Print

PrintEleanor Viney is an Analyst, Neil McCarthy is Co-Founder and Chief Product Officer, and Emily Drazan Chapman is a Legal AI Architect at DragonGC. This post is based on their DragonGC memorandum.

Executive Summary

The Environmental, Social, and Governance (“ESG”) framework, once a dominant feature across corporate governance and sustainable finance, has declined in prominence, retreating from both corporate disclosures and investor focus. This report quantifies that retreat through two lenses: (1) the elimination and re-branding of ESG terminology in S&P 500 and Fortune 1000 DEF 14A proxy and Form 10-K filings, and (2) the sustained capital exodus from ESG-designated mutual funds and ETFs. Together, these illuminate the impact of recent regulatory, political, and market developments on the ESG framework, indicating that the tides are turning against ESG narratives as well as ESG investment.

ESG Disclosures

At the disclosure level, aggregate “sustainability” keyword mentions in S&P 500 DEF 14A proxy filings peaked in 2024 and registered their first decline in 2025. Analysis of recent 2026 proxy filings indicates that the ESG narrative decline is accelerating. Target Corporation’s proxy record offers compelling insight into the nuances of this “greenhushing” trend. Yet, in the “Item 1A. Risk Factors” section of annual 10-K filings, the use of the term “sustainability” continues to grow at the aggregate index level, indicating continued awareness and monitoring of sustainability risks among large corporations.

Capital Flows

DragonGC analysis of data published by the Investment Company Institute (ICI) quantifies waning investor backing of ESG investment. ESG-designated funds recorded a net outflow of $935 million in January 2026, the fourteenth consecutive month of negative flows. The number of ESG funds has contracted by 100 since January 2025. Total AUM of $629 billion reflects market appreciation on existing positions, not new investor conviction.

The narrative decline and capital retreat are synchronized responses to the same regulatory pressure: anti-ESG state legislation, pension fund divestment mandates, and an emerging judicial framework characterizing ESG mandates as exhibiting “unconstitutional vagueness” in fiduciary contexts. The once-roaring ESG tidal wave has ebbed.

Section I: Trends in ESG Disclosures

Industry-Wide Proxy Disclosure Data

Analysis of S&P 500 and Fortune 1000 DEF 14A proxy filings and Form 10-K filings from 2010 through 2026 reveals distinct but related dimensions of the shifting disclosure landscape.[1] The frequency of the term “sustainability” is used here as a metric for quantifying the trends in ESG disclosures across DEF 14A proxy filings and Form 10-K filings since 2010.

