Print

PrintMatteo Tonello is the Head of Data Benchmarking and Analytics at The Conference Board, Inc. This post is based on a report developed by The Conference Board in partnership with ESGAUGE, KPMG, Russell Reynolds, and the University of Delaware and authored by Ariane Marchis-Mouren, Senior Researcher, Corporate Governance at The Conference Board.

This report examines CEO/chair leadership structures in the S&P 500 and Russell 3000, focusing on succession events, chair independence, and related policy and rationale disclosures. Leadership structure remains context dependent, and most disclosures preserve board discretion to separate or combine the roles based on circumstances.

Trusted Insights for What’s Ahead®

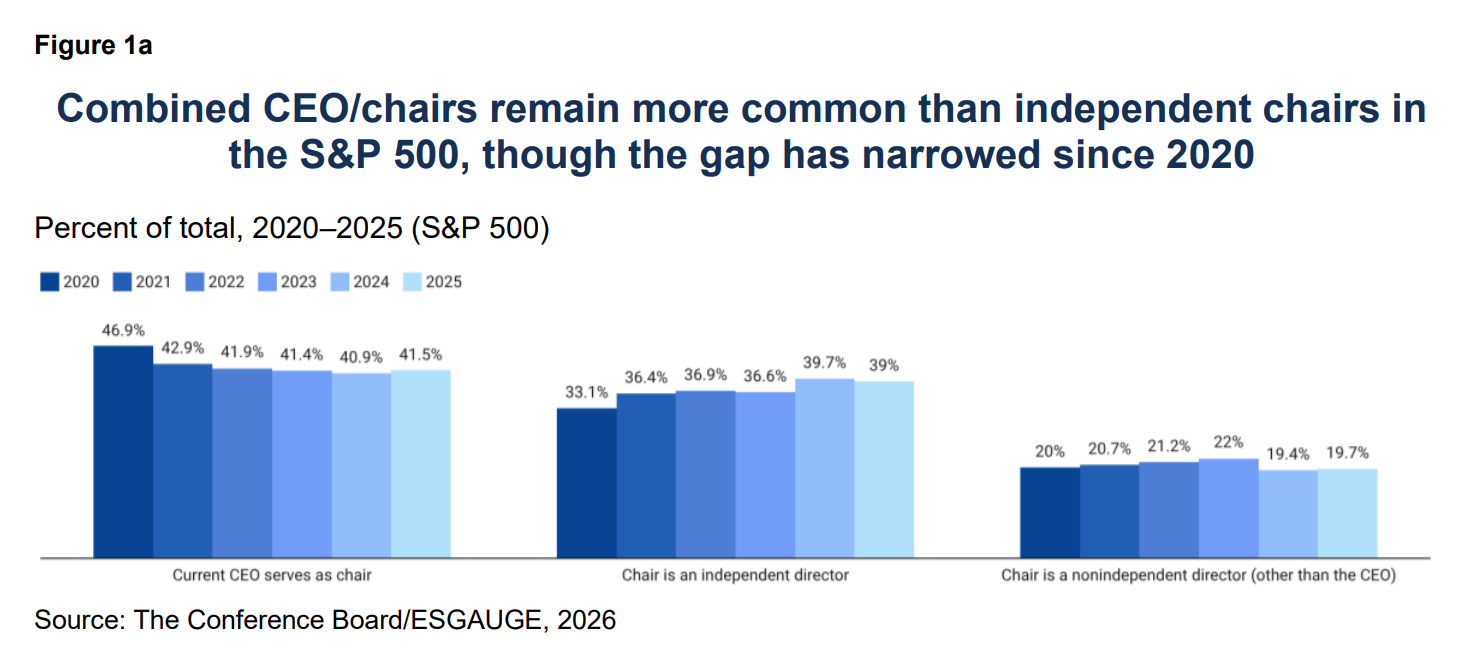

• Large-cap companies are more likely to have a combined CEO/chair. In 2025, the current CEO served as chair at 42% of S&P 500 companies, compared with 34% in the Russell 3000.

• Incoming CEOs are rarely elected board chair at the time of transition. In 2025, 3 of 65 CEO successions in the S&P 500 (4.6%) and 9 of 353 in the Russell 3000 (2.5%) involved the CEO being named board chair at the same time.

