Print

PrintThe following post comes to us from Aharon Cohen Mohliver of the Department of Management at Columbia University, and Gitit Gur-Gershgoren, Chief Economist at the Israel Securities Authority.

In the paper Channeling Funds into the Group: IPO Pricing in Business Groups, which was recently made publicly available on SSRN, we demonstrate that business groups use financial intermediaries to boost the stock prices of affiliated firms in initial public offerings (IPO). This is done when mutual funds belonging to the group strategically participate in the IPO’s that originate from the group during the road show, and subsequently sell their holdings quickly after the IPO.

In the past decade there has been increasing interest in pyramidal business groups and in the ability of group owners to transfer assets from one firm in the pyramid to another. This phenomenon, dubbed “tunneling” by Kogut and Spicer (1998) and Johnson (2000), can take many forms such as transfer pricing, transfer of goods at nonmarket prices and inflated payments for intangibles. Much of the research examined the internal capital markets in these groups yet the theoretical possibility of transferring resources from external sources into the group’s internal capital markets, an activity we refer to in this paper as “channeling” was not previously addressed.

Channeling funds from sources external to the group is fundamentally different from tunneling from firms within the group. In business groups where ownership is pyramidal the transfer of value in tunneling presents serious governance problems for firms at low tiers in the pyramid, where the divergence is great between cash flow rights and control rights. Unlike trades conducted from firms’ own cash flows, trades conducted on funds managed by financial intermediaries such as mutual, trust, and pension funds can exhibit similar agency problems without a large divergence of control rights from cash flow rights, because the major shareholder of the company owns no portion of the funds being transferred. Furthermore, while tunneling negatively affects the value of the tunneling target, channeling from sources external to the group has limited financial implications for the value of the mutual fund managing companies and the resources accessed are vastly larger. Channeling can therefore be viewed as an extension of the agency problem in mutual funds to business group firms who manage “other peoples’ money”, and result in large benefit to the business group at the expense of savers.

In this paper we seek to shed light on the perseverance of business groups in developed economies, and to provide insights into the persistent underdevelopment of capital markets in these economies. We also verify assumptions made in previous research (e.g., Barca and Becht (2001) that institutional investors controlled by a business group act as “vehicles of power” for the controlling shareholder. We use mutual fund investment decisions in IPOs in which prices of the transactions and the participation of group managed funds are evident. We point to an interesting finding: ownership of financial intermediaries gives business groups the ability to go public with firms that are less profitable, yet they benefit from notably high prices on the stocks sold. This price increase is absorbed by all institutional investors who participate in IPOs generated from the business groups with affiliated financial intermediaries. In this way the business groups systematically weaken the efficiency of capital allocation in stock-exchange offerings.

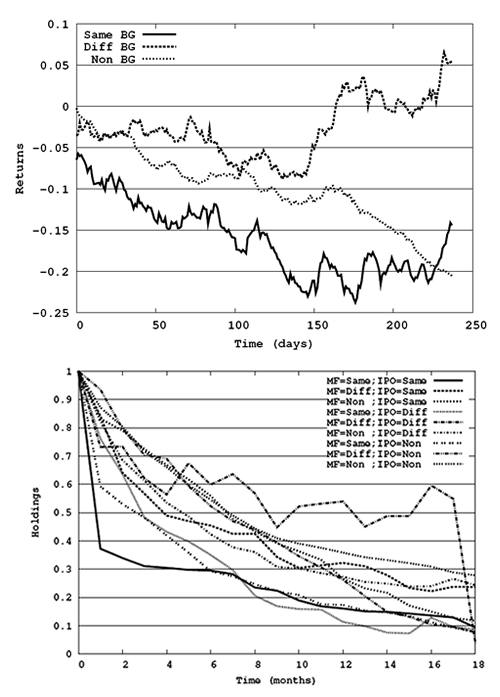

Using a unique data set of all IPOs in the Israeli market over a four-year period, we show clear cases in which institutional investors belonging to a business group transfer funds from small investors to the group at high prices and subsequently incur large losses when selling the stocks. Because Israeli companies use the Dutch auction method to go public, increased participation at the bidding stage can support the demand for the IPO and drive prices up. Systematic behavior like this can create inefficiencies in the IPO market by allocating excessive resources to firms in business groups with financial intermediaries. Figure 1 shows the stock price pattern of Israeli IPO’s divided into three groups: IPOs originating from business group that also control financial intermediaries (same group), business group that don’t control financial intermediaries (different group) and non-group firms (non group). Figure 2 tracks the holdings of mutual funds in those IPO’s over time, showing that mutual funds that purchase stocks in IPO’s originating from their own group sell those stocks quickly after the stocks became listed on the exchange (MF=same, IPO=same).

The contribution of this paper is threefold. First, it contributes to the literature on the transfer of value to firms within business groups and to the corporate governance literature by identifying a potentially significant problem arising from business group control over nonbank financial intermediaries. Second, the paper advances the discussion about how business groups can gain a persistent advantage in domestic stock markets. Third, from a welfare point of view it sheds light on how business groups’ control over financial intermediaries can result in the misallocation of capital in the economy.

The full paper is available for download here.