Print

PrintBarnabas Reynolds is head of the global Financial Institutions Advisory & Financial Regulatory Group at Shearman & Sterling LLP. This post is based on a Shearman & Sterling client publication by Mr. Reynolds, Thomas Donegan, and James Webber. The complete publication, including footnotes and annex, is available here.

The UK is holding a referendum on 23 June 2016 to decide whether or not to remain a member of the European Union. There seems to be a disconnect between some aspects of public discourse on the vote and the actual effect of an in or out vote. A vote to leave would have numerous possible legal consequences but, if the UK rejoins the EEA, the passporting regime for financial institutions and “free movement of persons” would continue. A vote to remain would also kick off a process to change the UK’s relationship with the rest of the EU. This post discusses potential legal issues arising from a Brexit.

Introduction

As a member of the EU, the UK has access to the Single Market. The Single Market was created to remove barriers and constraints between EU countries and to create a single economic area. The Single Market has largely abolished trade barriers and physical customs requirements within the EU, reducing costs associated with the cross-border trade of goods. In addition to removing internal tariff barriers, the EU has also implemented a common external tariff which is applied to goods imported from non-EU countries. The abolition of internal tariffs combined with common external tariffs cements the EU as a Customs Union. It provides, amongst other things, for the free movement of individuals, goods and services and a right of establishment within the EU. The model which the UK negotiates with the EU will determine its access to the Single Market.

The UK’s new settlement with the EU will take effect if the UK decides to stay in the EU. The settlement is in the form of a Decision of the Heads of State or Government meeting within the European Council (the “Settlement”). The UK government has confirmed that in its view the Settlement is legally binding under international law. However, the extent and pace of implementation of all aspects of the Settlement is not certain. Those aspects requiring the implementation or repeal of EU directives and regulations will need to be endorsed by the European Commission, European Parliament and Council of the European Union.

Briefly, the Settlement provides for the UK: (i) not to further its political integration with the EU, which is an attempt to secure the degree of sovereignty that the UK currently holds; (ii) not to participate in the Euro in the future and not be discriminated against for not participating; (iii) to be able to push for the EU to adopt better regulation and pursue an ambitious trade policy; and (iv) to have greater control over immigrants coming to the UK and their access to the benefits system.

According to the Bank of England, the Settlement does not alter the powers of the EU bodies, but will guide how the powers are used. The revised EU financial services framework, as agreed under the Settlement, would enable the Bank to meet its financial stability objectives.

Brexit Mechanism

Should there be a “leave” vote, the Settlement will fall away and the UK will need to negotiate its exit from the EU. There are several legal models that the UK government could negotiate following a vote to leave. These may include:

- Complete withdrawal from the EU, with new bespoke bilateral agreements that retain freedom of trade and/or establishment, without membership of an existing European bloc.

- Joining the European Free Trade Association (“EFTA”) and re-joining the European Economic Area (“EEA”) (i.e. like Norway, Liechtenstein and Iceland).

- Joining EFTA and relinquishing membership of the EEA whilst gaining access to the European markets through bilateral agreements (i.e. like Switzerland).

- Entering into a customs union with the EU (i.e. like Turkey, although the Turkish-EU customs union is limited to trade in goods).

- Entering into a free trade agreement with the EU within the World Trade Organisation framework (i.e. like Canada).

