Print

PrintPaula Loop is Leader of the Governance Insights Center at PricewaterhouseCoopers LLP. This post is based on a PwC publication by Ms. Loop and Aaron Gilcreast. Related research from the Program on Corporate Governance includes The Long-Term Effects of Hedge Fund Activism by Lucian Bebchuk, Alon Brav, and Wei Jiang (discussed on the Forum here), The Myth that Insulating Boards Serves Long-Term Value by Lucian Bebchuk (discussed on the Forum here).

The numbers are sobering: nine of the Fortune-100 and 38 of the Fortune-500 companies dealt with an activist campaign in 2015. [1] And of the latter group, four were targeted more than once. [2] But hedge fund activism is not confined to only the largest public companies—all businesses, along with every industry and part of the world have become fair game.

Activists’ reach is growing wider, they’re getting bolder, and they are wielding even greater war chests. With $173 billion in assets under their management (AUM), [3] hedge fund activists are constantly looking for opportunities to profit from your blind spots.

Activists go after companies with vulnerabilities, and most companies have some. These could be related to financial performance, such as missing quarterly numbers, a stagnant stock price, or comparatively weak revenue growth. Or activists might target the board due to corporate governance issues.

But vulnerabilities may be in the eyes of the beholder. If companies want to get ahead of an activist threat, they’ll want to understand their potential vulnerabilities, including how an outside hedge fund activist might see things.

The new activist landscape

- Deep pockets, deeper involvement. Activists are a new class of hedge fund that has grown tremendously: their AUM have surged 268% from 2010 to 2015 alone. [4] They don’t just invest in a stock to make a profit; they shake up companies in which they invest and actively try to shape future performance.

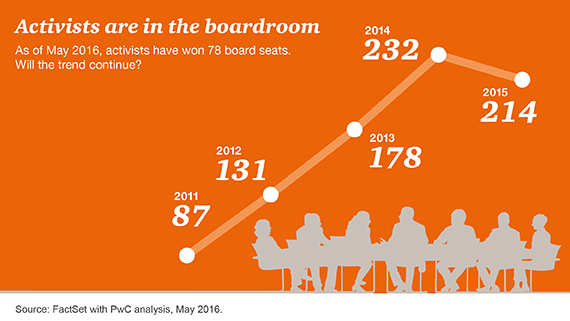

- Every public company is on notice. Neither size nor status is a defense. Nearly 1,300 unique companies were activated against from 2010 to 2015. In 2015 alone, 343 public US companies were targets; 113 have been targeted as of May 2016. [5] But that’s not the full picture—most estimate that the numbers double when you add approaches that aren’t public.

- Boards are talking—and taking action. Directors are well aware of the threat of an activist campaign: 49% of directors had extensive discussions about activism in the last year, [6] and many of those discussions included direct interaction with activists.

Understanding the big picture: the emergence of activism

Institutional investors dominate the equity markets today: the proportion of US equities owned by institutions has risen to about 68% in 2015 [7] from only 6% in 1950. [8] Many are long-term investors looking for a strong return: they have relevant perspectives about their investee companies’ strategy and direction, performance, and key risks, including cyber threats, CEO succession, and board composition.

They’ve wanted to engage and discuss these ideas, not simply follow management’s lead on the issues. But beyond shareholder proposals on governance issues, investors haven’t had any real means to push through their ideas. And institutional investors don’t always have immediate recourse if they want to exit the company: their time horizons, investment strategies, and the potential liquidity constraints related to selling large blocks of stock are issues they have to evaluate before making that decision.

Enter the hedge fund activists

Over the last decade, activist hedge funds increasingly started to populate the US investing scene. With the scale of assets under their management and their willingness to shake things up, institutional investors have been quick to ride their coattails. These activists will often look for a company’s weaknesses and then rally other investors who are also concerned, presenting to them their analysis of how they can improve shareholder value. Others will outline their concerns directly to the company, through white papers or letters to the board or CEO. And they won’t hesitate to use the media to make their concerns public.

If an activist launches a campaign, the target company shouldn’t be surprised to learn that the activist already has backing from its biggest institutional investors. This tag-team approach is a means for both to achieve their goals—and hold management accountable for creating shareholder value.

What’s at stake?

