Print

PrintMaximilian Horster is Managing Director at ISS-ESG and Kosmas Papadopoulos is Managing Editor at ISS Analytics. This post is based on their ISS-ESG memorandum. Related research from the Program on Corporate Governance includes Socially Responsible Firms by Alan Ferrell, Hao Liang, and Luc Renneboog (discussed on the Forum here) and Social Responsibility Resolutions by Scott Hirst (discussed on the Forum here).

Summary

- Investor awareness of environmental and social shareholder is growing on both sides on the Atlantic.

- European companies generally surpass U.S. firms on climate change disclosures.

- Climate change increasingly comes to a vote in the U.S. via the shareholder proposal process, and investors increasingly expressing support at the ballot.

- Shareholder resolution filings are relatively scarce in Europe, where high ownership requirements make it difficult to file proposals in most markets (especially for individual investors).

- Cultural differences may also explain the fewer proposals filed in Europe, as institutional investors often prefer engagement to instigate change

As the world came together in Katowice, Poland for the annual U.N. climate conference last week, institutional investors were also present, as they reiterated their climate commitments through at least three side conferences geared towards financial market participants. Host country Poland’s own stance on climate change is similar to how torn the investment world is on the issue: Poland is one of Europe’s most fossil fuel-dependent economies, with 80 percent of energy produced by burning coal. However, Poland is the first European country ever to issue a Green Bond—even before climate change poster child France, which has implemented reporting requirements and organized climate summits for investors endorsed by President Macron. Institutional investors are in the same situation: While many have launched ground-breaking new investment strategies and commitments to tackle climate change, these initiatives are often small in comparison to their core assets and are merely a modest first step vis-à-vis the challenges and risks that climate change poses.

The past four years (2014, 2015, 2016, and 2017) are the four hottest years on record since 1880, when tracking of global temperatures began. Nine of the ten hottest years on record took place in the past 15 years. 2018 will likely join the top ten list, as year-to-date records indicate temperatures for the January-to-October period to be the fourth highest on record for the first ten months of the past 139 years.

Top 10 warmest years (NOAA) (1880–2017)

| Rank | Year | Anomaly °C |

|---|---|---|

| 1 | 2016 | 0.94 |

| 2 | 2015 | 0.90 |

| 3 | 2017 | 0.84 |

| 4 | 2014 | 0.74 |

| 5 | 2010 | 0.70 |

| 6 | 2013 | 0.66 |

| 7 | 2005 | 0.65 |

| 8 | 2009 | 0.64 |

| 9 | 1998 | 0.63 |

| 10 | 2012 | 0.62 |

Source: U.S. National Oceanic and Atmospheric Administration, 2018

Investors are taking note of the effects of global warming and the associated risks.

- Short-Term Risks. Signs of acute physical risks in 2018 included floods (southeast Asia and southern U.S.), droughts (California, central Europe), snow during summertime (Spain), and other extreme weather events. The world’s largest reinsurer Munich Re calls the likelihood of the increase of such weather patterns the “the new normal.”

- Long-Term Risks. Long-term physical risks include the effects on agriculture, rising sea levels, or other consequences that will likely impact communities, companies, supply chains, and investors.

- Transitional Risks. Transitional risks are the effects of climate regulation and societal change that international agreements (e.g. Paris Agreement) or national legislation (e.g. energy transition laws) can pose on companies and can impact investment returns.

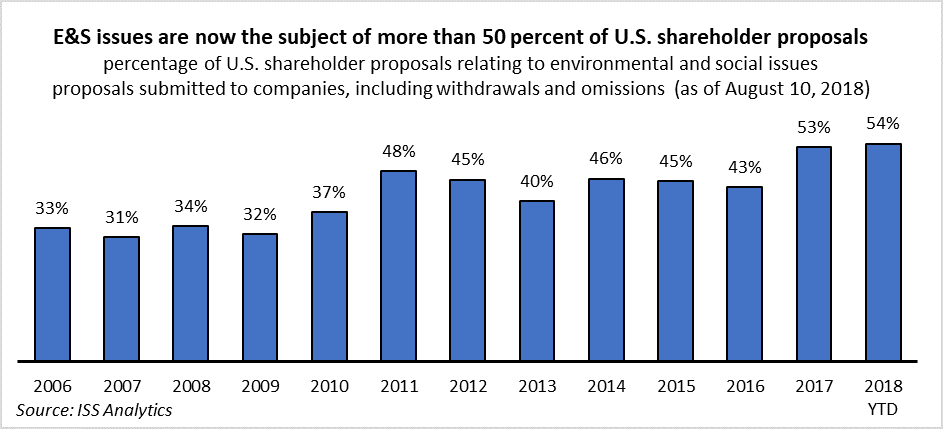

Environmental and climate proposals continue their ascent in the U.S.

