Print

PrintRobert Kalb is a Senior Associate at Institutional Shareholder Services, Inc. This post is based on an ISS publication by Mr. Kalb. Related research from the Program on Corporate Governance includes The Untenable Case for Perpetual Dual-Class Stock by Lucian Bebchuk and Kobi Kastiel (discussed on the Forum here).

For many years, companies have often held their initial public offerings (IPOs) while maintaining potentially shareholder-unfriendly features, such as multi-class share structures, restrictions on shareholders’ ability to amend bylaws, supermajority vote requirements, and classified boards. Arguments for those practices include giving management room to maneuver during its initial public years, protecting certain shareholder classes, and more. Recently, however, shareholder tolerance for these features has waned, with proxy advisers following suit as reflected in their voting policies and recommendations.

Shareholders Increasingly, But Still Tentatively, Expressing Frustration Through Votes

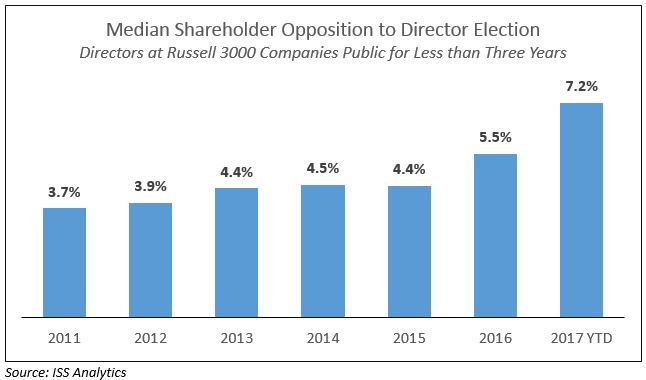

Shareholders are starting to express their views at the proxy ballot box. We focus our attention on director elections at new companies—defined as director elections held less than three years from a company’s IPO date. Among this group, the proportion of directors receiving less than 80 percent shareholder support has increased from 1.5 percent in 2011 to 6.5 percent in 2016. Four directors among this group failed to earn majority support in 2016—up from zero in 2011. Looking more broadly at support for directors at these newly-public companies, we also find new trends. Median opposition for directors at these newly-public companies has doubled since 2011 (although voting data for 2017 is still relatively limited, with peak meeting day in the U.S. occurring next week).

ISS Policy Shifts to Hold IPO Companies Increasingly Accountable

Over the past several years, ISS has had many conversations with institutional investors regarding shareholder rights issues at newly-public companies. For example, last year, ISS’ annual Global Policy Survey addressed one of these points, asking market participants “Should ISS policy also consider recommending voting against the directors if the company, when it goes public or emerges from bankruptcy, has a structure that includes multiple classes of stock with unequal voting rights?” Fifty-seven percent of investor respondents agreed, with another 24 percent expressing that support for the director should be contingent upon a sunset provision on the unequal voting rights.

In response, ISS clarified and updated its policy on director elections in late 2015, and again in late 2016, most recently saying:

For newly-public companies, generally vote against or withhold from directors

individually, committee members, or the entire board (except new nominees, who should be considered case-by-case) if, prior to or in connection with the company’s public offering, the company or its board adopted bylaw or charter provisions materially adverse to shareholder rights, or implemented a multi-class capital structure in which the classes have unequal voting rights considering the following factors:

- The level of impairment of shareholders’ rights;

- The disclosed rationale;

- The ability to change the governance structure (e.g., limitations on shareholders’ right to amend the bylaws or charter, or supermajority vote requirements to amend the bylaws or charter);

- The ability of shareholders to hold directors accountable through annual director elections, or whether the company has a classified board structure;

- Any reasonable sunset provision; and

- Other relevant factors.

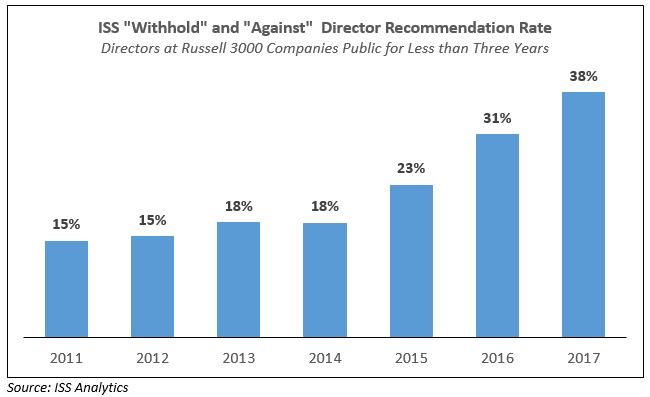

The impact of this updated policy has been pronounced. Today, ISS’ adverse vote recommendation rate on directors at companies within the Russell 3000 and public for less than three years is 23 percentage points higher than it was in 2011.

New IPO Companies Beginning to Introduce More Favorable Shareholder Rights

Notably, companies are responding as evidenced by movement on the issues at newly-IPO companies. For instance, when Valvoline, Inc. completed its spinoff from Ashland, Inc. in September 2016 it retained an 80 percent supermajority vote requirement to amend its bylaws and certain sections of the charter. At its first annual meeting on Jan. 24 certain members of the nominating and governance committee received vote support of less than 95 percent, significantly below the median of all director elections across the Russell 3000 (including non-IPO companies). Valvoline subsequently called a special meeting on April 26 for the sole purpose of requesting shareholders approve an amendment to the charter and bylaws to phase out the supermajority requirement in favor of a simple majority over a period of three years. This proposal was overwhelmingly supported.

Several other newly-public companies have publicly committed to put proposals to reverse these adverse provisions on the ballot at their 2018 annual meeting. Exterran Corp and California Resources Corporation shareholders will see 2018 management proposals to reduce supermajority vote requirements, while Babcock & Wilcox Enterprises and SPX Flow, Inc. shareholders will see shareholder proposals to both declassify the board and reduce supermajority vote requirements.

With the exception of Valvoline, where Ashland currently retains a controlling stake, each of the other mentioned newly-public companies were spun off from their former parents. As a result, from the start of their trading the shareholder bases were diversified with significant institutional shareholder ownership.

More Mature Companies Making Shareholder Rights Improvements, Too

It’s not just IPO companies that are feeling the pressure. Anthem Inc. and Columbia Property Trust, Inc. placed management proposals on the ballot this year to amend governing documents to provide shareholders the right to amend the bylaws. While Anthem shareholders will convene on May 18, Columbia Property shareholders overwhelmingly passed this amendment on May 2.