Print

PrintSteve Cirami is Global Securities Class Actions leader at Broadridge. This post is based on his Broadridge memorandum.

Industry trends: Noteworthy class action developments in 2023

Securities class actions before the Supreme Court.

Despite being the cornerstone of securities litigation worldwide, securities class action law in the United States is continually evolving. Lately, the Supreme Court has taken on cases of substantial significance in shaping securities law and securities litigation. Since 2017, the Court has reviewed no fewer than five cases that have had a profound impact on the evolution of securities class action litigation.

In 2023, the Court clarified, in Slack Techs. LLC v. Pirani, that unregistered shares obtained as part of a direct listing cannot support a claim under Section 11(a) of the Securities Act, which requires the plaintiff to have purchased “such security” pursuant to a materially misleading registration statement.

Further, on September 29, 2023, the Court granted certiorari in Macquarie Infrastructure Corp. v. Moab Partners, L.P.1, to address a circuit split related to whether disclosures required by Item 303 of SEC Regulation S-K, which requires companies to disclose trends or uncertainties likely to have a material impact on a company’s financial position, could give rise to securities fraud claims under Section 10(b) of the Exchange Act and Rule 10b-5. The resolution of this issue may potentially lead to an expansion of securities liability concerning Item 303 disclosure claims in the future.

Emphasis on ESG investing and shareholder activism through securities class and collective actions.

2023 was in line with previous years with an increase in shareholder class and collective actions with broader ESG-related allegations. This level of ESG-related allegations mirrors the growing interest in ESG investing among Broadridge clients and the broader market, which is projected to reach $30 trillion by 2030 as highlighted in the Broadridge ESG and Sustainable Investment Outlook report.[1] This trend was further fueled by a change in investor behavior, with institutional and other investors increasingly viewing class and collective actions rooted in ESG principles as an effective mechanism to uphold and implement their ESG policies and objectives.

This year, shareholder derivative lawsuits, especially those related to breaches of fiduciary duty within the diversity and inclusion context, have gained recognition as an effective means of implementing and upholding ESG reforms. Additionally, the SEC is currently in the process of proposing rule changes mandating specific climaterelated disclosures in registration and periodic filings. Historically, the introduction of new disclosure or reporting requirements has been associated with a rise in litigation.

Expansion of opt-in jurisdictions and the increasing prevalence of collective investor actions.

Each year we bring attention to new legislation or additional regions that permit collective actions. Significant developments in 2023 included:

- In March 2023, revisions to the Rules of the Supreme Court and Consolidated Practice Directions in Western Australia paved the way for a new class action framework for the region, pursuant to legislation that was enacted in September 2022, under the Civil Procedure (Representative Proceedings) Act 2022. This Act introduced a class action framework that closely mirrors the already existing regime in the Federal Court of Australia, a jurisdiction globally recognized for its prominence in securities class actions. This development is noteworthy because it offers investors in Australian securities an additional venue for initiating legal proceedings, by filing cases in the Supreme Court.

- The New Zealand parliament accepted, in principle, the recommendations put forth by the Law Commission concerning R147 Ko ngā Hunga Take Whaipānga me ngā Pūtea Tautiringa (Class Actions and Litigation Funding). The report, which was released in 2022, comprised 121 suggestions for establishing a statutory framework for class actions. The government is presently engaged in the process of working towards implementation, though it recently cautioned that the process will be time-consuming due to the complex nature of the issues involved and the requisite legislative reform.

- In April 2022, the Monetary Authority of Singapore (MAS) released its enforcement report, covering the 18-month period concluding in December 2021. Within this report, MAS emphasized three primary areas of concentration for the upcoming reporting period (ending December 2023). Importantly, one key issue to be addressed in 2023 included exploring possibilities for improving investors’ options to seek redress for losses arising from securities market misconduct.