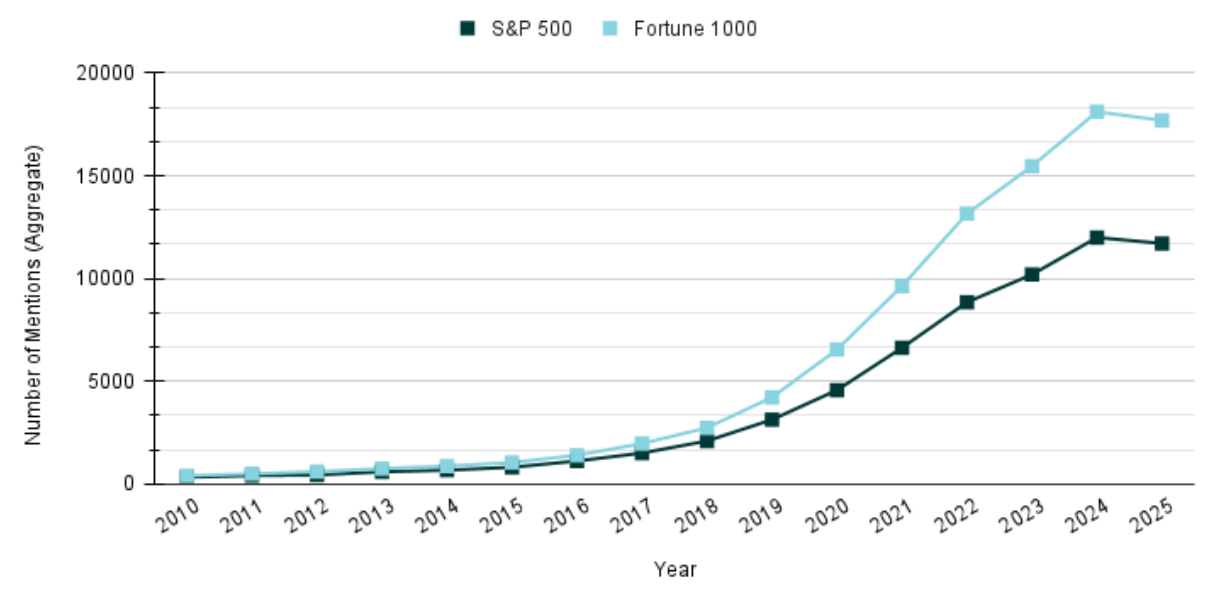

Chart 1 — DEF 14A Proxy Filings: “Sustainability” Keyword Count (2010-2025)

Source: S&P 500 / Fortune 1000 DEF 14A Proxy filings (SEC), 2010-2026. Aggregate raw keyword counts of “sustainability” across all constituent filings.

Chart 1 captures the full arc of sustainability disclosure expansion and its first inflection point. Both the S&P 500 and Fortune 1000 series followed an uninterrupted growth trajectory from 2010 through 2024, showing significant growth beginning around 2020. During this period, ESG disclosures ballooned in a favorable political and regulatory landscape. The 2025 decline is modest in absolute terms (−289 mentions for S&P 500; −413 for Fortune 1000) but significant nonetheless: it marks the reversal of a multi-year growth trend. This metric demonstrates the intense proliferation and subsequent contraction of ESG disclosures in DEF 14A proxy filings, driven primarily by concerns around recent anti-ESG legislation. In aggregate, anti-ESG legislation has had a measurable impact, with companies responding to this pressure by “greenhushing”, or deemphasizing voluntary sustainability disclosures.

Fortune 1000 consistently runs ~1.5× the S&P 500 count, reflecting the larger population (1,000 vs. ~500 companies), but the ratio is stable across years, indicating proportional adoption across both groups. The 2024 peak and 2025 modest decline is simultaneous across both indices, suggesting a collective response to political and regulatory pressure. Yet, notably, sustainability mentions remained historically elevated in 2025, exceeding 2023 levels, indicating the retreat is in its early stages.

