Print

PrintMarc D. Jaffe and Greg Rodgers are partners at Latham & Watkins LLP and Horacio Gutierrez is General Counsel at Spotify Technology S.A. This post is based on a Latham & Watkins client alert by Mr. Jaffe, Mr. Rodgers, Mr. Gutierrez, Alexander F. Cohen, Benjamin J. Cohen, Paul M. Dudek, and Dana G. Fleischman.

Spotify Technology S.A. went public on April 3, 2018 through a direct listing of its shares on the New York Stock Exchange.

Key Points:

- A direct listing is an innovative structure that provides companies with an alternative to a traditional IPO in the path to going public.

- Spotify had a number of important goals that it wanted to achieve along with going public, and a direct listing enabled it to do so.

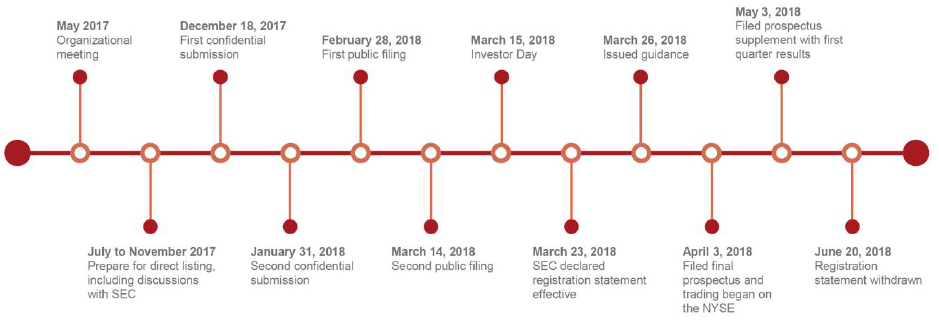

If Spotify’s direct listing were a song, it would surely be at the top of the Today’s Top Hits [1] playlist for 2018. Since Spotify first announced its intention to become a public company using this groundbreaking and innovative structure, it has generated enormous interest from the financial press and market participants.

Latham represented Spotify in the direct listing, and in this case study Latham lawyers and Spotify’s General Counsel, Horacio Gutierrez, provide a behind-the-scenes look at the transaction, including why Spotify chose to pursue a direct listing, the path to a direct listing, and the challenges encountered along the way.

What Is a Direct Listing?

In a direct listing, a company’s outstanding shares are listed on a stock exchange without either a primary or secondary underwritten offering. Existing shareholders, such as employees and early-stage investors, become free to sell their shares on the stock exchange, but are not obligated to do so. Since there is no underwritten offering, a direct listing does not require the participation of underwriters. This means that certain features that are typical of a traditional IPO—such as lock-up agreements and price stabilization activities—are not present in a direct listing. [2]

Why a Direct Listing?

When Spotify came to Latham in May of 2017 with its goal of becoming a publicly traded company, it also wanted to achieve a number of other important objectives that did not necessarily align well with a traditional US IPO process. Specifically, Spotify wanted to:

- Offer greater liquidity for its existing shareholders, without raising capital itself and without the restrictions imposed by standard lock-up agreements

- Provide unfettered access to all buyers and sellers of its shares, allowing Spotify’s existing shareholders the ability to sell their shares immediately after listing at market prices

- Conduct its listing process with maximum transparency and enable market-driven price discovery

Having enjoyed great success in the private capital markets, Spotify had no immediate need for funding. So, with a large and diverse shareholder base, a well-known brand, global scale, a relatively easily understood business model, and a transparent company culture, Spotify felt that reimagining the process of going public through a direct listing was the path that best enabled it to achieve these goals.

This post discusses each of these goals in turn.

Offer Liquidity for Shareholders

Shareholders in a private company face a basic limitation—they can’t freely resell their shares on a securities exchange. An IPO solves that problem, but at the cost (among other things) of contractual lock-up agreements. These lock-up agreements, which are commonly required by the underwriters of the IPO, typically restrict additional sales of shares outside of the IPO by certain existing shareholders and the issuer for 180 days post-listing. They are designed to assist in the distribution of the shares being offered by managing potential post-offering supply and resulting volatility in the market. By forgoing the underwritten offering process, Spotify was able to accomplish its goal of providing liquidity without imposing IPO-style lock-up agreements upon listing, and, as a result, the Spotify shareholders were free to sell their shares on the New York Stock Exchange (NYSE) immediately.