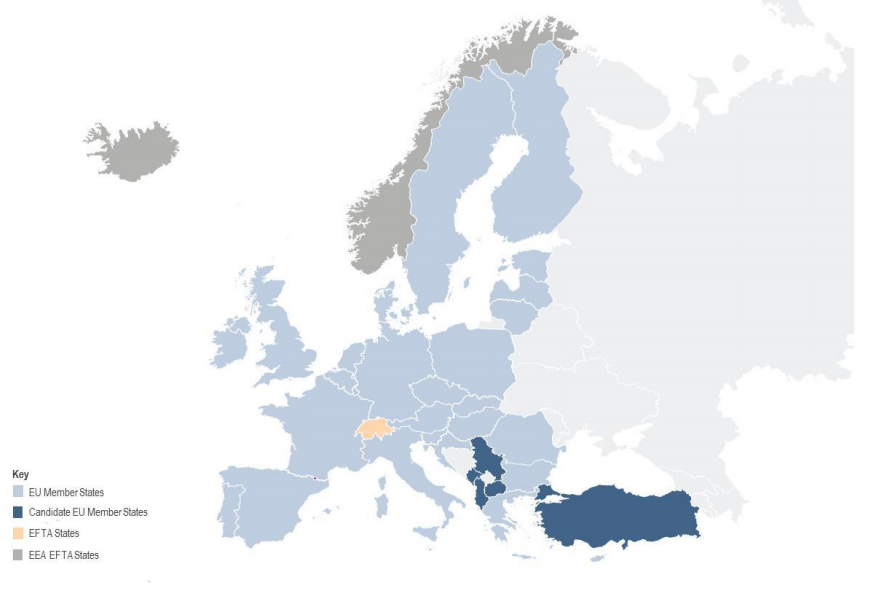

The map below depicts the countries that are currently in the EEA as well as the candidate EU member states.

Current Legal Framework: Background

The UK legal framework for its EU membership and the manner in which it fulfils its current EU obligations is found in the European Communities Act 1972 (“ECA”). The ECA provides for all pre-existing EU texts to apply in formal UK law, although the method of transposition varies depending on the nature of the EU legislative instrument. All “directly effective” EU legislation (i.e. EU regulations and certain articles of the EU treaties) is automatically incorporated into national law without the need for further enactment through an Act of Parliament. In practice, some UK legislative changes are often needed to eliminate any inconsistencies with a particular EU regulation. In contrast, EU directives are binding on EU member states but require national implementation measures, often done in the UK by statutory instrument under authority of the ECA. In addition, in sectors which are subject to regulation, such as financial services, rules and guidance are often issued by the regulators to implement or further detail the requirements. It is unclear what would replace the ECA on a Brexit or whether previous EU legislation would need to be grandfathered.

EU law includes the principle of direct effect. EU law may be of vertical direct effect, which means that individuals can invoke an EU provision in relation to a country, or of horizontal direct effect which means that an individual can invoke an EU provision in relation to another individual. The EU treaties are of direct effect, both vertically and horizontally, provided that the obligations are precise, clear, unconditional, do not require additional measures at either national or European level and do not give member states any discretion. EU regulations are always of direct effect, both horizontally and vertically. EU directives are of vertical direct effect when the provisions are unconditional, clear, precise and have not been transposed by the relevant member state by the required deadline.

Another key EU principle is the precedence principle which provides that European law is superior to the national laws of member states and that member states may not apply a national law that is contrary to European law. If a member state law is contradictory to EU law, then the member state law is invalid. The precedence principle applies to all EU laws of binding force—the treaties, regulations, directives, decisions and international agreements. The Court of Justice of the European Union (“CJEU”) is responsible for ensuring compliance with both the precedence principle and the principle of direct effect.

Brexit Negotiation Process

The process for exiting the EU is established under the Treaty on European Union. The provisions were inserted into the Treaty after Greenland exited the EU and for which there was no mechanism at the time. An exit under the Treaty provisions has not occurred before and so the practical application of the relevant provisions is inherently uncertain. The Treaty provides that a member state may withdraw from the EU following the negotiation and conclusion of an agreement with the EU, outlining the exiting member state’s arrangements for withdrawal from the EU and its future relationship with the EU. EU Treaties would cease to apply to the UK upon an agreement taking effect or the expiry of two years from the date of the UK’s notification to exit from the EU. The UK could apply to the European Council for an extension of the two-year period. However, approval of any such extension requires unanimous consent.

The UK would be faced with a period of uncertainty once the exit process is triggered—although in theory the exit process could be triggered by the UK only after the new arrangement had been negotiated. It would no longer have a presence in European Parliament after notice is given and the exit negotiations would be led within the EU by representatives of the remaining EU member states in the relevant institutions. If no agreement is settled within the prescribed two-year period, and no extension of time is granted, the UK would be deemed to have exited the EU and all associated trade and other arrangements would largely cease to apply, unless other steps were taken.

Transitional arrangements necessary for the two-year period to be observed will add a layer of complexity concerning: (i) the validity of existing EU legislation; (ii) the nature of the legislation, in particular, whether it is directly effective or not; and (iii) the terms of the exit.

