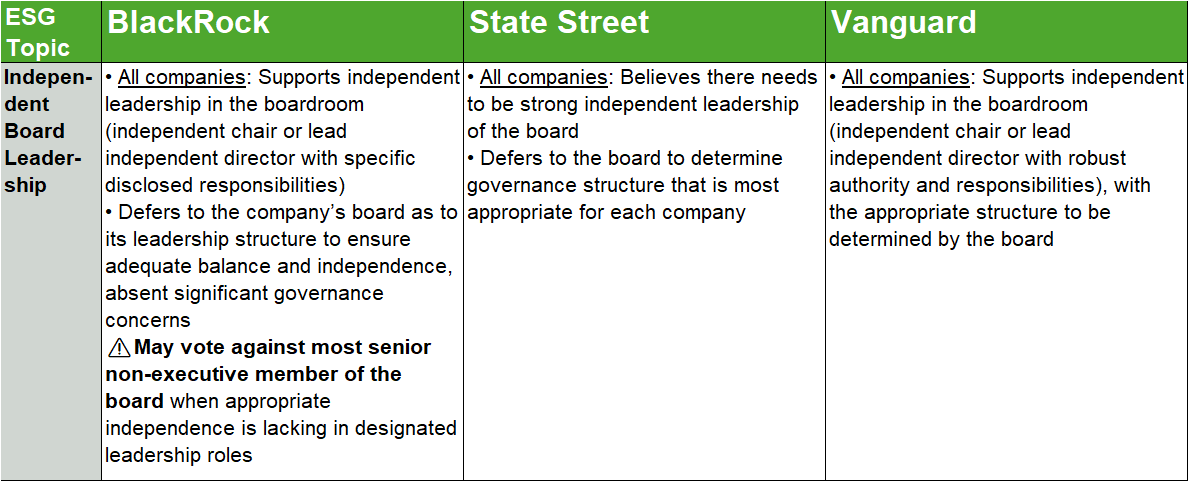

Big Three: 2026 ESG Policy Changes

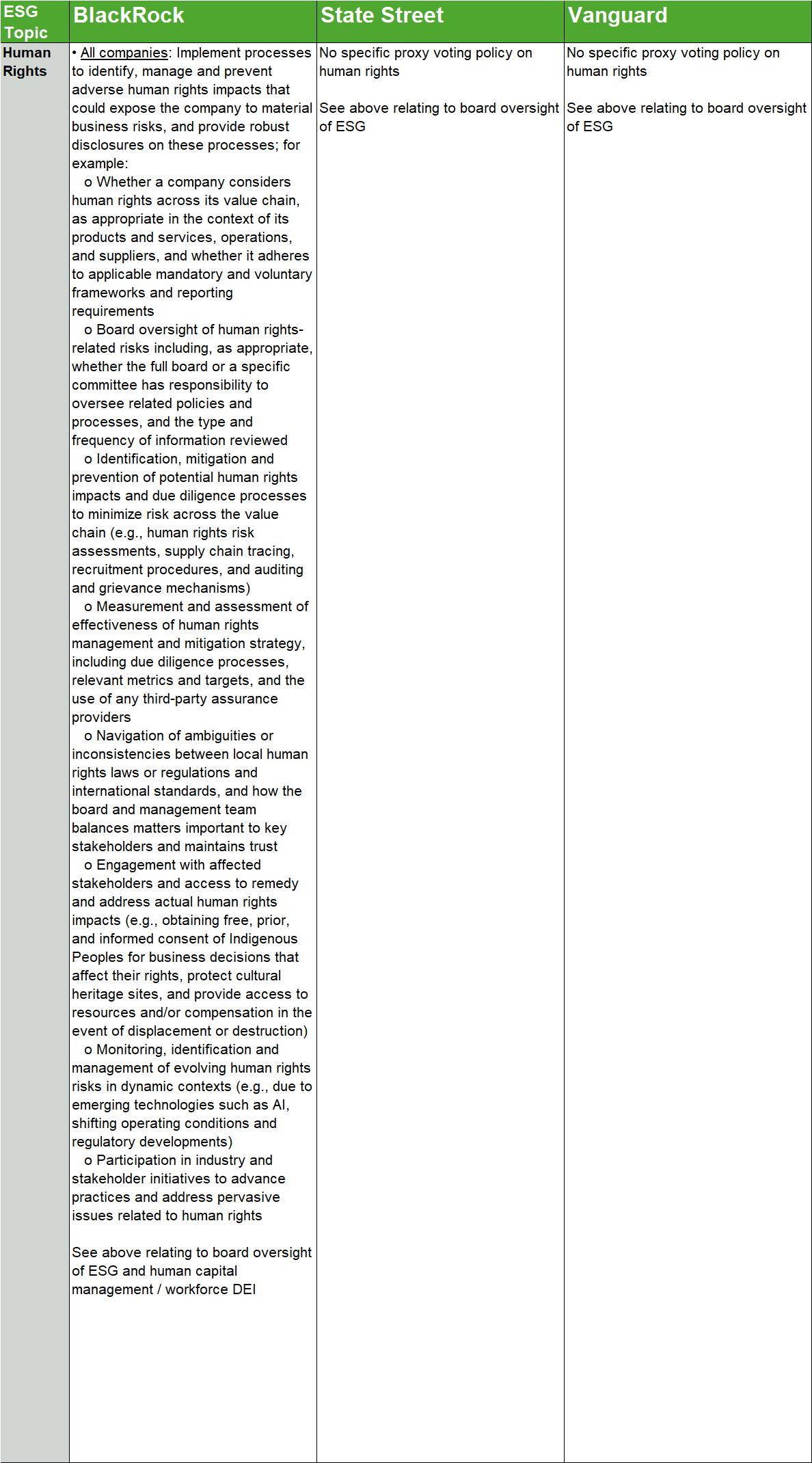

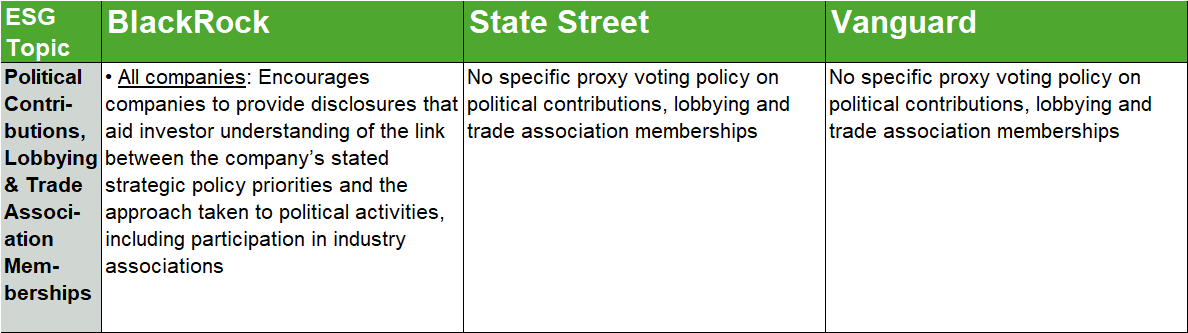