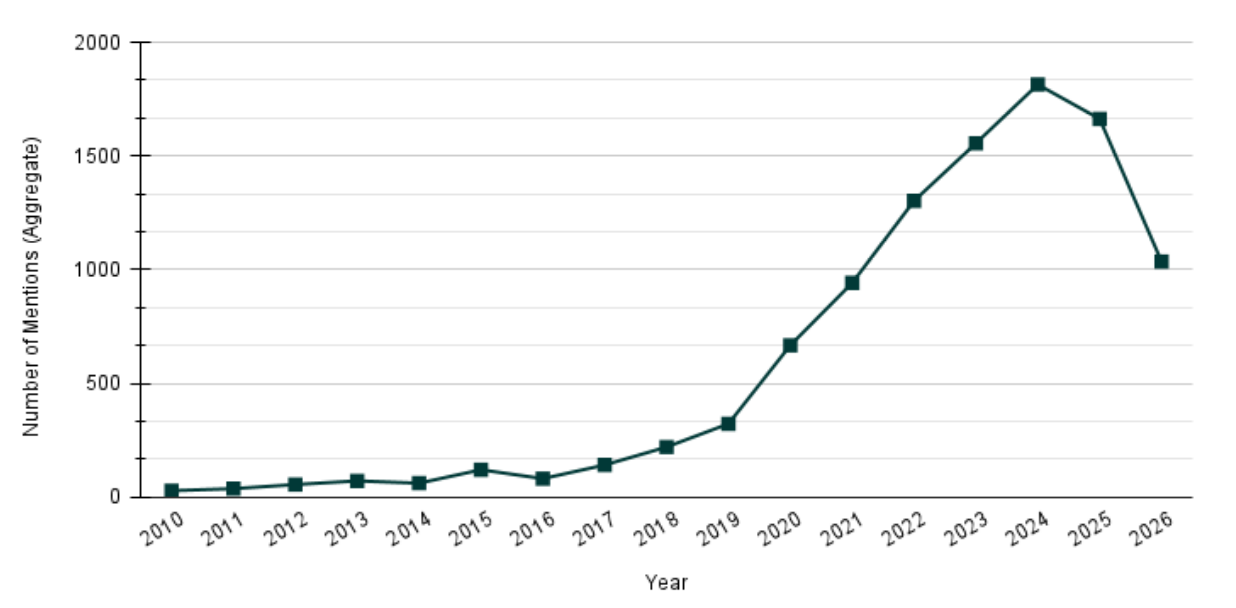

Chart 2 — DEF 14A Proxy Filings: “Sustainability” Keyword Count (2010-2026 YTD)

Source: Fortune 1000 DEF 14A proxy filings (SEC), 2010-2026. Aggregate raw keyword counts of “sustainability” across a subset of 50 Fortune 1000 companies that have filed DEF 14A proxy filings in Q1 2026.

Early analysis of 2026 DEF 14A proxy filings suggests a more dire outlook for ESG disclosures and provides the most current available signal on the disclosure trajectory for the present year. Data on a subset of Fortune 1000 companies (50 companies that have filed DEF 14A proxy statements so far in 2026) and their 2010-2026 DEF 14A filings indicate that, so far this year, the “sustainability” keyword count is declining more dramatically than in 2025, dropping below 2022 levels. The 2025 decline appears modest in comparison with this massive early 2026 ESG retreat, an emerging trend that suggests that anti-ESG regulation remains a potent force in shaping DEF 14A disclosures in this current proxy season.