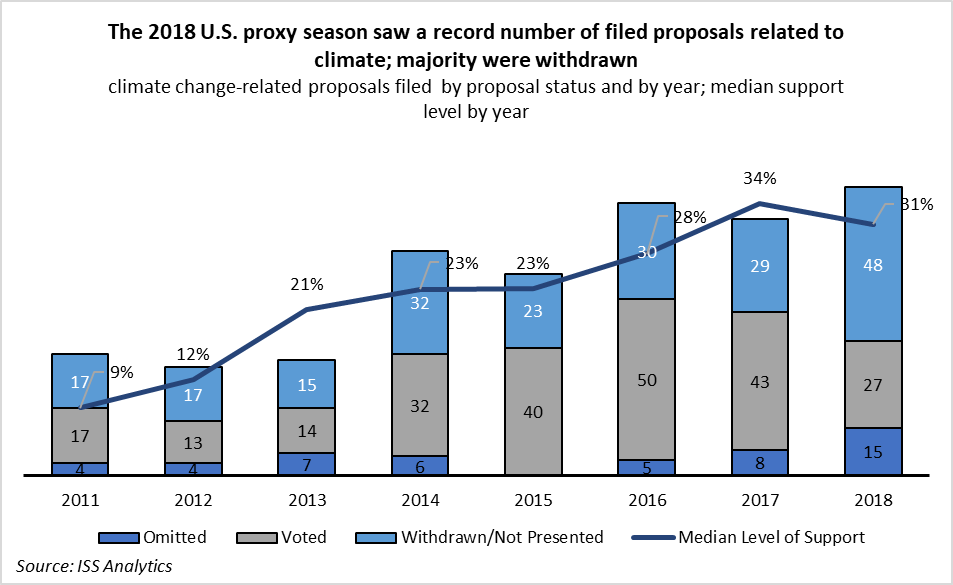

In the U.S., shareholder resolutions on climate-related issues often serve as an indicator of the level of financial market concern on the subject. In 2017 and 2018, shareholder resolutions focusing on environmental and social issues made up the majority of all filed shareholder proposals, showing a notable increase relative to resolutions focusing on governance topics compared to prior years. What is more, some members of the Chevedden Group, a group of individual shareholder proponents who have historically focused on filing dozens of proposals related to governance issues, recently indicated they will shift their focus towards environmental and social issues. Proposals focusing on the environment, including climate change, ranked first among the various categories environmental and social proposals filed in 2018, with a total of 121 proposals dealing with the environment filed at U.S. companies. Climate change-related proposals reached a record-high of 90 filed proposals. In 2018, companies were more willing to address proponent requests prior to the general meeting, following exceptionally high support levels in 2017, including majority support levels at the high-profile meetings of Exxon Mobil Corporation and Occidental Petroleum Corporation. As a result, the majority of climate-related proposals were withdrawn from ballots by proponents, indicating a successful engagement with the company. Moreover, median support levels have increased significantly in the past eight years, from single digits in 2011 to more than 30 percent in 2017 and 2018.

Proposals focusing on the environment, including climate change, ranked first among the various categories environmental and social proposals filed in 2018, with a total of 121 proposals dealing with the environment filed at U.S. companies. Climate change-related proposals reached a record-high of 90 filed proposals. In 2018, companies were more willing to address proponent requests prior to the general meeting, following exceptionally high support levels in 2017, including majority support levels at the high-profile meetings of Exxon Mobil Corporation and Occidental Petroleum Corporation. As a result, the majority of climate-related proposals were withdrawn from ballots by proponents, indicating a successful engagement with the company. Moreover, median support levels have increased significantly in the past eight years, from single digits in 2011 to more than 30 percent in 2017 and 2018.

