Print

PrintSteve W. Klemash is Americas Leader and Jamie C. Smith is Associate Director at the EY Center for Board Matters. This post is based on their EY memorandum. Related research from the Program on Corporate Governance includes Socially Responsible Firms by Alan Ferrell, Hao Liang, and Luc Renneboog (discussed on the Forum here) and Social Responsibility Resolutions by Scott Hirst (discussed on the Forum here).

As the spotlight on board diversity intensifies, the pace at which women are joining boards is accelerating, and a growing number of companies are disclosing the board’s racial and ethnic diversity. At the same time, against a backdrop of increased focus on companies’ efforts to create long-term value, enhanced proxy disclosures on corporate sustainability highlight how companies are protecting the environment, considering their social impact, investing in their people and promoting diversity and inclusion.

Investor outreach, often involving directors, has become a mainstay of leading governance practice among top companies. Overall, investors show notable support for directors and executive pay programs. A growing support for many environmental and social shareholder proposals highlights further opportunity for engagement.

This post provides five key takeaways for boards as they reflect on this proxy season and evolving governance developments. [1]

While director opposition has crept up in recent years, partly in connection with stricter board gender diversity and overboarding policies, we continue to see more than 90% average support for director elections and executive compensation programs.

• Only 6% of director nominees have received less than 80% support, and just 0.3% have not secured majority support.

• Only 8% of say-on-pay votes have secured less than 70% support, and just 2% have not achieved majority support.

1. Gender diversity accelerates

Last year we reported on the advancement of gender diversity on boards in the wake of major institutional investors incorporating gender diversity expectations into their director voting policies. Since then the pressure on boards to diversify has increased, partly due to state legislatures taking up the issue. In September, the California General Assembly passed a bill urging publicly traded state companies to add more women to their boards, and New Jersey is now considering similar legislation. [2] Against this backdrop, women are joining boards at a faster pace, all-male boards are disappearing among the largest companies and more investors are demonstrating their board diversity views through proxy voting.

Rate of increase in women-held directorships doubles

After growing just one percentage point each year since 2013, the rate of increase in women-held directorships has doubled, increasing two percentage points in both 2018 and 2019 to reach 23%. If this pace sustains, gender parity will be reached across the S&P 1500 by 2033, versus 2046 at the previous pace.

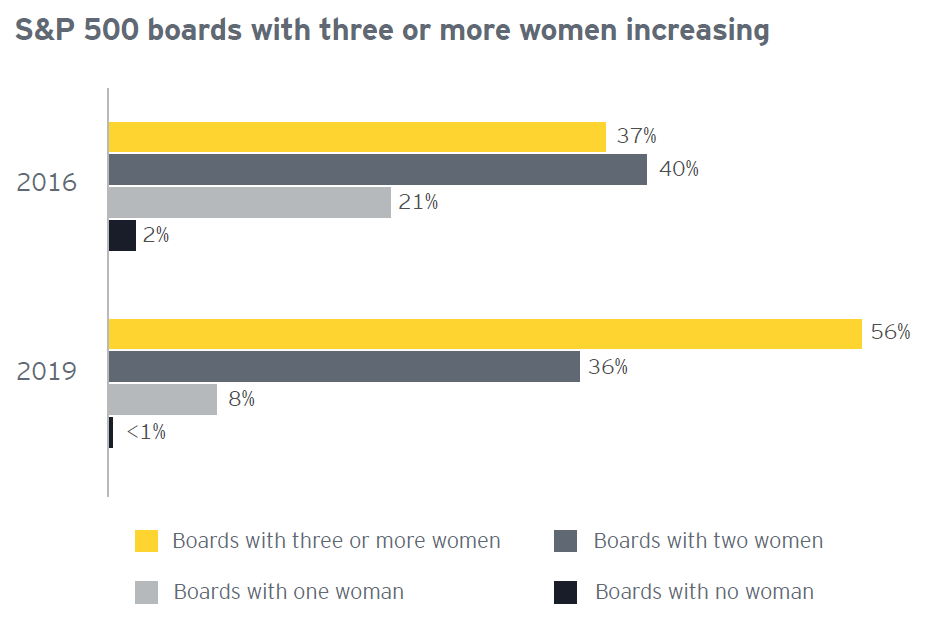

All-male boards nearly extinct

Most (56%) S&P 500 boards now have at least three female directors, up from 37% in 2016. At the same time, all-male boards have nearly

disappeared (fewer than 1%). A similar, but less dramatic, shift is underway across the S&P 1500. The portion of companies with three or more women on the board has grown from 20% in 2016 to 34% this year, and just 5% remain all-male.