Complete Exit from EU

The most extreme option is complete withdrawal from the EU. All EU legislation, including treaties, would cease to form part of UK law.

Effect of Brexit on Existing EU Regulatory Framework

Legal Implications

On any Brexit situation, the ECA would need to be repealed or substantially amended. Any amendment to, or removal of, the entire legislative framework for implemented EU law would have several constitutional, administrative and practical implications relevant to a broad field of laws implemented under the ECA. In addition, EU regulations would cease to apply in the UK. This means that a grandfathering system would need to be implemented or a large legislative drafting exercise undertaken or a combination of both followed by a review to assess which laws the UK wanted to keep, remove or tailor. This will be particularly important in areas where EU legislation on a particular issue has been implemented by both regulation and directive. For example, the EU legislative framework on capital standards for banks is contained in the Capital Requirements Regulation (“CRR”) (of direct effect in the UK) and the Capital Requirements Directive (“CRD”) (which has been implemented through UK legislation). Without a grandfathering system or new laws being drafted expeditiously to replace the EU legislation, the UK legislation implementing CRD would not, without the CRR sitting alongside it, have practical application. The situation would lead to legal uncertainty.

In practice, for example, UK and EU businesses currently operating on a cross-border basis may find that they have to comply with different (unharmonised) laws in both the UK and a post-Brexit EU. Further, and for example, given that the existing UK financial regulatory framework is largely (albeit with some tailoring) influenced by, and dependent upon, EU policy-making and legislation, UK regulated firms operating on a purely domestic basis may potentially find themselves subject to a different regulatory regime in a post-Brexit world. Other areas where UK laws are principally or significantly EU-based, such as agriculture, fisheries, employment, health and safety, customs, environment and product specifications are likely to prove particularly challenging for industry in the absence of transitional measures.

In terms of EU legislation, all references to the UK in existing EU legislation would need to be removed and there may be some unknown effects that the EU legislators will need to address.

Financial Services Sector

Loss of Influence over EU Legislation

If there was a vote to leave the EU, the UK would lose influence in framing any EU legislation. This is mostly viewed as a negative aspect of leaving the EU. However, the corresponding increase in national sovereignty would also present an opportunity to remove or modify those aspects of EU legislation that the UK has opposed in the past, for example, the bonus cap for bankers and the framework for marketing and managing funds under the Alternative Investment Fund Managers Directive (“AIFMD”). The UK would need to negotiate its access to the EU markets through bilateral agreements. If one looks at the EU-Canada Comprehensive Economic and Trade Agreement (“CETA”), the EU appears to be more willing than in the past to create favourable terms for the financial services sector. For individual pieces of legislation where equivalence determinations are required, the UK could likewise request some kind of access on the basis that, while its laws do not mirror those of the EU, they achieve similar outcomes and there is no threat to the financial stability of the EU.

Whether and how UK businesses would have access to the EU after a vote to leave would depend on what substitute arrangements were negotiated between the UK and EU. Some financial businesses have announced that they would move some staff and operations to continental Europe, presumably if “passporting” was not replicated in a post-leave settlement. It is difficult to predict what would happen in any Brexit situation. However, it does seem inconceivable that the UK government would seek to manage a Brexit in such a way as to damage the City and broader national economy. It is also inconceivable that other EU countries would fail to achieve concessions (e.g. contributions to the EU budget) in return for such rights.

The converse situation of EU firms’ access to the UK post-Brexit would contrast starkly, at least under current laws. Pursuant to the UK’s “overseas persons exclusion,” all EU and non-EU firms have access to wholesale UK markets. This exclusion allows a non-UK firm to enter into certain regulated activities (such as dealing in derivatives as principal or agent) with UK client or counterparties from outside the UK, without needing to be authorised, provided that the firm enters into transactions with or through a locally regulated entity or if marketing laws are complied with. Presumably the overseas persons exclusion would continue to apply to EU firms if there was a vote for the UK to leave the EU. There are few EU countries that would give non-EU firms access as they have less liberal laws and the UK’s currently liberal approach should in principle be a strong global negotiating chip.