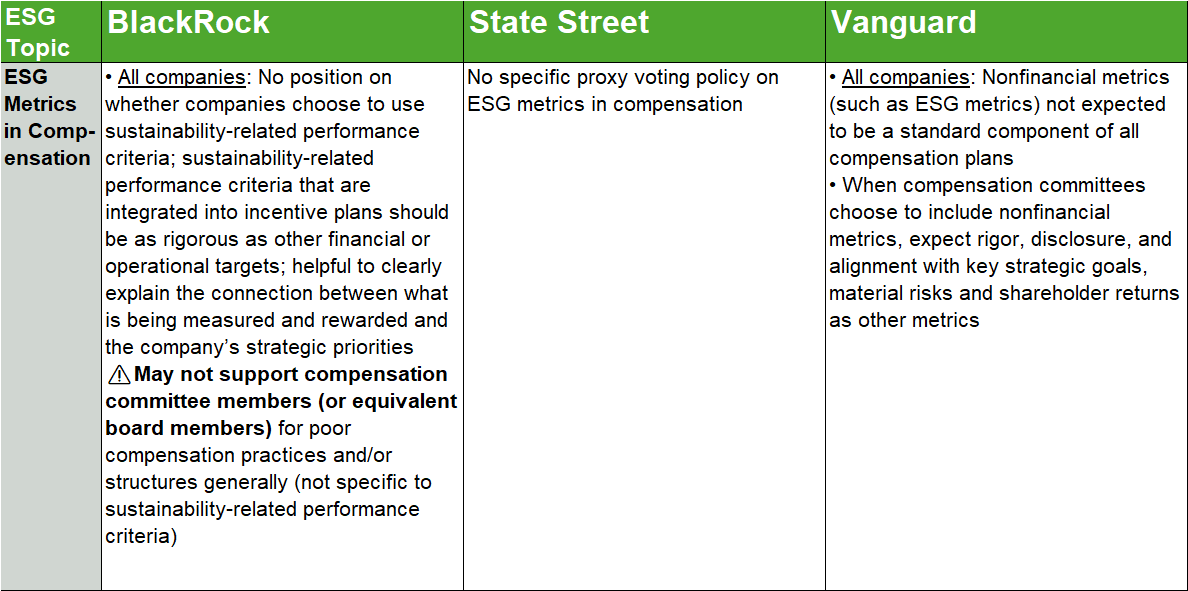

Summary of Big Three Proxy Voting Policies and Key Guidance on Selected ESG Issues

