Print

PrintMartin Liebi is a Director and Alexandra Balmer is a Consultant at PricewaterhouseCoopers LLP. This post is based on a PwC publication by Mr. Liebi and Ms. Balmer.

The new EU Benchmarks Regulation (BMR) was published in June 2016 and most rules will apply as of 1 January 2018. The BMR introduces new compliance requirements for benchmark administrators, contributors, and users, with regard to interest rate, foreign exchange, security, commodity, and other benchmarks used in financial transactions. The BMR was enacted in response to public pressure resulting from the aftermath of the LIBOR scandals and follows the recommendations of the IOSCO and ESMA EBA Principles. Like many EU financial services regulations does also the BMR have an extraterritorial reach and apply to US based benchmark providers and contributors. This post will give an overview about how US based financial market participants will be affected by the BMR.

What is a benchmark?

A benchmark is defined as

“a reference index, to which the amount payable under a financial instrument or a financial contract, or the value of a financial instrument, is determined, or an index that is used to measure the performance of an investment fund with the purpose of tracking the return of such index or of defining the asset allocation of a portfolio or of computing the performance fees” (Article 3(1)(3) BMR).

Such an index is a figure, fulfilling one of the following criteria:

- Published or made publicly available;

- Determined at a regular interval by either

- partially or entirely applying a formula or any other method of calculation, or another means to assess it by; and

- on the basis of the value of one or more underlying assets or prices, including estimates of prices, actual or estimated interest rates, quotes and committed quotes, or other values or surveys.

Derivatives as defined in Section C, Annex I, Directive 2014/65/EU do not qualify as an index where there is only a single reference value. Such is the case where a single price or value is used as a reference for a financial instrument, e.g. the reference price for a future or option, without any calculation, input data or discretion. The exclusion does not cover, e.g. a basket of securities or an index based on the price of more than one financial instrument. Equally, reference or settlement prices produced by central counterparties are not considered to be benchmarks. The setting and reviewing weights within a combination of benchmarks, which is generally also only based on a simple average or similar figure if any, does not involve discretion and is thus not considered to be the provision of a benchmark.

Who will be affected?