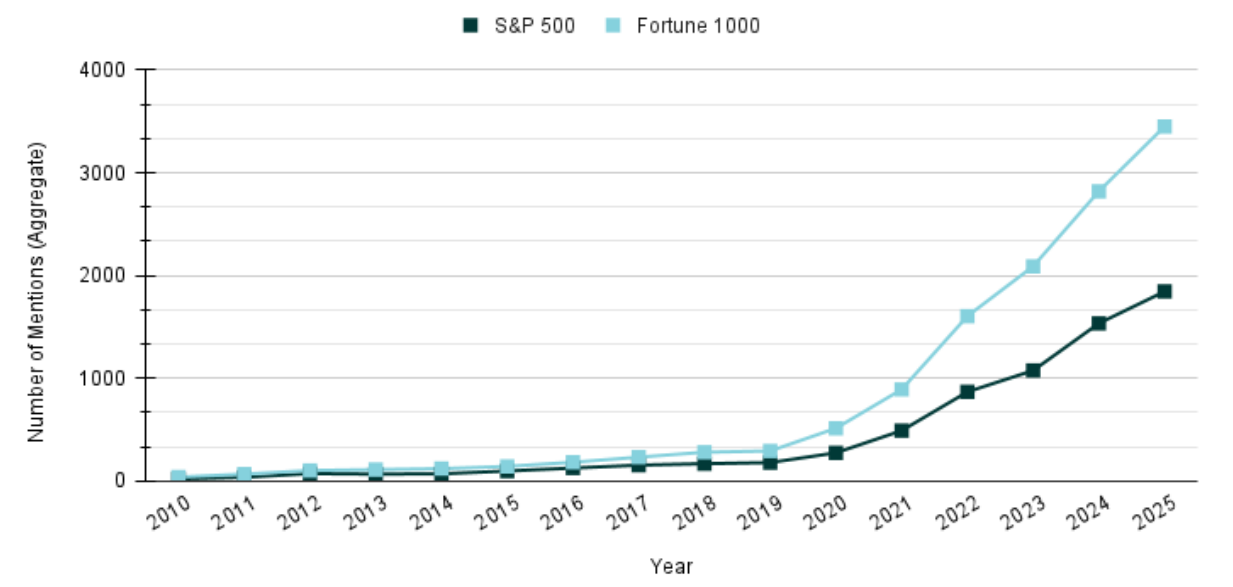

Chart 3 — Form 10-K Filings: “Sustainability” Keyword Count (2010-2025)

Source: S&P 500 / Fortune 1000 Form 10-K filings (SEC), 2010-2026. Aggregate raw keyword counts of “sustainability” in the “Item 1A. Risk Factors” section across all constituent filings.

Turning to Form 10-K filings offers a more nuanced view of ESG disclosures in public company filings. Even as voluntary ESG disclosures are declining across DEF 14A proxy filings, companies are increasingly attuned to “sustainability” as a key “risk factor”. Keyword counts of “sustainability”, specifically in the “Item 1A. Risk Factors” section of Form 10-K filings, have grown continually from 2010 to 2025 for both S&P 500 and Fortune 1000 companies, with significant gains beginning around 2020. The DEF 14A growth trend is reflected here, though 10-K disclosures diverged in 2025, continuing to increase as proxy disclosures contracted. As such, it is clear that “sustainability” remains (increasingly so) on companies’ radars, though notably as risk to be monitored, disclosed, and managed for the sake of liability management. Indeed, removing “sustainability” from the Risk Factors section could leave companies vulnerable to potential litigation in the event of investor losses. Different legal and regulatory pressure dominates here.

Case Study: Target Corporation — ESG Decline in Action

Target Corporation’s proxy statement record from 2021 to 2025 offers a more granular and particularly insightful view of the ESG narrative retreat in DEF 14A proxy filings. Target progressed from minimal disclosure in 2021 through peak ESG branding in 2023 to complete ESG elimination in 2025 within four proxy cycles.

Target Corp: ESG & Sustainability Proxy Mention Counts (2021-2025)

Sources: Target Corporation DEF 14A filings, 2021-2025. U.S. SEC EDGAR. See footnotes 4-8 for year-specific URLs

In two proxy cycles (2023→2025), Target eliminated 100% of explicit ESG mentions (62 → 0), reduced sustainability mentions by 7% (70 → 65, elevated due to the name “Governance & Sustainability Committee”), removed references to its “Target Forward” strategic sustainability initiative, and reframed its director skills criterion from “ESG Understanding” (2022) to “Environmental, social, and governance” (2024) and most recently to “Sustainability and governance” (2025), progressively de-emphasizing ESG and refocusing on risk oversight and shareholder value creation.

2021: Baseline Governance Disclosure

The 2021 proxy contained 1 mention of “sustainability” and 12 mentions of “ESG,” confined exclusively to the Board’s Risk Oversight section.[2] ESG was a compliance and risk function, not a strategic identity.

2022: Peak ESG Integration and Strategic Branding

The 2022 proxy marked a key shift in Target’s ESG framing.[3] Mentions expanded to 49 (sustainability) and 46 (ESG), reflecting the launch of Target Forward and the rebranding of the Governance Committee to the “Governance & Sustainability Committee.” “ESG Understanding” was added as a board director skills criterion, and ESG shareholder engagement was formally documented.

2023: ESG Disclosure at Maximum Density

The 2023 proxy reached peak disclosure density: 70 sustainability mentions and 62 ESG mentions.[4] ESG skills were highlighted in individual director biographies. Target Forward goals, stakeholder engagement frameworks, and cross-committee ESG responsibility were fully documented. Target framed ESG as a core strategic and brand identity in this disclosure.