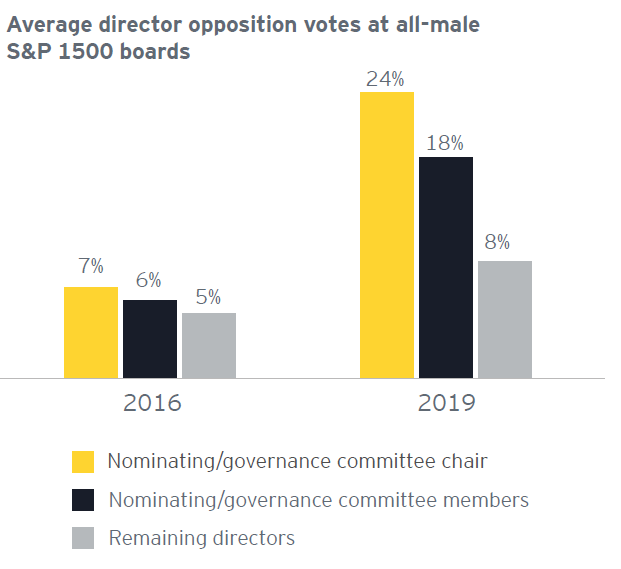

Votes against all-male boards continue to climb

This year we continue to see increasing opposition to all-male boards. While director opposition votes typically average around 4%-5%, average votes against all-male boards are significantly higher—and rising. Votes against nominating/ governance chairs at all-male S&P 1500 boards have tripled since 2016, with those chairs receiving an average opposition vote of 24% this year. By comparison, average opposition votes for nominating/governance chairs on boards that are at least 20% female were just 5% this year. Similarly, votes against nominating/governance committee members and all other board members at all-male S&P 1500 boards rose to 18% and 8%, respectively, compared with 4% and 3% for their counterparts at boards composed of 20% women.

Key board takeaway

Challenge the board’s director recruitment and refreshment processes. Prioritize building diverse personal networks, and require director recruitment firms to include women and minorities in the candidate pool. Also look beyond search firms to nontraditional sources for obtaining diverse candidates, including executives who have yet to serve on a board. Consider the tone the company is setting for diversity through the board’s composition.

2. Diversity disclosures on the rise

Racial/ethnic diversity disclosures climb

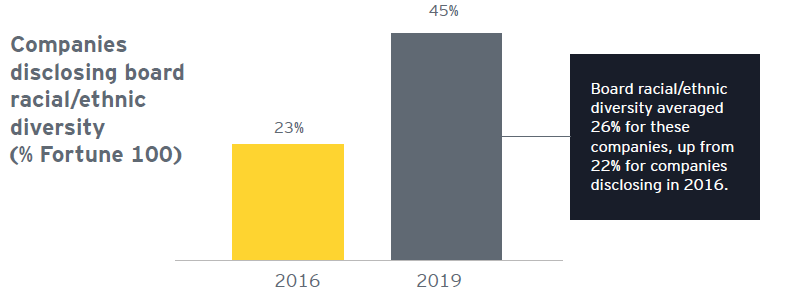

When we spoke with more than 60 investors this past fall, over half (53%) emphasized that boards should make diversity, primarily inclusive of gender, race and ethnicity, a top focus in 2019. Many noted that assessing racial and ethnic board diversity poses a challenge given the current lack of disclosure. According to these investors, gender can largely be inferred, but self-identification by directors and explicit disclosure in the proxy are needed for reliable racial and ethnic diversity information. Thirty percent of investors who said boards should focus on diversity also said they are asking companies for better disclosure of director demographics.