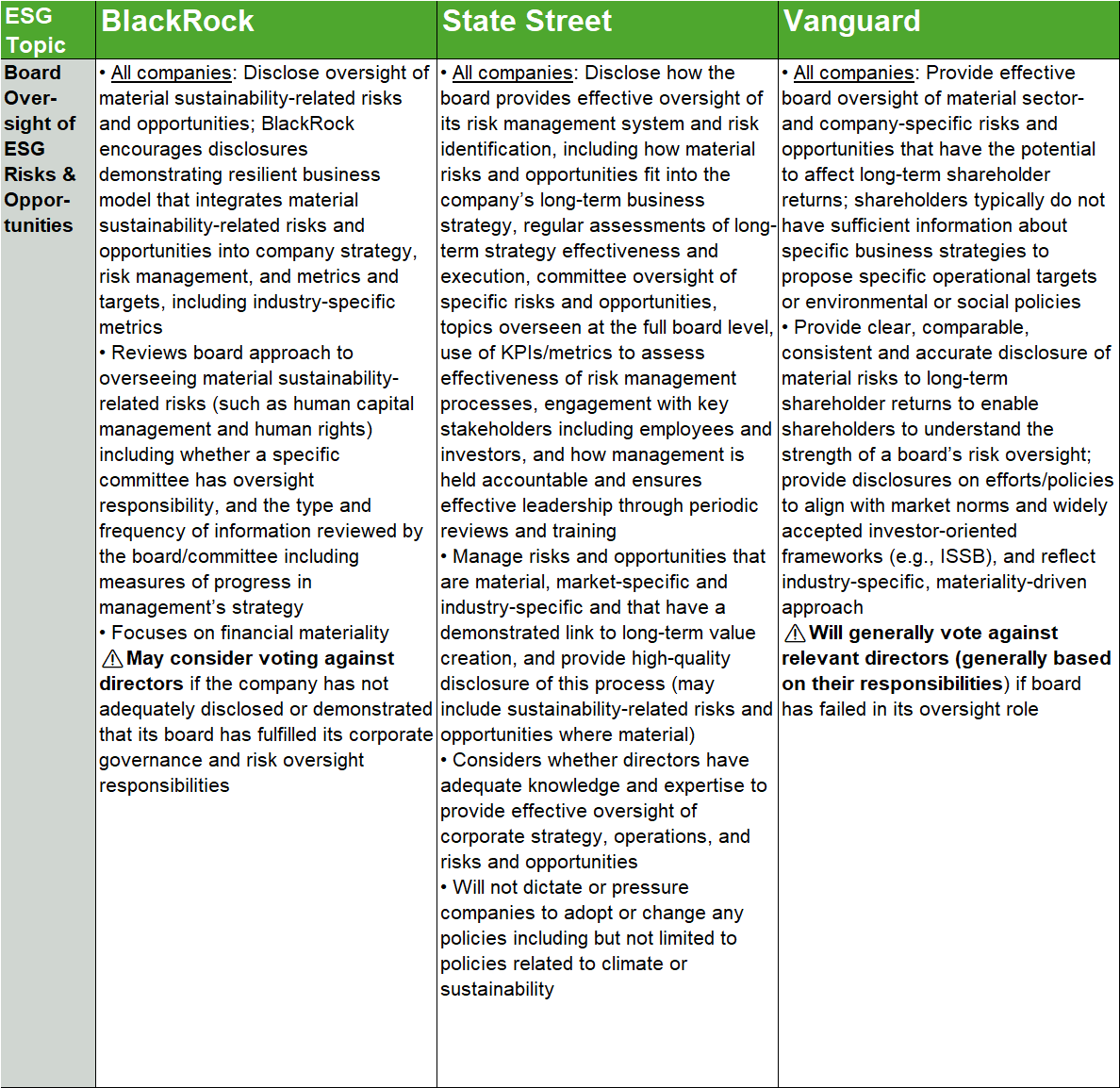

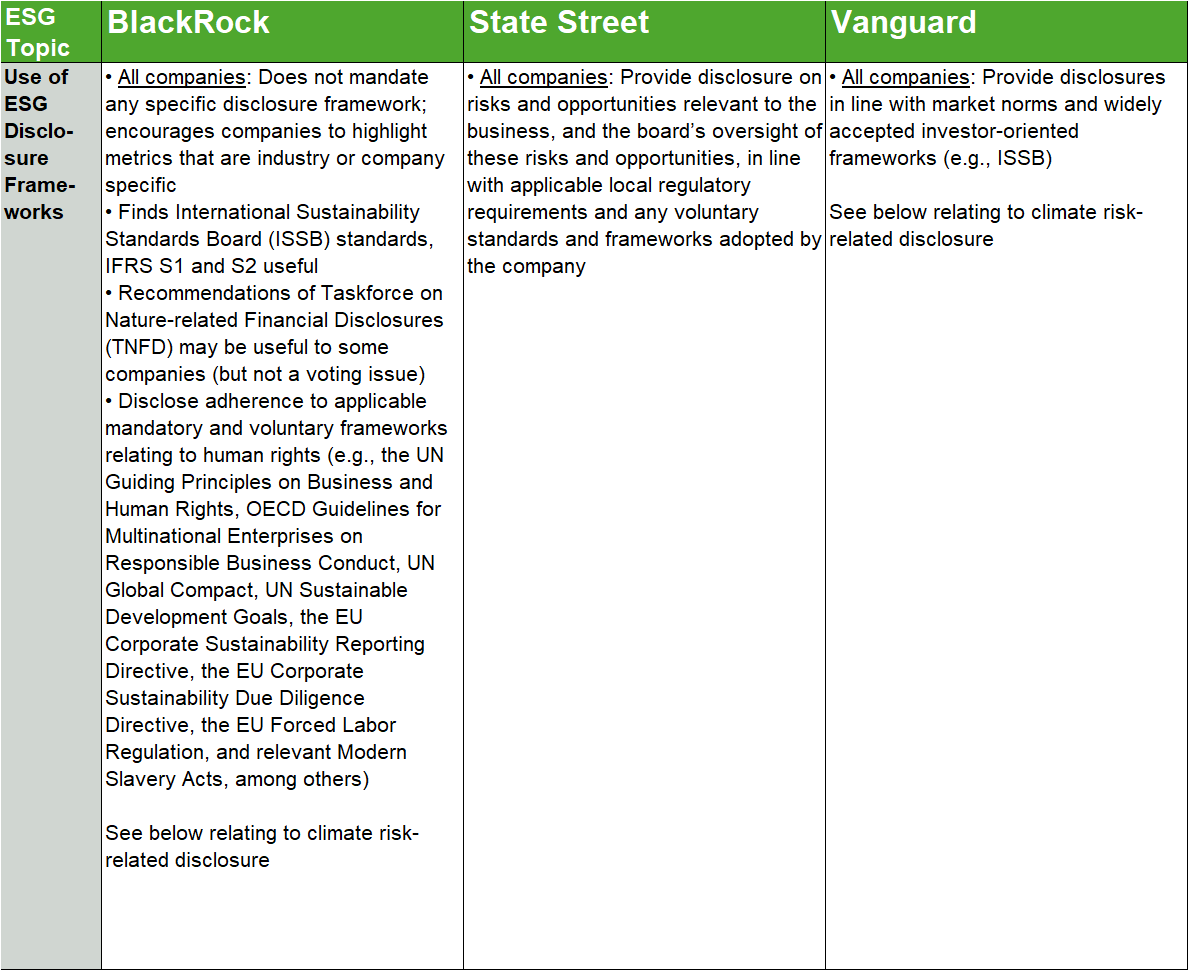

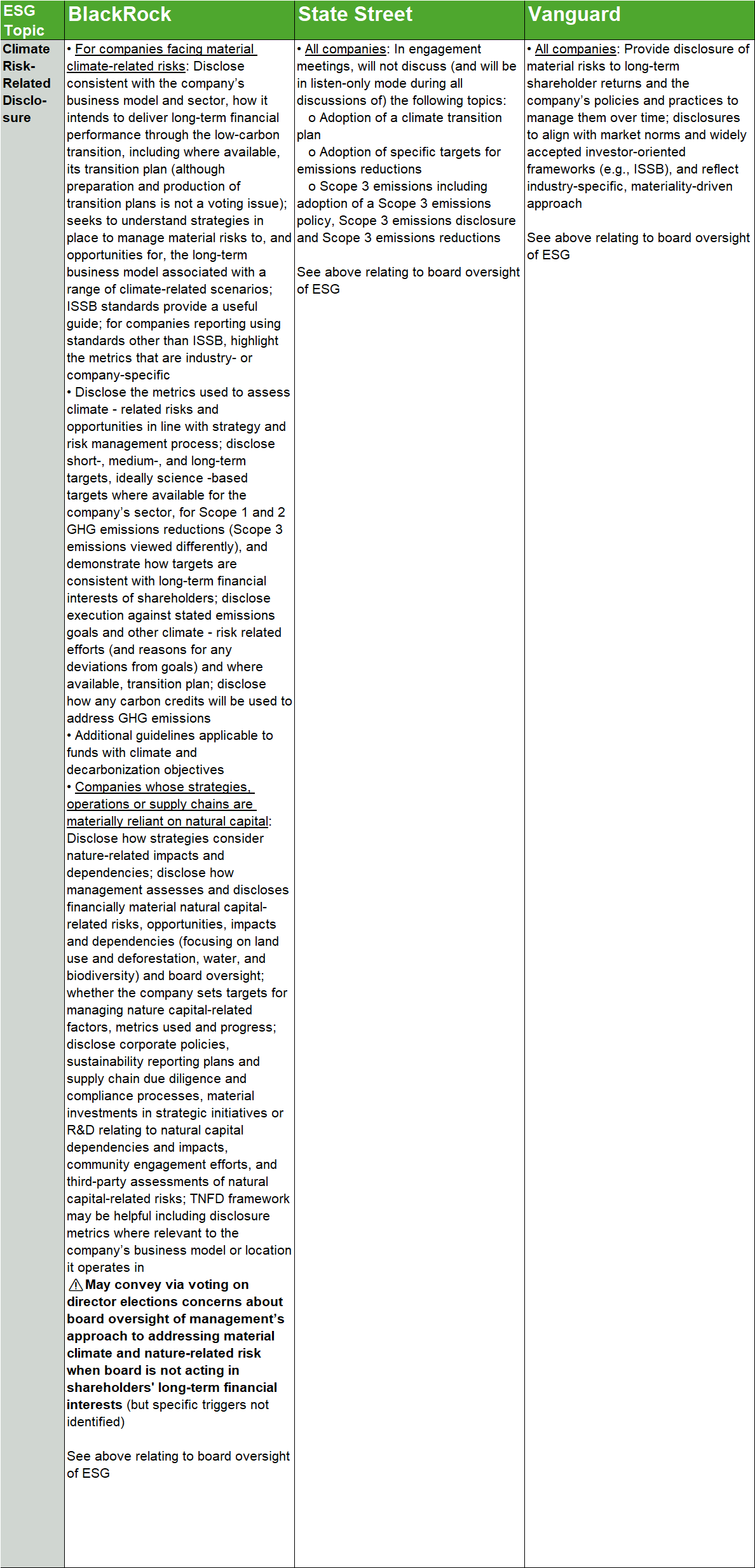

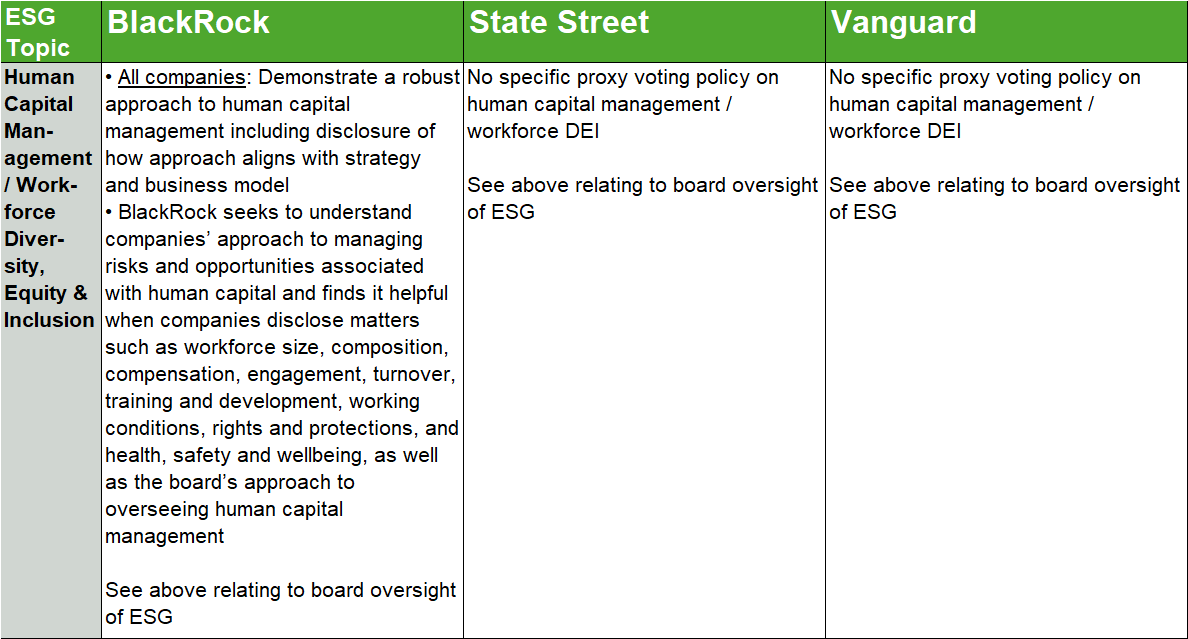

The chart below summarizes the expectations of BlackRock, State Street and Vanguard as to US company practices and/or disclosures relating to selected ESG topics, as described in benchmark proxy voting guidelines and related guidance in effect for the 2026 proxy season. These expectations guide Big Three engagement with companies on material issues as well as voting on directors and relevant shareholder proposals (e.g., proposals calling for particular disclosure on an ESG topic). The chart also highlights (with a ) where failure to meet expectations may result in votes against (or not supporting) directors, as described in the relevant proxy voting guidelines and/or guidance.

While the Big Three provide specific guidance in proxy voting policies about the disclosures they expect to see on a range of ESG topics, they do not specify when or where this disclosure should be provided (e.g., ESG report, publicly available policy, company website, SEC filing), except that BlackRock encourages companies to provide sustainability-related disclosures sufficiently in advance of the annual meeting so that disclosures can be considered in relevant vote decisions.

The complete publication is available here.