- On December 26, 2023, China’s first securities class action settlement under the country’s new opt-out regime, the Special Representative Action (Provisions of the Supreme People’s Court on Several Issues Concerning Representative Actions Arising from Securities Disputes (eff. July 31, 2020), was announced. The 280 million yuan ($39.5 million USD) settlement will benefit a class of over 7,000 investors and was initiated on April 28, 2023. To date, two special representative actions have been initiated, the first of which reached a 2.46 billion yuan ($385 million USD) verdict in 2021.

- The deadline for EU member states to enact or modify their collective redress systems in accordance with the EU Directive on Representative Actions was December 25, 2022, with an implementation deadline of June 25, 2023. As a result, various EU countries are currently in different stages of implementing these changes. Two notable revisions in jurisdictions that have historically provided strong investor recoveries are:

- The Netherlands, which was the first EU member state to implement the Directive and first introduced its legislative proposal back in February 2022 which was adopted by the Dutch parliament in June 2023, and then entered into force on September 1, 2023. The law supplements and amends its existing plaintiff-friendly collective redress regime (the “WAMCA”).

- The German parliament, or Bundestag, implemented the Directive on July 7, 2023. The new law will result in a reorganization of the German collective redress system via the Verbraucherrechtedurchsetzungsgesetz, or Consumer Rights Enforcement Act (VDuG). As part of its implementation, the Bundestag also renewed the Capital Markets Model Case Act (KapMuG), originally set to expire at the end of 2023. KapMuG, which, until the passing of VDuG, was Germany’s only procedure for shareholder asset recovery in a class-wide opt-in basis in Germany, is now on its third extension. For now, the VDuG and KapMuG will coexist, and it is possible that issuers may face class-wide claims under both VDuG and KapMuG concurrently.

Increased participation in opt-in litigation.

In 2023, Europe saw the filing of more than 100 collective redress claims; even more were initiated globally. Notably, within Europe, securities-related collective redress actions constituted more than 30% of all filings. Year after year we continue to see increased investor interest in opt-in litigation worldwide. In fact, some of the most common questions that the Broadridge team fields from institutional investors relate to participation in these matters. Some of these questions relate to ESG, as investors tie ESG and class actions together more frequently, and the rest can be attributed to increased jurisdictions, thus increasing global awareness and the amount of money at stake.

International competition claims reach new highs.

Competition claims are being filed at record pace in multiple jurisdictions around the world. For instance, the U.K. Competition Tribunal (CAT) currently has more than 20 collective actions pending, with more than 10 at the collective proceedings order (CPO) stage. The CPO procedure is significant as it allows certain claims to be pursued on an opt-out basis for U.K.-domiciled entities (while non-U.K. domiciled entities will still need to opt-in).

One such claim revolves around allegations that six of the world’s largest banking groups were involved in cartels related to foreign exchange manipulation and spot trading. Initially, the £2.7 billion claim was limited by the CAT to opt-in claims only. However, on July 25, 2023, the Court of Appeal overturned the CAT’s decision, and the claim may now proceed on an opt-out basis (for U.K.- domiciled entities). This marks the first collective action primarily representing businesses that has been granted court approval to proceed as an opt-out action.

SPAC and cryptocurrency-related securities litigation continues to predominate federal filings.

Special Purpose Acquisition Company (SPAC) and cryptocurrencyrelated securities class action filings continue to lead federal court dockets in the U.S. for the third year in a row. Altogether, 16 SPAC cases and 12 cryptocurrency-related cases were filed in 2023.

Although we expect cryptocurrency-related securities class actions (and SEC enforcement actions) will continue to be filed at, record pace both within and outside the U.S., SPAC cases are expected to cool during the next several years. This projection stems from the significant decline in SPAC IPOs, dropping by 95% from their peak in 2021 (613) to 2023 (22)— the lowest IPO count since 2016. The picture is even more clear considering most SPAC claims fall under the Securities Act, which requires claims to be brought within three years of the offering. That said, even though SPAC IPOs have fallen out of vogue, hundreds of SPACs are already underway, searching for acquisition partners. Whether the SPAC closes or goes through a de-SPAC transaction, we can expect litigation to persist — at least for now.

Fewer IPOs yield fewer Securities Act claims.