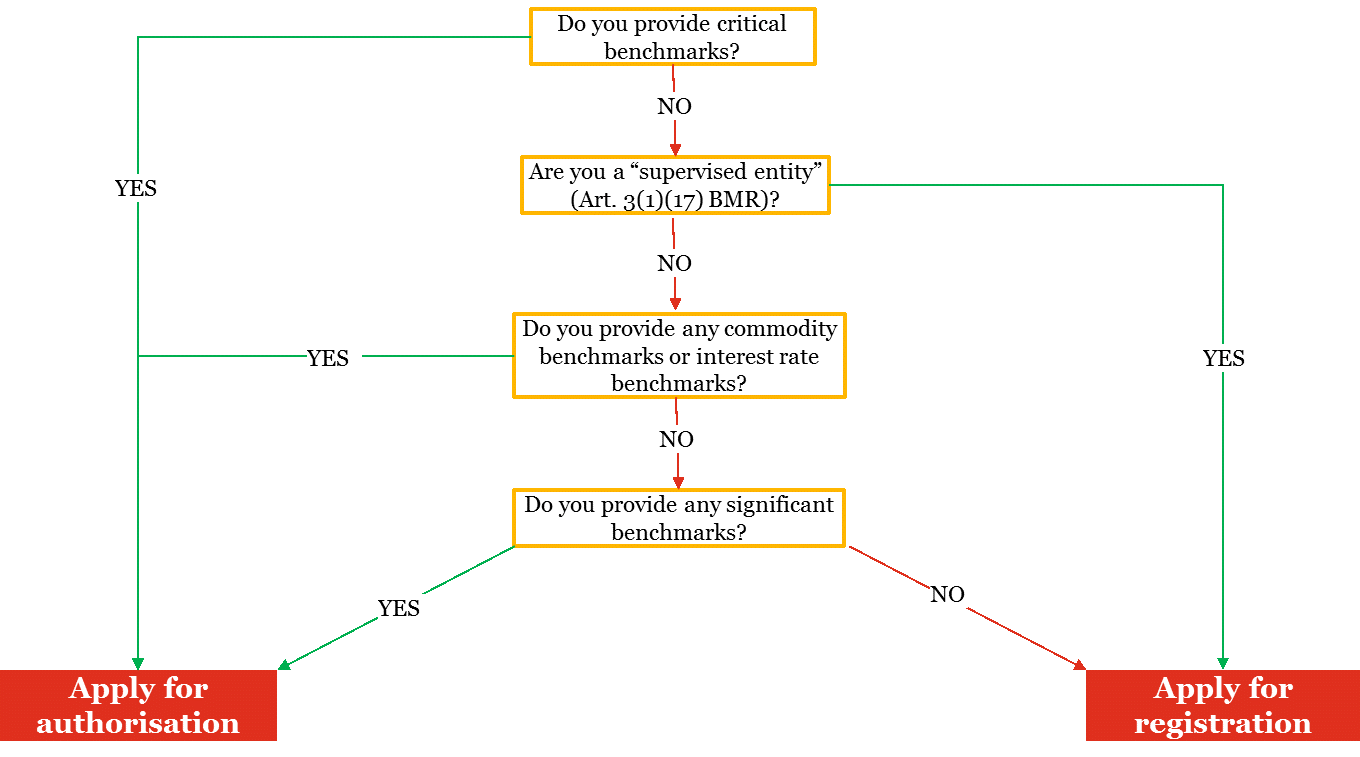

While the IOSCO Principles are the basis of the BMR, the Principles included the concept of “comply or explain”; this exemption with respect to proportionality and the nature of the benchmark is only included to a limited extent in the BMR. In order to comply with the new Regulation, administrators of a benchmark will either have to apply for registration or for authorisation, depending on the type of benchmark they provide. The provision of critical and significant benchmarks, as well as commodity and interest rate benchmarks, requires an application, while in all other cases registration with the designated authority will suffice.

