Print

PrintRobert J. Jackson, Jr. is a Commissioner at the U.S. Securities and Exchange Commission. The following post is based on Commissioner Jackson’s recent remarks at the Greater Cleveland Middle Market Forum, available here. The views expressed in the post are those of Commissioner Jackson and do not necessarily reflect those of the Securities and Exchange Commission, the other Commissioners, or the Staff.

Thank you so much, Tom, for that kind introduction. It’s a real honor to be here with you today at the Greater Cleveland Middle Market Forum. In addition to leading some of the Nation’s most promising young companies, you all have done exceptional work making sure that the middle market gets the attention it deserves in Washington. And as a lifelong baseball fan, I couldn’t miss the chance to see the Indians show the Cubs who’s boss tonight in Cleveland. [1]

Now, before I begin, let me just give the standard disclaimer: the views I express here are my own and do not reflect the views of the Commission, my fellow Commissioners, or the SEC’s Staff. And let me add my own standard caveat: I fully expect to convince my colleagues of the absolute and obvious correctness of my views.

As Tom mentioned, although it feels like a lifetime ago I was just recently sworn in as a Commissioner in January. It’s been an incredible honor to serve with my fellow Commissioners—and the real privilege is working with the incredibly talented and hardworking SEC Staff who have dedicated their lives and exceptional talents to protecting investors.

Before coming to the Commission I had every job under the sun—from my brief college career as a busboy in Philadelphia to my time as a corporate lawyer. Although my Dad likes to point out how much trouble I seem to have holding a job, [2] one benefit of my varied background is that I’ve been able to bring those experiences with me to my work at the SEC. And they’ve convinced me that we’re not doing enough to give middle-market companies the access they need to our public markets. More on that in a moment.

First, I’d like to start with a story. In 1999, at the peak of the dot-com boom, a 22-year-old investment banker was getting his first taste of high finance. Every Monday, wearing the sharp suit he bought with his signing bonus, this young hotshot banker boarded a flight to Silicon Valley to pitch young hotshot companies on the idea of using his firm for their IPO. Many of these companies had weak financials and even weaker business plans. No matter. This 22-year-old banker didn’t know any better. In fact, he helped take many of those companies public. [3]

As you might have guessed, that young hotshot banker was me—and, upon reflection, I’m less of a hotshot than I once believed. A lot has changed since 1999: I was humbled by the dot-com crash, advised the Treasury during the financial crisis, and became a law professor. And in the two decades since I left Wall Street, our markets have been transformed by technology. Today stocks trade with dizzying speed and our markets move faster than ever.

But some things have remained the same. You see, when I was a banker, we charged a standard fee for a middle-market IPO: seven percent. We would negotiate a reduced price for large, high-profile companies, where the client’s bargaining power produced a better deal. But for middle-market companies, our fee was always seven percent. Whatever industry the company was in, whatever its growth profile, however qualified its management team was, if they were a smaller firm, they always paid seven percent. [4]

Back in 1999, I assumed that technology and competition would eventually lead bankers to give middle-market companies better pricing on IPOs. That’s why, when I arrived at the SEC, I asked my team to dig into the data to see how middle-market IPO pricing has changed. We’ll get into what we found in a moment. But the short version is that nothing has changed: middle-market entrepreneurs still have to pay 7% of what they’ve created to access our public markets.

That’s why I’ve come here today to talk about the middle-market IPO tax. These days in Washington folks seem convinced that so-called red tape is the reason why smaller companies so rarely go public. [5] We’ve even come up with a name for it: “burdensome regulation.” [6] But I think the story is much more complicated than that. And I think it’s high time to ask whether middle-market companies are paying too high a price for access to America’s capital markets.