2024: ESG Term Excised; Strategic Reframing Begins

ESG re-branding began in the 2024 proxy, with Target favoring the language of “sustainability” over explicit “ESG” references.[5] “ESG” dropped from 62 to 2 mentions (both residual). The “Sustainability & ESG” section was renamed “Sustainability matters”, and sustainability was explicitly reframed as serving “long-term growth and value creation for our business and our shareholders.”

2025: Complete ESG Elimination and Resiliency Reframing

The 2025 proxy completed the rebranding initiative.[6] “ESG” appeared zero times, and most mentions of “sustainability” came from the name “Governance & Sustainability Committee”. Target Forward was deleted entirely. The “Sustainability matters” section was reduced to three sentences, with additional information relegated to a link on the Target website. The director skills criterion was renamed to “Sustainability and governance” with the definition rewritten to center on “business resiliency matters.” The Governance & Sustainability Committee’s sustainability mandate was redefined as “overall approach to resiliency in our business model”, a formulation from which environmental, social, or governance content is entirely absent. The shift from 2023 to the most recent filing in 2025 is stark, with large corporations like Target leading the ESG narrative retreat in corporate disclosures.

A review of the Target DEF 14A proxy filings between 2021 and 2025 reveals an unmistakable “U-turn” on ESG disclosures during this period. “Sustainability” began as a risk and compliance function in 2021, grew into a strategic and brand identifier in 2022 and 2023, and shrank back into an area of risk oversight across 2024 and 2025. Target also successfully rebranded “sustainability” away from environmental stewardship and “green” initiatives to a principle of long-term value creation and business resiliency.

The decline in and rebranding of ESG disclosures offers a partial view of the full impact of shifting sentiment toward ESG. The next section, which examines fund flow of dedicated ESG mutual funds and exchange-traded funds, enhances the assessment of this ESG retreat.

Section II: ESG Retreat in Numbers

Key Findings at a Glance

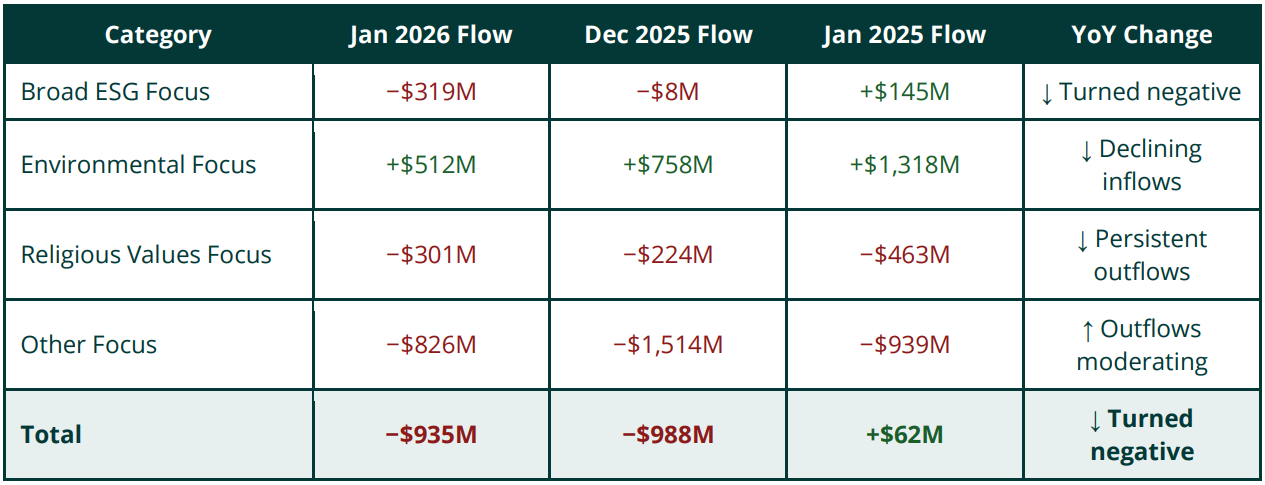

Source: Investment Company Institute (ICI), February 2026 release. Data as of January 2026.

