Print

PrintSanford Lewis is General Counsel, Khadija Foda is an Associate Counsel, and Tanya Agarwal is a Research Associate at the Shareholder Rights Group. This post is based on an SEC comment letter submitted by the Shareholder Rights Group.

The SEC Division of Corporation Finance is conducting a comprehensive review of Regulation S-K, and Chairman Paul Atkins has indicated that the current disclosure regime elicits significant volumes of immaterial information. As such, it appears the agency will seriously consider revisions to reduce disclosure requirements.

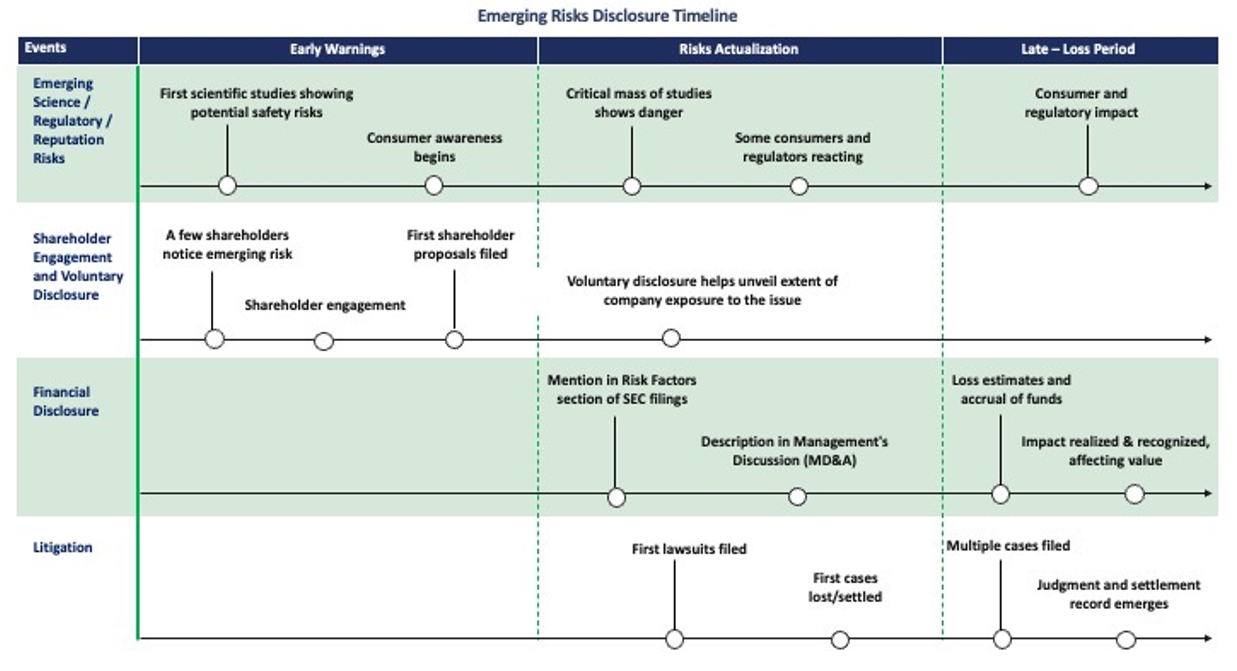

However, paring back Regulation S-K disclosures would harm a critically valuable disclosure ecosystem that provides investors with information on emerging risks and helps investors assess their portfolio companies and engage in stewardship in alignment with their fiduciary duties. Shareholder proposals and Regulation S-K disclosures work together in this ecosystem of disclosures. Shareholder engagement often leads to voluntary reporting, which, in turn, informs and ultimately expands Regulation S-K disclosures.

Emerging investor concerns about risks relevant to issuers are often surfaced initially through shareholder engagement and shareholder proposals, which lead to voluntary reporting such as sustainability reports, which are later filtered by board and management in the formal disclosures of Regulation S-K.

Information overload, which has been asserted as a basis for trimming disclosure obligations, is a false narrative in the current technical environment in which AI and other tools allow investors to efficiently sift through both voluntary and SEC mandated disclosures for the information relevant to their investment strategies.

In fact, we believe the lens for assessing materiality under Regulation S-K should be broadened to recognize that significant shareholder engagement and substantial support for shareholder proposals is evidence of materiality that should inform the need for disclosure under Regulation S-K as it demonstrates a substantial level of interest in an issue by a company’s own investors.

The investor engagement to surface these issues and assess a company’s potential exposure to these risks is a necessity because of the tendency of corporations to avoid calling attention to potential bad news for a company’s investors. As financial economist Michael C. Jensen observed, corporate reporting and market communications are often shaped by incentives to meet or beat market expectations rather than to present a full account of risk. Former SEC Chairman Arthur Levitt similarly warned in 1998 that the drive to satisfy earnings expectations could displace faithful representation with “a game of nods and winks.” That concern remains salient today.

