Print

PrintAdam M. Kanzer is Managing Director at Domini Impact Investments LLC. This post is based on a Domini publication by Mr. Kanzer. Related research from the Program on Corporate Governance includes Private Ordering and the Proxy Access Debate by Lucian Bebchuk and Scott Hirst (discussed on the Forum here).

This has been a historic proxy season, marking three majority votes for shareholder proposals addressing climate change at Occidental Petroleum, PPL Corp. and ExxonMobil, with the latter proposal exceeding 60% support. As of this writing it is too early to tell which asset managers voted for these proposals, with the exception of BlackRock, which announced that it voted for the proposal at Occidental (Vanguard also reportedly supported that proposal). This year, Fidelity announced that it may support shareholder proposals on sustainability matters and both BlackRock and Vanguard said they were strongly weighing supporting the ExxonMobil proposal.

So-called “mainstream” asset managers are waking up to the significant risks posed by climate change and other sustainability issues at the same time that the business community is moving aggressively to ensure that these managers do not have the opportunity to support such proposals in the future.

Last year, the Business Roundtable (BRT) published a proposal to “modernize” the legal process shareholders use to submit shareholder proposals. These ideas were submitted to the White House and have now found their way into the Financial CHOICE Act (Section 844), currently under consideration by Congress. This provision would raise the threshold to submit a shareholder proposal from $2,000, held continuously for one year, to 1% of market capitalization, held for three years (the BRT proposed 0.15% of market capitalization). The Act would also raise the vote thresholds for resubmission of proposals and eliminate the ability to submit proposals “by proxy.”

These ideas have also been championed by Nasdaq, in a recent report, “The Promise of Market Reform: Reigniting America’s Economic Engine” (Discussed on the Forum here). At the same time that Nasdaq has led important work at the World Federation of Exchanges to promote greater corporate disclosure of environmental, social and governance (“ESG”) information, it has launched a set of ideas that undermine these efforts and, in some places, explicitly contradict them. [1]

If fully implemented, these ideas would effectively prevent shareholders from engaging corporations through the shareholder proposal process, a process that has catalyzed thousands of constructive engagements with corporations to the benefit of shareholders, corporations and the broader society.

Weakening the ability of shareholders to exercise oversight of the companies they own is no solution to a decline in IPOs, short-termism or wealth inequality, all issues that appear to have motivated Nasdaq’s set of proposals for capital markets reform. [2] It strains credulity to assert that entrepreneurs are choosing to forego an IPO because they fear they may, at some point in the future, receive a non-binding shareholder proposal. It is also counter-intuitive to assert that a proposal to silence a company’s long-term investors will do anything but exacerbate short-termism.

These recommendations to “reform” the shareholder proposal rule are founded on several misconceptions and factual errors, as outlined below.

Rule 14a-8 is a Cost-Effective Tool for Managing Long-Term Risk

Any assessment of the efficacy of a rule should consider both its costs and its benefits. I address some of the problems with the highly exaggerated cost estimates we have seen, below. The larger problem with these assertions, however, is that they ignore the substantial benefits to corporations, investors and the U.S. capital markets that SEC Rule 14a-8—in its present form—provides. It is a cost-effective, market-driven mechanism to surface emerging risks and provide guidance to corporations on how to address them.

In addition to making substantial contributions to long-term risk management, particularly in terms of the management of externalities, the shareholder proposal rule has also enhanced (not “poisoned,” as Nasdaq’s report claims) corporate relationships with a broad range of shareholders. Speaking from my personal experience submitting shareholder proposals over the course of nearly twenty years, I can point to numerous constructive, long-term relationships with corporations that began with the submission of a shareholder proposal. Each year, the number of proposals we submit are a small fraction of the number of companies we engage. [3] Our goal is to build long-term constructive relationships with companies in our portfolios in support of long-term broad-based wealth creation. We have found the shareholder proposal to be a critical tool in this process, to initiate engagements and to accelerate progress when we cannot move forward on a pressing issue. We have also seen conversations with companies end the moment a 14a-8 no-action request was granted.