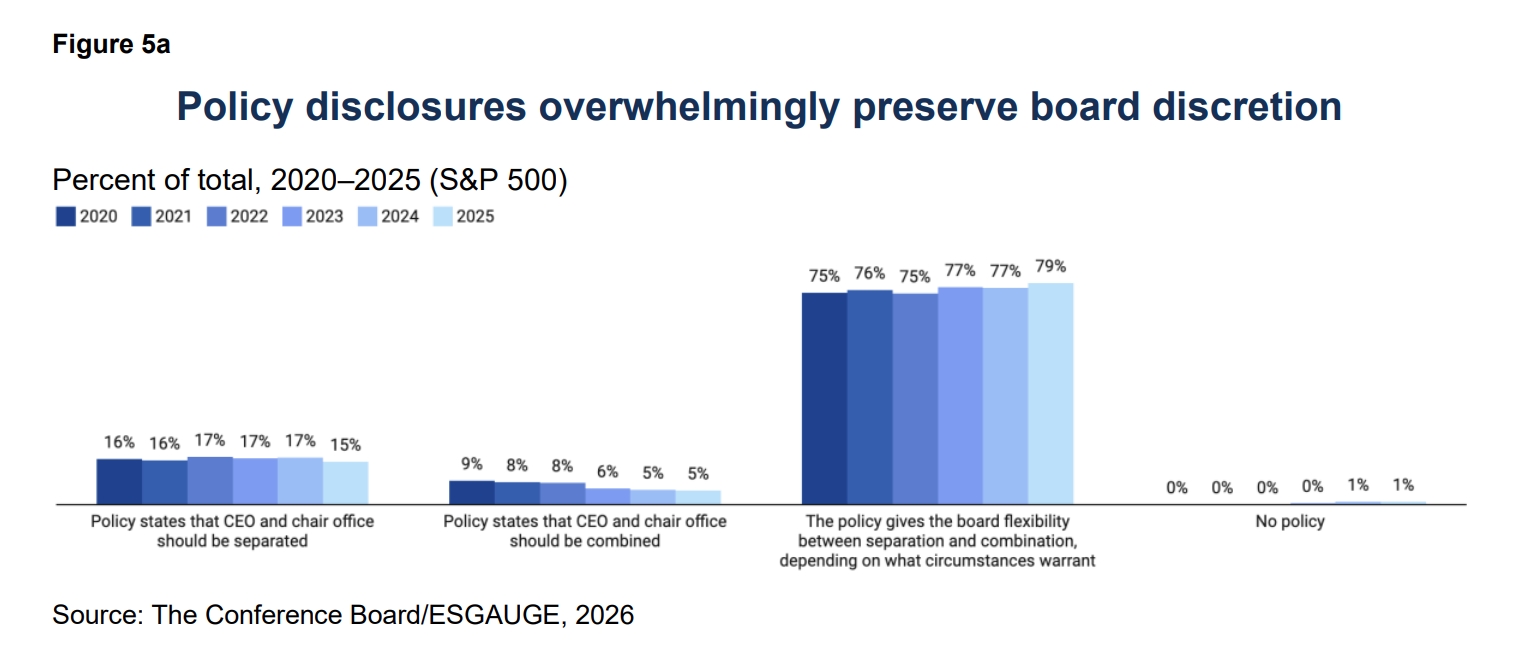

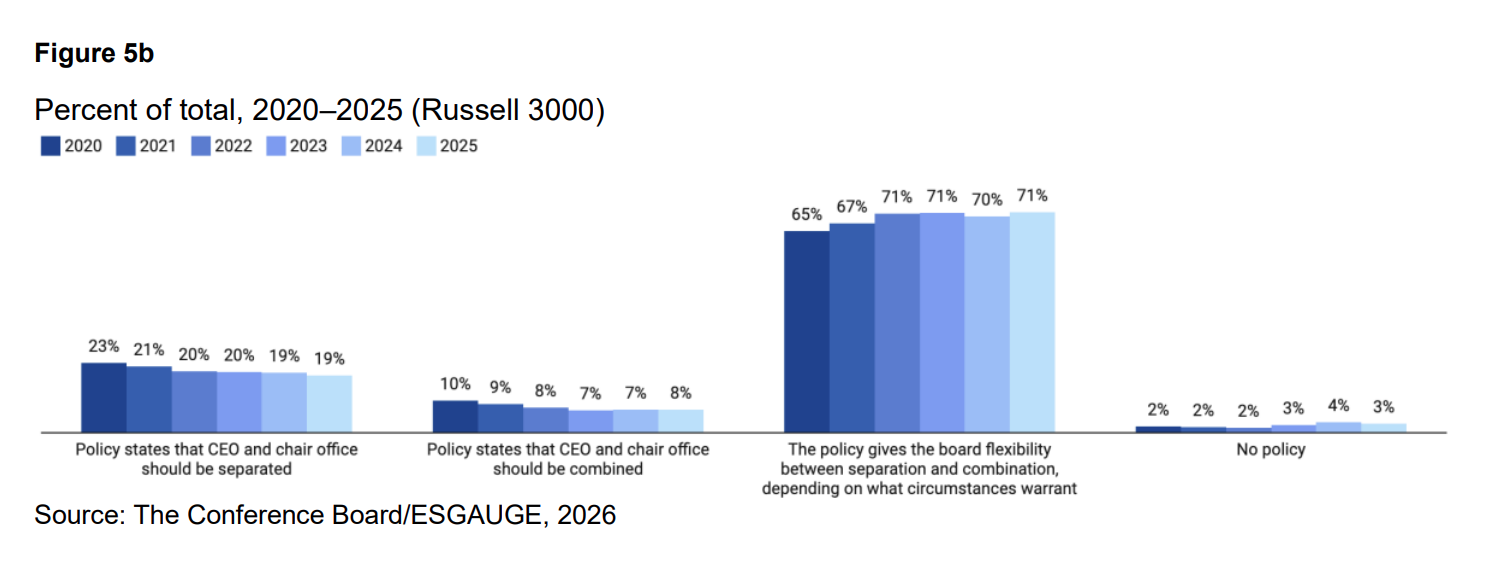

• Most companies disclose a policy that preserves board discretion. In 2025, 79% of S&P 500 companies and 71% of Russell 3000 companies disclosed policies giving the board flexibility to separate or combine the roles depending on circumstances.

• Disclosed rationales for leadership structure are evolving. For role separation, the most commonly disclosed rationale remains that the two positions have different responsibilities. For role combination, references to improved communication and strategic execution have increased, while mentions that the CEO is best suited to set the board agenda have declined.

• Proxy advisors and large institutional investors typically focus on independent board leadership (independent chair or strong lead independent director) and evaluate proposals to separate the chair and CEO roles case by case.

In practice, boards can use their regular performance evaluation processes—including assessments of the board, committees, and individual directors—to periodically test whether the chosen chair structure is enabling effective oversight and clear decision-making and to identify when changes may be warranted.

Over the past decade, combined CEO/chair roles have declined across major indexes and now represent less than half of chair roles, as independent chairs have increased. In assessing leadership structure, stakeholders commonly focus on whether independent board leadership is effective and clearly described, particularly where the roles are combined—and the rigor of the board’s evaluation and feedback processes is increasingly viewed as an important indicator of that effectiveness

Board Chair Independence and CEO Duality

Board leadership structures have gradually evolved since 2020, with a modest shift away from CEO duality and toward independent chairs. The pace and direction of change differ meaningfully between sectors, large-cap companies, and the broader market.

In the S&P 500, CEO duality declined from 47% in 2020 to 42% in 2025, while independent chairs increased from 33% to 39%. The share of companies chaired by a nonindependent director other than the CEO—often the founder or a former CEO—peaked at 22% in 2023 before reversing back to below 20%.

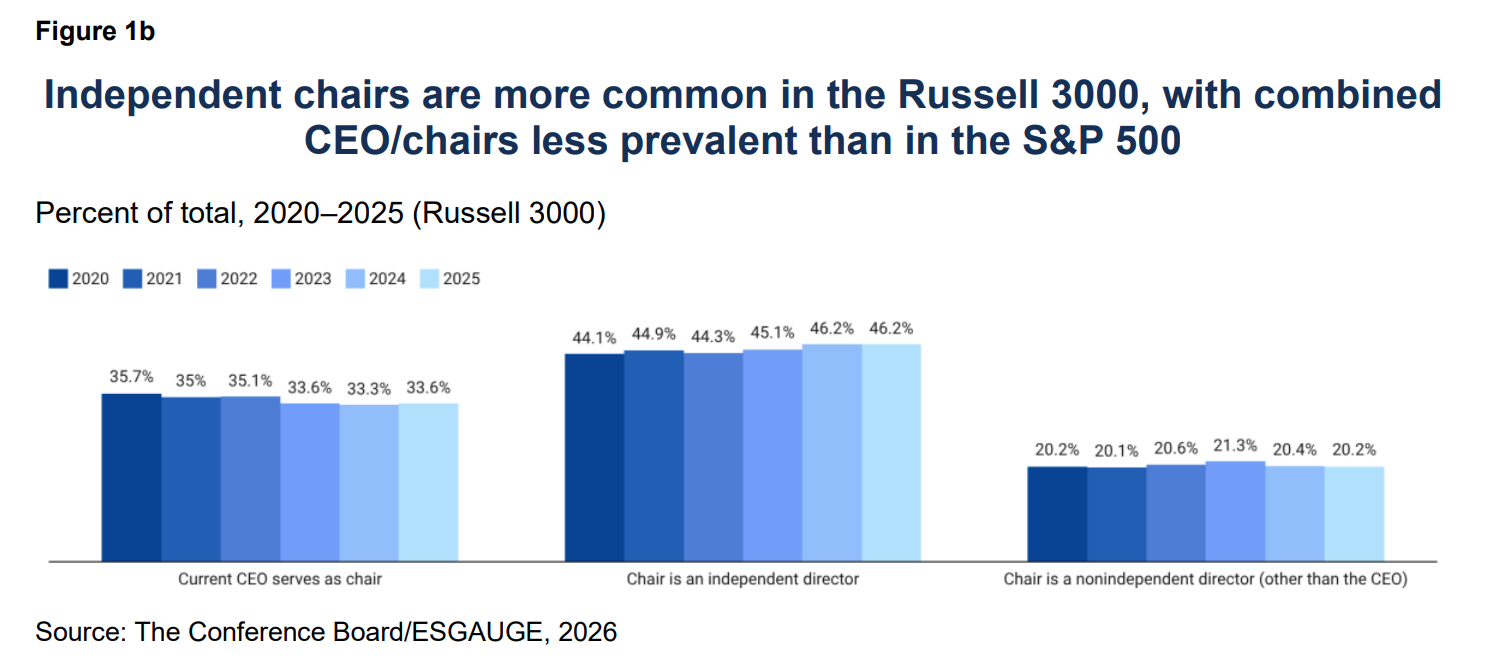

Among the companies in the Russell 3000, independent chairs remain the predominant model, and the gap versus combined CEO/chairs has widened modestly since 2020. As of 2025, over 46% of companies had an independent chair, compared with 34% chaired by the CEO and 20% chaired by another nonindependent director.

Differences between the indexes likely reflect a mix of company scale and investor expectations. Large-cap boards may be more likely to have CEO duality—often paired with a lead independent director and other oversight mechanisms—while the broader market more frequently adopts independent chairs as the default structure. In both indexes, boards appear to adjust chair arrangements episodically (such as around leadership transitions) rather than converging on a single model.