The Commission’s own staff has recognized this tendency by examining whether information conveyed in press releases, conference calls, investor presentations, sustainability reports, or other non-filed communications appears to reveal material information omitted from SEC filings.

In our experience, shareholder engagement and proposals seeking additional voluntary disclosure often lead directly to additional internal measurement, analysis, and board-level attention. Once a company begins developing metrics for public disclosure, it will naturally scrutinize the underlying issue more closely. That scrutiny, in turn, prompts management to assess more closely whether the issue constitutes a material risk requiring disclosure under Regulation S-K, and whether the disclosures are complete enough to avail the firm of a safe harbor. Although management and shareholders may initially diverge in their assessment of a risk’s significance, this disclosure ecosystem helps prompt critical evaluation of the differing perspectives. In this way, the market self-identifies and defines emerging and potentially material risks through iterative engagement between companies and their investors as risks emerge and ripen.

Disclosures help investors engaged in active stewardship to assess whether management has identified and is actively managing risks that could affect long-term financial performance, to evaluate whether the company’s risk oversight framework is commensurate with its risk exposure, and to determine whether further engagement or escalation through the proxy process may be warranted. The disclosures are also a baseline against which to assess the need to file shareholder proposals requesting enhanced reporting or management action on identified risks.

Several recent shareholder proposals illustrate how Rule 14a-8 helps surface potentially material risks which ultimately interplay with companies’ Regulation S-K disclosures.

Artificial intelligence and emerging risks. AI-related shareholder proposals at U.S. companies have increased significantly in number, scope, and ambition between 2022 and 2025, driven by investor demand for transparency regarding the related risks and opportunities.

In 2025, investors filed proposals at Alphabet and Amazon seeking greater transparency regarding the water and energy demands associated with AI infrastructure. A similar proposal at Salesforce preceded the company’s launch of a dedicated water program as part of its updated sustainability strategy.

In 2024, shareholders at Meta and Alphabet filed proposals requesting annual reporting on the risks posed by generative AI, including misinformation and broader societal harms; the proposal received 56.3% support from Meta’s independent shareholders and 45.7% of the independent vote at Alphabet. Similarly, at Apple in 2024, shareholders filed a proposal seeking greater transparency regarding the company’s use of AI and its ethical guidelines, which received 37.5% support of votes cast.

Online child safety. In 2024, faith-based investors co-filed a proposal at Meta requesting annual reporting on child safety risks, including cyberbullying and mental health harms to young users. The proposal received 59.1% support from independent shareholders. Similar proposals have occurred at Alphabet and Apple, reflecting broad investor concern. This risk has materialized in recent litigation. In March 2026, a $6 million jury verdict was issued against Alphabet and Meta in a lawsuit in which a young woman alleged that negligent platform design contributed to her addiction to social media and resulting mental health harms. Additional lawsuits raising similar allegations are currently pending.

Opioid crisis oversight. In 2020, the Illinois State Treasurer co-filed a proposal at Johnson & Johnson requesting review of opioid-related risks. The proposal received 60.9% support. Similar proposals were filed at McKesson, AmerisourceBergen, and CVS Health. These proposals anticipated risks that later proved financially and operationally significant, including the $26 billion opioid legal settlements reached by these companies in 2022.

Worker safety. In 2022, shareholders at Amazon filed a proposal requesting an independent audit of working conditions, citing injury rates reportedly well above the national average. The proposal received 44% support. Amazon has since been the subject of a class action lawsuit concerning its treatment of workers with disabilities and in 2025 reached a settlement with the U.S. Department of Labor following a multi-site Occupational Safety and Health Administration investigation and resulting cases concerning hazardous working conditions. Similar proposals have been filed at Walmart and other issuers, highlighting investor concern that workplace safety failures can create material operational, legal, and reputational risk.

We are aware that the SEC has been urged to reconsider its rules governing environmental and social shareholder proposals, such as in the December 2025 White House executive order on ESG and DEI. However, the shareholder proposal process is one of the principal mechanisms through which investors communicate and escalate their information needs and emerging risk concerns to portfolio companies. Constraining the subject matter of Rule 14a-8 proposals to eliminate environmental or social issues, which often emerge as material risks, would pose substantial harm to the market by disrupting the channels for improved disclosure. Curtailing the ability of shareholders to file proposals on any topics relevant to their companies would weaken the ecosystem of disclosure that includes Regulation S-K.

Moreover, we believe that it is appropriate for the Commission to strengthen and clarify the relationship between Rule 14a-8 and S-K. For example, the Commission can clarify that substantial support for a shareholder proposal (for instance, above 20% voting support) may constitute evidence of materiality of the related issue for purposes of Regulation S-K disclosure. The Commission can also make clear that while voluntary sustainability reports, CDP responses, and other ESG-specific disclosures do not substitute for Regulation S-K risk factor disclosure, it can be appropriate for voluntarily reported and formatted ESG information to be included in Commission mandated filings under Reg S-K without substantial additional formatting.

Read the full comment letter submitted by SRG here for a comprehensive analysis of these issues.