Cross-Border Passporting Regimes

A full exit from the EU would result in loss of access to the EEA financial market and the corresponding rights to freedom of trade and establishment. Various laws allow EEA banks, brokers, exchanges, fund managers, clearing houses, funds and payment service providers the right to “passport” into other EEA member states without the need for further regulatory approval. Passport rights can be exercised by either establishing a branch or providing services in the other member state. The basis of the EEA “passporting system” is founded in the Treaty on European Union and the EEA Agreement, in particular the freedoms of establishment and provision of services, but has been built upon in legislation by sector. Some freedoms of access have not been implemented or replicated in domestic UK legislation and are instead directly effective in the UK by virtue of the UK’s ascension to the EU or because they are in EU regulations.

In the absence of new access arrangements replacing the passport, UK financial institutions must establish subsidiaries or branches in the EU to be able to access investors or counterparties. Without that, access to the EU markets would be governed by the EU regime for third countries, including the equivalence framework (about which, see the discussion below). If the UK did not adopt new legislation that resulted in outcomes equivalent to that of the EU regulatory legislation, access to the EU markets in some sectors could be blocked.

Reduced Access to EU Financial Markets?

The EU has set up a framework through which financial institutions, insurers and reinsurers, funds and market infrastructure (trading venues, central counterparties, trade repositories, benchmark administrators and central securities depositories) established outside of the EU (third countries) can access European investors and markets. For these financial sector participants to access the EU markets, in addition to being properly authorized and supervised in their own countries, there are various requirements relating to the legal and regulatory regime of those countries that need to be fulfilled. The requirements vary by sector but typically revolve around the “equivalence” of the third country regime to the EU regime, co-operation arrangements between the third country and EU countries or the European Securities and Markets Authority (“ESMA”) and the anti-money laundering and tax arrangements in the third country.

Access to the EU markets for these UK-established financial sector participants will therefore depend on how closely aligned the UK’s legal and regulatory regime is to the EU regime. It is quite likely that initially the UK’s regime would be deemed automatically equivalent to the EU regime for those areas where the UK has already adopted EU laws (for example, under the European Market Infrastructure Regulation (“EMIR”)) but this depends on how the UK approaches grandfathering. For those areas where EU legislation is due to be introduced or which have not been fully implemented in the UK, equivalence determinations would need to be made and a negotiation would be required. Equivalence determinations can take time. The UK would need to ensure that its financial regulatory regime achieved similar outcomes to that of the EU regime if it wanted any immediate access. However, it would no longer have any input into deciding on the EU regulatory regime. Third country access can fall below the access given under a passport for many sectors.

For some kinds of UK entities that have obtained access to the EU markets by virtue of being established in an EU member state, the position is uncertain. For example, trade repositories are centrally regulated by ESMA and will have satisfied the conditions required for EU-based trade repositories under EMIR. Different requirements apply to non-EU trade repositories for which access depends on an equivalence determination (including, in this case, for the relevant country’s laws on professional secrecy), similar access to and exchange of information on derivatives contracts held by trade repositories in the third country and co-operation arrangements. In the interest of minimising market disruption, it is likely that any exit negotiations would include grandfathering provisions that allow a recognised UK trade repository to continue providing services subject to the relevant conditions being met by a certain date. This would require a new UK legislative framework for such bodies.

The Impact of MiFID II

For the passporting of investment banking businesses, the position could be largely unaffected at least in the medium to short term, depending on whether MiFID II was in effect. The current date for implementation of MiFID II is 3 January 2017. However, there is a legislative proposal to extend that date to 3 January 2018 and at the moment the actual date is uncertain.

MiFID II allows non-EU firms to provide services on a cross-border basis across the EU upon registration with ESMA, subject to those services only being provided to wholesale clients and the authorisation of the firm in its own country covering the same services. Registration with ESMA requires, amongst other things, an equivalence determination that the conduct and prudential rules of the relevant third country are equivalent to those in the EU. Non-EU firms that want to provide services to retail clients may do so through a branch which is authorised in the relevant member state. There is an EU passport for those branches under certain circumstances.

The timing of the UK’s exit from the EU, if there is a vote to leave, and the effective date for MiFID II is key for the passporting of investment business and how these businesses structure themselves to gain access to the EU markets and investors.

