Print

PrintBarbara Novick is Vice Chairman at BlackRock, Inc. This post is based on a Policy Spotlight issued by Blackrock.

Index funds have democratized access to diversified investment for millions of savers who are investing for long term goals, like retirement. However, the popularity of index funds has drawn critics, who claim that index fund managers may wield outsized influence over corporations through their proxy voting and engagement. Executive compensation is often cited as an example because public company shareholders can participate in ‘say-on-pay’ votes. As discussed in the Policy Spotlight, Proxy Voting Outcomes: By the Numbers, index fund managers are rarely the determining factor in say-on-pay votes. That notwithstanding, the focus on say-on-pay is misplaced, since executive compensation is neither structured nor decided by shareholders. Rather, a process is undertaken by the Board of Directors, often under the advisement of the Board’s compensation committee and/or compensation consultant, to determine the amount and composition of executive pay packages. This post provides an explanation of the process by which executive compensation is determined, and the role of shareholders in that process. First, we begin by outlining the roles of the various parties that are relevant to executive compensation determinations:

- Boards of Directors are ultimately responsible for making executive compensation decisions. The Board relies primarily on input from its Compensation Committee (or similar committee) to make this determination, as well as compensation consultants, who are often hired by the Compensation Committee.

- A Compensation Committee is a Board committee that is composed of independent directors (directors who are not company executives). The Compensation Committee is charged with designing the executive compensation program and determining executive compensation. In the US, the role of the Compensation Committee is disclosed in annual proxy statements that each company files with the SEC.

- Compensation Consultants are independent advisors who are often retained by the Compensation Committee to provide advice on executive compensation. Compensation Committees are not required to engage a compensation consultant; however, nearly 90% of large companies use compensation consultants and 90% of retention agreements are made directly with the Compensation Committee or Board. [1] In addition to traditional compensation consultants, advisors to the Compensation Committee may include tax and accounting experts in particularly complex situations.

Independence from management in both hiring and continuing relationships with compensation consultants is important to assure that the compensation consultant is truly an advisor to the Board, which in turn is charged with a fiduciary duty to all shareholders. In the US, the use of compensation consultants is disclosed in annual proxy statements that each company files with the SEC. While there are a number of compensation consultants, Exhibit 1 shows the ten compensation consultants most often retained by large cap companies based on proxy statement disclosures.

Exhibit 1: Top 10 Compensation Consultants

| Rank | Consulting Firm | Rank | Consulting Firm |

|---|---|---|---|

| 1 | Frederic W. Cook & Co. | 6 | Towers Watson |

| 2 | Meridian Compensation | 7 | Mercer |

| 3 | Pay Governance | 8 | Exequity |

| 4 | Pearl Meyer & Partners | 9 | Compensation Advisory Partners |

| 5 | Semler Brossy Consulting Group | 10 | Compensia |

Source: Equilar. As of March 2019.