The Seven-Percent Middle-Market IPO Tax

When an entrepreneur decides to tap our public markets, she usually needs the help of a team of bankers, accountants, and lawyers to navigate the process. Those teams can add a great deal of value for the company and its investors by making sure that the firm is ready for the rigors of being public. [7]

But the fees founders pay for an IPO also function as a tax, taking precious capital away from investment, research, and job creation. The question I want to ask you today is not whether the team should be paid something for the value it adds. Of course it should. Instead, I want to ask whether the price of an IPO today really reflects the best deal we can get for founders and investors at America’s middle-market companies.

Nearly two decades ago Professor Jay Ritter published a compelling paper in the Journal of Finance showing that, in the 1990s, more than 90% of middle-market firms paid exactly 7% [8] of the firm’s value in order to go public. Professor Ritter and his coauthor pointed out that IPOs had not always been priced that way. In fact, they explained, in the 1980s a far smaller fraction of IPOs cost exactly 7%. [9] The authors worried that the costs of midsized IPOs in the 1990s were “above competitive levels.” [10]

They gave three reasons why. First, IPO costs were far higher in the United States than elsewhere in the world. [11] Second, the 7% figure seemed unrelated to the costs of taking a company public; otherwise, “the average spreads on $80 million [IPOs] would be lower than on $20 million [IPOs],” “but they are not.” Finally, the authors explained, “investment bankers readily concede that [IPO costs] are high.” [12]

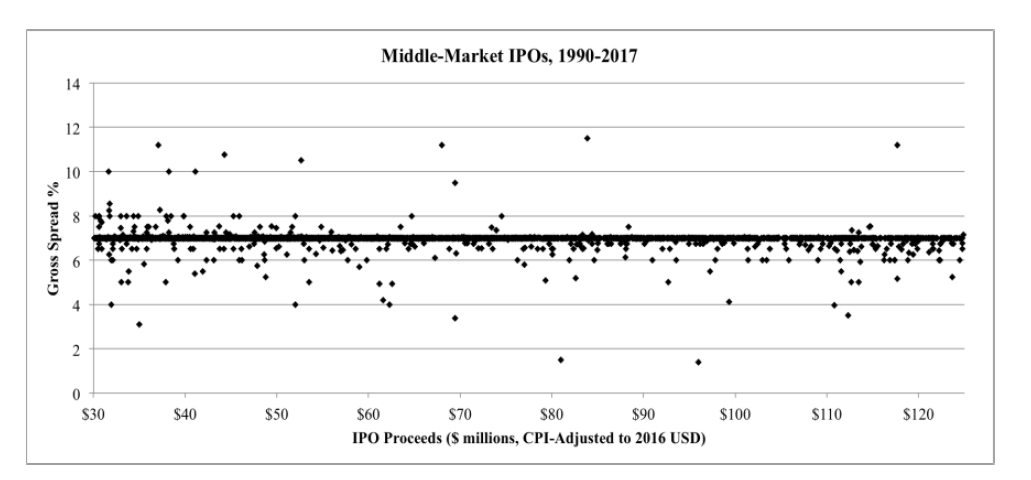

Because that study was published so long ago, my Staff and I asked Professor Ritter to help us take a closer look with more recent data. He kindly worked with us to examine more than 700 middle-market IPOs over a fifteen-year period starting in 2001. We found that the problem he documented years ago has, if anything, gotten worse. [13] As the figure below shows, from 2001 through 2016, we found that over 96% of midsized IPOs featured a spread of exactly 7%: [14]

Even worse, as the figure above shows, this is mostly a middle-market problem. In larger IPOs—where the company can use its bargaining power to insist on lower fees—the price of going public is different. In fact, nearly half of those companies paid less than 7% when going public. For example, Facebook famously negotiated a fee of just 1.1% for its IPO. [15]

Although the direct costs of smaller IPOs are significant, they’re only part of the tax middle-market companies pay to go public. In addition to these direct costs, companies pay indirectly when bankers price their shares to produce a first-day pop in the company’s stock price—sometimes called IPO “underpricing.” The big first-day returns are meant to reward institutional investors who sign up to participate in IPOs. [16] But retail investors rarely get in on those returns—and the first-day pop forces the entrepreneurs who are selling stakes in their companies to leave real money on the table.