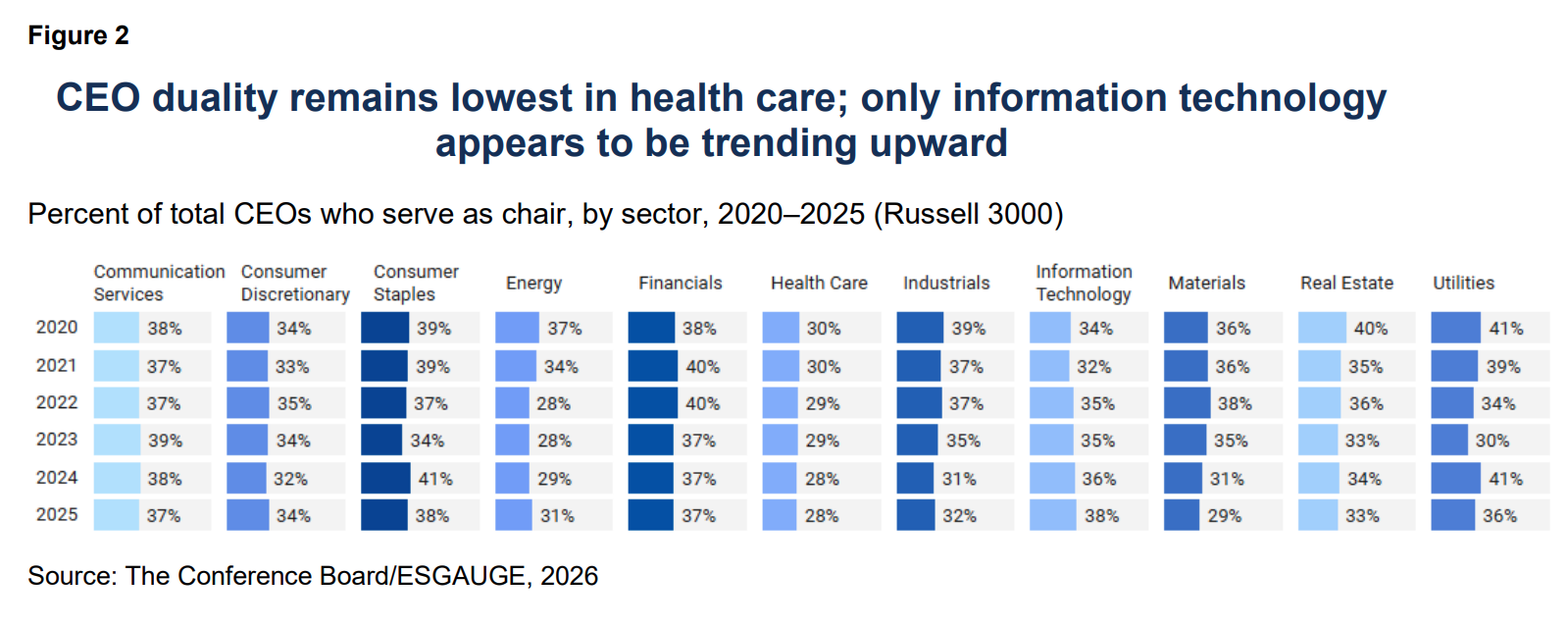

The widening separation between information technology and health care suggests that CEO duality is increasingly shaped by sector context rather than uniform convergence toward a single governance standard. Differences in ownership influence and leadership continuity—alongside sector-specific expectations for independent oversight—may help explain why role combination appears more durable in parts of technology while separation remains more common in health care.

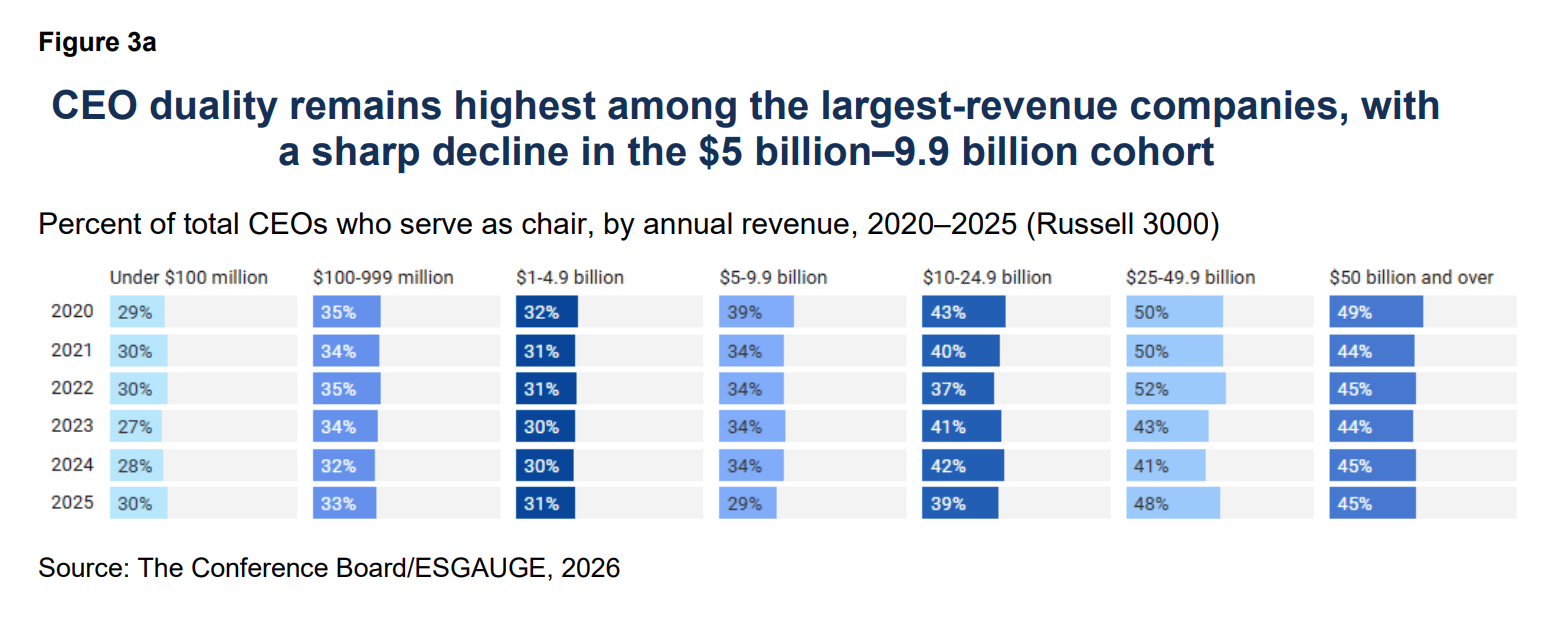

Across revenue cohorts, CEO duality remains most common among the largest companies, with the $25 billion–49.9 billion and $50 billion+ revenue groups in the mid-40% to near-50% range by 2025. The most notable shift occurs in the $5 billion–9.9 billion cohort, which declines markedly over the 2020-2025 period, while other revenue bands change more modestly and exhibit intermittent year-to-year movement.