Executive Overview

ESG mutual funds and exchange-traded funds are experiencing a sustained investor exodus that began in mid-2022 and has deepened markedly since the 2024 elections. According to DragonGC analysis of ICI data, funds investing according to environmental, social, and governance criteria recorded a net outflow of $935 million in January 2026, the fourteenth consecutive month of negative flows.[7] The number of ESG funds has dropped by 100 since January 2025, a contraction of 12%.

A critical analytical distinction must be made between total assets and fund flows. Total ESG fund assets have risen to $629 billion (+7.4% YoY), but this reflects equity market appreciation on existing holdings. The net flow figure is the key signal of investor sentiment, cutting through the buoyed total funds figure.

Rising total assets do not indicate investor enthusiasm. They suggest that investors who have not yet exited are sitting on unrealized paper gains. A fund can report record AUM while experiencing sustained outflows; the two metrics are disconnected once market appreciation is factored out. The $935M net outflow in January 2026 represents deliberate investor withdrawal.

Flow Reversal: From Expansion to Sustained Outflows

Between 2019 and early 2022, ESG funds were among the fastest-growing segments of the fund industry, driven by strong performance in ESG-heavy technology stocks and growing regulatory pressure to adopt sustainability frameworks.

That dynamic reversed sharply in mid-2022 when rising interest rates hit growth stocks hardest, stocks that dominate most ESG portfolios. Political headwinds followed: Republican-led states began passing anti-ESG legislation, mandating pension fund asset withdrawals from major asset managers including BlackRock. By late 2022, monthly outflows had become the norm across dedicated ESG funds.

Monthly Net Flows by Category — January 2026

The ICI classifies ESG fund flows into four categories. Performance diverges greatly across segments:[8]

Monthly Net Flows by ESG Category ($M)

Figures in millions of dollars. Red = net outflows; green = net inflows. Source: ICI, February 2026 release.

Broad ESG focus: “These funds focus broadly on ESG matters. They consider all three elements of ESG (rather than focusing on one or two of the considerations) or may include ESG in their names. Index funds in this group may track a socially responsible index such as the MSCI KLD 400 Social Index.”

Environmental focus: “These funds focus more narrowly on environmental matters. They may include terms such as alternative energy, climate change, clean energy, environmental solutions, or low carbon in their principal investment strategies or fund names.”

Religious values focus: “These funds invest in accordance with specific religious values.”

Other focus: “These funds focus more narrowly on some combination of environmental, social, and/or governance elements, but not all three. They often negatively screen to eliminate certain types of investments.”

Most notable is the turnaround in Broad ESG Focus funds: a $319M outflow in January 2026 compared with a $145M inflow one year prior, a $464M swing in twelve months. The most resilient category is Environmental Focus, sustaining net inflows at $512M, though declining sharply from $1.318B one year prior.

Environmental Focus funds have maintained positive net inflows through every month of the 14-month outflow streak that has plagued the broader ESG investment category. This growth is likely driven by the strong performance of clean energy and climate solutions equities, creating a performance-driven investor base less sensitive to political ESG retreat. Yet, inflows are declining rapidly ($1.318B to $758M to $512M over three months). If the ICI’s “Environmental Focus” sub-category enters a period of sustained outflow, it signals that even climate-focused investing is not immune from political forces.