While Professor Ritter’s initial study also identified this issue, my Staff worked with him to obtain more recent data on IPO underpricing. We found, once again, that this tax on going public is far more significant for middle-market companies than for larger firms. [17] In every single year from 2000 through 2017, the average amount of IPO underpricing for middle-market companies was greater in percentage terms than for large-company IPOs. [18]

With the deck stacked against them, it’s no wonder that middle-market IPOs have been on a steady decline. And this has had real effects across our economy, which is now dominated by fewer, and larger, public companies than ever before. [19] From 1975 to 1991, one out of two U.S. public companies were worth less than $100 million in inflation-adjusted dollars. But public companies of that size are vanishing: today that fraction is less than one in four. [20]

The Effects of the Middle-Market Tax on Today’s Markets

I’m not the first to identify—or worry about—the middle-market IPO tax. [21] In fact, the research establishing how much it costs middle-market companies to tap our markets is decades old. So you might ask why its effects on our markets are being felt so only now. Why did it take so long for the IPO tax to change the complexion of our public markets?

Part of the answer lies in what’s happening in our private markets. Two decades ago, a small but growing private company looking for significant funding had little choice but to go public. Private markets were important, of course, in the early stages of a company’s life. But significant growth required scale and liquidity that could only be provided by an IPO.

Today, private markets provide a much more competitive alternative. Those markets are larger and more robust than ever—and can support a company’s growth well into the later stages of its life. [22] In short, when public markets were the only game in town, companies were more willing to pay the IPO tax. Today, that tax can lead many middle-market companies to choose to stay private—with significant implications for the broader economy.

That’s why it’s so puzzling that the middle-market IPO tax is still so high. If going public no longer adds the marginal value for smaller firms that it once did, one would expect the price of taking them public to fall. And to the degree that these costs are meant to compensate for the diligence and research that bankers conduct on companies before the IPO, one would expect those costs to fall now that companies are going public later in their lives, when more is known about the business and its future. [23] But for middle-market companies, three things are as certain today as they were two decades ago: death, taxes, and seven percent IPO fees. [24]

The Path Ahead

The reasons why middle-market companies are vanishing from public view are complex. I’m not claiming today that the 7% tax explains everything we see today in our capital markets. As others have noted, for example, the ongoing costs of being a public company can be substantial. [25] But before they even encounter those costs, midsized firms first have to decide whether to pay the 7% tax standing between entrepreneurs and our public markets.

Nor can we expect markets alone to provide a path for middle market firms to go public. For one thing, the price small companies pay to go public has remained exactly the same for decades—a pattern that can hardly be said to give us real hope for robust competition going forward. [26] For another, although important new methods for listing shares have recently emerged, those solutions will likely be limited to large, well-known companies. [27] If lawmakers do nothing to level the playing field for middle-market IPOs, the trend that is taking small American businesses out of our public markets will likely continue.

One might ask: so what? After all, it may be that private markets are the most efficient source of capital for America’s growing businesses. But for two reasons I think the middle-market IPO tax poses real risks for our economic future. First, it’s bad for smaller companies because it puts them at a significant disadvantage. Without a realistic alternative to private capital, middle-market firms can be forced to accept less favorable terms when raising money. If we reduce the 7% middle-market IPO tax, private capital providers will face increased competition from public markets—improving financing terms for middle-market businesses.

Second, the middle-market IPO tax is bad for ordinary investors. When the tax causes our most exciting young companies to raise private capital rather than go public, retail investors are left out of a significant part of the Nation’s economic growth. The reason is that families saving for education and retirement typically invest in public-company indexes increasingly dominated by large, mature firms. When middle-market companies stay private, ordinary investors never get the chance to provide them with the kind of early capital that spurs growth. Our tradition of giving American investors an important role in the growth of our economy—by investing in big firms and small—has served us well. We should not allow a persistent, puzzling tax on middle-market IPOs to keep Americans from investing in companies so crucial to the long-term growth

of our economy. [28]

So what can be done to lower the barriers to bringing middle-market companies public? For starters, I urge my colleagues on the Commission to consider more robust disclosure rules regarding both the direct and indirect costs of an IPO. In particular, underwriters should disclose and highlight for entrepreneurs and investors the total costs of taking the company public—including the money that will be left on the table as a result of underpricing. Bankers should also be required to explain why these costs are justified—especially in light of the lower price that larger companies pay for the same services.

