Print

PrintDavid Bixby is managing director and Paul Hudson is principal at Pearl Meyer & Partners, LLC. This post is based on a Pearl Meyer memorandum. Related research from the Program on Corporate Governance includes Social Responsibility Resolutions by Scott Hirst (discussed on the Forum here).

With some help from leading investor groups like Black Rock and T. Rowe Price, environmental, social, and governance (“ESG”) issues, once the sole purview of specialist investors and activist groups, are increasingly working their way into the mainstream for corporate America. For some boards, conversations about ESG are nothing new. For many directors, however, the increased emphasis on the subject creates some consternation, in part because it’s not always clear what issues properly fall under the ESG umbrella. E, S, and G can mean different things to different people—not to mention the fact that some subjects span multiple categories. How do boards know what it is that they need to know? Where should boards be directing their attention?

A natural starting place for directors is to examine the guidelines published by the leading proxy advisory firms ISS and Glass Lewis. While not to be held up as a definitive prescription for good governance practices, the stances adopted by both advisors can provide a window into how investors who look to these organizations for guidance are thinking about the subject.

Institutional Shareholder Services

In February of 2018, ISS launched an Environmental & Social Quality Score which they describe as “a data-driven approach to measuring the quality of corporate disclosures on environmental and social issues, including sustainability governance, and to identify key disclosure omissions.”

To date, their coverage focuses on approximately 4,700 companies across 24 industries they view “as being most exposed to E&S risks, including: Energy, Materials, Capital Goods, Transportation, Automobiles & Components, and Consumer Durables & Apparel.” ISS believes that the extent to which companies disclose their practices and policies publicly, as well as the quality of a company’s disclosure on their practices, can be an indicator of ESG performance. This view is not unlike that espoused by Black Rock, who believes that a lack of ESG disclosure beyond what is legally mandated often necessitates further research.

Below is a summary of how ISS breaks down E, S, & G. Clearly the governance category includes topics familiar to any public company board.

ISS’ E&S scoring is based on answers to over 380 individual questions which ISS analysts attempt to answer for each covered company based on disclosed data. The majority of the questions in the ISS model are applied to all industry groups, and all of them are derived from third-party lists or initiatives, including the United Nations’ Sustainable Development Goals. The E&S Quality Score measures the company’s level of environmental and social disclosure risk, both overall and specific to the eight broad categories listed in the table above. ISS does not combine ES&G into a single score, but provides a separate E&S score that stands alongside the governance score.

These disclosure risk scores, similar to the governance scores companies have become accustomed to seeing each year, are scaled from 1 to 10 with lower scores indicating a lower level of risk relative to industry peers. For example, a score of 2 indicates that a company has lower risk than 80% of its industry peers.

Glass Lewis

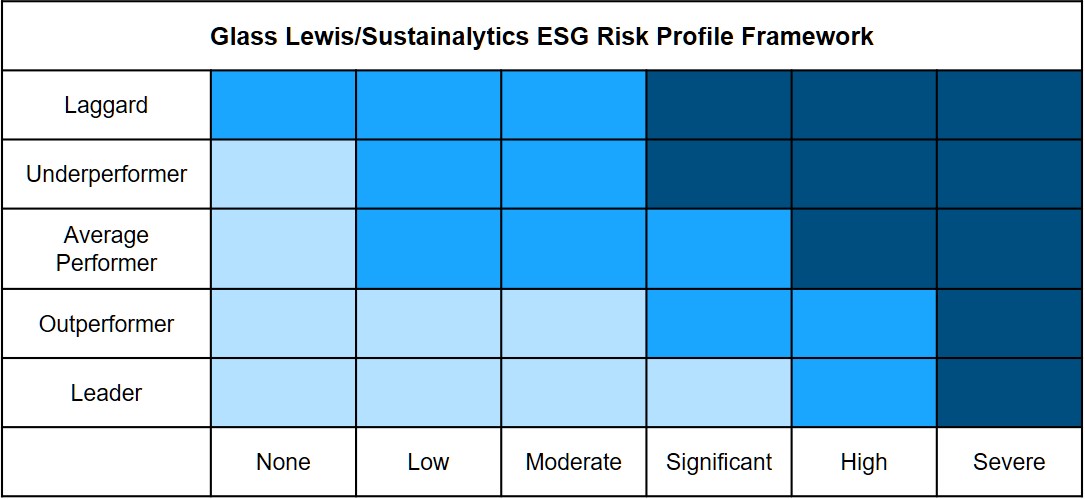

Glass Lewis uses data and ratings from Sustainalytics, a provider of ESG research, in the ESG Profile section of their standard Proxy Paper reports for large cap companies or “in instances where [they] identify material oversight issues.” Their stated goal is to provide summary data and insights that can be used by Glass Lewis clients as part of their investment decision-making, including aligning proxy voting and engagement practices with ESG risk management considerations.

The Glass Lewis evaluation, using Sustainalytics guidelines, rates companies on a matrix which weighs overall “ESG Performance” against the highest level of “ESG Controversy.” Companies who are leaders in terms of ESG practices (or disclosure) have a higher threshold for triggering risk in this model.

The evaluation model also notes that some companies involved in particular product areas are naturally deemed higher risk, including adult entertainment, alcoholic beverages, arctic drilling, controversial weapons, gambling, genetically modified plants and seeds, oil sands, pesticides, thermal coal, and tobacco.

Conclusion

ISS and Glass Lewis guidelines can help provide a basic structure for starting board conversations about ESG. For most companies, the primary focus is on transparency, in other words how clearly are companies disclosing their practices and philosophies regarding ESG issues in their financial filings and on their corporate websites? When a company has had very public environmental or social controversies—and particularly when those issues have impacted shareholder value—advisory firm evaluations of corporate transparency may also impact voting recommendations on director elections or related shareholder proposals.

Pearl Meyer does not expect the advisory firms’ ESG guidelines to have much, if any, bearing on compensation-related recommendations or scorecards in the near term. In the long term, however, we do think certain hot-button topics will make their way from the ES&G scorecard to the compensation scorecard. This shift will likely happen sooner in areas where ESG issues are more prominent, such as those specifically named by Glass Lewis.

We are recommending that organizations take the time to examine any ESG issues relevant to their business and understand how those issues may be important to stakeholders on a proactive basis, perhaps adding ESG policies to the list of sunny day shareholder outreach topics after this year’s proxy season. This does take time and effort, but better that than to find out about a nagging ESG issue through activist activity or a negative voting recommendation from ISS or Glass Lewis.