Print

PrintMatteo Tonello is managing director at The Conference Board, Inc. This post relates to an issue of The Conference Board’s Director Notes series and was authored by Mr. Tonello and Thomas Singer. The complete publication, including footnotes and Appendix, is available here.

Corporate investment in environmental, social, and governance (ESG) practices has been widely investigated in recent years. Studies show that a business corporation may benefit from these resource allocations on multiple levels, ranging from higher market and accounting performance to improved reputation and stakeholder relations. However, poor data quality and the lack of a universally adopted framework for the disclosure of extra-financial information have hindered the field of research. This post reviews empirical analyses of the return on investment in ESG initiatives, outlines five pillars of the business case for corporate sustainability, and discusses why the positive correlations found by some academics remain disputed by others.

Corporate sustainability can be broadly defined as the pursuit of a business growth strategy by allocating financial or in-kind resources of the corporation to ESG practices. Examples of ESG investments that would comprise a corporate sustainability program include: hiring additional auditing specialists to strengthen an internal control or risk management process; engaging a search firm to recruit new female board members; introducing an Ombudsman’s office to address ethical concerns by employees; adopting a procurement policy that increases outsourcing costs but ensures the highest level of compliance with human rights standards; or spending on technology that reduces greenhouse gas (GHG) emissions.

When made, these investments are typically justified as a means to satisfy financial or operational needs or to respond to an explicit stakeholder request. For instance, improving internal control and risk management practices may become a financial priority for a company that experienced difficulties in forecasting its future cash flow.

Similarly, an organization may recognize that the lack of a cohesive ethical culture among its employees is hindering its productivity or that its reputation as an environmental offender is preventing its expansion into a segment of the consumer market. Finally, a company may choose to appoint an independent board chairman in response to a resolution filed by one or more activist shareholders.

The question then arises as to whether this type of resource allocation should be made even when it does not respond to an immediate business concern, based on the consideration that the ESG practice in question will serve the corporation as an intangible asset, reinforcing the trust of stakeholders in the business, and ultimately generating a return in terms of better firm performance. For example, should a company introduce more stringent procurement standards that would require it to sever its ties with a cost-efficient supplier, in the absence of a specific reputational incident or an explicit stakeholder demand? Similarly, should a company (continue to) invest in its employee engagement program in the absence of any indication of employee dissatisfaction? Should a board of directors adopt a diversity policy that could require one or more of its well-performing current members to step down?

A review of empirical research regarding the return on investment in ESG initiatives identifies five pillars of the business case for corporate sustainability:

- Corporate investment in ESG enhances market and accounting performance

- Corporate investment in ESG lowers the cost of capital

- Corporate investment in ESG is a means of engagement with key shareholders

- Corporate investment in ESG improves business reputation

- Corporate investment in ESG channeled to product innovation fosters new revenue growth

The Search for Evidence that ESG Pays Off

The return on ESG investment has been widely investigated in the last decade. Even though there is great variation in the methodologies deployed, the data sources used, and the time horizon examined, many research projects have explored the link between this type of resource allocation and key measures of firm performance. The Appendix (available in the complete publication here) lists the most noteworthy publications in the field that were considered in the preparation of this report. All articles listed in the appendix were published in peer-review journals by academics affiliated with accredited universities; a separate section enumerates the main meta-studies or literature reviews conducted on the subject, including by non-academic organizations. The selection is limited to empirical analyses of the performance of securities (including studies of market indexes) or socially conscious investment funds.

A heterogeneous group of studies

It is important to recognize that this is a heterogeneous group of studies. Some review a wide range of corporate activities across the ESG spectrum, while others are thematic and choose to limit their analysis to one of the three areas of ESG activity (for example, the effect of a series of social policies on firm performance) or to individual practices within an area of ESG activity (for example, the correlation between a board diversity policy and firm performance). Their universe varies, with some studies focusing on firms incorporated or listed in a certain country and others drawing information from large companies included in global indexes. Studies on corporate governance practices, for example, tend to be concerned with the proof of lower capital constraints enjoyed by companies in developed countries, and compare mandatory practices at companies operating in a modern system of securities regulations with their counterparts operating in a bank-centric capital market; for this reason, these studies are of limited or no use to assess the impact of additional governance practices voluntarily adopted by a subgroup of companies in the United States. Moreover, even though many studies show significant variations of their findings depending on the business sector that is scrutinized, others aggregate results without offering sector-specific insights.