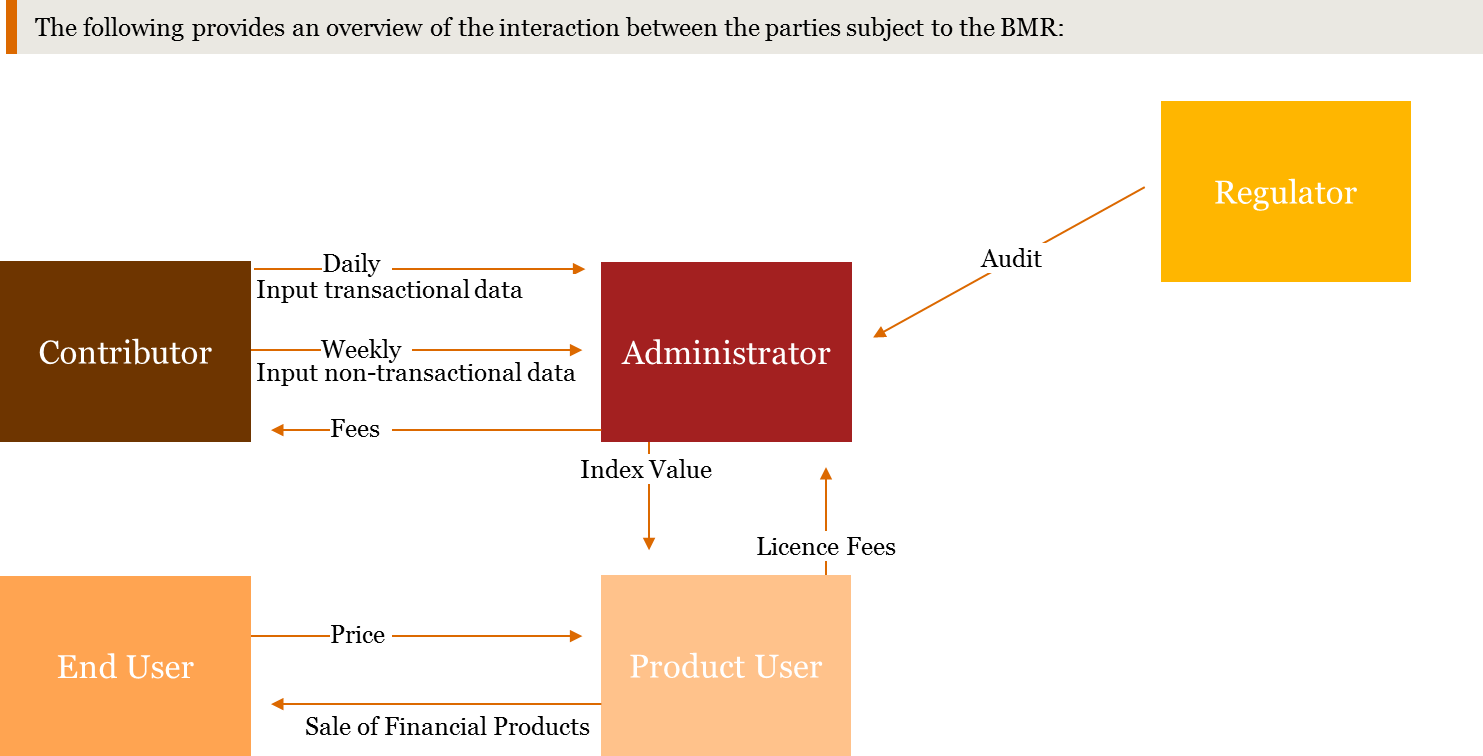

Administrators: An administrator can be either a natural person or a legal entity with control over the provision of a benchmark, in particular by administering the arrangements determining the benchmark, by collecting and analysing the input data, as well as by determining the rate of the benchmark, and by publishing it. While specific functions of the administrator can be outsourced to a third party, the sole act of publishing or referring to an existing benchmark is insufficient for an individual or an entity to be considered as the benchmark administrator. Control of provision of the benchmark is a necessary regulatory requirement for the provider to become subject to the BMR.

(Supervised) Contributors: The two types of contributors are differentiated in that any natural person or legal entity can contribute input data as a “contributor”, but only a “supervised contributor” can contribute input data to an administrator located in the EU as a supervised entity and the contributor has to comply with more stringent requirements, in accordance with Article 16 BMR. The quality and reliability of any benchmark is based on the integrity and accuracy of the input data, which is provided by the contributor. To prevent manipulation at data contribution level, contributors are subject to stringent rules under the BMR. The administrator has to ensure contributors adhere to the code of conduct and that input data is of the required integrity and can be validated, even if the contributor is located in a third country. Any omission by a contributor providing input data to a critical benchmark can undermine the credibility and representativeness of such a benchmark, with severe impact on the underlying market and economic reality. As such, national authorities are given the power to demand mandatory contributions from supervised contributors to critical benchmarks.

User of a benchmark: A supervised entity may use a benchmark or a combination of benchmarks in the EU if the benchmark is provided by an administrator located in the Union and included in the register or is a benchmark which is included in the register. Where the object of a prospectus is transferable securities or other investment products that reference a benchmark, the issuer, offeror, or person asking for admission to trade on a regulated market shall ensure that the prospectus also includes clear and prominent information