Print

PrintRobbie McLaren and Nick Cline are partners at Latham & Watkins LLP. This post is based on a Latham publication by Mr. McLaren, Mr. Cline, and Catherine Campbell. This post is based on a publication in IFLR’s Mergers and Acquisitions Report 2017.

Britain’s decision to leave the European Union in June 2016, coupled with the election of Donald Trump as US president in November 2016, gave dealmakers plenty of pause for thought last year—but ultimately did little to derail strategic M&A. Encouraged by the post-Brexit decline in the value of sterling and supported by the continuing availability of transaction financing at attractive rates, the number of acquisitions of UK companies by US acquirers reached the highest level in 10 years, with 262 deals valued at US$48 billion closing in 2016.

With attractively priced credit predicted to continue to finance M&A transactions throughout 2017 and foreign buyers continuing to regard the UK and Europe as an attractive investment opportunity, there are strong indications that inbound UK and European M&A activity from the US will continue. In our view, transatlantic deal makers will increasingly encounter the following key deal term differences between the US and UK M&A markets.

Transaction Accounts: Completion vs. Locked Box

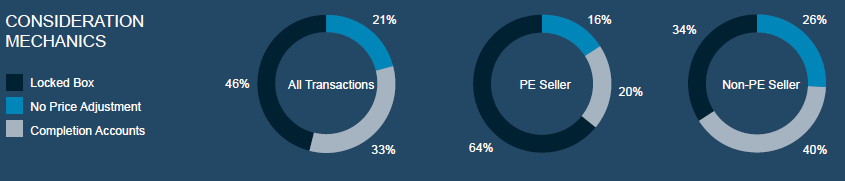

In the Latham & Watkins 2016 European Private M&A Market Study (which examined over 170 deals signed between July 2014 and June 2016) as much as 46% of European deals included a locked box mechanism. 33% of deals included a completion accounts mechanism and 21% of deals did not provide for price adjustment. In contrast, locked box mechanisms are significantly less common in the US, where the majority of deals use completion accounts. Locked box mechanisms fix the deal price at an agreed date based on a set of accounts, with the seller giving undertakings that value will not be extracted, or leak, from the target before completion. In contrast, a completion accounts mechanism calculates the final deal price after completion, by reference to accounts relating to the target, drawn up to the date of completion. This allows the buyer to test and adjust its valuation by reference to the actual financials of the target.

The prevalence of locked box mechanisms in Europe reflects the historic seller friendly European M&A market.

In our view, 2017 may see a shift in the prevalence of locked box mechanisms in Europe, as private equity buyout firms (who traditionally favour locked box accounts) seeking to deploy record amounts of unspent capital, compete against US acquirers (who traditionally favour completion accounts) with a keen interest in Sterling transactions.

Will Tax Changes Impact Deals?

The reduction of the headline UK corporation tax rate increased the attractiveness of the UK as a holding company jurisdiction in 2016. While the UK is still behind Ireland and the Netherlands in terms of overall number of US-listed holding companies domiciled, recent transaction trends point to the UK being favoured. Further, the introduction of restrictions on interest deductibility in the UK will limit the amount of debt that companies can set off against tax and may impact historic deals and new acquisitions, giving cash rich US corporate acquirers an advantage over other purchasers who rely on debt to fund transactions.

Anticipated changes to the way that US companies are taxed will surely impact deal structures. The US House of Representatives’ proposed plans are expected to incentivise US companies to repatriate cash currently held overseas, which may bring an estimated US$2.5 trillion in foreign profits stored outside of the US, back to the US. The eventual impact of the prospective changes in the US is currently uncertain but may include changes to the US tax regime on interest deductibility and the territorial taxation (and rates of taxation) of US based multinationals’ overseas earnings. These changes may, over time, result in fewer inversion style transactions and influence the attractiveness of the UK and other European countries as holding company jurisdictions, possibly driving US multinational businesses to US parented groups. Alternatively, there may be structural advantages to holding deal leverage offshore.

Conditionality: Are We There Yet?

UK and US dealmakers take different approaches to deal conditions, the satisfaction of which is required before a deal can complete. In European deals, conditionality beyond regulatory and antitrust conditions is uncommon with business risk typically transferred to the buyer on signing, as is the case, from an economic perspective, on a locked box deal. Under US practice, deal and business risk is typically not transferred until completion. While completion conditions will vary, in a US led deal, conditions may include a requirement for the seller’s representations and warranties to be materially accurate at completion and absence of a material adverse change.

With increasing numbers of US acquirers in the European market, European deal makers can expect a greater range of deal conditions requested than in the past. Those buyers considering how to mitigate risks of potential US tax changes should note that material adverse change clauses are unusual in Europe and, in any event, tax change is seldom included as a change event, even in US deals. Deal makers should not assume that transactions can be cancelled if attractiveness is eroded by new tax legislation. Instead, specific conditions, representations or warranties should be sought and acquisition structures developed to allow as much flexibility as possible.

Looking ahead, 2017 will clearly be another year of global political uncertainty. Notwithstanding the political turbulence, the M&A market remains in good shape. Last year global M&A continued through some of the biggest political shockwaves in years, and we expect it to do the same in 2017. In a world increasingly difficult to predict, deal makers will need to use global M&A terms and terminology to navigate key risks.