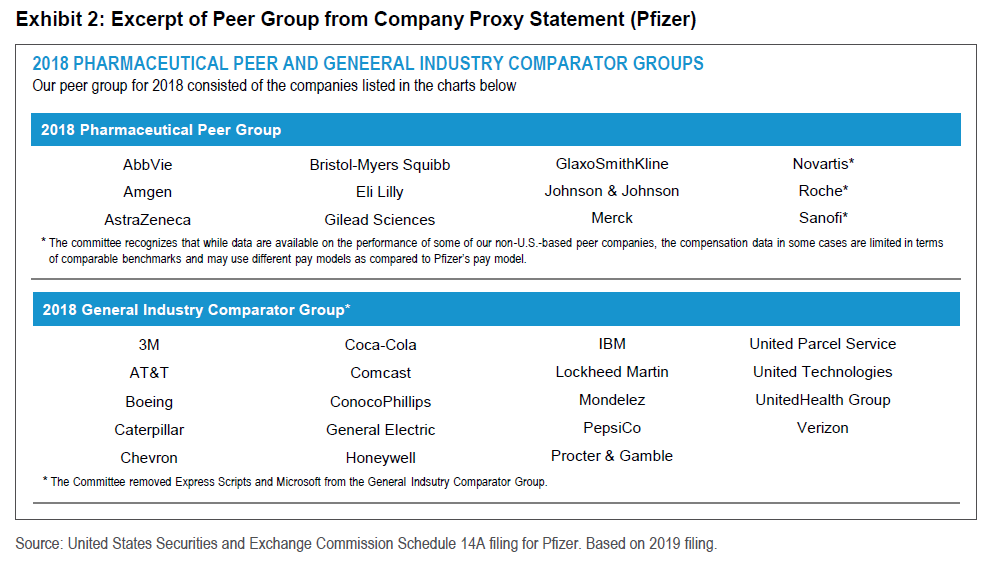

In setting executive compensation, a Board considers the mix of fixed (salary and benefit) and variable (performance-based) compensation, as well as the form of compensation. The Board is informed in this review by individual and company performance, both in the current compensation year and also over the longer-term (usually 3 to 5 years). Variable compensation often vests over a period of time under a plan that sets specific targets for both individual and company performance. The Board considers the quantum and structure of compensation relative to what executives in similar companies (by industry, sector, size and complexity of business) may earn. Oftentimes the compensation consultant performs a peer group analysis for the Compensation Committee to facilitate this comparison. The compensation consultant will develop a relevant ‘company peer group,’ which is determined by reference to companies within the same or similar sectors. Peer groups are often publicly disclosed by companies as a reference point in how the Board reaches its compensation decision. An example of a peer group disclosed in a company’s proxy statement is shown in Exhibit 2.

At its heart, peer group analysis presumes that a successful executive in one company would be equally successful in a similar one, and thus compensation should be comparable. Peer group analysis also helps companies ensure that they are compensating their executives in line with industry standards for talent retention purposes. The compensation consultant helps guide the Compensation Committee, and ultimately the Board, throughout the review process, including comparisons to programs in other companies. The consultant also provides analysis on how it believes proxy advisors and institutional shareholders will view a particular compensation package against their guidelines, so the Board can be fully informed as to likely reactions, especially if significant compensation changes are under consideration. A report of how executive compensation was determined is included in companies’ annual proxy statements that are filed with the SEC. Exhibit 3 provides excerpts of disclosures made by US public companies on various aspects of the determination of executive compensation packages—the discussions included in proxy statements are quite detailed so these excerpts are meant to be illustrative rather than exhaustive.

Exhibit 3: Excerpts from Company Proxy Statements

Microsoft

Use of compensation consultants

“The Compensation Committee retains Semler Brossy Consulting Group, LLC (“Semler Brossy”) to advise the Committee on marketplace trends in executive compensation, management proposals for compensation programs, and executive officer compensation decisions…Semler Brossy is directly accountable to the Committee. To maintain the independence of the firm’s advice, Semler Brossy does not provide any services for Microsoft other than those described above.”

Johnson & Johnson

Peer group analysis

“The Committee compares our executive compensation levels and practices to those of the Executive Peer Group companies. It consists of companies that generally: are similar to Johnson & Johnson’s size and scope; have executive positions similar to ours; and compete with us for executive talent. The Committee reviews the composition of the Executive Peer Group annually. We compare our salaries, annual performance bonuses, long-term incentives, and total direct compensation to the Executive Peer Group companies. We also compare our benefits, perquisites and other compensation to the Executive Peer Group.”

United Health Group

Compensation Committee role

“The Compensation Committee oversees the Company’s policies and philosophy related to total compensation for executive officers. The Compensation Committee approves the compensation for the named executive officers based on its own evaluation, input from our CEO (for all executive officers except himself), internal pay equity considerations, the tenure, role and performance of each named executive officer, input from its independent consultant and market data.”

Sources: United States Securities and Exchange Commission Schedule 14A filings for Microsoft, Johnson & Johnson, and United Health Group Inc. Based on 2018 filings.

Ultimately, the goal of any executive compensation program should be to incentivize senior executives to enhance company performance relative to prior years and relative to its competitors for the benefit of all shareholders. In general, Compensation Committees will set out metrics against which executive performance will be assessed, which provides some rigor around the determination of executive compensation. Examples of compensation metrics contained in company proxy statements are set out in Exhibit 4.

Exhibit 4: Examples of Compensation Metrics Included in Company Filings

American Airlines Group

Our CEO and other executive officers have demonstrated their commitment to fair pay and pay for performance by initiating the following exceptional actions with respect to their compensation.

- Since 2015, at Mr. Parker’s request, we provide 100% of his direct compensation in the form of equity incentives in lieu of base salary and annual cash incentive compensation. That has helped to advance our commitment to paying for performance and aligning Mr. Parker’s interests with that of our stockholders. More than half of these equity incentives will be earned not earlier than the third anniversary of the grant date based on our relative pre-tax income margin and total stockholder return (TSR) performance.

- At his request, Mr. Parker’s target direct compensation has been historically set at below the average for his peers at Delta and United.

- Also at his request, in 2016, our Compensation Committee agreed to eliminate Mr. Parker’s employment agreement so that he is no longer contractually entitled to receive a set level of compensation and benefits and is no longer protected by the change in control and severance provisions of that employment agreement.