Corporations that only confer with their largest shareholders are not getting the full picture. We certainly cannot expect a publicly traded company to speak with all of its shareholders. The shareholder proposal process provides those of us with smaller stakes, but good ideas, an opportunity to speak. Very often, these are ideas the board has not previously considered, or did not view as important to its shareholders.

Shareholder proposals provide an early warning of risks a company may not be aware of, as well as an opportunity to gauge investor sentiment on a wide range of issues. It is the only mechanism that provides companies with insight into the concerns of its entire shareholder base, without committing the company to action. I would also note that consultants charge companies hundreds of thousands of dollars for the kind of detailed guidance on policy development and public reporting that is provided free of charge by shareholder proponents due to our long-term interest in the company.

The “Costs” of 14a-8 Don’t Add Up

In a recent op-ed, “Shareholders are costing their companies—and calling it democracy,” Maria Ghazal, the BRT’s General Counsel, claims that the shareholder proposal process “costs companies tens of millions of dollars and countless hours of time, which diverts resources focused on creating long-term value for their shareholders.”

The exaggerated cost claims promoted by the Business Roundtable, the U.S. Chamber of Commerce and Nasdaq appear to be based on the assumption that public companies face a deluge of shareholder proposals, which imposes a severe financial burden. Nothing could be further from the truth. I believe it is accurate to say that the vast majority of public companies have never received a shareholder proposal. In addition, the “costs” to the companies that receive proposals (setting aside the clear benefits noted above) are largely self-imposed, as companies choose whether to challenge a proposal and choose whether to hire outside counsel to do so.

I have not seen any reliable data on the costs to companies of shareholder proposals. The only meaningful expenditures I can see are the expenditures of executive and board time on the issues presented. Presumably, time spent is correlated with the importance of the issue. It is therefore time well spent.

Ms. Ghazal claims that this process costs companies “tens of millions of dollars.” This is an extraordinary claim. What is the source for this figure? Ms. Ghazal links to a rulemaking petition filed with the SEC by the U.S. Chamber of Commerce that cites a U.S. Chamber-funded study on the costs and benefits of Rule 14a-8, conducted by Navigant. The Navigant study cites a comment letter submitted to the SEC in 2003 by Professor Stephen Bainbridge, who calculated that all shareholder proposals submitted for the 2003 proxy season—in aggregate—cost companies a total of $90,654,000 based on an estimate of $87,000 per proposal. This materially misleading figure is drawn from a 1998 SEC Release which included the results of a survey on 14a-8 costs.

Anyone who chooses to follow this breadcrumb trail all the way to its end will find little to satisfy their appetite.

Professor Bainbridge states that “according to the SEC’s own figures, the cost per company of determining whether or not a 14a-8 proposal should be included in the proxy statement is $37,000 and the direct cost per company of including a proposal is $50,000.” But these were not the SEC’s “own” figures, they were averages drawn from a congressionally mandated survey the Commission conducted on the shareholder proposal process. The SEC divided these costs into two categories—the cost to determine whether to include or exclude a proposal, including legal fees, and the costs to print and distribute shareholder proposals. It is also important to note that the 1998 Release contained changes to the Rule that the Commission expected would reduce the costs of compliance for both companies and shareholders. [4] The survey responses reflected the status of the Rule prior to the implementation of those cost-saving measures.

Before examining these figures, it is also important to note that they are averages, based on a very wide range of responses. For example, the reported costs to determine whether or not to include a proposal ranged from a low of $10 to a high of approximately $1,200,000. The median cost was $10,000. A $1.2 million expense to address a non-binding shareholder proposal is not credible, and this extremely wide band suggests that the question may have been subject to vastly different interpretations.