The limitations of meta-studies

Considering these studies as a single body of work can lead to major simplifications. In particular, it runs the risk of overemphasizing the conclusions about a phenomenon that remains difficult to analyze empirically, primarily due to the lack of a universally adopted framework to capture and disclose ESG practices. Other research organizations have conducted meta-studies to categorize these empirical analyses, calculating the percentage of them that prove a link between ESG investment and certain metrics of performance. It should be noted, however, that such a meta-analytical approach does have its shortcomings, as it puts the studies on a par with one another, without fully validating individual methodologies and data sources. It also ignores a publication bias, given that studies that show a negative or insignificant correlation are less likely to be published.

While this report brings to the fore some of the publications that corroborate the business case for corporate investment in ESG, readers should note that, perhaps with the exception of the link between ESG investment and a lower cost of capital, none of the “pillars” of the business case for ESG investment described in this report is undisputed in academic research. For example, despite a number of persuasive studies on the correlation between ESG and stock performance conducted on securities, conclusions are far less consistent when the investigation is conducted on socially responsible investment funds using ESG factors as portfolio composition criteria.

An evolving business context

Readers should also be aware that these studies have been conducted over a period of time in which the business context has evolved tremendously. Fifteen years ago, when the first of the projects were undertaken, terms such as ESG or “sustainability” were still largely unknown to a business and investment community that had yet failed to recognize the strategic relevance of these activities and qualified them as an extracurricular “social responsibility” of the corporation.

Today, many market participants are committed to the multiple reputable attempts to codify ESG measurement and reporting, including the Global Reporting Initiative, the Sustainability Accounting Standards Board, and the International Integrated Reporting Council. As documented by The Conference Board, the demand for assurance services in this field has also grown steadily. [1] The empirical investigation of the link between corporate investment in ESG and firm performance must therefore continue, as harmonized reporting and standardized verification practices will help to address the limitations of academic research conducted so far.

Defining Corporate Sustainability

There is a persuasive school of thought on the need for the business community to abandon the “corporate social responsibility” (CSR) term to illustrate the allocation of business resources to ESG. It is based on the argument that CSR inadequately emphasizes the notion of responsibility instead of the strategic, long-term growth rationale that should motivate a corporate sustainability program. In recent years, The Conference Board has endorsed this perspective and chose “sustainability” over “CSR” to name several of its initiatives—including an Institute on Sustainable Value Creation (a distinguished group of CEOs committed to reinforcing trust in business through long-term investment in a wide range of intangible assets), two councils of sustainability officers, an annual conference, a Dashboard of ESG practices adopted by corporations across the globe, and a periodic Sustainability in the Boardroom survey of director oversight practices. For more information, click here.

The Five Pillars of the Business Case for Corporate Sustainability

Empirical research from respected institutions outlines five pillars of the business case for corporate investment in ESG practices:

Corporate investment in ESG enhances market and accounting performance

Multiple empirical studies conducted in the last decade show that companies adhering to strong ESG standards enjoy high profits, low capital expenditures, and high stock return. Even though such conclusions are disputed by other research, the few analyses revealing negative correlations between corporate investment in ESG and firm performance tend to be the oldest and to rely on smaller data samples.