United Continental Holdings, Inc.

Our 2017 incentive awards are directly tied to Company performance metrics that we believe are appropriate measures of our success and that will lead to value for our stockholders:

- annual pre-tax income;

- long-term pre-tax margin performance improvement (measured on a relative basis versus our industry peers);

- stock price performance;

- operational performance, as measured by key indicators of customer satisfaction (on-time departures, flight completion factor, and mishandled baggage ratio); and

- specified strategic initiatives designed to enhance management focus on key corporate objectives.

We eliminated ROIC performance, which had historically been included as a performance measure under our prior long-term incentive program design, from our 2017 long-term incentive design in order to accommodate greater focus on our pre-tax margin results. The 2017 long-term incentive structure is equally divided between the pre-tax margin Performance-Based RSU awards and time-vested RSU awards, which provides stability and retentive features to the design.

Sources: United States Securities and Exchange Commission Schedule 14A filings for American Airlines Group Inc. and United Continental Holdings, Inc. Based on 2018 filings.

The mix of cash and non-cash compensation and the aggregate amount of compensation, which is subject to deferral or future vesting, has evolved over the years. Further, compensation programs may differ depending on the size of the company and where it is in terms of its lifecycle. For example, emerging growth companies are more likely to use options as part of their compensation program, while established companies generally use restricted share grants. Tax and accounting rules can drive some compensation design issues. Increasingly, certain practices, including the trend toward greater use of performance based compensation (compensation that is only paid or vested if specific performance metrics are achieved), are driven by criteria established by proxy advisors.

US public companies must disclose in their annual proxy statements the amount and type of compensation (including perquisites) paid to its CEO, CFO and the three other most highly compensated executive officers. In addition, US public companies are required to disclose the criteria used in reaching executive compensation decisions and the relationship between the company’s executive compensation practices and corporate performance. Likewise, many other countries require executive compensation disclosures, with varying degrees of granularity (see section on Regional Differences).

As discussed in the following sections, compensation consultants consider the guidelines of proxy advisors as well as the views of institutional shareholders as inputs into the design of executive compensation packages.

The Role of Proxy Advisors

Proxy advisors are a critical component of the proxy voting system as they affect both the design of compensation packages and the vote outcomes for ‘say-on-pay’ votes and director elections related to compensation decisions. This contributes to the considerable influence that proxy advisors can have in executive compensation matters, as it has been estimated that due to the mechanical voting of some institutional investors, recommendations by proxy advisory firms can determine between 15-25% of a say-on-pay vote. [2] For more information on the role of proxy advisory firms, please see our recent ViewPoint, The Investment Stewardship Ecosystem.

The major proxy advisors have established compensation guidelines that are focused on ‘pay for performance’ relative to a peer group determined by the proxy advisor. Importantly, proxy advisor peer groups may differ from the peer groups identified by the Board and its compensation consultant. Failure to clearly link executive compensation to performance, or the use of weak performance standards, can result in a negative vote recommendation from proxy advisors on the say-on-pay ballot item. Other compensation practices, such as the inclusion of tax gross-up rights or single trigger severance arrangements, can also result in a negative recommendation. In some cases, the negative recommendation goes beyond the say-on-pay vote and includes a recommendation to vote against directors on the compensation committee or even directors at large. Some believe that over time, deference to the proxy advisors’ models and policies has led to more standardization and fewer compensation programs tailored to the particular circumstance of the company and the executives that the compensation policy is intended to incentivize. This homogeneity can reduce the effectiveness of pay plans and their alignment with corporate performance.

Say-on-Pay

Shareholders’ participation in ‘say-on-pay’ votes is often pointed out as a mechanism by which shareholders express their view on executive compensation. Yet, the nature and content of say-on-pay is not well-understood. Most people assume that a say-on-pay vote is a vote to approve the executives’ compensation for the current year. This is an incorrect assumption.

In the US, say-on-pay votes are non-binding advisory votes by shareholders, most commonly conducted on an annual basis at the annual general meeting. [3] As an advisory vote, even were a say-on-pay proposal to not receive majority support, this would not prevent a company from implementing its pay practices. Say-on-pay votes ask shareholders to opine retrospectively on the compensation of named executives that is disclosed in the proxy statement, rather than on the company’s compensation program going forward. The proxy statement disclosure includes the compensation paid to the top five named executive officers over the previous three fiscal years, as well as the Compensation Discussion and Analysis, which provides additional narrative around the objectives of a company’s compensation plan and how they are implemented. [4], [5] Say-on-pay requirements were put in place in the US in 2011 under provisions of the Dodd-Frank Act.