Provide Equal Access to All Buyers and Sellers

Spotify wanted to provide all buyers and sellers of its shares with unfettered access to the markets. The traditional IPO process includes a limited set of participants: a company and possibly certain existing shareholders who are offering to resell their shares in the IPO; an underwriting syndicate of investment banks that builds an order book of indications of interest from investors; and the investors who receive the initial allocation of shares being offered in the IPO at the price to the public appearing on the front page of the prospectus. Institutional buyers tend to feature prominently in the initial allocation. In the Spotify direct listing, no fixed number of shares was being sold to the public and no allocations were available at a set public offering price; rather, any prospective purchasers of shares could place orders with their broker of choice, at whatever price they believed was appropriate and that order would be part of the price-setting process on the NYSE. This open access feature and the ability of virtually all existing holders to sell their shares, and of any investor to buy their shares, created a powerful market-driven dynamic for the opening of trading.

Since virtually all of Spotify’s existing shareholders had the opportunity to participate in the first day of trading, shareholders who chose to sell were able to do so at market trading prices rather than only at the initial price to the public that would have been available to them in a traditional IPO. The ability to sell at market prices on the first day of a listing can be a significant benefit to sellers. In 2017, the average first-day return for IPOs was 11.8%, up slightly from 11.4% in 2016, but below the long-term average of 13%. [3]

As of March 28, 2018, the average first-day return for 2018 IPOs was 13.2%. [4] On April 3, 2018, when Spotify opened for trading on the NYSE, the NYSE’s initial reference price that was published to the market pre-trading was US$132.00 per share and the opening price of the shares was US$165.90 per share, or approximately 25.7% higher than the NYSE reference price. Trading in Spotify’s shares closed at a price of US$149.01 per share, which was approximately 10.2% below the opening price and 12.9% above the reference price.

Conduct the Process With Maximum Transparency and Enable Market-Driven Price Discovery

Spotify wanted to enable market-driven price discovery by providing increased transparency. To accomplish this, Spotify provided traditional public company-style guidance prior to listing. On March 26, 2018, a week before trading in its shares commenced, Spotify issued guidance to the market consistent in scope of an already public company with its financial outlook for the first quarter and full year 2018.

Spotify also made its investor education process more transparent to the public through its Investor Day. Instead of the usual IPO road show targeted to institutional investors, Spotify hosted an Investor Day presented by its entire leadership team that was publicly streamed live and viewable around the world. [5] With this increased transparency, and without any lock-up agreements, Spotify believed that market-driven supply and demand forces would allow its share price to reach a natural equilibrium. Spotify’s market valuation upon listing on the NYSE was the product of market forces at work—an unlimited number of willing buyers and willing sellers brought together through the facilities of a US stock exchange.

Spotify’s Path to Direct Listing

With a listing ecosystem designed around a traditional underwritten IPO process, Spotify had to work closely with the US Securities and Exchange Commission (SEC) Staff, the NYSE, and its financial and legal advisors to achieve its goals for the direct listing within the confines of the Securities Act, the Exchange Act, NYSE listing rules, and investor expectations. The path to a direct listing involved many features not usually found in the traditional IPO, the most significant of which are highlighted below.

The Registration Statement

As a foreign private issuer, [6] Spotify used a Form F-1 registration statement to register its shares with the SEC. Because Spotify was not selling any shares and there were no coordinated sales by any existing shareholders, the registration statement took the form of a resale registration statement. [7] This permitted existing shareholders whose shares were registered on the registration statement to resell their shares as long as the registration statement remained effective and the prospectus was current. While most of the information in the registration statement tracked the information ordinarily included in a registration statement for an IPO, there were important differences, including (1) the shares registered on the registration statement; (2) the “bona fide estimate” of the price range for the cover of the preliminary prospectus; and (3) the plan of distribution section of the prospectus, which delineates how shares may be sold under the registration statement.