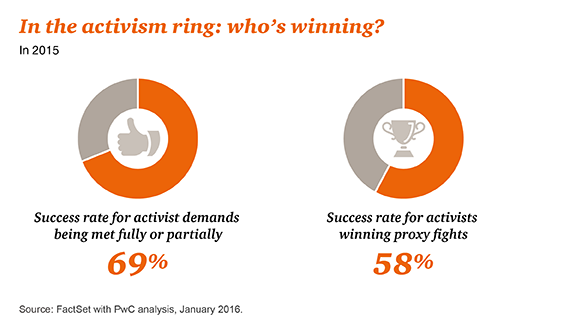

In most cases, activists seek changes to company strategy, the capital allocation plan, or even the CEO or members of the board of directors. Responding to some of these requests may result in dramatic changes, such as divestitures of underperforming businesses, increased share buyback programs, or changes to board composition. Activists frequently demand board seats in order to continue to drive their agenda and provide oversight to management.

Thinking like an activist to shore up the business

Company leaders and board members are taking stock of their financial and governance vulnerabilities and making efforts to understand what they mean to the company—including being a magnet for activist hedge funds. Recent volatility in equity markets and concerns about slow growth have companies thinking about new ways to increase and protect shareholder value.

Know your weaknesses

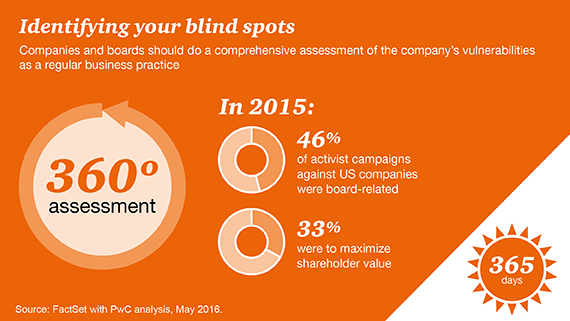

Companies may not see things the way activists do. They may think their strategy is working and everything is on track. But activists do their homework. Most often, activists do detailed reviews and analyses of the companies they target, looking at their cash balances, CEO performance, company holdings, operating margins, and even board composition. Red flags for activists might include unprofitable non-core assets, revenue growth that isn’t in line with that of peers, acquisitions that haven’t panned out, and overall poor performance.

Management and boards must take an honest look at their businesses. They also need to consider where activists might see a weakness, even if they do not. Then they need to address these vulnerabilities or put together a plan to defend them. Leaders also need to recognize that aggressive activists are not easily dissuaded; they will be relentless in their efforts to find weaknesses they can profit from.

The long-term goal: value creation

Companies should analyze where and how customers, products, and areas of the business create value for shareholders and then determine which areas have the highest potential for growth. Undertaking a granular analysis and assessment of the company’s current state can reveal weaknesses that activists might latch onto.

Some critics, including some institutional investors, charge that activists are short-term investors who look for a quick gain and then cash out. In early 2016, BlackRock CEO Larry Fink called for S&P-500 company CEOs to have a strategic framework for long-term value creation—one that articulates management’s vision and plan for the future—and share it with shareholders. [9]

Companies need to demonstrate how focusing on creating enterprise value—by building new products, engaging with customers, making smart capital investment decisions, and optimizing operations—will lead to improving shareholder value. Focusing on exceptional performance through a value-creation lens will naturally lead to strong stock performance. Companies that regularly outline how they’re doing this and how their plan is more valuable than a short-term gain should be able to garner the support of their institutional investors. This should provide a strong defense against an activist looking to entice those shareholders with a short-term gain.

Getting shareholders on your side through ongoing engagement

Engaging with shareholders about the company’s current state and its long-term strategic plan is one of the best antidotes to disruptions from activism. Begin by understanding who owns stock in the company. What are their motivations? Are they short- or long-term investors? How do they assess the company? This allows the company to tailor its messages to continue fostering shareholder support—giving it an information advantage over activists.

Communicate with your shareholders

Company management—and sometimes board members—should engage with their biggest shareholders about company strategy (and the board’s involvement), its capital allocation plan, how executive compensation is linked to strategy, and why the board is made up of the right directors to oversee the company in the future. [10] They should also listen to shareholder concerns and opinions, addressing them and working through any issues.

Explaining how certain decisions are directly linked to strategy can address concerns. And communicating the company’s value story and how it’s taking steps to achieve its strategic goals can help secure alignment. One company was able to fend off a hedge fund activist’s calls to split into two by having a strategic plan in place that delivered growth and defending that business model. The company addressed market changes and regularly communicated the strategy to investors in statements, on earnings calls, and in media interviews.