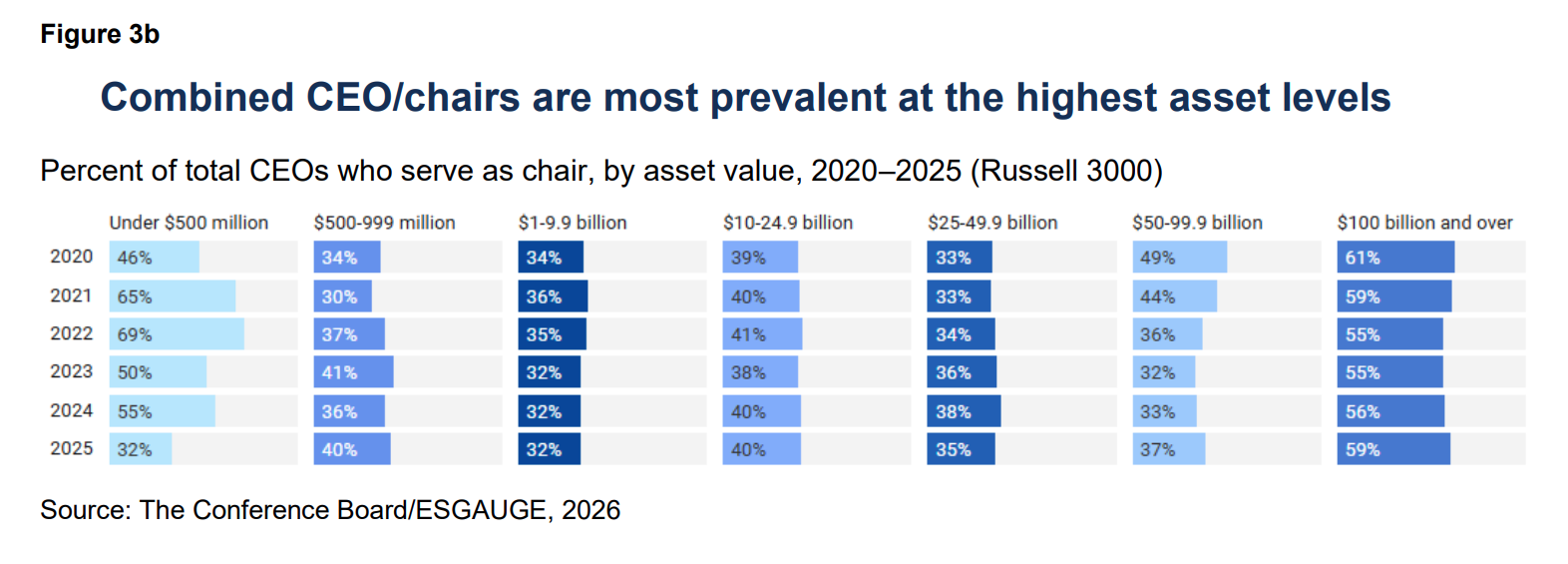

By asset value, the $100 billion+ cohort consistently shows the highest prevalence of combined CEO/chairs throughout the examined years. Over the same period, the $50 billion–99.9 billion cohort trends downward, while the smallest-asset cohort exhibits pronounced variability— suggesting sensitivity to smaller sample sizes.

Taken together, the revenue and asset profiles indicate that CEO duality is associated with scale but not uniform across all size bands. Variation across adjacent cohorts—and sharp movement in select groups—suggests that chair structure decisions may be event driven (CEO succession, founder transitions, governance reforms) rather than a steady function of company size.