Legal Costs: The SEC noted in that Release that “no commenters submitted empirical data demonstrating how much it costs companies to consider and prepare an individual no-action submission under rule 14a-8.” The SEC reported an average of approximately $37,000 based on responses from 80 companies, to determine whether to include or exclude a proposal, including legal fees. As the Commission noted, legal costs are within the company’s control. [5]

Printing and Distribution Costs: The SEC noted that the average cost reported by 67 companies to print and distribute shareholder proposals was approximately $50,000. [6] The SEC noted that these responses may have included more than one proposal.

These costs have everything to do with the overall cost of printing and distributing proxy materials, and nothing to do with Rule 14a-8, which adds roughly one page to a lengthy document. Each proposal is limited to 500 words (the Board may, at its discretion, include a statement in response, generally a statement in opposition). This estimate would therefore amount to $100 per word, or $50,000 per page (there will be no additional postage costs to add one page to a corporate proxy statement). This seems unreasonably high. [7] If the Chamber and the BRT are going to continue to use this figure for printing and distribution costs, they should apply it to all printed pages. For example, this estimate suggests that J.P. Morgan Chase spent $2,250,000 to print and distribute Jamie Dimon’s 45-page letter to shareholders in its most recent Annual Report.

Professor Bainbridge notes that his $87,000 figure is based on the assumption that corporations seek to exclude all proposals, an assumption that Professor Bainbridge himself noted was “doubtful.” The figure is therefore, by his own admission, clearly too high. In fact, corporations do not seek to exclude all proposals. In 2016, 27% of proposals were challenged, meaning that legal expenses for roughly three quarters of the proposals presented were nominal.

In any case, it makes little sense to combine these figures. If a no-action request is granted, there will be no printing costs, and roughly 60% of 14a-8 no-action requests are granted each year. A company may also balance the nominal cost of printing a proposal against the higher costs of challenging one, or choose to handle the legal challenge in-house, a choice many companies make.

Nasdaq claims that “The current process is costly, time-consuming and frustrating for companies, which in aggregate must address thousands of such proposals each year.”

This is simply false. According to Gibson, Dunn & Crutcher, a law firm with an active 14a-8 no-action practice on behalf of corporations, between 2013 and 2016, the number of proposals submitted to companies ranged from 820 to 916. There is no support for the assertion that companies must address “thousands” of proposals each year.

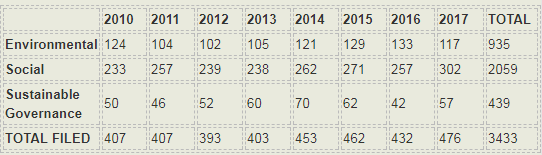

The Sustainable Investments Institute (Si2) tracks shareholder proposals relating to sustainability. The table below[8] provides data for all such proposals from 2010—2017. [9]

Further, the proposals that are filed tend to be concentrated at high-profile large cap companies, which often receive more than one. Very few small or midcap companies ever receive a shareholder proposal.

An Ad Hominem Attack on Investors—No Proposals for the 99%

Nasdaq claims that the reforms it recommends would “ensure that shareholder proposals representing the views of a meaningful percentage of the companies’ long-term owners are considered at shareholder meetings” and argues that raising the minimum ownership amount and lengthening the holding period will “ensure proposals have meaningful shareholder backing.”

It is good to see Nasdaq’s recognition that there is value in considering proposals representing the views of a meaningful percentage of a company’s long-term owners. In fact, the current process already provides for this. According to Gibson Dunn data, shareholder proposals received an average of 32% support over the past four years, certainly a meaningful percentage of any public company’s shareholder base.

Nasdaq’s assumption is ill-founded, and contrary to the math. In reality, the proposal to raise the ownership threshold to 1% (or to the Business Roundtable’s 0.15%) would ensure that no shareholder proposals are submitted as no current proponent, including the largest pension funds in the United States, would be able to meet the 1% threshold. [10]

Raising the ownership threshold for submission of proposals would do nothing to ensure that a proposal has “meaningful shareholder backing.” Literally, it would only ensure that a proposal had the backing of 1% of a company’s shareholder base, which wouldn’t even be high enough to permit the proposal to be resubmitted.