I also hope that the conversation in Washington about the reasons for the disappearance of middle-market IPOs will change. Solutions to that problem will require more than cutting red tape. It makes little sense to address the decline in small public companies without grappling with the 7% IPO tax. In an economy increasingly built to benefit our largest companies, the middle market should be able to access our public markets at a competitive price.

I am deeply grateful to my colleagues Bobby Bishop, Matthew Cain, Caroline Crenshaw, Marc Francis, Satyam Khanna, and Prashant Yeramalli, whose hard work made these remarks possible. We are also grateful to Professor Jay R. Ritter, Cordell Eminent Scholar at the Warrington College of Business at the University of Florida, for helping us better understand matters he has carefully studied for over a decade. Any errors are solely my own.

Endnotes

1My Chicago friends have tried to persuade me that in baseball, as in pizza, Illinois is the envy of the Nation. We’ll see. Compare CHICAGO CUBS, ROSTER & STAFF (2018), available at http://m.cubs.mlb.com/roster with CLEVELAND INDIANS, ROSTER & STAFF (2018), available at http://m.indians.mlb.com/roster and NEW YORK YANKEES, ROSTER & STAFF (2018), available at http://m.yankees.mlb.com/roster(go back)

2For my father’s favorite citation for this point, see GEFFRAY MINSHULL, ESSAYS AND CHARACTERS OF A PRISON (1618) (providing the origins of the famous phrase “jack of all trades, master of none” ). For mine, see AZIZ ANSARI ET AL., 1 FINALE, MASTER OF NONE (Netflix 2015).(go back)

3To be clear, I failed a lot more than I succeeded during these pitches. But one company that did use us for its IPO was DrKoop.com, a health-information website founded by President Reagan’s former Surgeon General, Dr. C. Everett Koop. Like too many offerings of its era, that IPO ended badly. See CNN MONEY, 10 BIG DOT.COM FLOPS, DR.KOOP.COM (March 10, 2010); see also In re Dr.Koop.com, Inc. Securities Litig., Case No. 00-CV-427-JN (W.D. Tex. Jan. 11, 2001).(go back)

4For the seminal study identifying this fact, see Hsuan-Chi Chen & Jay R. Ritter, The Seven Percent Solution, 55 J. FIN. 1105 (2000). See also Matt Levine, Money Stuff: Rates, Regulations and Casinos, BLOOMBERGVIEW (Nov. 14, 2016) (“[t]here is no obvious explanation for why the investment banks underwriting an IPO should get 7% percent of the proceeds”; instead, “there is a sense that only a limited number of banks can do all the stuff involved,” “and those banks all just happen to charge the same fees.”).(go back)

5See, e.g., CROWDFUND INSIDER (February 16, 2017) (quoting John Berlau of the Competitive Enterprise Institute) (“The best way to [protect investors and facilitate capital formation] is to cut the red tape from both the Barack Obama and George W. Bush administrations that led to an unprecedented decline in IPOs and public company listings, depriving entrepreneurs of the best method to raise capital and investors of an opportunity to grow wealthy with smaller companies.”).(go back)

6See, e.g., Ze-ev D. Eiger & Anna T. Pinedo, JOBS Act Quick Start, INT L. FIN. L. REV. 5 (2016) (arguing that the JOBS Act was designed to “address concerns about capital formation and unduly burdensome Securities and Exchange Commission regulations ”).(go back)

7See, e.g., RICHARD A. BREALEY, STEWART C. MYERS & FRANKLIN ALLEN, PRINCIPLES OF CORPORATE FINANCE 371-72 (11th ed. 2016) (describing the diligence process and its value to firms and investors).(go back)