More companies are starting to respond: this year, close to half (45%) of the Fortune 100 explicitly disclosed the board’s racial/ ethnic diversity, up from 23% three years ago. More boards are also disclosing their aggregated diversity, combining diversity across gender, race, ethnicity and sometimes other identity categories to provide an overall percentage of “diverse” directors. This year, 36% of the Fortune 100 disclosed the level of overall diversity on the board, up from just 13% in 2016.

More changes in board diversity disclosures could be forthcoming. The SEC’s recently released Regulation S-K Compliance and Disclosure Interpretations (C&DIs) states that where director nominees have self-identified diversity characteristics and consented to their disclosure, the company’s disclosures should identify those characteristics, along with other qualifications or attributes, to the extent they were considered by the board or nominating committee in evaluating board membership. This guidance could lead to enhanced diversity disclosures in future proxy statements, but such change will hinge on director willingness to self-identify, and some directors may choose to not do so for personal reasons.

While the likelihood of passage is unclear, federal legislation has been introduced that would require companies to disclose information related to the racial, ethnic and gender makeup of boards and senior executives, among other things. [3] Similarly, a proposed diversity bill in Illinois would require companies to report on the self-identified gender and minority status of directors. [4]

More companies disclosing skill matrices

Investors remain focused on whether boards have a diversity of skills and experience that align to the company’s evolving strategy and risk profile.

Three-quarters of the Fortune 100 now use a skills matrix to highlight the diversity of relevant director qualifications in an easily readable format, up from 30% in 2016. The areas of expertise most frequently cited in independent nominees new to the board in 2018 were international business, corporate finance and accounting, and industry expertise. Nearly one-quarter of those directors were also recognized for their experience in innovation, transformation and in navigating change. [5]

Key board takeaway

Enhance director diversity disclosures to highlight the board’s current diversity across director characteristics and qualifications, and communicate any commitments to increasing diversity. Challenge whether the proxy statement effectively communicates why the company has the right directors at the right time who bring a diversity of relevant perspectives and expertise.

3. Companies voluntarily enhance communication around corporate sustainability and citizenship

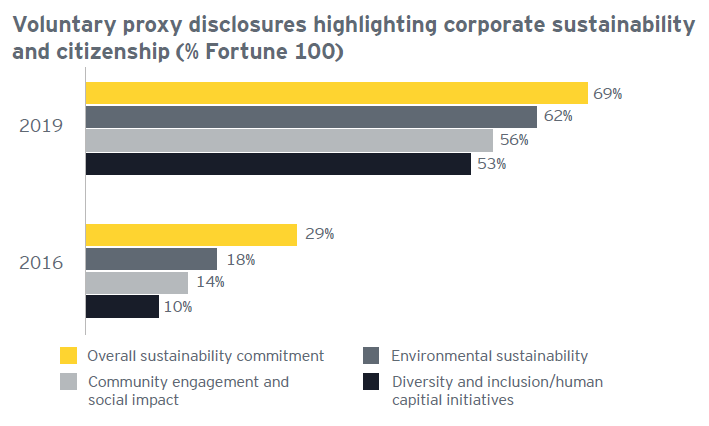

Proxy disclosures around how companies are creating broader, long-term value for their employees, communities and society are rapidly evolving. Since 2016, the number of Fortune 100 companies using the proxy to highlight their commitment to corporate sustainability and citizenship has more than doubled. Most leading companies now use the proxy to highlight the company’s approach to environmental sustainability, people and culture, community investment and social impact.