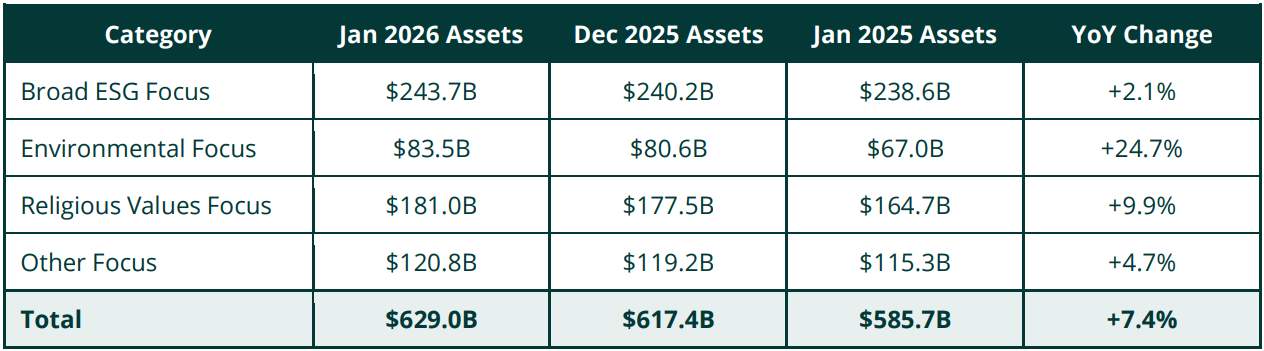

Total Assets: Market Appreciation as Headline Distortion

Total ESG Fund Assets by Category ($B)

Figures in billions of dollars. Source: ICI, February 2026 release.[1]

The Environmental Focus category (smallest in absolute AUM at $83.5B) displayed the highest YoY asset growth at +24.7%, driven by the aforementioned strong performance of clean energy equities. The Broad ESG Focus category grew by only 2.1%, the lowest of any category and barely ahead of inflation, reflecting both sustained outflows and an equity composition underperforming the broader market.

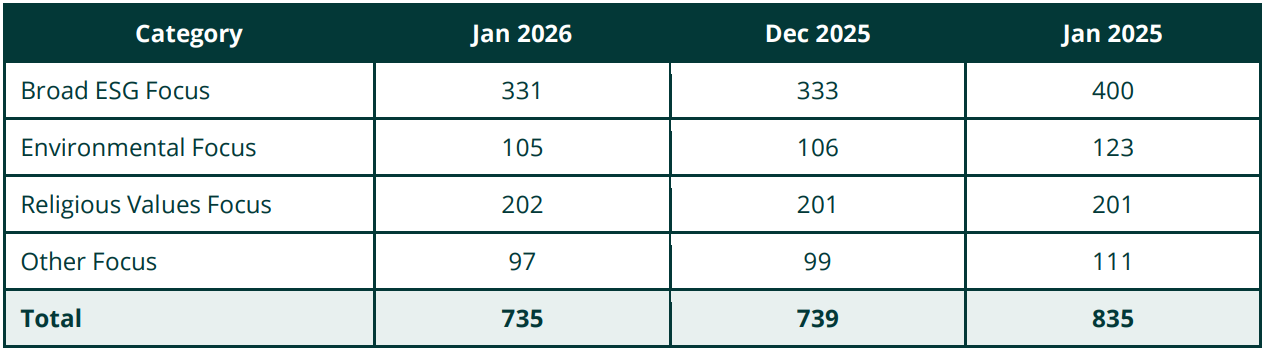

Fund Count Contraction: Further Evidence of Retreat

ESG Fund Count by Category

Source: ICI, February 2026 release.[1]

The Broad ESG Focus category has shed 69 funds, more than one-fifth of its January 2025 total. Total fund count has declined from 835 to 735 (−12% YoY). This structural contraction represents deliberate retreat from ESG investment by fund sponsors.

Fund count contraction is a leading indicator of sustained capital retreat. The closure of 100 ESG-labeled funds in 12 months, concentrated in the Broad ESG Focus category (−69 funds, −17%), signals that fund sponsors have concluded that the ESG label will not attract sufficient flows to sustain minimum viable fund economics.