8For purposes of these remarks, I follow Professor Ritter’s terminology, referring to the direct costs of the IPO to be equal to the underwriting fees paid to the investment banks divided by the IPO proceeds. These costs are often referred to as the IPO “spread.” See generally Chen & Ritter, supra note 4.(go back)

9See id. at 1105 (“There is much more clustering at seven percent now than [in the 1980s], although the average spread on IPOs has not changed during this period.”).(go back)

10Id. at 1106.(go back)

11See Mark Abrahams on, Tim Jenkins on & Howard Jones, Why Don’t U.S. Issuers Demand European Fees for IPOs? (working paper 2009) (“[A]lthough the same investment banks conduct IPOs in Europe using the same methods [as they do in the United States], we find that [the banks] charge fees that are roughly 3 percentage points lower [in Europe]”; thus, if “U.S. issuers had paid European fees over the last decade they would have saved around $6 billion”).(go back)

12I feel for the anonymous, and I assume now-former, banker who conceded this on the record to a reporter, only to later find the admission published in the Journal of Finance. Id. at 1106 & n.2 (citing Roger Lowenstein, Street’s Incredible Unshrinking Spread, WALL ST. J. (April 10, 1997) (describing the seven-percent IPO tax as “one of the holy grails,” and noting that investment banks would be “cutting our own throats to compete on price”)).(go back)

13 Compare Chen & Ritter, supra note 4, at 1108 (documenting that, from 1995 through 1998, “[f]ully ninety-one percent of … moderate-sized IPOs paid a spread of exactly 7.0%”).(go back)

14 Rather than bore you with the details of our data collection and analysis, we point the interested reader to the Data Appendix we are posting simultaneously with this speech. There, you can learn more about the data we used and the choices we made in identifying the costs of middle-market IPOs. We are especially grateful to Professor Ritter for his assistance in obtaining and examining these data.(go back)

15 See Alistair Barr & Alexei Ores kovic, Facebook Underwriters to Get 1.1 Percent Fee: Source, REUTERS (March 20, 2012).(go back)

16 See, e.g., Thomas J. Chemmanur, Gang Hu & Jiekun Huang, The Role of Institutional Investors in Initial Public Offerings, 23 REV. FIN. STUD. 4496 (2010 (“nothing that “[t]he theoretical literature on IPOs has long argued that institutional investors possess private information about IPOs and that underpricing is a mechanism for compensation them to reveal this private information”).(go back)

17 As discussed in the Data Appendix we have posted concurrently with these remarks, for these purposes we define a middle-market company as those with training twelve-month sales of $50 million to $1 billion in inflation-adjusted 2017 dollars.(go back)

18 It is true, of course, that underpricing may be larger for smaller firms because investors are more wary of smaller, less-established companies—and, thus, require more significant first-day returns to compensate them for the risk of participating in a small-company IPO. That does not explain, however, why middle-market firms are virtually always required to pay their bankers seven percent of the firm’s value to go public.(go back)

19This has led even (or especially) adherents of the Chicago School to worry about the “emerging consensus among economists that competition in the economy has weakened significantly.” THE ECONOMIST, The University of Chicago Worries About a Lack of Competition (April 12, 2017).(go back)

20Craig Doidge, Kathleen M. Kahle, G. Andrew Karolyi & Rene M. Stulz, Eclipse of the Public Corporation or Eclipse of the Public Markets? 5 ECGI WORKING PAPER 547-2018 (Jan. 2018) (discussed on the Forum here).(go back)

21See Letter from Nine Members of Congress to Mary Jo White, Chair, U.S. Sec. & Exch. Comm’n and Richard G. Ketchum, Chairman, FINRA (July 15, 2016) (requesting that the SEC and FINRA study this issue).(go back)