This evolution aligns with growing investor interest in environmental, social and governance (ESG) considerations. Indeed, 63% of Fortune 100 companies that disclose engaging with investors over the past year say environmental and social factors were among the topics of focus. Many investors have also told us they are further integrating ESG considerations into their stewardship programs and broader approach, and want to see boards prioritize oversight of company-relevant environmental and social issues and human capital management. [6]

These developments align with a broader, ongoing market shift: the view that the primary purpose of companies is to enhance and protect value for shareholders (shareholder capitalism) is evolving to the view that corporations are better able to deliver long-term value to shareholders when they understand their social impact and address the needs of their communities, customers, employees and other key stakeholders (stakeholder capitalism). [7]

The actions companies are highlighting in these voluntary disclosures—from environmental stewardship to the business’s social impact—reflect how the companies are building long-term, broader value for multiple stakeholders. The disclosures vary widely in terms of depth and specificity and may include:

- Overall sustainability commitment—Nearly 70% highlight their overall commitment to corporate sustainability, responsibility or citizenship, more than double the amount that did so in Some include details regarding how these efforts are governed at the board level, and most link to the company’s sustainability report or website for further information.

- Environmental sustainability—Sixty-two percent highlight their related goals and progress around topics such as emissions reduction, energy efficiency and renewable energy, recycling and waste management, and water, as most applicable to the company’s core

- Community engagement and social impact—More than half discuss their investments in the communities in which they operate (e.g., charitable giving, community partnerships and employee volunteer opportunities) and/or efforts to enhance the broader social impact of the business (e.g., privacy considerations for technology companies, access to medicines and efforts to address the opioid epidemic for health service companies, financing environmental solutions and investing in economically underserved areas for financial institutions).

- Diversity and inclusion and other human capital initiatives—More than half are highlighting their commitment to workforce initiatives around people and Progress related to pay equity and workforce diversity, as well as workforce training and development programs, are key themes of these disclosures.

The most successful disclosures tie the company’s environmental and social commitments to its core values and purpose, business and strategy, and ability to deliver long-term value.

Key board takeaway

Consider the proxy statement as an opportunity for communicating the company’s approach to corporate sustainability and citizenship. Brief, high-level disclosures can carry the message of the company’s commitments and key progress regarding environmental sustainability, people and culture, communities and the social good, and direct stakeholders to other resources for more information.

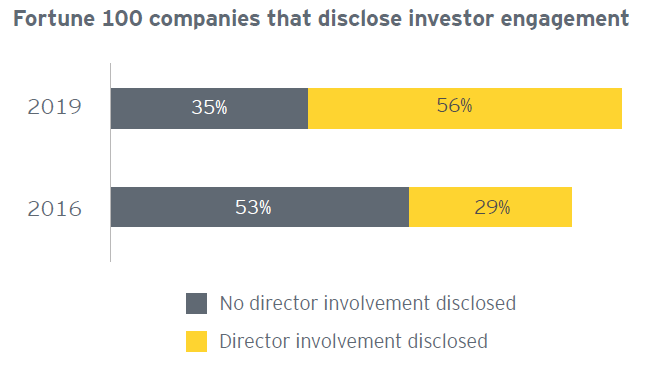

4. Investor engagement involving directors now standard practice for leading companies

Since company-investor engagement began to reshape the governance landscape, engagement on governance topics—and disclosure of these efforts in the proxy statement—continues to grow. Ninety-one percent of Fortune 100 companies have disclosed engaging with investors over the previous year, up from 82% three years ago. And director involvement in these efforts continues to increase. This year, more than half of Fortune 100 companies said board members were involved in select engagement discussions, up from 29% in 2016. These directors most often include lead directors and compensation committee members.

Top five engagement topics disclosed

- Executive compensation

- Strategy and performance

- Sustainability/environmental and social topics

- Corporate governance

- Board composition, diversity and refreshment

Key board takeaway

Companies undertaking engagement should work toward anticipating and meeting investors’ evolving expectations for maximizing the value and productivity of these meetings. They should also consider whether involving directors would be appropriate. Please see our 2019 proxy season preview for tips for more effective engagement based on what we’re hearing from investors.

5. With potential regulatory changes on the horizon, shareholder proposal landscape continues to evolve

The SEC’s current regulatory agenda includes amendments regarding the thresholds for shareholder proposals under Rule 14a-8, indicating that the Commission will consider the matter over the next year. It is generally expected that any changes will increase the current ownership and resubmission thresholds. [8] In the meantime, the shareholder proposal landscape continues to evolve.

