Print

PrintJeff Lubitz is Head of ISS Securities Class Action Services, Institutional Shareholder Services, Inc. This post is based on an ISS publication by Elisa Mendoza, Vice President with ISS Securities Class Action Services.

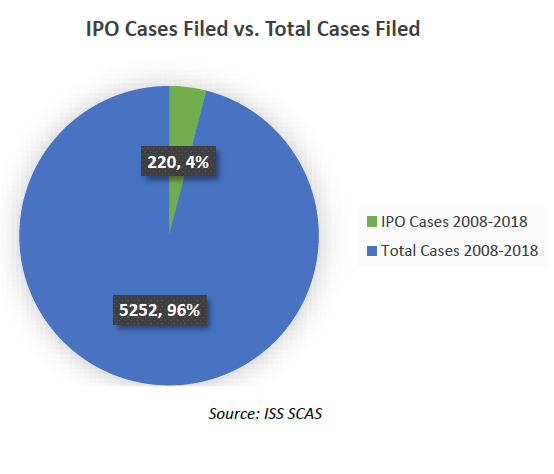

Though IPO-related class actions accounted for just four percent of all securities class actions over the past decade, according to ISS Securities Class Action Services (SCAS) data, much ink has been spilled in recent months over whether the U.S. Securities and Exchange Commission (SEC) might bar IPO-related lawsuits in lieu of arbitration. Supporters of arbitration argue that it would eliminate frivolous shareholder litigation and provide a more efficient way for investors to seek redress. [1] Treasury Department officials argue the change could be a way to “reduce costs of securities litigation for issuers in a way that protects investors’ rights and interests,” according to Bloomberg. [2] The change, proponents contend, would incentivize more companies to go public on the U.S. markets. This potential change to the SEC’s long-standing position would effectively give credence to the contention by advocates of mandatory arbitration that the burdens and expense of securities class action lawsuits are among the factors that have led to a decline in the number of IPOs in the U.S. in recent years. [3]

While advocates of mandatory arbitration contend that the burdens and expense of securities class action lawsuits are among the factors that underlie a decline in the number of IPOs, Jeff Lubitz, Head of ISS Securities Class Action Services, points to other reasons for the decline. “While the data shows a slight increase in the percentage of IPO cases filed each year (from 2009 to 2017), the reality is that more and more pre-IPO companies are remaining private likely due to increased equity investments and revenue growth from a strong economy,” said Lubitz. “The past benefit of going public is often outweighed by the negatives that come with additional regulation, added public disclosures, and being driven by quarterly expectations.”

Noting one aspect of benefits to investors and capital markets, Lubitz points to Facebook’s announced settlement of $35 million on February 26, 2018 that “won’t be a financial windfall for shareholders,” but will potentially “act as a needed deterrent against fraudulent activities for future IPO companies.”

Many in the industry are concerned that mandatory arbitration, while it may entice companies to offer IPOs on U.S. markets, will do considerable damage to the rights and abilities of investors to recoup their losses if fraudulent activities were to occur. Those that caution against mandatory arbitration, such as Rick Fleming, the SEC’s Investor Advocate, argue that stripping away the right of shareholders to bring a class action lawsuit is draconian and counterproductive to promoting capital formation. [4] Fleming argues that investors themselves have typically borne a large share of the responsibility for policing the markets and rooting out misconduct, due to the limited scope of the SEC’s resources. [5] However, if mandatory arbitration were in place, the costs of bringing claims individually in arbitration may exceed the amount of any likely recovery for individual investors who suffer losses in a widespread fraud. [6] Moreover, and unless their losses were sizable, victimized shareholders would struggle to find attorneys to represent them as well as to retain experts to establish elements such as materiality, reliance, loss causation, and damages. [7] The fallout would be a problem of a collective action with each investor lacking the economic incentive to bring an individual case, even though the collective losses of multiple investors would justify the costs of the litigation. [8] Supporters of this view contend that this can have many unintended consequences, such as placing the burden of investigating and litigating these cases entirely on the SEC and diminishing the deterrent effect of wrongdoing in this sector. [9]

As newly appointed Democratic SEC Commissioner Robert J. Jackson, Jr. explains, proposals like the mandatory arbitration provision are not as effective an deterrent because it “deprives the public of the law our judges make when they hold corporate insiders accountable to investors” and removes the inhibition because it is no longer public where “judges tell corporate insiders what the law expects of them.” [10] Therefore, the dangers of restricting the right of shareholders to sue in a class action and the downstream effects of class actions on the industry as a whole may outweigh the alleged benefits of including mandatory arbitration clauses in companies’ charters for IPOs.