Shares Registered; Rule 144 Resales

In an IPO, the registration statement registers the shares to be sold by the company and any selling shareholders, and substantially all other shares would typically be locked up from sale for a period of 180 days. Spotify wanted to ensure that existing shareholders had the option to sell on the NYSE on the first day of trading if they chose to do so. As a result, Spotify needed to either register all shareholders’ shares or ensure that an exemption from registration (such as Rule 144) would allow shareholders to sell without registration. To achieve this, Spotify registered shares held by affiliates and non-affiliates who had not held the shares for at least one year or otherwise did not meet the requirements for selling under Rule 144. Spotify registered shares held by employees to address any regulatory concerns that resales of shares by employees occurring around the time of the direct listing may not have been entitled to an exemption under the Securities Act. All non-affiliated shareholders who had held their shares for at least one year were free to resell their shares without registration pursuant to Rule 144. [8]

Spotify disclosed its intention to keep its registration statement effective for a period of 90 days after the effective date. This period was established with an eye towards the availability of the Rule 144 resale safe harbor, under which once an issuer has been subject to the Exchange Act’s reporting requirements for at least 90 days and has timely filed all required reports, an affiliate or non-affiliate that has held shares for at least six months may sell those shares under Rule 144, subject to compliance with the other requirements of the rule. Prior to being subject to those reporting requirements, neither affiliates nor non-affiliates who had held shares for less than a year would have been able to sell shares pursuant to Rule 144.

Price Range

In a traditional IPO, the cover page of the preliminary prospectus contains a price range of the anticipated sale price of the shares. That range, which is required by the SEC’s rules (in particular, Item 501(b)(3) of Regulation S-K), is usually arrived at by the issuer, any selling shareholders, and the underwriters based on the anticipated clearing price for the IPO. Since Spotify was not offering any shares, and since

Spotify’s management would play no role in initial pricing, it was not possible to include this disclosure in the preliminary prospectus. However, Spotify could not conduct investor education without an appropriate preliminary prospectus. The solution was to rely on the instructions to Item 501(b)(3) of Regulation S-K to explain how the price would be determined. The cover page of the preliminary prospectus explained that the opening public price of Spotify’s shares would be determined by buy and sell orders collected by the NYSE from broker-dealers. The NYSE’s designated market maker, in consultation with a financial advisor to Spotify (as discussed further below) and pursuant to applicable NYSE rules, would use those orders to determine an opening price for the shares. Additionally, in line with its goal of conducting the listing process transparently, Spotify disclosed recent high and low sales prices per share in recent private transactions on the cover page of the preliminary prospectus and the final prospectus.

Plan of Distribution

Since there was no underwritten offering, the registration statement did not include an underwriting section. The registration statement instead included a plan of distribution section that is typical of a resale registration statement. [9] In order to mimic the ordinary trading that would occur in the stock of a publicly listed company, the plan of distribution was limited to brokerage transactions on public exchanges or registered alternative trading venues. Given that there were no underwriters and no organized sales by the existing shareholders, the method of distribution was narrower than many resale registration statements. Nevertheless, the disclosure accomplished Spotify’s goal of providing liquidity to its shareholders without implicating an organized sale process that could be deemed an underwriting.

The plan of distribution section also described in detail the roles of the NYSE’s designated market maker, including the NYSE’s requirement that the designated market maker consult with Spotify’s financial advisor with respect to the establishment by the designated market maker of the opening price. The plan of distribution also clarified that the activities of the designated market maker in opening the shares for trading and facilitating an orderly market for Spotify’s shares would be conducted without coordination with Spotify.

Role of Financial Advisors

In the absence of an underwriting syndicate, Spotify turned to Goldman Sachs & Co. LLC, Morgan Stanley & Co. LLC, and Allen & Company LLC to serve as its financial advisors. The financial advisors assumed clearly defined roles, which included helping Spotify to define objectives for the listing, advising on the registration statement, and assisting in preparing presentations and other public communications. Morgan Stanley was also appointed by Spotify to serve as the financial advisor for purposes of consultation with the NYSE’s designated market maker as required by the NYSE’s direct listing rules.