The number of initial public offerings (IPOs) has continued to decline significantly since reaching an all-time high in 2021, when there were 1,035 IPOs. By contrast, there were only 154 IPOs in 2023. Given the substantial decrease in both traditional IPOs and SPAC IPOs in 2022 and 2023 and considering the truncated statutes of repose and limitations for Securities Act claims, we have observed and anticipate a decrease in the proportion of lawsuits filed against newly public companies relative to the overall docket.

Cybersecurity-related securities class actions are on the rise.

Jurisdictions worldwide are introducing new disclosure requirements and regulations related to cybersecurity, thereby exposing issuers to potential claims associated with cybersecurity risk management, governance and incidents.

For example, on July 26, 2023, the U.S. SEC adopted rules (SEC Final Rule Release No. 33-11216, Cybersecurity Risk Management, Strategy, Governance, and Incident Disclosure) requiring public companies that are subject to the reporting requirements of the Securities Exchange Act of 1934 to disclose any cybersecurity incident deemed material on the newly created Item 1.05 of Form 8-K. The disclosure must include key details regarding the incident’s nature, extent, timing and its material impact (or reasonably anticipated material impact) on the registrant. Comparable disclosure obligations were also extended to foreign private issuers by the Commission.

According to IBM’s Cost of Data Breach 2022 report, 83% of organizations surveyed faced multiple data breaches in 2022. During the past decade, breaches have surged by 600%, costing the U.S. economy trillions of dollars annually. Now, there is a new wave of cybersecurity-related securities litigation on the horizon, one contingent upon how issuers implement these increased disclosure requirements. In fact, cybersecurity-related class actions were the second-highest ranked area of future concern for class actions reported by Norton Rose Fulbright LLP in their 2024 Annual Litigation Trends Survey, which surveys more than 430 general counsel and in-house litigation leaders in the U.S. and Canada.[2]

2023 United States banking crisis in court.

In 2023, the U.S. Federal Deposit Insurance Corporation (FDIC) included four banks on its list of failed banks, and a fifth underwent voluntary liquidation. Notably, two of these banks had substantial exposure to cryptocurrency. The downfall of each of these banks had a ripple effect across the industry, impacting the stock prices of banks globally. Investors followed suit investigating deficiencies, particularly in relation to claims of diversification, a key factor in several of the bank failures. To date, nine securities class actions have been filed in the wake of the crisis.

Broker-dealers shift in service.

Broker-dealers have been key to providing notification of potential securities class actions to their retail wealth customers over the past few decades. During the last few years, there has been a significant shift in the industry to provide holistic claim-filing and asset recovery services to their clientele. Considering the historically minimal participation rates of retail investors in securities class action filings, offering this service has allowed broker-dealers to maintain client asset recoveries in their ecosystem, alleviate the filing-related burden on their advisors and operations teams, and deliver optimal customer experience.

Custodians to provide comprehensive support.

With the increasing complexities in securities class action recovery opportunities, especially opt-in and antitrust cases, many custodians are reevaluating their current class actions programs and have taken steps to provide comprehensive global class action asset recovery support. Although some custodians offer coverage for opt-out filings, many are recognizing the growing need for support in complex cases, and the administrative challenges associated with meeting this need internally.

Concern over short-seller claw back exposure.

Recent settlement programs out of the Delaware Chancery Court have introduced potential complexities for Deposit Trust & Clearing Corporation (DTCC) participants in merger cases for clients that had open short positions at the time of a merger that later resulted in additional merger consideration being distributed as part of a settlement program directly paid by DTCC. Broadridge has been addressing inquiries and collaborating with its clients to gain a deeper understanding of this matter and to minimize any associated risks.

Each of these trends informs the services we provide to our clients. Broadridge continues to expand its suite of services around notification, portfolio monitoring, and class action asset recovery on behalf of asset owners and managers as the industry grows and becomes more complex.