22MCKINSEY & COMPANY, THE RISE AND RISE OF PRIVATE EQUITY (Feb. 2018) (private fundraising in 2017 reached nearly $750 billion—more than six times the level of private funds raised fifteen years ago).(go back)

23See Matt Levine, Unicorns Take Different Paths to Being Public, BLOOMBERG VIEW: MONEY STUFF (March 27, 2018) (noting that, given the compression of the valuation system between private and public markets, “late-stage private investors now are doing the job that the post-IPO public investors used to do, and are being compensated accordingly … . The IPO investors—the ones who buy in the offering—are doing … well, it is harder to see what job they are doing, or why they should get a 30 percent pop for doing it.”).(go back)

24Although this famous phrase is often attributed to a letter written by Benjamin Franklin in 1789, its provenance is probably earlier. See 10 THE WRITINGS OF BENJAMIN FRANKLIN 69 (Albert Henry Smyth ed., 1907) (quoting a letter from Franklin to Jean-Baptiste Leroy) (“Our new Constitution is now established, and has an appearance that promises permanency; but in this world nothing can be said to be certain, except death and taxes.”); CHRISTOPHER BULLOCK, THE COBBLER OF PRESTON (1716) (“‘Tis impossible to be sure of any thing but Death and Taxes.”)).(go back)

25See, e.g., PWC STRATEGY, CONSIDERING AN IPO? (2012) (“[I]n addition to the costs associated with going public … there are significant expenses related to the being-public process, which consists of developing the infrastructure to operate in a public environment. Most public private companies do not have this infrastructure, and to satisfy this new level of regulatory and reporting rigor, many will incur a series of … incremental ongoing costs associated with being a public company.”).(go back)

26 It is true, of course, that some sophisticated counterparties, such as private equity investors, pay significant fees when they take portfolio companies public, suggesting that substantial IPO fees can be justified. Notably, however, private equity owners exit their firms by way of IPO far less frequently today than they did in previous eras. See PREQIN, 2017 BUYOUT DEALS AND EXITS FOR JANUARY 2018 (noting that just 12% of private-equity exits in 2017 were by way of IPO, as opposed to 54% through a sale to a strategic buyer). And there is evidence that banks do engage in less underpricing when the lead IPO underwriters themselves are among the affected investors. See Xi Li & Ronald W. Masulis, Venture Capital Investments by IPO Underwriters: Certification or Conflict of Interest? (working paper 2002) (“[I]t is not prior equity investments by any underwriter that significantly reduces IPO underpricing, but rather an equity investment by a lead underwriter.”).(go back)

27 That’s why Spotify’s recent decision to list directly on the New York Stock Exchange, while a hopeful development for competition over IPO pricing at large firms, provides little comfort that the seven-percent tax is likely to be lifted for smaller companies anytime soon. See Polina Marinova, Spotify’s First Investor on Why the Company’s Unusual IPO Makes Sense, FORTUNE TERM SHEET (March 21, 2018) (quoting Par-Jorgen Parson, an early investor in Spotify) (“I think it’s highly unlikely that a b-to-b company can go down this route. It’s just unlikely that a smaller market-cap company would be able to get enough interest in the capital markets. So for huge market cap, household names with cash-efficient models that don’t need to raise external capital, I absolutely think it could be a right fit. But there are very few companies who have all of those characteristics.”).(go back)

28 Indeed, as I have previously argued, one problem raised by earlier efforts to reduce the costs of going public for small companies is that those legal changes may result in less retail participation in the IPO process. See Colleen Honigsberg, Robert J. Jacks on, Jr. & Yu-Ting Forester Wong, Mandatory Disclosure and Individual Investors: Evidence from the JOBS Act, 93 WASH. U. L. REV. 293 (2015).(go back)

29 NATIONAL CENTER FOR THE MIDDLE MARKET, 1Q 2018 MIDDLE MARKET INDICATOR (2018) (during the financial crisis, middle-market companies “outperformed through the financial crisis … by adding 2.2 million jobs ” during that period, “demonstrating their importance to the overall health of the U.S. economy.”).(go back)