The key here is to get your shareholders to understand and buy into your plan before the activists show up. Activists will have a much harder path if the company has already cultivated relationships with shareholders and shareholders are content with the strategy as communicated. One hedge fund activist lost a proxy battle after shareholders re-elected all company board nominees, thanks to its strong history of engaging with and responding to shareholders. Another company defeated an activist by expanding its engagement outreach beyond institutional investors to retail shareholders, who often are loyal to management, to win their support.

Entertaining activist concerns

Companies will want to consider engaging with activists, too. Listening to what an activist has to say can foster negotiation and prevent what could become an antagonistic situation down the road. Some companies have learned the hard way. For example, after a year of recommending to the company numerous business and management changes—from creating a separate company for two holdings to how it prepares its products—and being rebuffed, one activist successfully replaced the company’s entire board.

Not all interaction with an activist is contentious; some companies negotiate with activists to prevent the disruption that comes with a long and expensive proxy fight, sometimes offering them a board seat. Others might learn from the different perspectives, ideas, and insight an activist brings to the table.

Three steps for staying ahead of activists

The tandem strategy of self-analysis and engagement is not a one-and-done event. It’s an ongoing process that requires critical analysis from different perspectives and continuing two-way dialogue.

Keep your eyes on the ball

Companies and boards need to check their vulnerabilities, prepare for the threat of an activist attack, and engage with shareholders on a regular basis. View engagement as an active, not a passive effort.

The board also needs to emphasize its independent oversight and be able to withstand scrutiny regarding its tenure and composition, including diversity. Continual refreshment ensures having the right people in the boardroom for effective oversight.

How to get up to speed

Whether they’ve won a board seat or have only just purchased a stake in a company’s stock, activists are the new player at the table for many companies. And they’re not going away any time soon. Companies have advantages over activists—but only if they recognize and use them. Here’s how they can be their own best advocates:

- Tap your knowledge of the inner workings of the business. Activist investors may be smart, have deep pockets, and hold the megaphone with the media, but management has the deep knowledge of the business and customers that activists don’t: details and nuanced information about operations, customers, markets, and competitors, and which are driving profit. With this knowledge, company management should be able to confidently outline plans to deliver on growth opportunities.

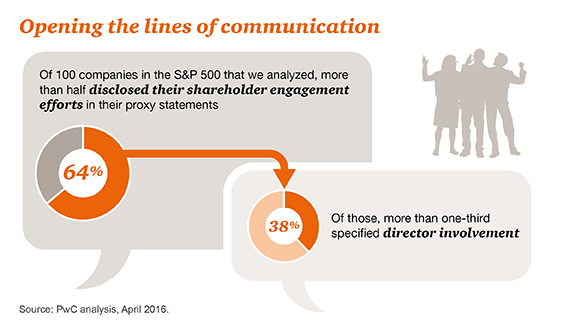

- Build better relationships and increase transparency. Many companies, including board members, are directly communicating with their shareholders to understand their concerns. Some do so annually. Other companies are starting to outline how they’re engaging with their shareholders in their annual proxy statement or other reporting, listing topics they discuss, the purpose for direct dialogue, and the frequency of engagement.

- Create robust processes to assess vulnerabilities and engage with investors. Companies can use a risk assessment tool to spot weaknesses and then evaluate their gravity. They can frame informed responses to explain why they are making certain decisions or to change track.

An engagement plan should be comprehensive and include analyst calls and meetings, one-on-one investor meetings, letters to shareholders, investor days, and transparent proxy disclosures and SEC filings.

Endnotes:

[1] FactSet with PwC analysis, January 2016.

(go back)

[2] Ibid.

(go back)

[3] Activist Insight Annual Review 2016, January 2016.

(go back)

[4] FactSet with PwC analysis, May 2016.

(go back)

[5] Ibid.

(go back)

[6] PwC, 2015 Annual Corporate Directors Survey, October 2015.

(go back)

[7] PwC + Broadridge, ProxyPulse, Third Edition 2015, September 2015.

(go back)

[8] The Conference Board, The 2010 Institutional Investment Report, November 2010.

(go back)

[9] Matt Turner, “Here is the letter the world’s largest investor, BlackRock CEO Larry Fink, just sent to CEOs everywhere,” Business Insider, February 2, 2016.

(go back)

[10] When engaging, companies and boards must be aware of and comply with Regulation Fair Disclosure.

(go back)