Print

PrintUmit Gurun is Associate Professor of Accounting at the University of Texas at Dallas. This post is based on an article authored by Professor Gurun; Noah Stoffman, Associate Professor of Finance at Indiana University, Bloomington, and Scott Yonker, Assistant Professor of Finance at Cornell University.

When the massive Ponzi scheme orchestrated by Bernie Madoff collapsed in December 2008, its effects were immediately felt by a large number of charities, universities, wealthy individuals who altogether disclosed investments of more than $20 billion with Bernard L. Madoff Investment Securities LLC.

In our paper, Trust Busting: The Effect of Fraud on Investor Behavior, which was recently made publicly available on SSRN, we argue that this fraud had effects far beyond the direct investments that were lost by thousands of victims. Public trust in the financial system was affected, especially among people who lived close to Madoff victims. This “shock” to trust could have arisen from a heightened awareness of the fraud either through social connections to victims, or increased coverage by local media in areas with many victims. Indeed, across states, the amount of searching on Google for the term Madoff is highly correlated with the concentration of victims in that state. Moreover, Gallup survey data indicate that people who lived closer to Madoff victims reported larger declines in confidence in the criminal justice system than did others.

We combine data from court documents on the home addresses of more than 11,000 victims with data from the FDIC on branch-level bank deposits and data we received through a FOIA request to the SEC on the assets managed by Registered Investment Advisors. The structure of our data allows us to use a difference-in-differences regression approach that identifies the causal effect of a shock to trust on investor risk-taking and asset flows.

We show that investors in areas close to victims moved substantial amounts of money out of risky investments with Registered Investment Advisors and into safe cash deposits at federally insured banks relative to demographically similar investors in areas with few Madoff victims. In aggregate, we estimate that approximately $430 billion was moved by investors out of delegated portfolios at investment advisers to safer investments as a result of their decrease in trust. This number is more than 25 times as large as the direct wealth loss (court-ordered restitution was $17 billion).

We find no evidence that the withdrawals were reversed—even up to four years after the fraud was revealed—consistent with the view that trust shocks have long-lasting effects on investors. As a result of withdrawals, an investment advisor with a one standard deviation increase in client exposure to the fraud was almost 50% more likely to subsequently cease operating, indicating that trust shocks can lead to adverse real effects in the economy.

We also document, however, that money managers who are able to build trust with their clients through the provision of additional services—such as providing financial planning advice—suffered very little from trust-based withdrawals. This finding is very much in line with the predictions of the Gennaioli, Shleifer, and Vishny (2015) of the important role for “Money Doctors” who build trust with clients and give confidence to invest in assets by providing hand-holding.

