Print

PrintHolly J. Gregory is a partner and co-global coordinator of the Corporate Governance and Executive Compensation group at Sidley Austin LLP. The following post is based on a Sidley update by Ms. Gregory, John P. Kelsh, Thomas J. Kim, Rebecca Grapsas, and Claire H. Holland. The complete publication, including footnotes, is available here. Related research from the Program on Corporate Governance about proxy access include Lucian Bebchuk’s The Case for Shareholder Access to the Ballot and The Myth of the Shareholder Franchise (discussed on the Forum here), and Private Ordering and the Proxy Access Debate by Lucian Bebchuk and Scott Hirst (discussed on the Forum here).

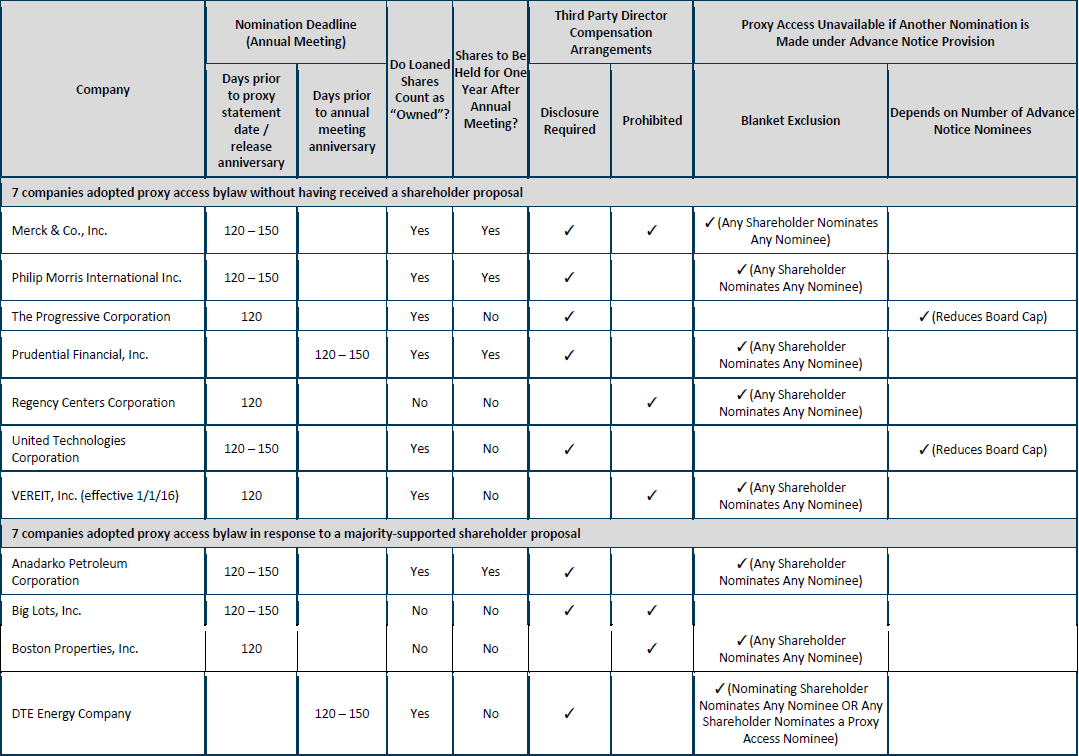

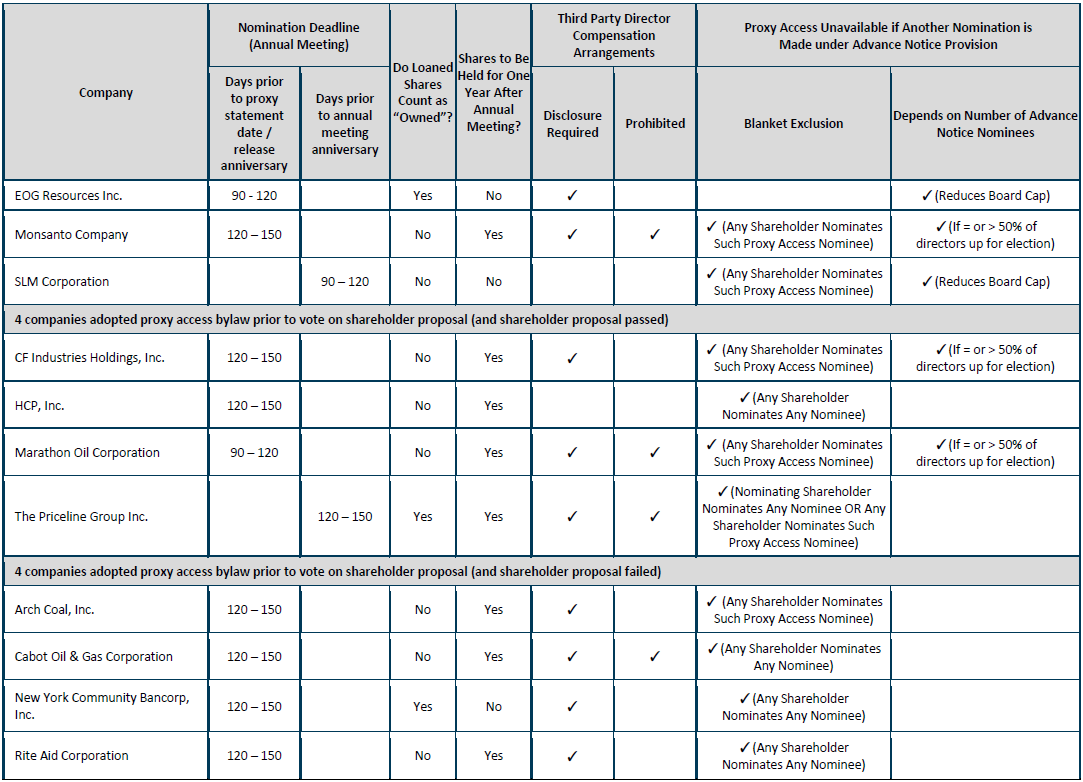

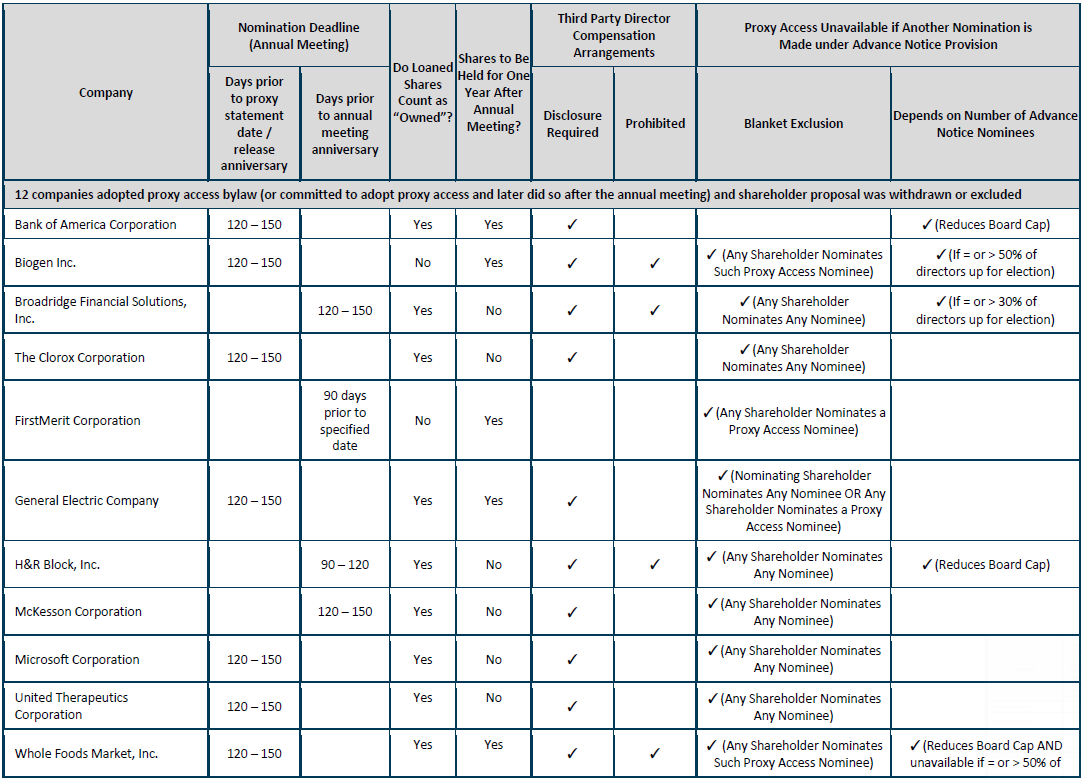

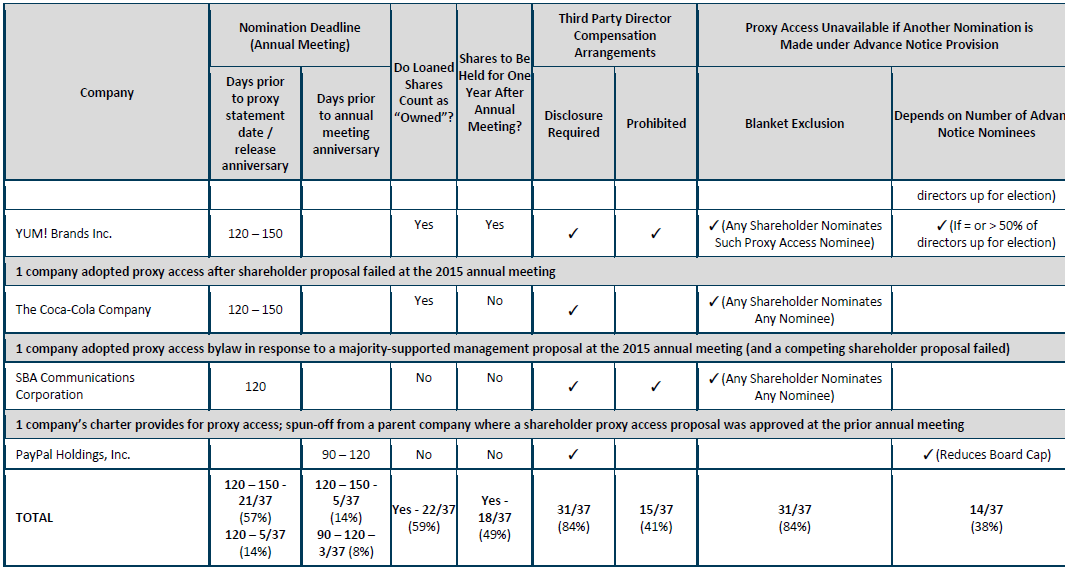

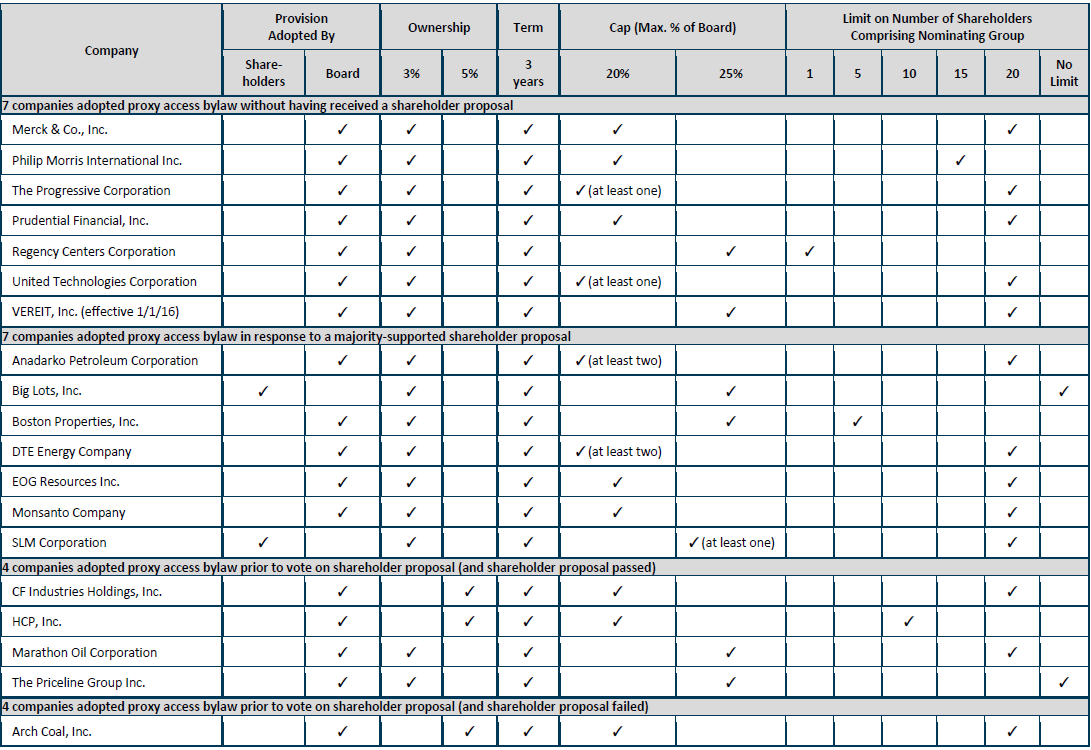

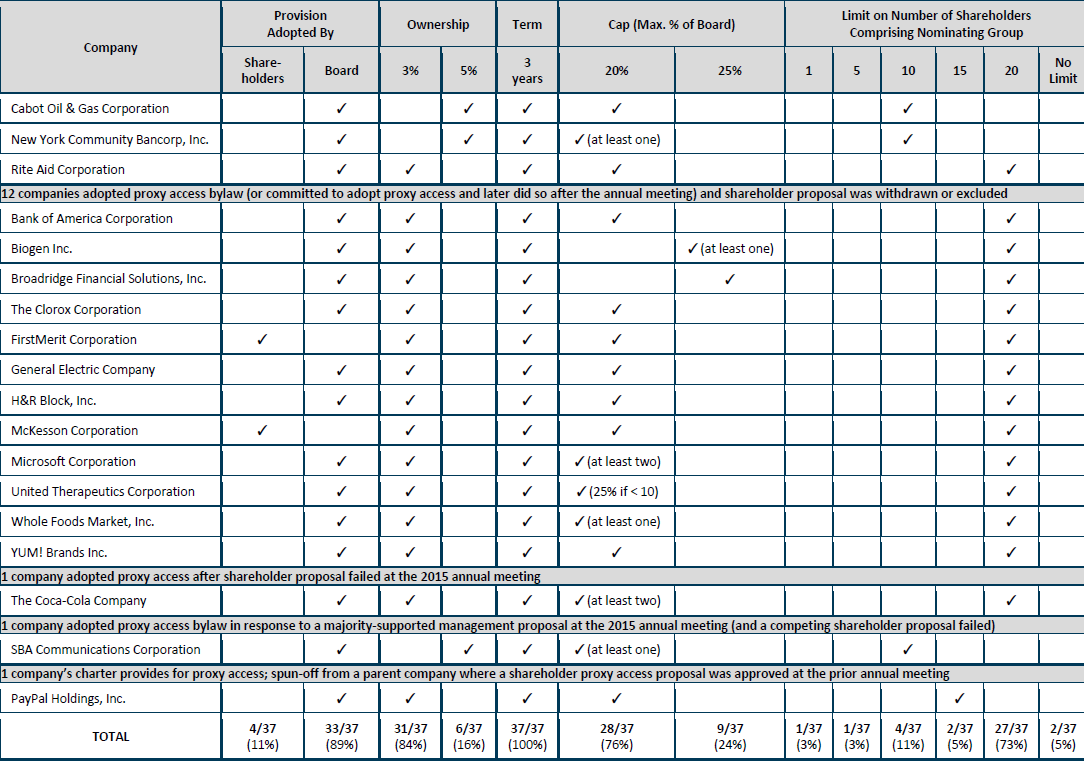

This post revises our August 3, 2015 post to include additional information relating to the prevalence of certain types of proxy access provisions. In particular, the charts included in Appendix A and Appendix B highlight, on a company-by-company basis, the following terms of proxy access provisions adopted so far this year.

- the minimum ownership thresholds and holding periods,

- the maximum percentage of board seats open to proxy access nominees,

- the maximum number of shareholders that can comprise a nominating group,

- the nomination deadline,

- whether loaned shares are treated as owned for purposes of the meeting the minimum ownership threshold,

- whether shares are required or expected to be owned for one year following the annual meeting,

- whether third-party director compensation arrangements are prohibited and/or required to be disclosed and

- whether proxy access is unavailable if a director nomination has been made under the company’s advance notice provision.

Appendix A: Key Parameters

Appendix B: Additional Selected Provisions