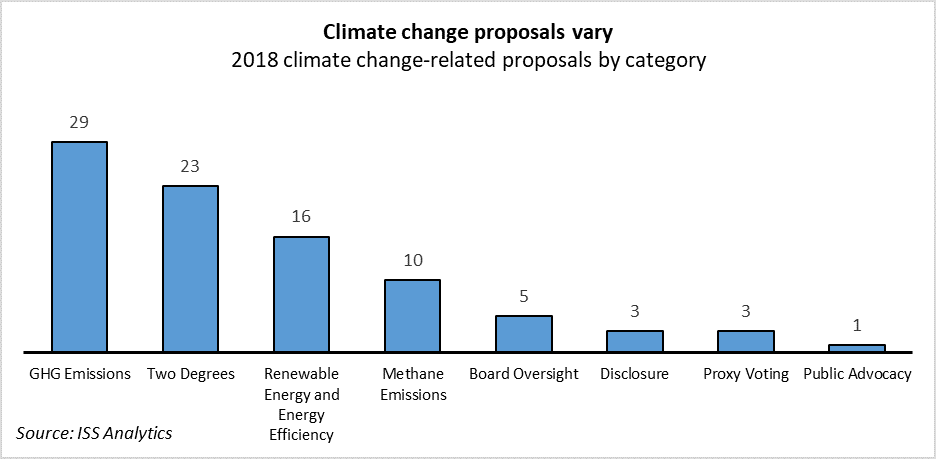

Requests to adopt and report on emissions targets and goals made a significant portion of climate-related proposals in 2018. Proposals dealing with emissions targets mark an evolution compared to the types of proposals that were filed five years ago, which primarily focused on emissions disclosure. In more recent years, shareholder proponents have been pushing for reduction targets, including goals of net-zero emissions at some companies.

In 2017, only six environmental and social shareholder resolutions in the U.S. received support by more than 50 percent of votes cast. In 2018, this number doubled to 12 resolutions, with four majority-supported resolutions dealing with climate change issues, and three proposals focusing on sustainability reporting. Social issues dominate the rest of the highly-supported items, including two relatively new types of proposals dealing with the opioid crisis and gun violence.

Majority-Supported Environmental and Social Shareholder Proposals in 2018

| Company | Shareholder Resolution | Support (F/(F+A)) |

|---|---|---|

| Rite Aid Corp. | Report on Sustainability | 80.0% |

| Sturm Ruger & Company, Inc. | Report on Gun Safety | 68.8% |

| Depomed Inc. | Governance Measures Related to Opioids | 62.3% |

| Rite Aid Corp. | Report on Governance Measures related to Opioids | 61.4% |

| Kinder Morgan | Report on Sustainability | 60.4% |

| Kinder Morgan | Climate Risk – Two Degree Scenario | 59.7% |

| Middleby Corporation | Report on Sustainability | 57.2% |

| Genesee & Wyoming | Adopt GHG Emissions Reduction Goals | 57.2% |

| Ameren Corporation | Report on Coal Ash Risks | 53.2% |

| Anadarko Petroleum | Climate Risk – Two Degree Scenario | 53.0% |

| American Outdoor Brands Corp. | Report on Gun Violence | 52.2% |

| Range Resources Corp. | Report on Methane Emissions Reduction | 50.3% |

Source: ISS Analytics

In Europe, voting is not a main avenue for shareholder engagement in relation to climate

European companies and European investors are generally more engaged on sustainability and climate change, in line with the more advanced regulatory developments and political commitments in relation to these issues in their markets. However, the topic of climate change rarely appears as a voting item in Europe. In 2018, only two climate change proposals appeared on the ballots of European companies, both of which received very low support rates. A proposal at Norwegian energy company Equinor ASA to shift company strategy from fossil fuels towards producing energy from renewable sources support by only 0.3 percent of votes cast. Meanwhile the proposal at Royal Dutch Shell plc to set and publish reduction targets for greenhouse gas emissions received support by only 5.5 percent of votes cast. The reasons for the difference in the use of shareholder proposals on the two sides of the Atlantic are both structural and cultural.

Structurally, it is much harder to file a shareholder resolution in most European markets than in the U.S. There are legal and regulatory hurdles in Europe to place items on the ballot, including higher ownership requirements. In the U.S., the ownership requirement to file a shareholder proposal is a holding of USD 2,000, while, in most European countries, shareholders are required to own between 0.5 percent and 5 percent of a company in order to be able to file a proposal (see appendix). These requirements make it extremely difficult to file proposals at large-capitalization companies, where proponents typically have their highest-impact engagements. Moreover, in some European markets, the process for filing shareholder proposal gives broad discretion to management on whether to include a resolution on the ballot, making the use of shareholder resolutions less appealing to investors. In France, Belgium, and the Netherlands, for example, companies may omit resolutions on the general grounds that they deal with subjects that are outside the competence of the general meeting.