The above considerations would apply equally if the UK entered into a Customs Union with the EU or if it adopted the Swiss or the Canadian models. Each of these options is discussed below.

Joining EFTA and Re-joining the EEA

The Transition

EFTA was created in 1960 as a separate organisation from the European Economic Community (which is the precursor to the EU). Like the EU, EFTA’s goal is to establish free trade, but it opposes uniform external tariffs and does not include the establishment of supranational institutions such as the European Commission, Council of the European Union or the CJEU. There are currently four countries in EFTA—Iceland, Norway, Liechtenstein and Switzerland (the “EFTA States”). Iceland, Norway and Liechtenstein are also members of the EEA (the “EEA EFTA States”). The EEA is made up of the EU member states and the three EEA EFTA States.

The UK is currently a member of the EEA as a result of its EU membership. If the UK leaves the EU, it may re-join the EEA by joining EFTA as an EEA EFTA State.

There are various challenges, both legal and political, involved in joining EFTA. The existing EFTA States would have to agree to the UK’s accession to the EFTA Convention and the terms and conditions for doing so would need to be negotiated. The current EFTA States are fairly homogenous in terms of their size, economic development and trade preferences. They may have concerns regarding the UK’s suitability and other changes which could be perceived as being to their disadvantage.

From a legal perspective, the contractual route to leaving the EU and becoming an EEA EFTA State will likely require three new treaties. It will involve negotiations with all of the EU member states and the EFTA States. The agreements that will need to be entered into are between:

- all current EU member states on the UK’s withdrawal from the EU (or two years’ expiry past exit notice, as above);

- the EFTA States and the UK agreeing to the terms of the UK’s EFTA accession; and

- remaining EU member states, the EEA EFTA States and the UK, formalizing the UK’s EEA membership based on it becoming a member of EFTA.

The main differences between being an EU member state, an EFTA State and an EEA EFTA State are set out in Table A below.

Table A

| EU Member State | EFTA State | EEA EFTA State | |

|---|---|---|---|

| Veto in the European Council | √ | X | X |

| Right to be consulted on new EU legislation | √ | X | √ |

| Representation in the European Council | √

Note: The UK currently has a veto right. |

X | X Note: The EEA Council meets twice a year to discuss amendments to the EEA Agreement in line with EU policy and legislative developments |

| MEPs or Votes in the European Parliament | √ | X | X |

| Representation in the European Commission | √ | X Note: Potential for the UK to provide feedback on EU legislative proposals via independent working groups committees. |

X Note: Potential for the UK to provide feedback on EU legislative proposals via independent working groups committees. |

| EU Law supreme over national law | √ | X | X |

| EU Regulations directly effective | √ | X | X |

| Representation at the CJEU (e.g. judges or staff) | √ | X | X |

| Right to refuse to implement EU legislation or delay implementation | X | √ | √ |

| Independent seat at trade and standard-setting bodies | √ Note: the UK, unlike most other EU member states, has its own seat at the G20, Financial Stability Board and Basel Committee on Banking Standards |

√ | √ |

Legal Differences

In terms of substance, EU law will likely continue to apply in a similar manner should the UK become an EEA EFTA State. The EEA EFTA legislative process primarily consists of making “appropriate amendments” to the EEA Agreement to ensure that it reflects the body of EU legislation that is EEA-relevant. Once an EEA-relevant piece of legislation has been formally adopted by the EU, the Joint Committee of the EEA then decides whether to amend the EEA Agreement “with a view to permitting a simultaneous application” of legislation in the EU and the EEA EFTA States. All of the EEA EFTA States must agree to the adoption of the legislation. Unsurprisingly, the majority of EU legislation with EEA relevance is adopted by the EEA joint Committee into the EEA Agreement.

The EEA institutional structure also has supervisory mechanisms to ensure that implementation of EU legislation “with EEA relevance” is appropriately monitored. This structure mirrors the supervision of compliance by member states within the EU. Once implemented, EU legislation “with EEA relevance” is therefore enforced through the EFTA Surveillance Authority (which mimics the European Commission) and the EFTA Court (which mimics the CJEU).