The financial advisors did not on behalf of Spotify engage in any book-building activities, participate in investor meetings, conduct price discovery (with the exception of Morgan Stanley’s additional limited role as financial advisor consulting with the designated market maker under NYSE rules), or provide any price support or stabilization activities as they typically would in an IPO. [10]

In its capacity as financial advisor for purposes of the NYSE’s consultation requirements, Morgan Stanley provided the designated market maker with an understanding of the ownership of Spotify’s outstanding shares and the pre-listing selling and buying interest that it was aware of from potential investors and shareholders.

Investor Education

In a typical IPO, the underwriters take representatives from the company (usually the Chief Executive Officer and Chief Financial Officer) on a one or two-week “road show”, a series of group meetings with buy-side institutional investors, and one-on-one meetings with large institutional investors. Retail investors are offered a video recording of the road show, which is made freely available on the internet. [11]

These meetings are designed to help the underwriters build an order book of indications of interest from investors, which helps them gauge the level of demand for a stock. With its goal of enhanced transparency in mind, and with no need for book-building, Spotify dispensed with a traditional IPO road show and instead hosted a large-scale Investor Day.

Despite its unique features, Spotify’s Investor Day qualified as a road show under the SEC’s rules. Spotify had chosen to submit its registration statement for confidential review and was therefore required by the SEC to publicly file its registration statement at least 15 days before commencing a road show or, in this case, hosting its Investor Day. The publicly filed registration statement needed to include a “red herring” prospectus meeting the requirements of Section 10(b) of the Securities Act. [12] One of the key features of a red herring prospectus is a “bona fide estimate” of a price range on the cover, which, as noted above, Spotify satisfied by explaining the method by which the price would be determined and providing the high and low sales prices per share of recent private transactions. Finally, as is typical practice in an IPO, the Investor Day materials were consistent with the information contained in the registration statement.

Spotify held its Investor Day on March 15, 2018 after the first public filing of its registration statement on February 28, 2018. The Investor Day lasted just more than two hours, about twice as long as a traditional IPO group meeting, and involved presentations from Spotify’s entire leadership team rather than just the Chief Executive Officer and Chief Financial Officer. The Investor Day was streamed live to anyone with interest and an internet connection. Since the financial advisors did not participate in investor meetings with Spotify, Spotify relied on the strength of its internal investor relations team to lead the investor education effort.

Post-Effectiveness and Pre-Listing Period

The SEC review and comment process was generally in line with that of a traditional IPO. Perhaps not surprisingly in light of the novel characteristics of the listing, roughly a third of the SEC Staff’s comments related to the direct listing structure and the risks related to it, the procedures used in determining the opening trading price on the NYSE, and the roles of the financial advisors and the designated market maker. In its comment letters on the Form F-1, the SEC Staff appeared focused on ensuring that Spotify highlighted the direct listing structure as a novel method for going public and noting that, as a result, the trading volume and share price could be more volatile than in a traditional IPO. On March 23, 2018, the SEC declared Spotify’s registration statement effective after being in registration with the SEC for just more than three months, approximately the same timing as an IPO.

In an IPO, effectiveness would mark the end of the road show process and would mean that the offering was ready to price and begin trading the following morning. Spotify chose a different path, deciding to hold the first day of trading more than a week later, on April 3, 2018. Why such a gap? First, once Spotify was subject to the reporting requirements of the Exchange Act, it wanted to further its goal of transparency by issuing standard public company-style guidance to the market with its financial outlook for the first quarter and full year 2018 and then to allow this information to season with investors before listing and the beginning of trading. Second, in order to achieve its goals of liquidity for existing shareholders and equal access to all buyers and sellers, Spotify wanted to ensure that existing shareholders had sufficient time to deposit their shares through the Depository Trust Company (DTC) into a brokerage account prior to the first day of trading, if they wished to do so. Consequently, existing shareholders would be able to potentially trade the shares starting from the moment of the opening bell. Much of the work required to effect such deposits needed to occur after the effectiveness of the registration statement.