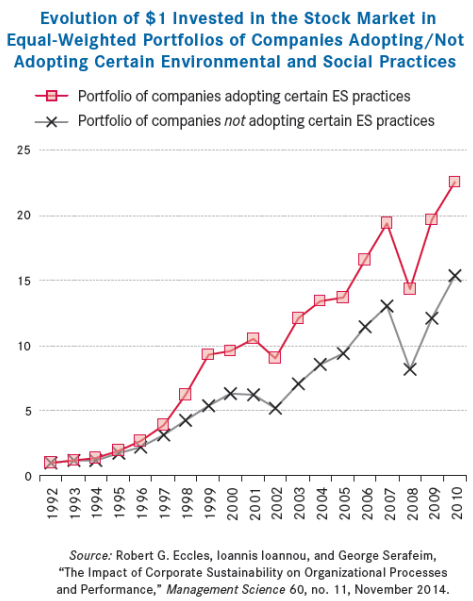

One of the most recent studies proving a positive correlation is a Harvard Business School article first circulated as a working paper in 2011 and released in Management Science in late 2014. [2] The project consisted in the observation of the long-term market and accounting performance of a matched sample of 180 companies, some of which had voluntarily established a range of environmental and social practices many years before. The study found that the subset of more sustainable companies significantly and consistently outperformed, over time, others in the sample that had introduced none of the environmental and social policies in question. The authors suggest that such outperformance may be a function of certain governance traits that appear to be commonly adopted in conjunction with those environmental and social policies—namely, the explicit assignment to the board of directors of the responsibility for sustainability oversight, the use of sustainability metrics as objectives in executive compensation packages, and the propensity to engage with stakeholders and disclose non-financial information to the market.

Another notable article, published in 2006 by the Journal of Marketing, ranked companies based on their performance across a range of environmental and social issues and quantified that a single-unit increase in the rating would result on average in approximately $17 million of additional annual profit in the years following the increase. [3]

The study argued that customer satisfaction mediates the relationship between ESG factors and performance, given the increasing sensitivity to these factors displayed by the consumer market. For this reason, the correlation can be observed more prominently among companies in the business-to-consumer segments of the market.

Analyses of market performance typically use stock return data and Tobin’s Qs (a stock valuation measure calculated by dividing the market value of a company by the replacement value of its assets). Instead, the correlation between ESG factors and other, non-equity asset classes remains largely unexplored.

Corporate investment in ESG lowers the cost of capital

It is shown that publicly traded firms may reduce their cost of capital by adopting strong ESG practices. The relationship has been studied more extensively for corporate governance practices, with research building on the undisputed observation that companies listed in countries with advanced securities regulations and well-funded enforcement agencies benefit from easier access to the financial market.

Most of the analyses attribute the finding to the mitigation of business risks resulting from the adoption of superior governance practices (including a diversified and independent board of directors, a system of shareholder rights, and the elimination of unreasonable barriers to takeovers that would hinder a competitive market for corporate control). In general, lenders believe that better-governed companies are subject to fewer cases of shareholder suits or government investigations, and that they are less exposed to disruptions by activist investors. Studies published in 2003 and 2007, for example, found that firms with more elements of shareholder-centric corporate governance enjoyed higher ratings on their bonds issues and lower yields. [4]

More recently, the investigation has extended to the environmental and social area. According to an article published in 2011 by the Journal of Banking and Finance, firms publicly exposed to environmental and social concerns faced shorter maturities and higher loan spreads—paying for their borrowed capital, on average, 7 to 18 basis points more than companies that were more socially responsible. [5] Two other studies published in the same year reached similar conclusions for the cost of equity; they argued that socially responsible companies tended to voluntarily disclose this information, which led to more accurate coverage by analysts and better company valuations. [6]

Corporate investment in ESG is a means of engagement with key shareholders

Socially responsible investment (SRI) funds first made their appearance in the 1970s, when some faith-based institutions began excluding from their investment vehicles securities from military defense contractors and other business activities contrary to their values. Today, SRIs have evolved from a negative screening practice to a series of sophisticated ESG incorporation strategies spanning a wide range of asset classes (equity and fixed income but also alternative investments such as arbitrage, event-driven investing and activism, and asset-backed securities). Moreover, thanks in particular to initiatives such as the United Nations’ Principles for Responsible Investment (PRI), [7] an increasing number of public pension funds and investment entities affiliated with labor unions have become receptive to ESG-driven investment strategies, either by launching their own SRI vehicles or by exercising pressure on companies to introduce environmental and social reforms to their business practices (see “Shareholder Proposals on Social and Environmental Issues—A 2014 Update” in the next section).