Impact

As an EEA EFTA State, the UK would no longer have a right to negotiate or seek to influence EU law and policy as an EU member state. The EEA EFTA States have the opportunity to contribute to the work that the European Commission does before proposing new EU legislation. However, they have little or no formal opportunity to influence the Council of the European Union or the European Parliament who take the final decisions on all EU legislation.

As an EEA EFTA State, the UK would have some access to European markets, although access would be less than its current entitlement as an EU member state. As a counterpoint to this, the UK would increase control of access to its territorial waters for activities such as fishing. The UK would also no longer need to contribute to the “common agricultural policy” (a subsidy scheme for European (including UK) farming). However, access to EU markets for these activities and their products might become subject to tariffs. The UK would not be a part of the EU customs union, which means that any trade in goods between the UK and the EU would be subject to customs procedures and any beneficial rates could only be obtained if additional criteria were found to be met. The UK would need to negotiate its own trade and investment deals with countries outside of the EU. It could do this on its own or through EFTA. Such negotiations can take time and the outcome is uncertain.

There would be no automatic right to participate in the EU cooperation on police and criminal justice. The UK would need to negotiate a bilateral agreement with the EU to establish such arrangements.

Becoming an EEA EFTA State would, notably, include signing up to the “free movement of people” from both EU and EEA countries. The recently negotiated Settlement includes an “emergency brake” to limit full access to in-work benefits for new immigrants from the EU. That arrangement may be deemed inconsistent with the EEA Agreement and might therefore not be replicated if the UK leaves the EU and becomes an EEA EFTA State. EU immigration has been widely cited in public discourse as a key consideration for the politicians driving Brexit, such that becoming an EEA EFTA State may be unattractive to politicians in the event of a Brexit vote. However, not re-joining could, depending on what is agreed in its place, damage the City as a hub for Europe and affect the economy and jobs. Free movement of persons and free trade come hand-in-hand through EFTA.

Financial Services Sector

Retention of Cross-Border Passporting Rights

Joining EFTA and becoming an EEA EFTA State would mean that UK entities would retain their cross-border passporting rights. The passport rights would be based on the EEA Agreement instead of the Treaty on European Union.

Loss of Access to EU Financial Markets

To the extent that any EU legislation has not been incorporated into the EEA Agreement, the EU framework for entities established outside of the EU to access European investors and markets would apply to the relevant UK entities (see above discussion under “Complete Exit from the EU”). To date, there are several significant pieces of EU legislation which have not been incorporated into the EEA in the area of financial services, for example, EMIR. If EMIR is incorporated, then presumably a UK clearing house or central counterparty (“CCP”) would remain entitled to provide services in the EU and would not be considered a CCP that should be subject to the third country regime. The position is less clear for a UK trade repository. Unlike CCPs, which are authorised and supervised by regulators in their country of establishment, an EEA trade repository would be recognised and supervised centrally by ESMA. It is uncertain whether the UK would be willing to relinquish its regulatory role to an EU regulatory authority over which it has no power or influence. Some form of cooperation arrangement would need to be found.

Joining EFTA but Exiting the EEA: the Swiss Model

This would entail becoming an EFTA State (see discussion above) and leaving the EEA. The same position would apply for the situation where the UK opted to become an EEA EFTA State with regard to trade and investment deals with countries outside of the EU and cooperation on police and criminal justice. For access to the EU internal market the UK would need to negotiate bilateral agreements, which may take time.

Switzerland has only partial access to the internal market. Some products, such as agriculture, remain subject to tariffs. As a non-EU member state, some trade deals between the UK and the EU would be subject to the common external tariff. The EU imposes a common external tariff on exports from countries outside the EU, except those countries that have negotiated preferential trade agreements with it. The increased costs associated with any such tariffs would be compounded by additional administrative burdens, such as customs.

For the financial services sector, if not included in any of the bilateral trade agreements, the position would be the same as that discussed above under “Complete Exit from the EU.”

Customs Union: the Turkish Model

The UK could seek to participate in a Customs Union with the EU, similar to that which Turkey has negotiated. This would mean that the UK would have partial access to the EU markets. Customs checks would not be required for goods falling within the UK-EU Customs Union (which would depend on the outcome of negotiations). As part of a Customs Union, the UK would need to implement rules equivalent to the EU rules for the relevant areas, such as competition, environmental rules and State Aid. The UK would also need to negotiate trade agreements with any non-EU countries. However, tariffs under those agreements would need to match the EU tariffs.