NYSE Rulemaking

The NYSE generally expects to list companies in connection with an IPO with a firm underwriting commitment, upon transfer from another market, or pursuant to a spin-off; in each situation, companies must demonstrate they meet specified public float thresholds. On a case-by-case basis, the NYSE had the ability to list private companies that previously had not been registered with the SEC if the company could demonstrate a US$100 million aggregate market value of publicly held shares based on a combination of both (1) an independent third-party valuation; and (2) the most recent trading price for the issuer’s shares in a trading system for unregistered securities operated by a national securities exchange or a registered broker-dealer, or a so-called private placement market. With respect to this second prong, the NYSE looks for a sustained trading history over several months. Although there was a history of private resales of Spotify shares, the trading activity would not satisfy the NYSE requirements.

As a result, in order to amend its rules to permit the direct listing of a company like Spotify, in March 2017, the NYSE began the formal rule filing process with the SEC. This process was successfully completed in February 2018, when the SEC approved a new NYSE rule that permits issuers to effect a direct listing of their shares upon effectiveness of a resale registration statement under the Securities Act and without a related underwritten IPO. The new rule provides an exception to the private placement market trading requirement for issuers that (1) have a recent valuation from an independent third party indicating at least US$250 million in aggregate market value of publicly held shares; and (2) engage a financial advisor to be consulted by the NYSE’s designated market maker in determining the opening trading price. Because its shares did not trade in a private placement market, and since the aggregate market value of its publicly held shares was higher than US$250 million, Spotify was able to take advantage of the new NYSE rule to effectuate its direct listing.

Regulation M

The non-traditional nature of the Spotify direct listing also engendered a number of conversations with the SEC Staff as to whether or not the registration of shares for resale from time to time by existing shareholders under the Form F-1 registration statement constituted an “offering” and, if so, whether such offering, particularly when viewed together with the company’s investor relations and education activities would constitute a “distribution” for purposes of Regulation M under the Exchange Act.

Regulation M contains a set of prophylactic rules intended to protect the integrity of the securities offering process by preventing persons with a financial interest in a securities offering from taking particular actions that might manipulate the market for the securities being offered. [13] In a traditional IPO, the application of Regulation M is simply assumed and the requirements, including with respect to the delineation of the applicable pre- and post-pricing “restricted period,” are well-understood and easy to implement. In the case of a direct listing, however, in which there is no underwriter to establish the offering price and no specific number of shares to be allocated and sold to the public, the start and end dates for the Regulation M restricted period, to the extent it applies to a direct listing, are unclear.

To provide some certainty as to this question, but without conceding that its direct listing constituted a distribution for Regulation M purposes, Spotify sought and received a no-action letter from the SEC Staff. The SEC Staff agreed (subject to the facts and circumstances presented) that it would not recommend enforcement action against Spotify, Spotify’s financial advisors, or the registered shareholders if the restricted period observed in this context (in relation to communications or activities not otherwise excepted under Regulation M) both:

- Commenced five business days (the typical pre-pricing period in a traditional IPO) prior to the designated market maker’s determination of the opening price of the Spotify shares on the NYSE

- Ended with the commencement of secondary market trading on the NYSE

By obtaining this no-action letter, Spotify was able to provide clarity to its shareholders and the market regarding the types of activities and communications permissible in the context of the direct listing and signaled that normal course trading activity was expected to resume on the listing date (essentially, after the first trade on the exchange).

Listing

On April 3, 2018, Spotify opened for trading on the NYSE. The NYSE’s initial reference price that was published to the market pre-trading was US$132.00 per share, which was in line with the highest sales price per share of US$132.50 for private transactions from January 1, 2018 through March 14, 2018, as disclosed on the cover page of the prospectus. Given the lack of an initial “price to public” at which the underwriters would sell shares to investors, the buy and sell orders that were being balanced by the designated market maker took longer to reach equilibrium around an opening trading price and the shares did not open for trading until shortly after 12:30 pm ET. The opening price of the shares was US$165.90 per share. The shares experienced relatively low volatility in trading on a high volume of shares (day one trading volume of 30,526,500 shares with 178,112,840 shares outstanding) and closed the first day of trading at a price of US$149.01 per share. With an intraday volatility of 12.3% on the first day of trading, Spotify’s shares experienced low volatility compared to other large technology IPOs in the past decade. [14] Overall, the listing day accomplished Spotify’s main goals in this process by providing liquidity to the company’s shareholders, equal access to all buyers and sellers, a transparent process, and a trading price that was determined by market-driven supply and demand forces.