Even though there is no convincing evidence that SRI funds outperform the market in the long term, most academic studies published in the last decade found that these investments are competitive with non-SRI strategies. [8] The staggering growth of this segment of the asset management industry corroborates the empirical findings. According to the latest official survey of the industry, as of early 2014, assets managed by US-based firms considering corporate ESG practices as investment criteria had grown to $4.8 trillion, or more than two fold since the level registered in early 2012 ($1.4 trillion). [9]

For these reasons, corporate investment in ESG may help to attract to the company’s shareholder base a class of long-term investors that is increasingly gaining influence. It also offers new opportunities for companies to engage with large institutional investors sensitive to these issues.

Shareholder Proposals on Social and Environmental Issues

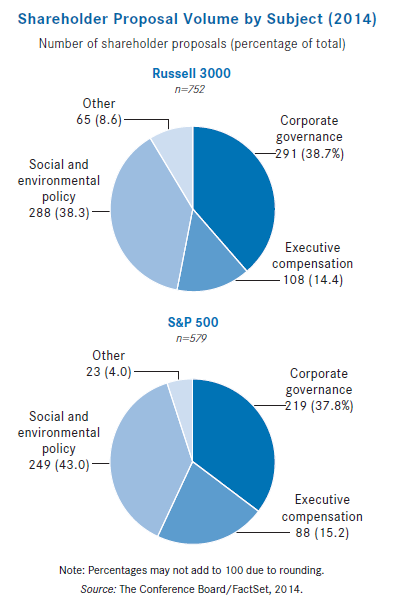

While their voting support remains far below the majority threshold, the volume of proposals on social and environmental policy issues rose to unprecedented levels in 2014. These requests represented the single most frequent subject of shareholder resolutions filed in the S&P 500 in the January 1-June 30, 2014 period (249 proposals, or 43 percent of the total filed at companies in that index) and more than one-third of the total submitted at Russell 3000 companies (288 proposals, or 38.3 percent).

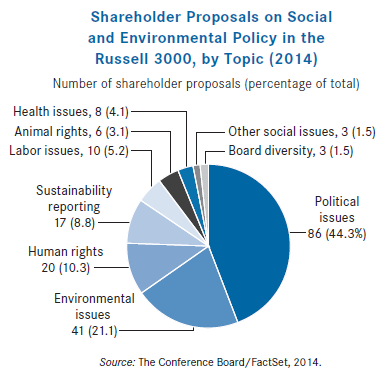

Widely diversified (ranging from political contribution disclosure to compliance with human rights and from sustainability reporting to the adoption of a climate change policy), these issues are pursued by multiple investor types, with the highest concentration among individuals (58 filed proposals in 2014), public pension funds (49 proposals), and other stakeholders like the Humane Society of the united States and the National Center for Public Policy Research. [10]

Corporate investment in ESG improves business reputation

When it does not satisfy immediate operational and financial needs, corporate investments in ESG can be strategic and long-term, as it enhances relations with key stakeholders (whether employees, customers, suppliers, or local communities where the company operates). Over time, the perception of the corporate brand benefits from these improved relationships: talent recruitment and retention, customer satisfaction, and the quality of media coverage are areas of intangible business success where, thanks to today’s technology, the effects of an ESG program can be easily monitored. Research published in 2014 by The Conference Board in collaboration with CSRHub explored the link between sustainability performance and Brand Finance’s Brand Strength Index (BSI), a proprietary methodology to calculate the brand value of more than 5,000 leading global companies. The study revealed that about 22 percent of the variation in BSI can be explained by changes in perceived ESG performance. [11] Corporate reputation and sustainability are therefore related, and a company that seeks to do well in one area should also consider investing in the other.