Methodology & Source Attribution

All fund flow data was sourced from the Investment Company Institute (ICI) January monthly reports on ESG investing data, with analysis performed by DragonGC.

Fund flow data represent net new cash flow (purchases minus redemptions) excluding market

appreciation effects.

Conclusion

Retreat across Language and Capital

The data analyzed in this report confirm that anti-ESG sentiment is causing a retreat from the ESG framework at the level of corporate disclosure language and investor capital allocation. ESG disclosures, quantified by keyword counts of “sustainability”, decreased in 2025, and the early 2026 data are forecasting a more precipitous decline for the upcoming proxy season. Target Corporation’s proxy disclosures from 2021 to 2025 showed in detail the ESG decline and rebranding. At the same time, major asset managers have closed or repurposed 100 ESG-labeled funds in twelve months, and capital outflows plague the investment category.

Retreat Driven by the Shifting Regulatory Landscape

The common driver is identifiable: a hostile regulatory environment that has assigned material legal, reputational, and fiduciary risk to ESG positioning.

At the state level: anti-ESG legislation passed in more than 20 states has created enforceable prohibitions on state pension fund allocations to managers deemed to prioritize ESG factors over financial returns. Boycott lists targeting BlackRock, Vanguard, and State Street have produced documented pension fund withdrawals, disincentivizing ESG investment.

At the federal judicial level: an emerging line of 2025-2026 cases has tested ESG-related mandates under a doctrine of “unconstitutional vagueness”, arguing that ESG criteria, lacking objective definition, cannot constitute a legally enforceable fiduciary standard. While no controlling circuit precedent has yet emerged, the litigation risk is sufficient to motivate preemptive re-branding. Corporate legal functions are advising that explicit ESG commitments in governance documents may constitute admissions usable in derivative litigation or state enforcement actions.

At the federal regulatory level: rollback of the SEC’s climate disclosure rule has removed the compliance-driven incentive structure that sustained ESG adoption through 2023.

The ESG framework is not being totally abandoned in corporate disclosures; rather, it is being renamed and rebranded using non-ESG vocabulary. The capital markets evidence is less equivocal: investors are withdrawing from ESG-labeled products at a rate that cannot be explained by performance differentials alone. The ESG label has become a liability in political environments where institutional capital is subject to state oversight.

The complete publication is available here.

1Proxy and 10-K sustainability mention data compiled from S&P 500 and Fortune 1000 SEC filings. Raw keyword occurrence counts in annual proxy statements (DEF 14A) and annual reports (10-K) for each filing year 2010-2026(go back)

2Target Corporation, 2021 Proxy Statement (Form DEF 14A). https://www.sec.gov/Archives/edgar/data/27419/000130817921000258/ltgt2021_def14a.htm.(go back)

3Target Corporation, 2022 Proxy Statement (Form DEF 14A). https://www.sec.gov/Archives/edgar/data/27419/000130817922000265/ltgt2022_def14a.htm.(go back)

4Target Corporation, 2023 Proxy Statement (Form DEF 14A). https://www.sec.gov/ix?doc=/Archives/edgar/data/0000027419/000130817923000828/ltgt2023_def14a.htm.(go back)

5Target Corporation, 2024 Proxy Statement (Form DEF 14A). https://www.sec.gov/ix?doc=/Archives/edgar/data/0000027419/000130817924000626/ltgt2024_def14a.htm.(go back)

6Target Corporation, 2025 Proxy Statement (Form DEF 14A). https://www.sec.gov/ix?doc=/Archives/edgar/data/0000027419/000162828025020275/tgt-20250428.htm.(go back)

7Investment Company Institute (ICI), Monthly ESG Investing Data — January 2026 Release (February 27, 2026). Washington, DC. www.ici.org. Available at: https://www.ici.org/monthly-esg-investing-data.(go back)

8ICI, ibid. Fund flow data: net new cash flow (purchases minus redemptions), excluding market appreciation effects(go back)