When there is a large vote against a particular say-on-pay proposal (or vote against directors due to prior compensation decisions), it is often based on views that the compensation is considerably out of alignment with company performance and shareholder returns. Thus, a significant level of shareholder dissent often leads to engagement between a company and its shareholders to understand the concerns regarding the executive compensation program and to gather input for the structuring of future compensation packages. Further, while non-binding, failure to heed majority votes against executive compensation may result in future votes against Board directors. Some institutional investors also expect that the Compensation Committee will engage with them in the event of a sizeable ‘against’ vote (generally 25%-30%), and will vote against directors if they fail to engage.

Nevertheless, data show that most say-on-pay proposals pass by a large majority. When there is a closer vote, the explanation is often found in the ‘against’ recommendation of proxy advisory firms. That said, larger institutional investors may take a more nuanced analysis of compensation decisions and, as a result, support the say-on-pay proposal often following engagement. We explore the levels of support received for say-on-pay votes as well as other types of votes in the Policy Spotlight, Proxy Voting Outcomes: By the Numbers.

Regional Differences

Generally speaking, the manner by which executive compensation at public companies is determined is consistent across regions. That said, there are some regional differences worth noting. Firstly, Compensation Committees in Europe are referred to as ‘Remuneration Committees’ and most national corporate governance codes or domestic laws require companies to have ‘remuneration committees’. Under the Shareholder Rights Directive II (SRD II), shareholders will be able to express their view twice. Ex-ante proxy votes related to remuneration at European companies focus on approving the remuneration policy that lays down the framework within which remuneration can be awarded to directors. The remuneration policy must be subject to a vote by shareholders at a general meeting at least every four years and after a material change. These remuneration votes will in principle be binding (as opposed to the non-binding say-on-pay votes in the US), though Member States are able to opt for remuneration votes to instead be advisory votes. This means that companies are allowed to apply a remuneration policy that has been rejected by shareholders, but they are required to submit a revised policy at the next general meeting. Further, in Europe under the SRD II, companies must prepare and publish on their website an annual directors’ remuneration report. Here shareholders will vote ex-post on the remuneration report describing the remuneration granted in the past financial year: this vote will only be advisory.

Say-on-pay requirements were put into place in 2003 for UK companies. Similar to SRD II, currently shareholders have the right to cast both an ex-ante and an ex-post vote. As per amendments to the Companies Act in 2013, the ex-ante vote is referred to as the ‘remuneration policy’ vote, and it is binding and occurs every three years. The ex-post vote is known as the ‘remuneration report’ vote or ‘implementation report’, and it is advisory and occurs annually.

Bottom line:

‘Say-on-Pay’ votes permit shareholders to express their views on executive compensation, but they do not dictate how much executives will be paid. Boards of directors, their Compensation Committees, and compensation consultants design, structure, and approve compensation plans. While shareholders do engage with companies to encourage good governance practices and alignment with company performance, compensation consultants and proxy advisors have a greater influence over the structure of executive compensation packages. Ultimately the decision on executive compensation is that of the Board.

Endnotes

1Ryan Chacon, Rachel Gordon, Adam S. Yore, Compensation Consultants: Whom do they serve? Evidence from Consultant Changes (January 2019).(go back)

2Nadya Malenko and Yao Shen, Boston College, The Role of Proxy Advisory Firms: Evidence from a Regression-Discontinuity Design (Aug. 2016), available at https://www2.bc.edu/nadya-malenko/Malenko,Shen%20(RFS%202016).pdf.(go back)

3Per section 951 of the Dodd-Frank Act, US companies must also provide shareholders with the ability to vote, also on an advisory basis, on the ‘frequency’ (one, two or three year) of the ‘say-on-pay’ vote.(go back)

4Final Rule 14a-21(a) requires that companies hold a say on pay vote at least every three years to approve the compensation disclosure required by item 402 of Regulation S-K.(go back)

5By contrast to say-on-pay votes which are retrospective and non-binding, management equity plans that also appear on company ballots are forward looking and are binding in As noted in the BlackRock Investment Stewardship 2018 annual report, equity plans are intended to incentivize and reward participants and provide a way for them to share in the long-term future success of the company. The fact that equity plan proposals are binding makes them as an effective tool to underscore concerns when equity is not being used effectively at the company. Management equity compensation plans are a means to attract and retain talent—in essence, a human capital management tool. These plans are particularly important when they apply to a wide range of employees. They can help create an ‘ownership’ mentality, and provide a streamlined incentive structure across the employee base.(go back)