CEO succession and joint CEO/chair elections

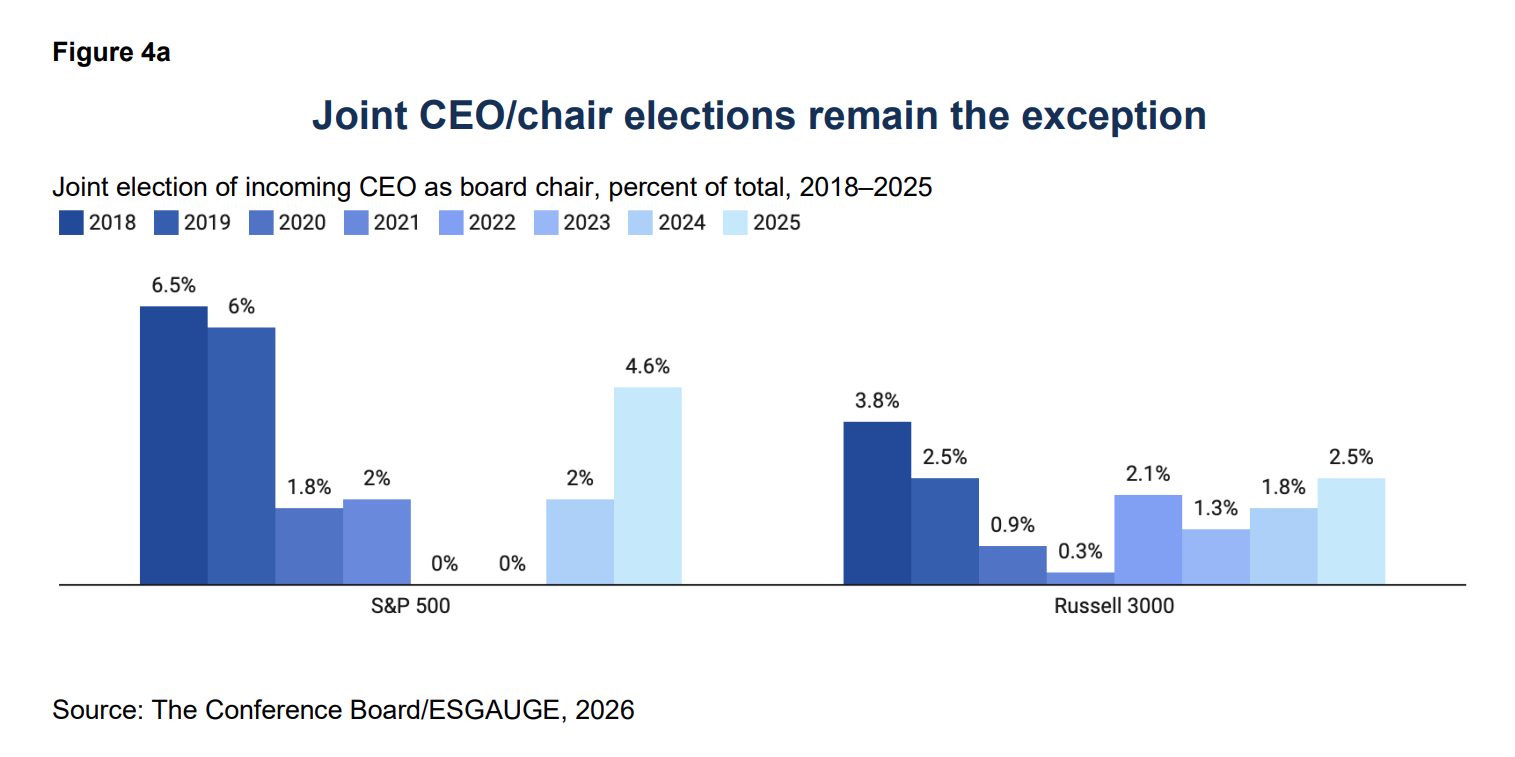

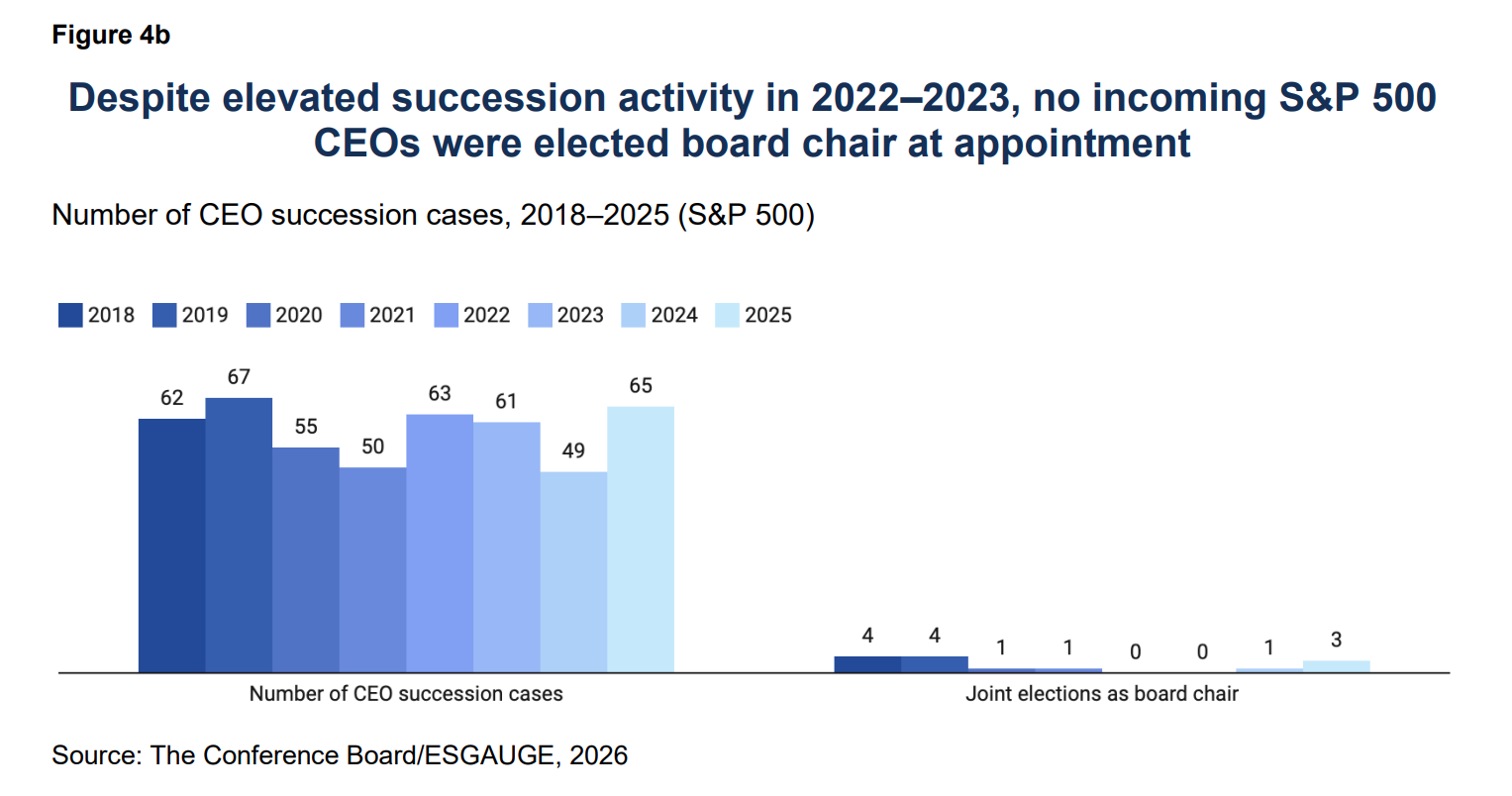

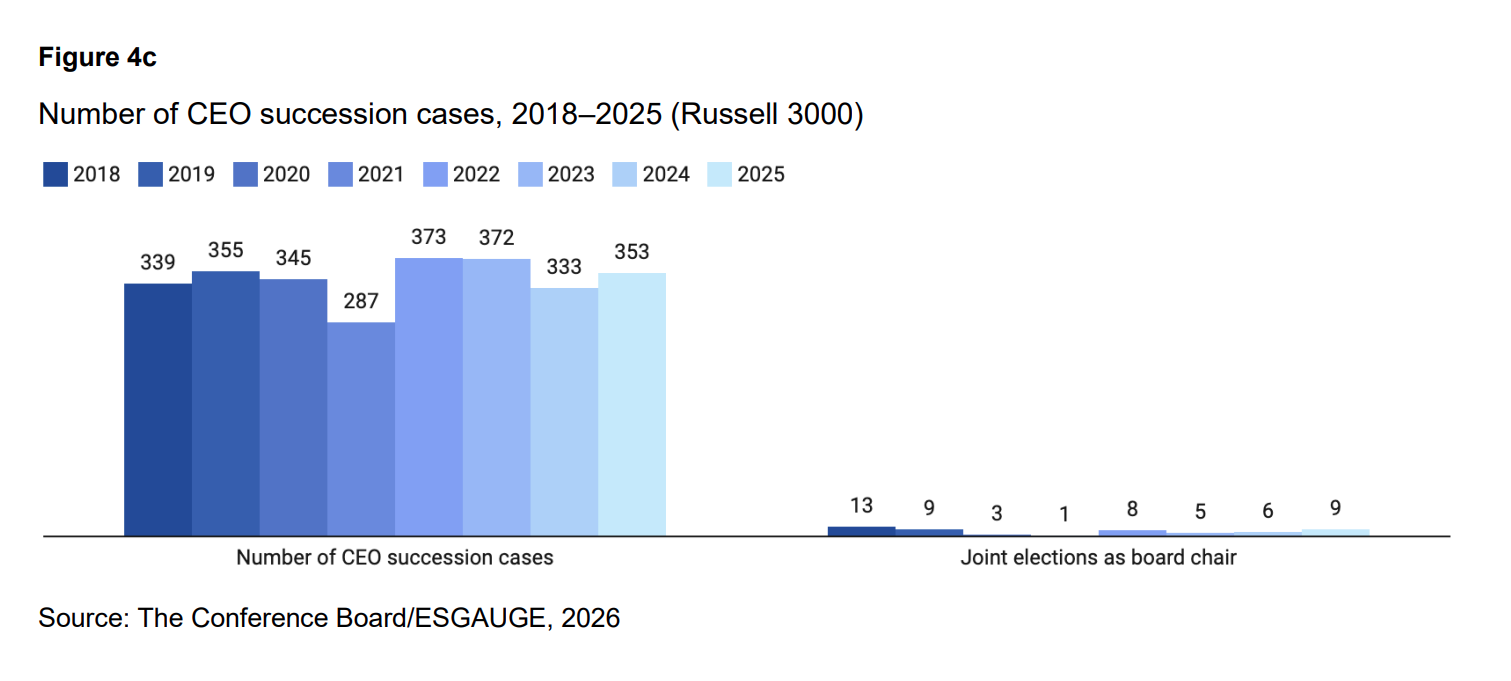

Across both the S&P 500 and Russell 3000, joint election of an incoming CEO as board chair remains the exception, accounting for about 3% of S&P 500 CEO successions and 2% of Russell 3000 CEO successions from 2018 to 2025.

In the S&P 500, the joint-election rate fell from 7% in 2018 to 0% in 2022 and 2023, before rising to 5% in 2025. In the Russell 3000, joint-election rates followed a similar pattern, dropping from 4% (2018) to 0% (2021) before increasing back to 3% in 2025.

In absolute terms, joint elections are limited relative to the number of CEO succession events. In 2025, S&P 500 companies reported 65 CEO succession cases and three joint elections, while Russell 3000 companies reported 353 CEO succession cases and nine joint elections.

CEO transitions are a practical moment to clarify how board leadership responsibilities will be handled during the transition period. Boards may also revisit leadership structure outside CEO transitions, including assigning (or separating) the chair role after a CEO has been in place, based on company circumstances and oversight considerations.

Policy approaches to combining and separating the CEO and chair roles

Companies’ governance policy disclosures continue to favor board discretion and avoid prescriptive statements. Among those that disclosed in 2025, 79% of S&P 500 companies and 71% of Russell 3000 companies indicated they had policies that give the board flexibility to separate or combine the roles depending on circumstances.

Explicit policies stating that the CEO and chair roles “should be combined” were relatively uncommon (5% of the S&P 500 and 8% of the Russell 3000 disclosing in 2025). Policies stating that the roles “should be separated” were also a minority (15% and 19%, respectively), underscoring that many boards preserve discretion while describing the considerations that may inform their leadership structure.