IPO Class Action Litigation: A 10-Year Review

IPO Case Filings and Settlements

As debate continues over whether arbitration should be made mandatory for IPOs or not, SCAS analyzed IPO class action litigation data to look at the number of IPO cases filed over the last 10 years in both federal and state courts which shows their prevalence is relatively low compared with the overall number of securities class actions filed.

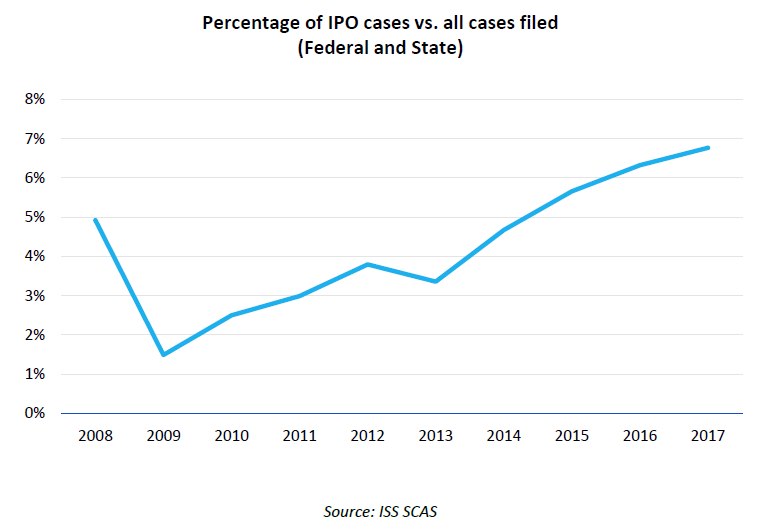

As noted earlier and from 2008 through year-to-date 2018, IPO class action litigation accounts for just four percent (of all securities class action litigations over the 10-year period). As illustrated in the graph below, however, the percentage of IPO cases filed each year has increased incrementally from 2009 to 2017, giving some credence to speculation that it may be a deterrent for IPOs being offered on U.S. exchanges in recent years. The number of IPO class action litigations filed in 2009 was approximately 1.5 percent of the total securities class action litigation and steadily climbed to roughly 6.8 percent in 2017. Still, less than 10 percent of securities class action filings constitutes a small percentage and does not carry much impact across the industry.

Taking a closer look at which types of companies or industries experience the most IPO class action litigation, certain trends emerge. Interestingly and as one might expect, smaller companies disproportionately see IPO-related litigation. In fact, ISS Securities Class Action Services tracked just two IPO class actions settled against large capital, S&P 500 companies over the last 10 years. Those cases were against Prudential Financial and Genworth Financial for IPO-related activity connected with a bond issue in the case of Prudential Financial, and for a new business unit in the case of Genworth Financial. The IPO class action against Prudential Financial was filed in 2009 and settled for $16.5 million. The IPO class action filed against Genworth Financial was filed in 2014 and settled for $20 million. The market cap for Prudential Financial in 2009 was $5.50 billion with the settlement representing just 0.30 percent of the company’s then market value. The Genworth Financial settlement represented just 0.25 percent of the company’s then value.

These settlements, or rather the absence of more settlements against S&P 500 companies, may reflect several scenarios:

- these companies have been public longer than 10 years and thus have not offered IPOs in the last decade;

- these companies are more prudent about valuation and pricing; or

- these companies were able to defeat any class action litigations brought against them in the past decade.

By contrast, the most high-priced tech company IPOs do seem to draw their fair share of class action litigation. Fox Business pulled together a list of the most high-priced tech stocks of the past decade which includes Snap Inc., Alibaba, Facebook, Twitter, Groupon, and Line. [11] Of the top six high-priced tech companies that offered an IPO in the past decade, five of the companies were named as a defendant in an IPO class action litigation. Alibaba, Facebook, Inc., Groupon, Inc. and Snap, Inc. all have faced or currently face litigation in the federal courts of New York, California, and Illinois. Twitter, Inc. faces an IPO class action in a California state court. Even though these top tech companies faced litigation, the settlement funds (for those that settled) have been a small percentage of the market cap of the company.

IPO Case Disbursements

Being that the disbursements were relatively small for the IPO class actions mentioned above, one can see a similar trend among all IPO settlements. As seen below, IPO disbursements only make up two percent of the total monies disbursed for securities class action litigations over the last 10 years. Taking a closer look at disbursements each year, IPOs appear to have an average disbursement of roughly $5 million per case compared with an average disbursement of $8 million per case for all other securities class actions. In terms of dollar value, IPOs have an even smaller footprint across securities class actions.