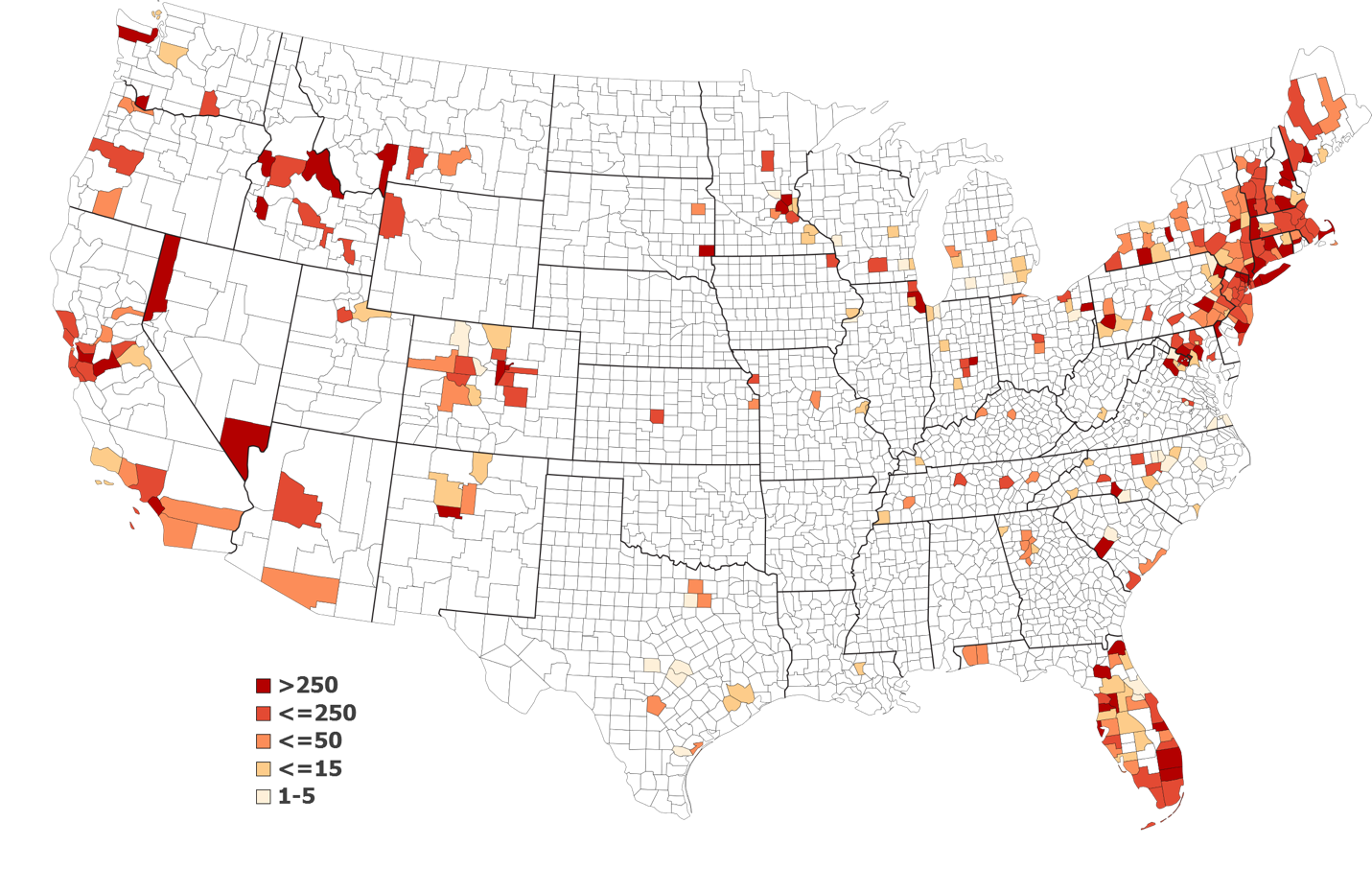

Our ability to identify these effects econometrically is due to the fact that Madoff victims were not uniformly distributed around the country. Rather, as shown in this figure, victims were heavily concentrated in particular areas, especially near Miami and the northeast.

This geographic concentration of victims is not a fluke. Rather, it is due to another aspect of the Madoff scheme: that it was an “affinity fraud”, in which fraudsters target potential victims who share a common bond, such as religion, to build trust. Such affinity links have been shown to be an important determinant in the success of Ponzi schemes. In the case of Madoff, many victims were Jewish people and organizations. The losses from the scheme were widely felt in the Jewish community, with a number of charities being forced to cut back operations, and in some cases, close.

We find evidence that abnormal adviser withdrawals were concentrated in areas with large populations of the affinity group, suggesting that the trust shock was transmitted through social networks within this group. Taken together, our results collectively suggest that trust is a critical determinant of asset allocation, has real economic effects and social networks transmit shocks to trust.

Despite having a relatively clean identification of the trust shock, we do face some important challenges to our empirical strategy that we are careful to address. For example, if investors in affected areas reduced their risky investments to cope with potential negative consequences of the subprime mortgage crisis—and not due to the Madoff fraud—that would cast doubt on whether the Madoff trust shock per se generated the effect we document. In particular, Florida—where several hundred Madoff victims resided—felt the subprime mortgage crisis acutely. Therefore, our analysis include time-varying fixed effects at various geographic levels and a battery of controls, including zip code level house price appreciation, to capture contemporaneous changes in the economic environment. We also show that people who were more affected by the fraud did not behave differently from others before the fraud, which is a critical assumption of the econometric design. Finally, we show that neither the “treated” group nor the affinity group responded differently from other groups during another large market decline (the collapse of the Internet bubble), indicating that the communities in which Madoff victims reside are not generally more conservative in the face of a crisis.

The full paper is available for download here.