The push to raise the ownership threshold is misguided. The problem is not simply that the CHOICE Act and the BRT overshot the mark with an unreasonably high threshold—the problem begins with a mischaracterization of the purpose of the ownership threshold in the first place.

This effort is based on the assumption that small investors don’t have any good ideas, or don’t have any legitimacy. It implies that 99% of a company’s shareholder base can be ignored and that companies should pay attention to 1% owners but ignore 30% votes—solely based on the identity of the proponent, rather than the quality of the ideas presented. The idea that only large investors have sufficient ‘skin in the game’ to have sensible ideas is easily discredited by the actual vote results of proposals submitted by small investors each year.

The current low ownership threshold combined with the one year holding requirement ensures that the proponent is an actual shareholder. It is not intended to distinguish between shareholders, or to suggest that one class of shareholder has greater legitimacy to raise an issue than any other. The ultimate test of the idea presented is the vote, not the amount owned by the proponent.

Any change to the ownership threshold raises the same set of problems. There is no principled way to raise it without disenfranchising most individual investors and many institutional investors as well. A 1% threshold would certainly exclude Mr. Chevedden and Mr. McRitchie, the most prominent individual shareholder proponents, but it would also exclude all other proponents. This is the proverbial “nuclear option” and is unwarranted.

Although the vast majority of proposals are submitted by fiduciaries, it must be recognized that small, individual investors were the first to use the Rule, and have played an important role in reforming corporate governance practices throughout its history. [11]

The quality of one’s ideas is not correlated with the size of one’s investment. The current rule allows an individual with a good idea to present that idea to a company’s shareholder base. If that individual’s idea garners significant support, this should be viewed as a strength of the process, not a weakness. [12]

The corporate backers of this idea to raise the ownership requirements are, frankly, seeking to eliminate potentially successful proposals on subjects they do not like by focusing on the identity of the proponent. It is the classic ad hominem attack. This is a patently illegitimate strategy, contrary to the public interest and to the long-term interests of investors.

No one percent owner that we are aware of has ever submitted a shareholder proposal, although they may vote for them from time to time. Large so-called “mainstream” money managers are paying greater attention to the financial risks of sustainability issues, including climate change. The BlackRock vote is not an anomaly, it is a sign of things to come.[13] The largest asset managers are unlikely to ever submit a shareholder proposal, but they should not be denied the opportunity to vote for them.

The shareholder proposal rule is not designed for use by a company’s largest investors. Such investors already have direct access to senior management and the board. We applaud these successes at ExxonMobil, Occidental and PPL, but note that these proposals are non-binding. As a gauge of investor sentiment, a proposal need not obtain a majority vote to succeed. Many prudent companies are willing to act on an idea supported by a significantly smaller percentage of its shareholder base.

According to the EY Center for Board Matters’ review of the 2016 proxy season, proxy access proposals, the most common issue presented last year, averaged close to majority support, with an average of 59% support when excluding companies that had already adopted proxy access by the time the proposal came to a vote. Average support for climate risk proposals rose to 28% from only 7% in 2011 including one proposal that received a 49% vote.

Further, according to EY, “The percentage of shareholder proposals withdrawn before going to a vote is 26%, which is consistent with recent years.” This significant withdrawal percentage is the sign of a healthy process of engagement. It also represents win-win outcomes, further validating the usefulness of the process. If companies are reaching agreement with shareholders, we must assume they are doing so because the ideas presented are in the company’s best interests.

The SEC’s No-Action Process Already Ensures Proposals are Proper

Nasdaq challenges investors’ “ability to include an issue on the company proxy for a shareholder vote, even if the issue is not material or relevant to the company’s business”and is seeking to “ensure that proposals considered at annual meetings are properly placed before shareholders [and] are meaningful to the business of the company, and not related to ordinary business matters.” Jamie Dimon went so far as to complain about “shareholder meetings that are hijacked by special interest groups and become a complete farce” and “proposals not intended to benefit the company.”