stating whether the benchmark is provided by an administrator included in the register. User of a benchmark are thus e.g. a trading venue, where the derivative is subject of a request for admission to trading on such trading venue or is traded on such trading venue and it has set the relevant terms of the derivative and thus chosen the specific benchmark to be referenced; an investment firm acting in the capacity of a systematic internalizer to the extent such systematic internalizer has set the relevant terms of the derivative and thus the chosen the specific benchmark to be referenced; a CCP, where the derivative is cleared by such CCP to the extent that such CCP has set the relevant terms of the derivative and thus chosen the specific benchmark to be referenced; or each supervised party to a contract not being one of the preceding parties.

Which benchmarks will be affected?

The BMR subdivides the benchmarks into various subcategories, based on the type of market they reproduce. The Regulation contains specific additional requirements for both commodity and interest rate benchmarks. The following provides an overview of the various subcategories of benchmarks:

| Type of Benchmark | Description |

|---|---|

| Regulated Data Benchmark | Data input for the benchmark is provided directly from regulated venues. Certain provisions of the BMR do not apply to regulated data benchmarks, and they cannot be classified as critical. |

| Interest Rate Benchmark | An IR Benchmark is determined on the basis of the rate at which banks may lend or borrow from other banks or agents in the money markets. They are subject to the requirements set out in Annex I BMR. Provisions of the BMR relating to significant and non-significant benchmarks do not apply. |

| Commodities Benchmark | The basis for the benchmark is a commodity as defined by MiFID II. Commodity Benchmarks are subject to the requirements of Annex II BMR, unless the benchmark also qualifies a regulated data benchmark, or is based on submissions from mainly supervised entities. Provisions of the BMR relating to significant and non-significant benchmarks do not apply. |

| Critical Benchmark | To qualify as a critical benchmark, the value of the underlying contracts needs to be at least EUR 500 bn, or it has to have been recognised as critical in a member state. Critical benchmarks are subject to more stringent and specific requirements than other types of benchmarks.