Stringent ownership requirements, however, are not the only explanation. In Scandinavian markets, for example, owning one share is sufficient to file a proposal, and Germany allows investors with an investment of EUR 500,000 to do the same. While there are isolated cases of individual proponents filing multiple proposals related to social and environmental issues in Sweden and Denmark, these requests are often prescriptive, focus on marginal issues, and fail to gain support by more than a few percentage points of voted shares. At the same time, in Finland, Norway, and Sweden, large investors are more directly involved in the company’s governance, as many of them may have representatives in the company’s nominating committee. In addition, German law allows shareholders owning at least one share in the company to file “counterproposals.” These proposals do not appear on the ballot, and they are not necessarily voted at the meeting, because they are filed against a management proposal. Similar to the Scandinavian proposals, counterproposals are typically filed by individuals, and they often deal with issues that many investors view as marginal. As a result, the chances of success for counterproposals are very limited.

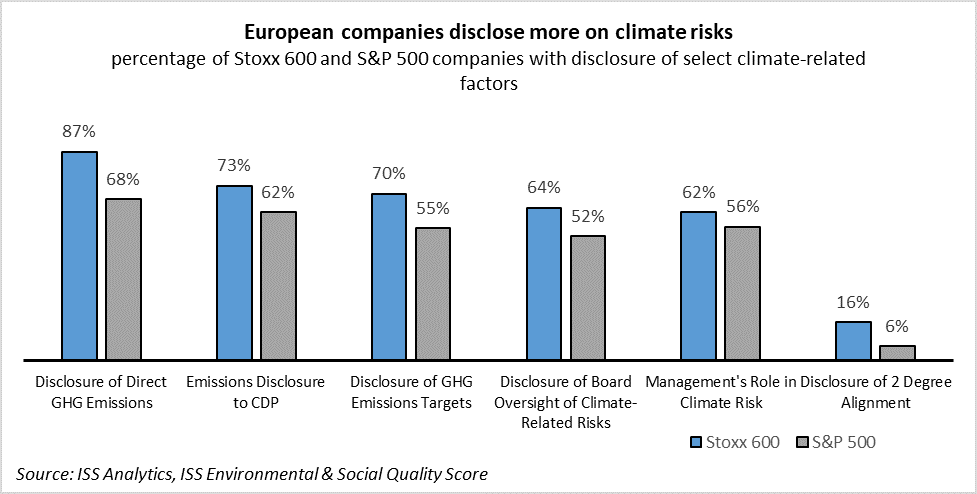

From a cultural standpoint, European markets, including businesses, appear to be closer to reaching a broader consensus around climate change risks. European firms’ disclosures on carbon emissions and the management of climate surpass their U.S. counterparts. And while companies and climate change-wary investors may not agree on all issues, consensus-building through engagement (often through collective action or letter-writing campaigns) may be the preferred approach—instead of the more public and confrontational avenue of shareholder resolutions. For many European investors, filing a shareholder resolution marks an escalation of a failed direct engagement, not the beginning of the engagement process.

However, one should not completely dismiss the possibility of more shareholder resolutions at European general meetings in the future. If regulatory changes fail to sufficiently address the goals of the Paris agreement, or if engagements between companies and investors prove unsuccessful, proponents of climate action may seek ways to bring their requests to the ballot. In the 2019 proxy season, BP plc and Royal Dutch Shell plc are both expected to face shareholder resolutions seeking reduction targets for emissions by Follow This, a Dutch-based organization. In the U.K., Follow This circumvents the 5-percent ownership rule by representing a coalition of more than 100 investors. Persistent proponents may find ways to build coalitions to make their voices heard in other markets as well.

As climate risks persist, voting on climate may evolve

While we do not expect a drastic change in shareholder proposal filing activity in the immediate future, it is important to consider that concerns about climate change risks are gaining prominence among investors on both sides of the Atlantic, and the growing urgency of the issue may result in shareholder proponents’ activities on proxy ballots heating up in the U.S. and Europe.

Beyond shareholder proposal filings, many investors are exploring ways to adopt climate change voting strategies that express concerns through voting on routine agenda items, such as director elections, executive compensation proposals, or the approval of annual reports. In the absence of a dedicated agenda item where investors can express their views on environmental and social issues, addressing such concerns via votes on routine agenda items could become more common practice.