Rating and ranking providers are also more likely to recognize companies committed to standardized sustainability disclosure. In fact, an empirical review conducted by G&A—Governance & Accountability Institute [12] showed a positive correlation between a firm’s adoption of the GRI guidelines on ESG reporting and its performance vis-a-vis prominent indicators of corporate reputation, such as:

- Inclusion in Ethisphere’s World Most Ethical Companies

- Inclusion in the Dow Jones Sustainability Index

- Inclusion in CR 100 Best Corporate Citizens (CR Magazine)

- Inclusion in Newsweek’s Greenest Companies

- More favorable Glassdoor ranking

- More favorable CSRHub ranking

- Higher Bloomberg ESG Disclosure Scores

Corporate investment in ESG channeled to product innovation fosters new revenue growth

There is ample literature on the benefits of a corporate sustainability strategy as an initiative to improve efficiencies, reduce costs, and minimize a firm’s environmental impact. However, there are also significant benefits associated with top-line growth that receive far less attention. An increasing number of companies recognize that ESG initiatives can yield new market opportunities, stimulate innovation in products and services, and ultimately be an important source of revenue.

In fact, recent research by The Conference Board examines the extent to which a sample of S&P Global 100 companies generate revenue from sustainability initiatives. [13] There are several examples of companies that have developed successful products or new lines of business built on sustainability considerations. The development of these products can be motivated by a variety of factors, such as cost savings and efficiencies(e.g., using fewer materials), customer demand (e.g., longer-lasting products, products free of hazardous materials),or regulatory developments (products with lower GHG emissions). In many cases these products represent a rapidly growing source of revenue and an increasingly larger share of a company’s total revenue.

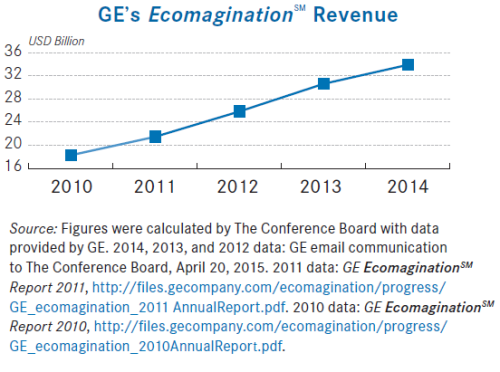

General Electric’s often cited EcomaginationSM initiative provides a good example. The initiative was launched in 2005 as the company’s commitment to technology solutions that save money and manage environmental impact for GE’s customers and the company’s own operations. Since its launch, EcomaginationSM has generated about $200 billion in revenue for GE. In 2014 alone, revenue from EcomaginationSM totaled $34 billion, accounting for 31 percent of the company’s total industrial revenue. Revenue from EcomaginationSM increased 89 percent from 2010 to 2014, about three times the growth rate of the company’s total industrial revenue over the same period.

DuPont is another example of a company that has generated significant revenue growth from investment in ESG initiatives. In 2011 DuPont set a 2015 goal to increase annual revenue from products that increase energy efficiency and/or significantly reduce greenhouse gas emissions by at least $2 billion. By 2013, these products generated $2.5 billion in revenue for DuPont—a 56 percent growth since 2010, compared to the company’s overall revenue growth of 29 percent in the same period.

A corporate sustainability strategy can be an effective way to manage risks, reduce environmental impacts, improve efficiencies, and lower costs. As evidenced by examples from a number of leading companies, a sustainability strategy can also pave the way for product innovation and new sources of significant revenue growth.

Conclusions

Corporations have been investing in ESG practices more frequently in the last decade. However, these resource allocations often respond to immediate business needs rather than a strategic and cohesive sustainability program intended to enhance for the long-term key intangible assets in the environmental, social, and governance spheres.

While empirical research on the link between corporate investment in ESG and firm performance is far from undisputed, several studies led by respected institutions have shown that a company can be rewarded for adopting these practices: higher profits and stock return, a lower cost of capital, and better corporate reputation scores are the key benefits enjoyed in return for this type of investment. As companies continue to adhere to harmonized reporting standards and verified data becomes more readily accessible, researchers will be able to continue this course of investigation and find the definitive proof that ESG-related corporate expenditures do pay off.

The complete publication, including footnotes and Appendix, is available here.