- These concerns are misplaced. There is already an effective process in place to ensure that proposals are “properly presented,” are relevant to the company’s business, and do not improperly focus on ordinary business matters. This process is administered by SEC Staff.

According to Gibson Dunn, in 2016 companies submitted 245 no-action requests to SEC Staff, and 143 (67.8%) were granted. Thirty-two percent of these exclusions were granted based on the Rule’s “ordinary business” exclusion. Only 27% of the 916 proposals submitted were challenged by companies, representing a tacit acknowledgment that the proposal was consistent with SEC rules and did not improperly interfere with management and the board’s purview over ordinary business matters.

- There is therefore no basis for the claim that any significant portion of shareholder proposals are irrelevant or inappropriately interfere with “ordinary business” matters. Such proposals are currently excludable under SEC rules and SEC Staff regularly enforces this rule. Proposals that are deemed by investors to be ‘irrelevant’ to a company’s business are ultimately eliminated by the Rule’s vote resubmission thresholds.

Rule 14a-8’s Resubmission Thresholds Ensure Emerging Risks are Addressed

The CHOICE Act contains two additional provisions that threaten the efficacy of the shareholder proposal rule.

The Act would dramatically raise the proposal resubmission thresholds. This is a dangerous idea, which would immunize corporations from considering emerging risks. Many critical risks have been raised in shareholder proposals long before they became obvious to the market, including predatory lending, off-balance sheet transactions and climate change. These issues took time to gain support, and the SEC’s current resubmission thresholds permitted that to happen. As noted above, just to cite one example, EY reports that average support for climate risk proposals rose to 28% in 2016 from only 7% in 2011, including one proposal that received a 49% vote. This year, as noted above, two climate risk proposals received majority votes. We would expect that trend to continue, as it has for many other issues over time.

The Act would also interfere with the state law of agency by prohibiting issuers from including in proxy statements proposals submitted by a “proxy, representative, agent or person otherwise acting on behalf of a shareholder.” This provision would interfere with a range of actors, including attorneys and financial advisors, and would even prohibit issuers from voluntarily publishing proposals submitted by agents.

Rule 14a-8 Serves the Best Interests of Long-Term Investors

Ms. Ghazal argues that: “Reforming shareholder proposals could enable companies and shareholders to focus on the issues that really matter to long-term performance: a company’s business plans, its investment strategy and its future in a dynamic marketplace. This is essential to creating long-term value, good-paying jobs and innovative products and services—the underpinnings of a sound economy.”

Shareholders and corporate managers often have disagreements about what “really matters” to long-term performance. Arguably, that’s the point of the shareholder proposal rule. We cannot have a conversation about these key questions if only one side is interested in talking.

In my personal experience, large corporations do a better job reaching out to shareholders, and responding to our inquiries, than they did ten or twenty years ago. But there are still many companies that will not talk to us unless we submit a shareholder proposal. And there are other times when we are unable to reach agreement on a particularly pressing issue and determine it Is worthwhile to put it to a vote. We have even had executives tell us that, in certain cases, a shareholder proposal would be helpful.

Nasdaq notes that its proposal would “enable the Commission to utilize data and input from investors to determine what is in the best interests of long-term shareholders.“

Long-term investors have already spoken. These changes would disenfranchise virtually all investors, but would have a particularly negative impact on long-term investors.

The current rule is already in the best interests of long-term shareholders. In a letter to Gary Cohn, Director of the White House National Economic Council, the Council of Institutional Investors, the UN Principles for Responsible Investment, US SIF, the Interfaith Center on Corporate Responsibility and the Investor Network on Climate Risk, investor organizations representing more than $65 trillion, wrote:

“Our members are long-term shareholders who can attest to the fact that for over 45 years the shareholder proposal process has served as a cost effective way for corporate management and boards of directors to gain a better understanding of shareholder priorities and concerns and to benefit from those insights on critical and emerging risks and opportunities. The process has proven to be valuable to numerous companies and has given shareholders an important voice.”