In practice, the predominance of flexibility policies places more weight on the quality of disclosure. Where policies emphasize board discretion, companies can strengthen clarity by describing the considerations the board weighs when deciding whether to separate or combine the roles.

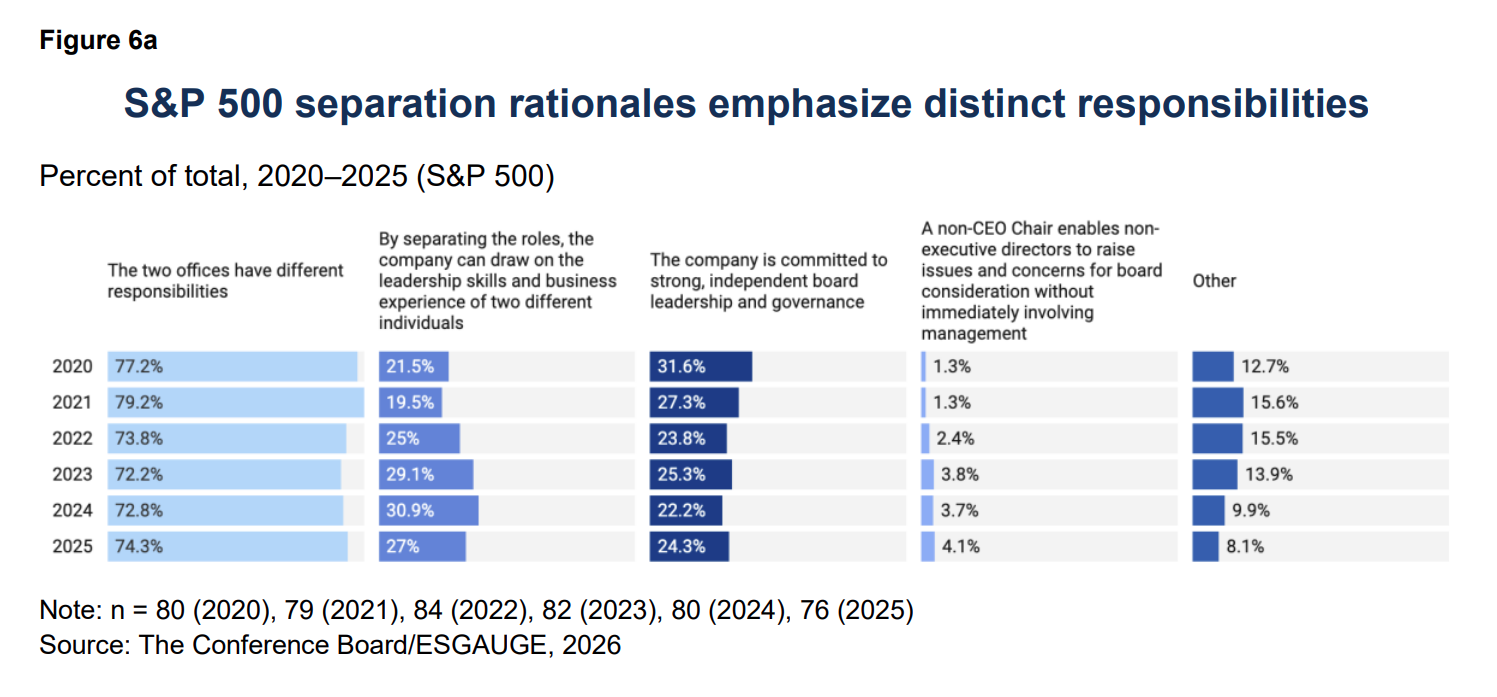

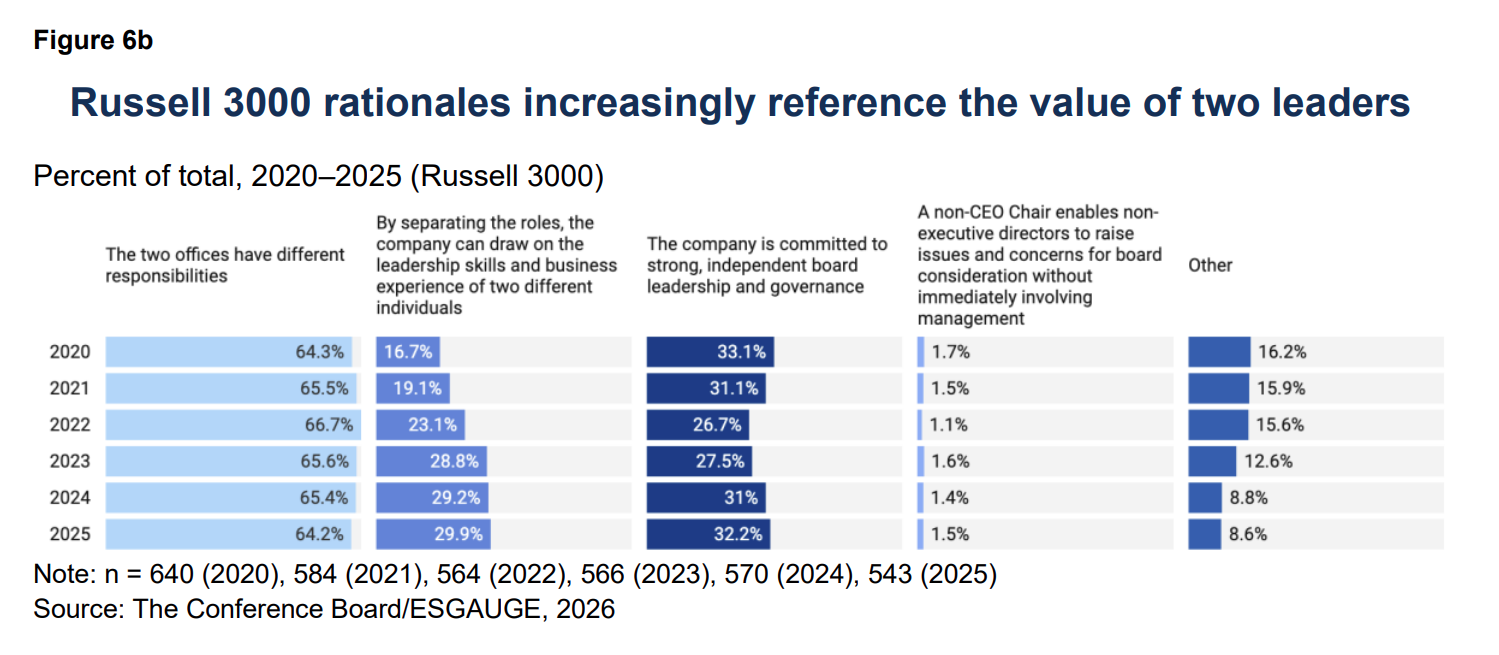

CEO/chair separation: rationale disclosure

Where companies disclose the rationale for separating the CEO and chair roles, the most frequently cited rationale continues to be that the two positions have different responsibilities. In 2025, this rationale was cited by 74% of S&P 500 companies and 64% of Russell 3000 companies.

Disclosures referencing the benefit of drawing on the leadership skills and business experience of two different individuals are more common than they were earlier in the decade. In 2025, this rationale was cited by 27% of S&P 500 companies and 30% of Russell 3000 companies. Meanwhile, “other” rationales declined over the period, suggesting increasing standardization in how companies describe the separation decision.

Separation disclosures remain anchored in role clarity, while references to the value of two leaders have increased. For boards, the practical takeaway is that disclosure tends to be most effective when it translates these themes into concrete governance outcomes, such as how responsibilities are allocated between management and the board and how independent oversight is organized.