Endnotes:

[1] In 2014, 30 percent of companies in the S&P Global 1200 and 12 percent of those in the S&P 500 issued sustainability reports that include third-party verification and assurance. The finding compares to the 25 percent and 8 percent respectively reported for the two indexes in 2013. The scope of assurance that companies include in their reports can vary widely and extend to the entire sustainability report, only specific sections, or just greenhouse gas (GHG) emissions. See Sustainability Practices Dashboard—2015 Edition Key Findings, The Conference Board, Research Report No. 1573, February 2015.

(go back)

[2] Robert G. Eccles, Ioannis Ioannou, and George Serafeim, “The Impact of Corporate Sustainability on Organizational Processes and Performance,” Management Science 60, no. 11, November 2014, pp. 2835-2857.

(go back)

[3] Xueming Luo and C.B. Bhattacharya, “Corporate Social Responsibility, Customer Satisfaction, and Market Value,” Journal of Marketing 70, no. 4, 2006, pp. 1-18.

(go back)

[4] Lucian A. Bebchuk, Martijn Cremers, and Urs Peyer, “CEO Centrality,” NBER Working Paper no. w13701, December 2007 and Sanjeev Bhojraj and Partha Sengupta, “Effect of Corporate Governance on Bond Ratings and Yields: The Role of Institutional Investors and Outside Directors,” The Journal of Business, vol. 76, no. 3, 2003 pp. 455-476.

(go back)

[5] Allen Goss and Gordon S. Roberts, “The Impact of Corporate Social Responsibility on the Cost of Bank Loans,” Journal of Banking & Finance 35, no. 7, 2011. In the social area, in particular, a 2009 study by Bauer et al. found that debt financing tends to be less expensive to companies with stronger employee relations.

(go back)

[6] Ghoul et al. “Does Corporate Social Responsibility Affect the Cost of Capital?” Journal of Banking & Finance 35, no. 9, September 2011, pp. 2388-2406 and Dhaliwal et al., “Voluntary Nonfinancial Disclosure and the Cost of Equity Capital: The Initiation of Corporate Social Responsibility Reporting,” The Accounting Review, 86, no. 1, 2011.

(go back)

[7] Established in 2005 response to an invitation by then UN Secretary General Kofi Annan, the Principles for Responsible Investment are based on the notion that ESG issues such as climate change and human rights can affect the performance of investment portfolios and should therefore be considered alongside more traditional financial factors if investors are to properly fulfill their fiduciary duties. As of December 2014, PRI signatories include 285 asset owners and 863 investment managers, including large US public pension funds such as CalPERS and TIAA-CREF. For more information, visit unpri.org.

(go back)

[8] Jeroen Derwall, Kees C.G. Koedjijk, and Jenke Ter Horst, “A Tale of Values-Driven and Profit-Seeking Social Investors,” CFA Digest, CFA Institute 41, no. 3, August 2011.

(go back)

[9] Report on US Sustainable, Responsible, and Impact Investing Trends 2014, US SIF Foundation, November 20, 2014.

(go back)

[10] Matteo Tonello and Melissa Aguilar, Proxy Voting Analytics (2010-2014), Research Report No. 1560, The Conference Board, November 2014. Also see Thomas Singer and Melissa Aguilar, “Shareholder Proposals on Social and Environmental Issues,” Director Notes No. 16/2014, The Conference Board, December 2014.

(go back)

[11] Bahar Gidwani, “The link between Sustainability and Brand Value,” in Thomas Singer (Ed.), Sustainability Matters 2014, Research Report, R-1538-14-RR, 2014, p. 25.

(go back)

[12] 2012 Corporate ESG/Sustainability/Responsibility Reporting. Does It Matter? Analysis of S&P 500 Companies’ ESG Reporting Trends and Capital Markets Response, and Positive Association with Desired Rankings & Ratings, G&A—Governance & Accountability Institute, December 2012 (http://www.ga-institute.com/fileadmin/user_upload/Reports/SP500_-_Final_12-15-12.pdf).

(go back)

[13] See Thomas Singer, Driving Revenue Growth Through Sustainable Products and Services, Research Report No. R-1583-KBI, The Conference Board, June 2015.

(go back)