I would urge anyone interested in this issue to read the full letter, as well as an in-depth briefing document from Ceres, “The Business Case for the Current SEC Shareholder Proposal Process.”

Like it or not, the shareholder proposal rule is a valuable part of the U.S. corporate governance landscape. The rule isn’t broken, and does not need fixing.

Endnotes

1: For example, Nasdaq’s report refers to CEO Pay Ratio disclosure as “political.” The World Federation of Exchanges’ ESG Guidance and Recommendations, however, developed under Nasdaq’s leadership, includes CEO Pay Ratio among its recommended disclosures. Nasdaq’s opposition to Dodd-Frank Section 1502 is equally troubling. It is difficult to see disclosure to shareholders regarding potential complicity in grave human rights abuses and armed conflict as a “political” effort.

Nasdaq has staked out a number of positions directly at odds with the interests of long-term investors. For example, Nasdaq’s insistence in its report that ESG disclosures remain voluntary is inconsistent with the emerging consensus among global long-term institutional investors. It is also inconsistent with Nasdaq’s opposition to the shareholder proposal rule, which has been the most important catalyst driving voluntary sustainability reporting among U.S. companies.

According to a new report from Ceres collecting feedback from more than 30 investors on the WFE’s ESG Metrics and Guidance document, investors overwhelmingly said they ultimately want sustainability reporting listing standards—not voluntary guidance—that could be phased in over time (Investors Have Their Say on Sustainability and Stock Exchanges: Feedback on the WFE ESG Guidance and Recommendations, available here).

This emerging consensus comports with the flood of letters the Securities and Exchange Commission received last year in response to its Disclosure Effectiveness Review. According to analysis by SASB, the SEC received over 276 non-form comment letters on the Release, with two-thirds addressing sustainability disclosures. Among these letters, eighty percent called for “improved disclosure of sustainability-related information in SEC filings, with only ten percent of letters opposing SEC action on this.”https://www.sasb.org/wp-content/uploads/2016/09/Reg-SK-Comment-Bulletin-091416.pdf (go back)

2The decline of IPOs in the United States is likely the result of a wide variety of macroeconomic factors, including excessive concentration in a range of industries that presents substantial barriers to market entry for smaller players. Setting aside for the moment whether this is a problem that needs attention, Nasdaq’s report provides no empirical evidence linking IPOs to job creation or linking any of its recommendations to the problem they are designed to solve. We would have preferred to see Nasdaq support stronger enforcement of our nation’s antitrust laws to promote greater competition and reduce these barriers to entry. In addition, Nasdaq could have balanced its radical ideas to undermine the ability to pursue securities class action lawsuits with a proposal supporting SEC self-funding, or at least a request to increase its enforcement budget. We were also deeply concerned to see Nasdaq’s tax proposals, several of which seem sure to increase wealth disparities, and your suggestion that the United States adopt a territorial tax system, which will only further incentivize the flight to tax havens.(go back)

3Domini Impact Investments has submitted more than 280 shareholder proposals with more than 100 companies since 1994. Available here (go back)

4“Our revision of rule 14a-8 to create a more understandable Question & Answer format should help decrease the time and expense incurred by both shareholders and companies attempting to comply with its provisions. Companies frequently consult with legal counsel in preparing no-action submissions under rule 14a-8. The rule’s added clarity may obviate the need for a shareholder or company to consult with counsel, depending on the issues raised by the submission. Under some circumstances, however, companies’ submissions must include supporting opinions of counsel.”(go back)

5“A company that receives a proposal has no obligation to make a submission under rule 14a-8 unless it intends to exclude the proposal from its proxy materials.”(go back)

6The SEC noted that reported “costs ranged from a low of $200 to a high of nearly $900,000. The median cost was $10,000.”(go back)