A framework has been developed by ESMA to determine Interbank Offered Rates benchmarks (IBORs) and the Euro Over Night Index Average (EONIA) as critical benchmarks. To date, only EURIBOR has been qualified as such by the EC. |

| Significant Benchmark | Requires the value of underlying contracts to be at least EUR 50 bn, or there to be none or very few market-led substitutes, leading to significant impact on financial stability, if the benchmark ceases to be produced. |

| Non-Significant Benchmark | All other benchmarks where the benchmark is neither a commodity nor an interest rate benchmark and the value of underlying contracts of the benchmark is less than EUR 50 bn. |

How will a US-based benchmark provider be affected?

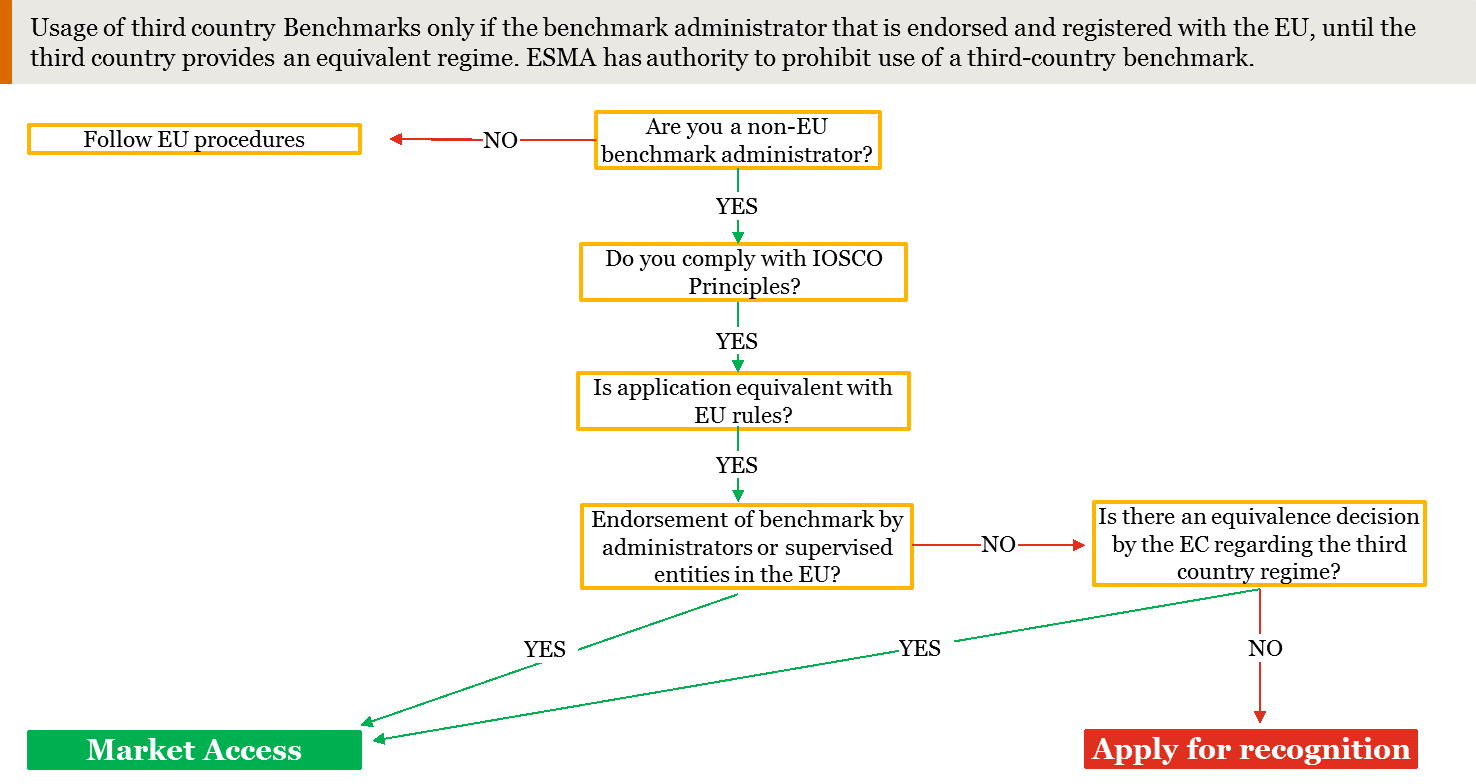

US-based administrators are subject to BMR rules where they intend to obtain EU market access; non-compliance will likely lead to these non-EU benchmarks being denied EU market access. There are three ways for US administrators to become compliant: equivalence, recognition, and endorsement. Firstly, an equivalence decision with regard to foreign jurisdictions can be made by the European Commission if the requirements of Article 30(1) BMR are met and this results in benchmarks from the US being eligible for use by supervised entities in the EU. Secondly, where an administrator located in the US provides proof of compliance with the IOSCO Principles and said compliance is equivalent to the BMR, the administrator should be recognised as an administrator within the EU. An administrator located in the US, such as Switzerland, must have a legal representative in the reference member state, if the entity intends to obtain recognition. The legal representative must oversee the provision of benchmarks as performed by the administrator and is accountable to the competent EU member state authority. Finally, market access as an US administrator can be gained through an endorsement by an administrator of a supervised entity located in the EU. Endorsement will permit market access where the US administrator adheres to the IOSCO Principles and such adherence results in equivalent compliance with the BMR.

Obligations for administrators and contributors

The BMR directly imposes a variety of obligations on persons involved in the provision, contribution, and use of benchmarks throughout the EU to prevent conflicts of interest and manipulation of benchmarks as well as to ensure maximum harmonisation in cross-border applications. If tasks are outsourced to an external service provider the provider also has to adhere to the BMR. In particular, the administrator is required to provide a code of conduct specifying the requirements and responsibilities regarding input data and to supervise adherence to the code, even if the contributor is located in the US.

The obligations include the following provisions for administrators:

- Robust governance arrangements, including a clearly organisational structure with well-defined, transparent and consistent roles and responsibilities for all involved, preventing conflicts of interest (Article 4 BMR).

- Develop and maintain robust procedures to ensure oversight of all aspects of the provision of a benchmark and communication with the relevant competent authorities (Article 5 BMR).

- Ongoing control of benchmarks to ensure they are provided, published and/or made available in accordance with the Regulation, and maintained through an accountability framework, record-keeping, auditing, and review and complaints handling process (Article 6 to Article 9 BMR). These frameworks must include any third party to which a task has been outsourced (Article 10 BMR).

- The administrator is also responsible for overseeing the quality of input data and reporting any infringements without delay to the competent authority (Article 11 to Article 15 BMR).

The obligations include the following provisions for contributors:

- The contributor must adhere to the code of conduct provided by the administrator and the specific requirements prescribed with respect to the contribution of input data (Article 15 BMR).

- Supervised contributors must also ensure input data is not affected by any existing or potential conflicts of interest and that all discretion is exercised in an independent and honest way (Article 16 BMR).