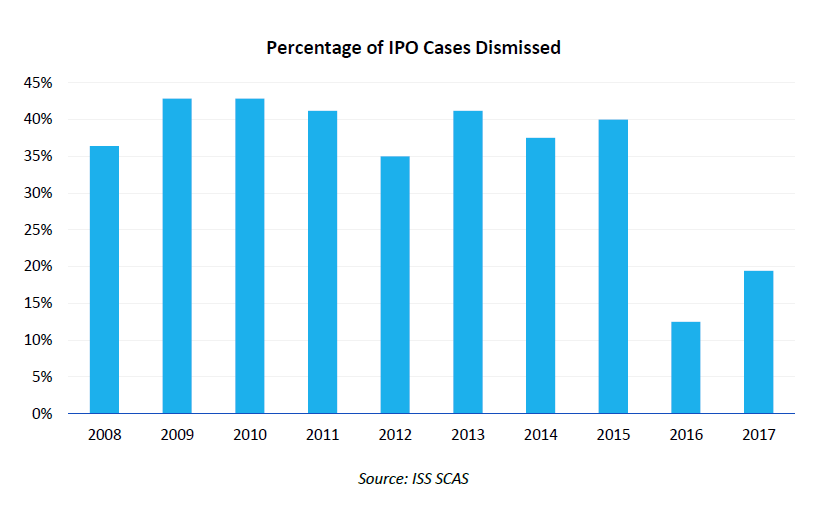

Even though IPO disbursements are a small fraction of the total monies of securities class action settlements, they have a higher probability of being fully litigated as compared to other types of securities class actions. Each year, roughly 35 to 45 percent of IPO class action filings are dismissed. Over the past decade, 32 percent of IPO class actions have, on average, been dismissed. Compare that to 49 percent of all other securities class actions cases being dismissed and one can conclude that the percentage of IPO cases surviving is greater than that for other cases.

In conclusion, even if IPO-related class actions have only filled a small space in the class actions arena over the previous ten years, the IPO class action is still a paramount opportunity for shareholders to enforce their basic rights. Shareholders, as owners of the company, should continue to have the ability and means to recoup lost assets in a public setting that shames fraudulent actors and chills fraud from occurring in the future. Given that the proposals to create mandatory arbitration for IPOs creates an uncertain future of the IPO class action, SCAS will continue to monitor the development of this important issue and to ensure clients receive compensation for all class action settlements to which they are entitled—big or small.

Data sourced from ISS Securities Class Action Services’ RecoverMax database on March 5, 2018 covering the year 2017.

Endnotes

1LaCroix, Kevin M. “The Latest on Proposed Mandatory Arbitration of Shareholder Claims.” The D&O Diary. 27 Feb. 2018: 1 Web. Accessed 1 March 2018. https://www.dandodiary.com/2018/02/articles/securities-laws/latest-proposed-mandatory-arbitration-shareholder-claims(go back)

2“Trump’s SEC Considering Shielding Companies from Investor Class Action Suits.” Insurance Journal. 29 Jan. 2018. Web. Accessed 27 Feb. 2018. https://www.insurancejournal.com/news/national/2018/01/29/478724.htm (go back)

3LaCroix, Kevin M. “The Latest on Proposed Mandatory Arbitration of Shareholder Claims.” The D&O Diary. 27 Feb. 2018: 1 Web. Accessed 1 March 2018. https://www.dandodiary.com/2018/02/articles/securities-laws/latest-proposed-mandatory-arbitration-shareholder-claims(go back)

4Fleming, Rick. “Mandatory Arbitration: An Illusory Remedy for Public Company Shareholders.” PLI’s The SEC Speaks in 2018, SEC.gov, 24 Feb. 2018, Accessed 8 Mar. 2018. https://corpgov.law.harvard.edu/2018/02/27/mandatory-arbitration-an-illusory-remedy-for-public-company-shareholders(go back)

5Ibid.(go back)

6Ibid.(go back)

7Ibid.(go back)

8Ibid.(go back)

9LaCroix, Kevin M. “The Latest on Proposed Mandatory Arbitration of Shareholder Claims.” The D&O Diary. 27 Feb. 2018: 1 Web. Accessed 1 March 2018. https://www.dandodiary.com/2018/02/articles/securities-laws/latest-proposed-mandatory-arbitration-shareholder-claims(go back)

10Ibid.(go back)

11Libassi, M. “Top 5 Tech IPOs in the Past 10 Years.” FoxBusiness.com. 2 Mar. 2017. Web. Accessed 12 Mar. 2018. https://www.foxbusiness.com/features/top-5-tech-ipos-in-the-past-10-years (go back)