7With respect to the $50,000 estimate for proposal printing costs, I reached out to a major financial printer and was told that the additional cost to add an additional 1-2 page proposal to the proxy is, as expected, nominal. I was told that they could not imagine a scenario where the 1-2 page proposal would add more than 2% to the proxy printing costs and, in the overwhelming majority of proxies, the proposal would add less than 1%. I was also told that although there are some very large proxy statements that cost $5 million to print and mail, by and large, those are the exception, not the rule.(go back)

8Data provided by Heidi Welsh, Executive Director, Sustainable Investments Institute: http://www.siinstitute.org (go back)

9See, also, http://www.ey.com/Publication/vwLUAssets/EY-four-takeaways-from-proxy-season-2016/$FILE/EY-four-takeaways-from-proxy-season-2016.pdf for a detailed breakdown of proposals by topic and vote results, for 2016.(go back)

10For example, Anne Sheehan, director of corporate governance at the California State Teachers’ Retirement System, the second largest U.S. public pension fund, recently told Bloomberg that the 1% threshold “would shut down the shareholder proposal process completely.” https://newsletters.briefs.bloomberg.com/document/Smdv0IFDtNViIvTUrZzjKw–_39z270q8mwwzotccc6/front We have heard the same from representatives of the New York City and New York State pension funds.(go back)

11Nasdaq’s report claims that “According to the The New York Times, three individuals were responsible for 70% of all proposals sponsored by individuals among Fortune 250 companies in 2014,” citing Stephen Davidoff Solomon, “Grappling with the cost of corporate gadflies,” The New York Times, August 19, 2014, available at https://dealbook.nytimes.com/2014/08/19/grappling-with-the-cost-of-corporate-gadflies/. This is taken out of context. First, this was one columnist’s view, supported by an unreliable source. Second, the data point is misleading, as it tallies a subset (individual filers vs. institutional filers) of a subset (Fortune 250 out of all companies that received proposals). In fact, very few individuals sponsor shareholder proposals and very few small or mid-cap companies receive them.

According to Gibson Dunn, Mr. Chevedden and Mr. McRitchie submitted 227 proposals in 2016, representing 25% of the total number of proposals submitted. However, only 137 of these went to a vote. The vast majority of proposals were sponsored by public pension funds, trade unions, faith-based investors, foundations and asset managers.(go back)

12According to Professor Jay Brown: “James McRitchie is one of the individuals who makes significant use of the rule. Ten of his shareholder access proposals went to a vote between Jan. 1, 2016 through June 30, 2016. They received the following percentages: Apple (32.7%); Kansas City Southern (26.8%); QUALCOMM Incorporated (46.9%); Bio-Rad Laboratories, Inc. (19.9%); CSP Inc. (7.5%); Genomic Health, Inc. (35.5%); Medivation, Inc. (63.5%); Proto Labs, Inc. (71%); SciClone Pharmaceuticals, Inc. (88.2%); and SolarCity Corporation (11.4%). See Annex A, 2016 Proxy Season, Sullivan & Cromwell, July 11, 2016. See also Dave Michaels, Republicans Declare War on Corporate Gadflies, Financial Regulation Newsletter, WSJ, May 5, 2017 (“Mr. Chevedden, for instance, has sponsored 91 proposals since 2007 that garnered more than 50% support, ISS data shows. The average rate of support for his proposals was 39%.”)”.J. Robert Brown, Jr., “Corporate Governance, Shareholder Proposals, and Engagement Between Managers and Owners” (CLS Blue Sky Blog, May 15, 2017), available: here (go back)

13Just recently, J. P. Morgan Asset Management updated its proxy voting policies—in response to a shareholder proposal—acknowledging that “a company’s environmental policies may have a long-term impact on the company’s financial performance” and “corporate shareholders have a legitimate need for information to enable them to evaluate the potential risks and opportunities that climate change and other environmental matters pose to the company’s operations, sales and capital investments.” Available here (go back)