Choosing the Path to Going Public

While Spotify proved that a direct listing is a viable alternative to an underwritten IPO, the process is certainly not right for every issuer. The success of Spotify’s direct listing was due in part to Spotify being a well-capitalized company with no immediate need to raise additional capital, while also having a large and diverse shareholder base that could provide sufficient supply-side liquidity on the first day of trading, as well as a well-recognized brand name and an easily understood business model. In addition, Spotify’s founders, board of directors, and senior management were comfortable having no involvement in establishing a market valuation and initial “price to public” of Spotify’s shares. Companies that do not share these traits may not be the right fit for a direct listing.

Nonetheless, even companies pursuing traditional firm commitment IPOs may look at aspects of Spotify’s direct listing and apply them in their offerings. For example, could IPOs without lock-up agreements or with shorter lock-up periods begin to enter the market? Will other companies choose to conduct an Investor Day like Spotify’s and forego more traditional, small-group meetings held as part of a road show?

While radical departures from the traditional IPO playbook are not imminent, elements of the direct listing process could start to filter into the traditional IPO process.

Endnotes

1Spotify’s Today’s Top Hits playlist has more than 20 million followers as of this writing.(go back)

2While a direct listing is an innovative structure, there are examples of certain analogous structures in which companies have listed on a US exchange without an underwritten offering. These structures include, among others, (1) a spin-off by a public company of a subsidiary without registration under the Securities Act in accordance with Staff Legal Bulletin No. 4; (2) the emergence of a public company from bankruptcy under Chapter 11 of Title 11 of the United States Bankruptcy Code; and (3) a listing on a US exchange by a foreign private issuer that is already listed on a non-US exchange.(go back)

3See Renaissance Capital IPO Intelligence, “2017 IPO Market: Good, But Not Great,” available at http://www.renaissancecapital.com/review/2017USReview.pdf.(go back)

4 See Renaissance Capital IPO Intelligence, “Mega Deals Drive Biggest First Quarter in a Decade,” available at http://www.renaissancecapital.com/review/RenCap1Q18_US_IPO_Review.pdf.(go back)

5Approximately 10,000 unique viewers watched the Investor Day presentation live.(go back)

6A foreign private issuer, or FPI, is an entity (other than a foreign government) incorporated or organized under the laws of a jurisdiction outside of the US unless: (1) more than 50% of its outstanding voting securities are directly or indirectly owned of record by US residents; and (2) any of the following applies: (i) the majority of its executive officers or directors are US citizens or residents; (ii) more than 50% of its assets are located in the United States; or (iii) its business is administered principally in the United States. FPIs enjoy a number of key benefits not available to domestic US issuers. These include, among others: (1) FPIs may file financial statements in US Generally Accepted Accounting Principles (GAAP), the English-language version of International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board or local GAAP; (2) FPIs are not required to file quarterly reports on Form 10-Q or current reports on Form 8-K; (3) the financial information of FPIs goes stale more slowly in a registered offering; (4) FPIs are exempt from the US proxy rules; (5) FPIs are exempt from Regulation FD; (6) FPIs are exempt from Section 16 reporting; (7) annual reports of FPIs on Form 20-F are not due until 120 days after fiscal year-end; and (8) FPIs enjoy exemptions from SEC and stock exchange corporate governance and other requirements.(go back)

7A resale registration statement is a registration statement filed with the SEC that registers under the Securities Act the resale of outstanding securities by the holders of such securities pursuant to the registration statement as long as the registration statement remains effective. Typically, a resale registration statement is filed on Form S-3 or F-3 because such forms allow a company to forward-incorporate reports filed under the Exchange Act and therefore keep the registration statement up to date with all material information regarding the company without filing a post-effective amendment or prospectus supplement. However, in order to be eligible to use a Form S-3 or F-3 registration statement, a company must, among other requirements, have been subject to the reporting requirements of Section 13 or 15(d) of the Exchange Act for at least 12 months. As a result, Spotify filed its resale registration statement on Form F-1 and Spotify filed its results for the first quarter of 2018, and Spotify also filed a prospectus supplement to update the resale registration statement. Due in part to the registration on Form F-1 (a Securities Act form), Spotify observed a traditional “quiet period” while the registration statement was effective (much to the chagrin of the financial press).(go back)