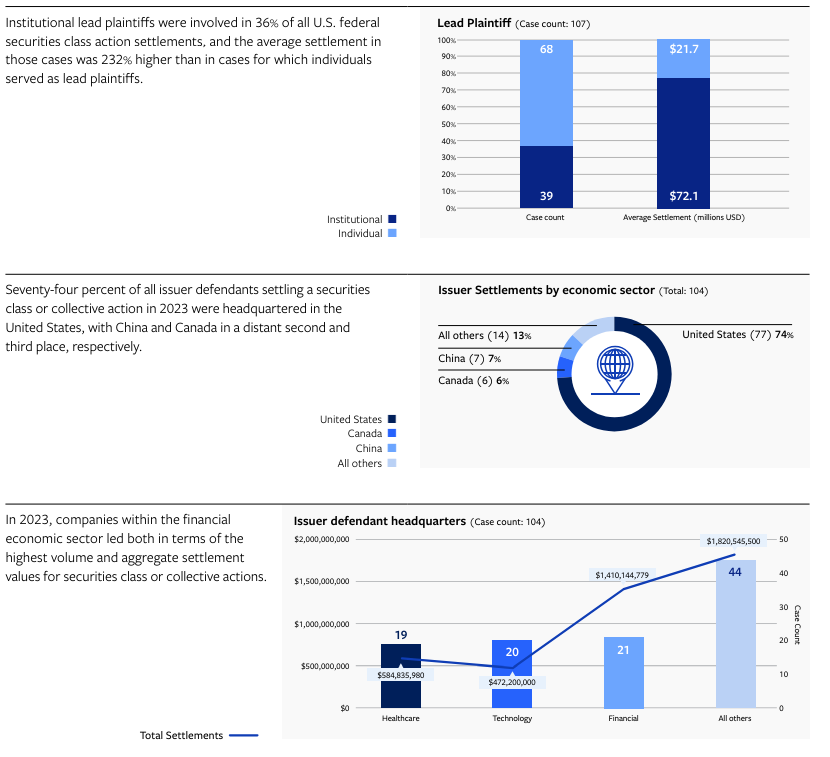

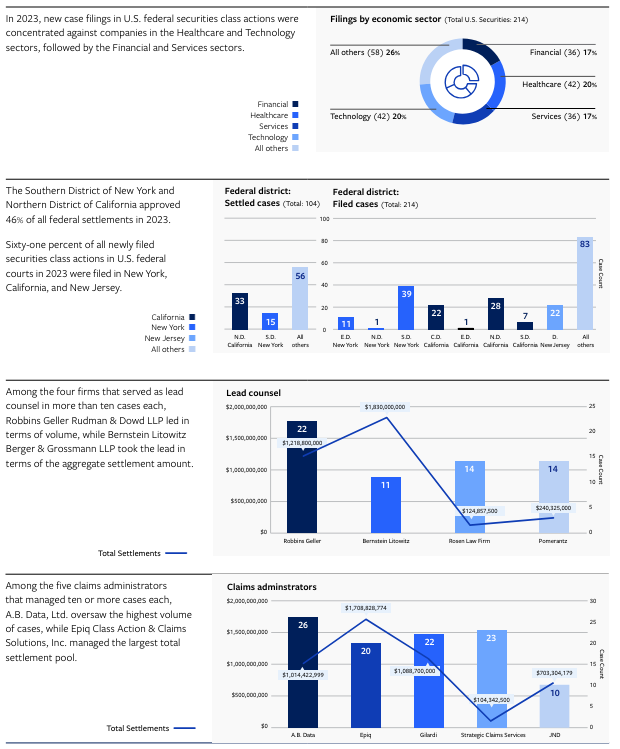

By the numbers: A scorecard

Here is a closer look at some key statistics gathered over the course of the year pertaining to securities and financial antitrust class action settlements.

1Broadridge Financial Services, ESG and Sustainable Investment Outlook, www.broadridge.com/white-paper/asset-management/esg-and-sustainable-investment-outlook (last visited Nov. 27, 2023).(go back)

2Norton Rose Fulbright, 2024 Annual Litigation Trends Survey, https://www.nortonrosefulbright.com/en-us/knowledge/publications/4097006f/2024-annual-litigation-trends-survey (last visited Jan. 22, 2024).(go back)