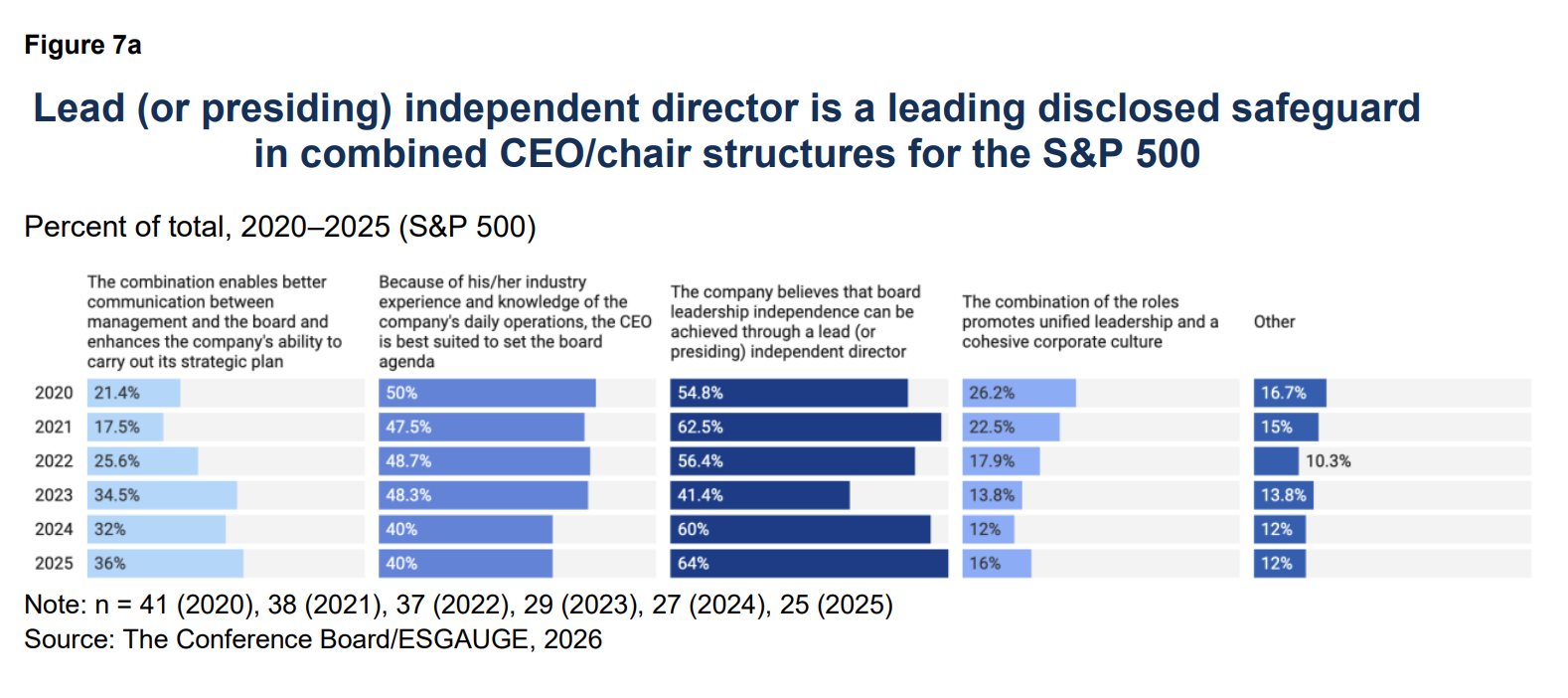

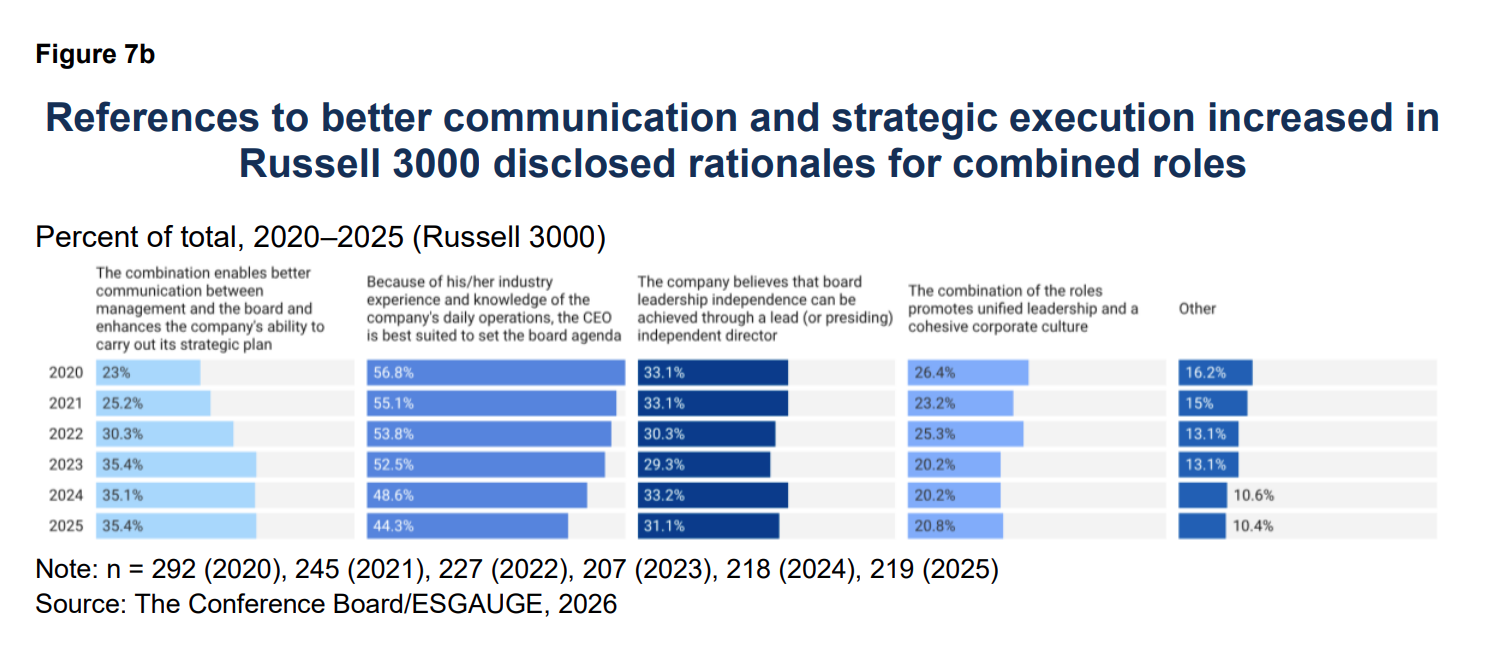

CEO/chair combination: rationale disclosure

When the CEO also serves as chair, the board typically demonstrates independent leadership through a clearly defined lead (or presiding) independent director role. Disclosures commonly describe lead independent director responsibilities such as presiding over executive sessions of independent directors, serving as a liaison between independent directors and the CEO/chair, providing input on board agendas and meeting schedules, and being available for shareholder engagement when appropriate. These features help clarify how independent directors organize oversight and board leadership within a combined CEO/chair structure.

Among companies that combine the CEO and chair roles and provide a rationale, disclosures commonly reference both leadership continuity and governance safeguards. In the S&P 500, citing a lead (or presiding) independent director as a mechanism to support board leadership independence was prevalent (64% in 2025), alongside industry experience and operational knowledge (40%), and references to improved communication between management and the board (36%).

In the Russell 3000, the most common rationale remained that the CEO is best suited to set the board agenda because of industry and knowledge of company operations (44% in 2025), although that rationale has declined since 2020 (57%). At the same time, references to improved communication and enhanced ability to execute strategy increased from 23% in 2020 to over 35% in 2025.

This pattern may reflect a shift in how companies describe the value of a combined structure, placing relatively more emphasis on board–management alignment and strategic execution than on CEO expertise alone. For boards, the shift underscores the importance of aligning the stated rationale with governance design in practice, including how agendas are set, how independent oversight is exercised, and how the lead (or presiding) independent director role is defined when the roles are combined.