8 If an issuer has not been subject to the reporting requirements of Section 13 or 15(d) of the Exchange Act for a period of at least 90 days immediately before a sale, then Rule 144(d) requires that a minimum of one year must elapse between the latter of the date of the acquisition of the securities from the issuer or an affiliate of the issuer and any resale of such securities in reliance on Rule 144 for the account of either the acquirer or any subsequent holder of those securities. Rule 144(d) applies to both sales by an affiliate or a non-affiliate of an issuer. Additionally, any person who is an affiliate of a reporting issuer, or any person who was an affiliate at any time during the 90 days immediately before a sale, must also satisfy, among others, Rule 144(c)(1), which requires the reporting issuer to have been subject to the reporting requirements of Section 13 or 15(d) of the Exchange Act for a period of at least 90 days immediately before a sale. As a result, for the first 90 days after Spotify was subject to the reporting requirements of Section 13 or 15(d) of the Exchange Act, neither affiliates nor non-affiliates who had held shares for less than a year would have been able to sell shares pursuant to Rule 144.(go back)

9Forms S-1 and F-1 require the inclusion of the information required by Item 508 of Regulation S-K. While Item 508 of Regulation S-K is entitled “Plan of Distribution,” it is market practice in a registration statement for an underwritten IPO that the information required to be disclosed under Item 508 is included in a section entitled “Underwriting,” mainly because the disclosure requirements regarding the underwriters in that section. In resale registration statements, for which no underwriters are typically named, it is market practice that the information required to be disclosed under Item 508 of Regulation S-K is included in a section entitled “Plan of Distribution.”(go back)

10It is worth noting that because the financial advisors did not act as underwriters or otherwise participate in investor solicitation or distribution activities on behalf of Spotify, the Spotify direct listing did not trigger the filing and approval requirements that apply to a traditional IPO under the corporate financing rules of the Financial Industry Regulatory Authority (FINRA). Moreover, since there was no “allocation” of Spotify shares, FINRA’s new issue allocation rules were likewise not applicable.(go back)

11Securities Act Rule 433(h)(4) provides the formal definition of “road show” as an offer (other than a statutory prospectus) that “contains a presentation regarding an offering by one or more members of an issuer’s management … and includes discussion of one or more of the issuer, such management and the securities being offered.” Securities Act Rule 433(h)(5) defines a “bona fide electronic road show” as a road show that is a written communication transmitted by graphic means. Although free writing prospectuses (FWPs) are generally required to be filed with the SEC and a road show for an offering that is a written communication is a FWP, Rule 433(d)(8) makes clear that such road shows are not required to be filed (unless an issuer at the time of the road show is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act, which is the case in a traditional IPO). Even in the context of an IPO, a road show is not required to be filed pursuant to Rule 433(d)(8)(ii) if the issuer makes “at least one version of a bona fide electronic road show available without restriction by means of graphic communication to any person, including any potential investor in the securities … .” In an IPO, it is common to record the first road show presentation and post it on the internet for viewing by all prospective investors. This version is usually called the “retail road show.”(go back)

12A “red herring” prospectus meeting the requirements of Section 10(b) of the Securities Act is required in order for an issuer to make written offers and, subject to certain exceptions, use an FWP. As a result, prior to commencing a road show in a traditional IPO or, in Spotify’s case, holding its Investor Day, the issuer must have filed a Section 10(b) prospectus.(go back)

13Among other things, Regulation M prohibits issuers, selling securityholders, and other distribution participants (and their respective affiliated purchasers) from bidding for, purchasing, or attempting to induce any person to bid for or purchase the security that is the subject of the distribution during a specified period of time prior to pricing and ending at the completion of the distribution unless the activity falls within one of certain enumerated exceptions.(go back)

14The intraday volatility on the first day of trading for three other high-profile technology company IPOs was 15.6%, 34.7%, and 48.1%.(go back)