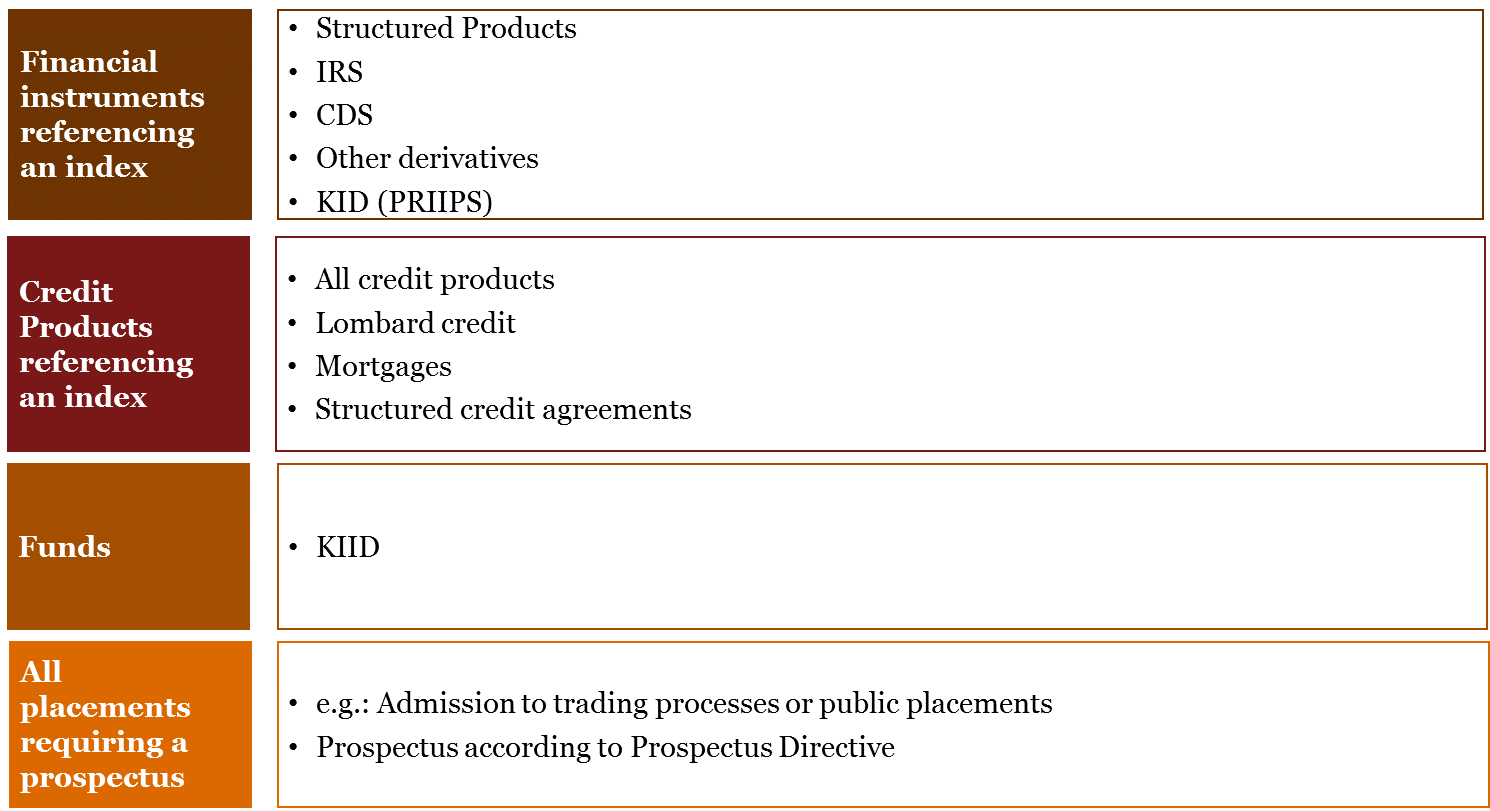

Typical products in scope

Entry into force, transition period, and grandfathering

The BMR will enter into force on 1 January 2018. There is a transition period for certain new and existing benchmarks until 1 January 2020. In accordance with the transitional provisions of Article 51(3) BMR, ESMA considers existing benchmarks as including benchmarks “existing on or before 1 January 2018”, including those provided for the first time on or before 1 January 2018. Index provider already providing a benchmark on 30 June 2016 have time to apply for authorization until 1 January 2020. This transitional provision applies on the entity level. The index provider is allowed during the time frame to provide benchmarks already provided before 1 January 2018, updating and modifying of benchmarks already provided before 1 January 2018, as well as the provision of new benchmarks for the first time after 1 January 2018. An index provider may provide a benchmark created between 30 June 2016 and 1 January 2018, including updates and modifications, to supervised entities in the EU until 1 January 2020, even if authorisation or registration has not yet been granted, unless authorisation or registration has been refused. However, in the case an index provider starts to provide benchmarks after 30 June 2016 and provides a new benchmark after 1 January 2018, supervised entities will not be allowed to use such newly provided benchmark, unless the index provider obtains first authorisation or registration.

The BMR has applied to the EURIBOR since 12 August 2016, following qualification as a critical benchmark.