Combination disclosures increasingly emphasize communication and strategic execution alongside governance safeguards. Institutional investors’ published voting frameworks frequently focus on whether independent leadership is clearly defined and empowered, including the scope of the lead (or presiding) independent director role and whether that role provides a meaningful counterbalance to and accountability for a combined CEO/chair.

Investor and proxy advisor perspectives on CEO/chair separation

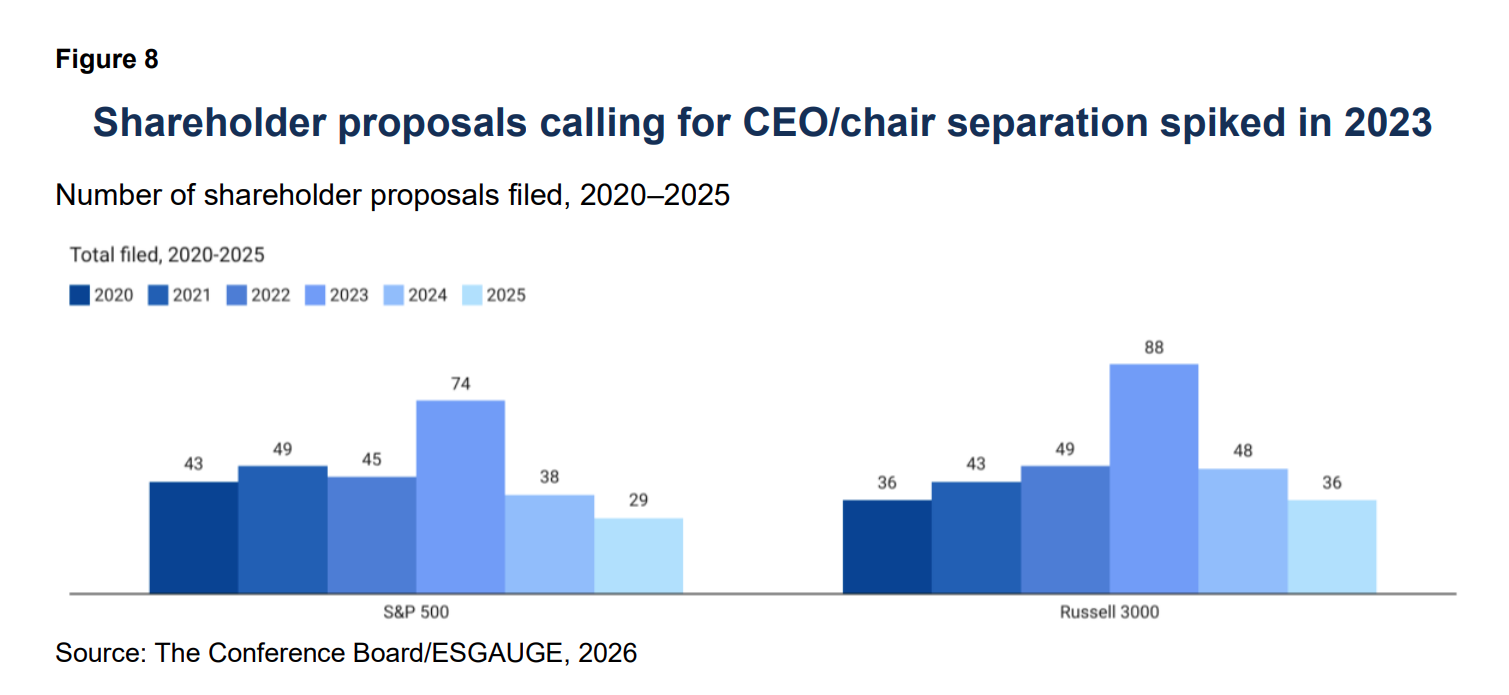

Shareholder proposals requesting that companies separate the chair and CEO roles rose sharply in 2023 and then declined in 2024 and 2025. More broadly, shareholder proposal volume across all topics also declined from 2024 to 2025, which may have contributed to lower filing levels in 2025. By contrast, average shareholder support was comparatively steady over the period, generally falling in the low-30% range year to year.

Despite the volume of filings, few proposals passed during the period highlighted—two in 2020 and one in 2021.

Proposal filings are concentrated in a few sectors, with financials (55 in the Russell 3000 from 2020 to 2025) and health care (52) accounting for the largest share of CEO/chair separation proposals, followed by industrials, consumer staples, and consumer discretionary. Other sectors, including energy and materials, appear less frequently. Overall, the sector mix indicates that proponents have focused on industries with a large population of widely held companies where board leadership structure may be a recurring governance issue.

Proponent activity is also concentrated among repeat filers, and many submissions follow a small set of recurring resolution formats. John Chevedden (105) and Kenneth Steiner (101) account for a substantial share of proposals, with average support generally in line with overall levels. Less frequent filers show greater variability in support, reinforcing that voting outcomes reflect company-specific circumstances and the way the request is framed—for example, an “independent chair when possible” policy versus more prescriptive separation language.

Independent chair proposals can draw significant attention despite the fact that they rarely achieve majority support. Boards can reduce ambiguity by meaningfully addressing CEO/chair structure directly in the proxy narrative, including the board’s rationale and the specific independent leadership features in place (independent chair or clearly defined lead independent director).

- Vanguard’s US proxy voting policy states that independent board leadership can take the form of an independent chair or a lead independent director with robust authority. It generally recommends votes against shareholder proposals to separate the CEO and chair roles, while noting it may support such proposals if there are significant concerns about board independence or effectiveness.

- BlackRock’s US benchmark voting guidelines similarly emphasize independent board leadership but defer to boards on leadership structure in the absence of significant governance concerns. It does not typically support separation proposals, with support more likely in cases of overarching and sustained governance concerns.

- ISS generally supports shareholder proposals requiring an independent board chair, while considering factors such as the proposal’s scope and rationale, as well as the company’s current leadership structure, governance practices, and performance.

- Glass Lewis evaluates these proposals case by case, generally supporting those it views as well crafted, but may recommend against overly prescriptive independence definitions or proposals where the company presents a compelling case for combining the roles and demonstrates effective independent leadership (or indicates an intent to separate the roles) alongside strong performance and governance provisions

Conclusion

Boards generally view the CEO/chair structure as a governance decision that may evolve over time and is often revisited during leadership transitions and other inflection points. Whether the roles are combined or separated, boards are expected to show effective independent oversight and clear disclosure of their rationale for the chosen leadership structure.

CEO/chair structure remains an area where expectations are shaped by governance or sector context rather than a single market standard. Looking ahead, boards can strengthen confidence in their approach by reassessing the leadership model as circumstances evolve (including through the board’s regular performance evaluation process and during CEO transitions), clearly defining independent leadership authorities (independent chair or lead independent director), and ensuring that proxy disclosures explains how the structure supports board oversight, decision-making, and accountability.

This article is based on corporate disclosure data from The Conference Board Benchmarking platform, powered by ESGAUGE.

1For additional context on the chair/CEO debate, including the principal governance arguments for and against separation and recent trends in investor activity and proxy advisor approaches, see Subodh Mishra (Institutional Shareholder Services), Investors Press U.S. Boards To Separate Chair, CEO Roles, Harvard Law School Forum on Corporate Governance, October 12, 2023. For a research synthesis of empirical studies on CEO duality and firm performance (noting that findings vary across settings and methodologies), see Mei Yu, CEO duality and firm performance: A systematic review and research agenda, European Management Review 20, no. 2 (2023): 346–358.(go back)

2Claudius A. Hildebrand, Kate Hurley, and Giovanna Galli, In Volatile Times, Select CEOs for Strategic Advantage, Not Safety, Spencer Stuart, October 2025.(go back)