The same implications for the financial services sector that apply to the Swiss model would apply under this model.

Free Trade Agreements: the Canadian Model

Under this model, there would be limited access to the EU markets but also fewer obligations on the UK. The UK would negotiate the market access arrangements and tariff levels with the EU and set quotas for trade between the EU and the UK. Negotiating trade agreements with the EU can be a lengthy process. CETA took seven years to negotiate. Currently, final approvals are pending before it can be implemented. The agreements are negotiated by the European Commission but must be approved by member states and the European Parliament.

While the EU acknowledges that CETA goes further than any other trade agreement, it does not grant Canada full access to the EU markets. If the provision of financial services was not included in any such trade agreement, the same issues that would arise upon a full exit from the EU would apply in this scenario (see discussion above).

Economic Analysis of Membership

To our knowledge, there has been no definitive cost-benefit analysis of the UK’s EU membership compared with the alternative models posed in this post. It is difficult to undertake an entirely comprehensive analysis as some costs and benefits associated with membership are subjective. There are also clearly other costs and benefits to the UK economy and taxpayer that come with being in the EU which are somewhat ephemeral and difficult to evaluate. Costs doubtless include additional government expenditure on public services as a result of the higher population. Benefits include those to business related to free trade, access to the single market and passport rights of financial institutions, and increased tax revenues from Europeans living and working in the UK under free movement rights. In 2015, it is estimated that EU membership cost the UK £8.5 billion through contributions to the EU Budget. Another is the economic cost associated with the implementation of EU regulations; this was estimated to be £33.3 billion in 2014. It has been forecast that future contributions to the

EU Budget, over the next four years, could fluctuate between £11.1 billion and £7.9 billion. If the UK enters into an agreement with the EEA EFTA States, it will have to contribute to the associated operational and administrative costs as set out in the EEA Agreement. The operational cost is calculated yearly based on the relative size of GDP of the EEA EFTA States, compared to the total GDP of the EEA. The annual contribution the UK would have to make under this model is based on a proportionality factor of the relevant EU budget line; in 2014, this was 3.03%. The administrative costs are less significant. The EEA EFTA States contribute to the costs associated with the administration of the European Commission, such as office rent. It is difficult to speculate on the extent of the UK’s contributions under an EEA EFTA agreement.

Other Issues

Human Rights

The European Convention for the Protection of Human Rights and Fundamental Freedoms (known as the “European Convention on Human Rights” or “ECHR”), along with immigration laws, is among the pieces of legislation highlighted in public discourse on Brexit as being objectionable. For example, the UK is under continuing pressure to change its law with regard to voting rights for prisoners as a result of various decisions by the European Court of Human Rights. However, this is not an EU body.

The UK has ratified the ECHR. It has also implemented the ECHR into its national law through the Human Rights Act 1998 (“HR Act”). The principal purpose of the HR Act is to give power to the UK courts to decide issues that fall under the ECHR, albeit that the courts must still follow the decisions of the European Court of Human Rights. Any judgment of the European Court of Human Rights under the ECHR is binding on the country to which the decision applies.

The HR Act provides that UK legislation must be given effect to the extent possible in a way which is compatible with the rights set out in the ECHR. If a UK court is satisfied that a provision of UK legislation is incompatible with one of those rights, it may make a declaration of incompatibility. Such a declaration does not affect the validity, continuing operation or enforcement of the provision and is not binding on the parties to the proceedings in which it is made. However, upon a declaration of incompatibility being made, the UK Parliament has powers to revoke or amend the relevant UK legislation.

If the UK votes to leave the EU, it would not cease membership of the Council of Europe and would remain in the ECHR. Both the ECHR and the HR Act would remain law. Therefore, any rights protected under the ECHR and HR Act would remain in place even if the UK votes to leave the EU. If the UK wished to withdraw from the ECHR, it would need to cease membership of the Council of Europe, which would be a separate matter.

The complete text, including footnotes and annex, is available here.