Environmental and social shareholder proposals gaining traction

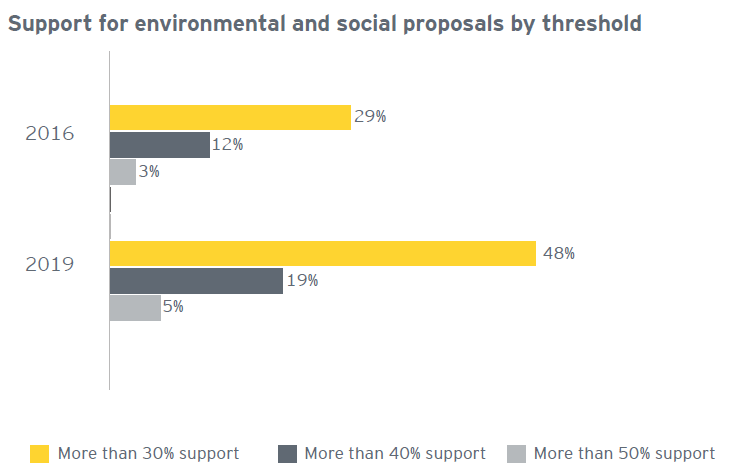

Environmental and social topics represent half of all proposals submitted to date, which is in line with recent years. Support for these proposals continues to climb, averaging 28% so far this year, up slightly from 27% last year and 22% in 2013.

The portion of these proposals reaching key support thresholds also continues to grow. So far, nearly half of the environmental and social shareholder proposals that have gone to a vote have secured at least 30% support, and 19% have attained at least 40% support.

Thirty-percent support is the level at which many boards take note of a proposal topic, and at 50% support, if the board is deemed to take insufficient action in response, many investors will consider voting against incumbent directors at the next annual meeting.

Environmental and social proposal topics securing majority support so far this year include workforce gender and racial diversity, risks related to the opioid crisis, corporate political and lobbying expenditures, and inmate/detainee human rights.

Not reflected by these vote results is the significant number of shareholder proposals on environmental and social topics that are withdrawn each year, usually after the companies and proponents find common ground and reach an agreement. Around 40% of the environmental and social shareholder proposals we are tracking have been withdrawn so far this year, and that includes proposals on environmental topics such as climate risk that have received notable voting support in recent years.

Sector insights: environmental and social shareholder proposal topics

Which sectors faced the most shareholder proposals related to:

- Addressing corporate EEO/diversity—consumer discretionary

- Greenhouse gas emissions—energy, industrials, utilities

- Climate risk—energy

- Pay inequality—financials

Key board takeaway

Engage with shareholder proponents to better understand their concerns and find areas of common ground. Recognize that many investors use the shareholder proposal process as an important part of their stewardship efforts. Also understand that some investors may share the concerns underlying a shareholder proposal even if they do not vote for the proposal as constructed.

Engaging investors and making use of their publicly available policies and reports is key to understanding their views.

Conclusion

As the ES of ESG grows in prominence, topics such as the company’s social impact, purpose, environmental sustainability and diversity (in the boardroom as well as across the workforce) are in the spotlight—and this year’s proxy votes and proxy statements reflect these developments. Along with direct investor engagement, the proxy statement serves as a critical opportunity for communicating the company’s long-term value proposition and highlighting how the company’s governance practices align with and support that proposition

Questions for the board to consider

- What is the board doing to proactively challenge its composition in terms of gender, race and ethnic diversity as well as diversity of skills aligned with the company’s oversight needs? How is it communicating these efforts to shareholders?

- How does the proxy statement showcase the board’s diversity and communicate related goals and commitments to help demonstrate the value the board places on diversity?

- Are there opportunities to highlight the company’s sustainability commitment, and specific goals and progress related to environmental sustainability, people and culture, community investment and efforts to benefit society?

- How is the board overseeing environmental and social risk and value drivers? Are those considerations integrated into long-term strategy—and is the company communicating that effectively to stakeholders?

- How is the company innovating its investor outreach program to maximize the value of those efforts and be responsive to investor feedback?

Endnotes

1Vote results and shareholder proposal data for 2019 are as available for meetings through June. Proxy disclosure data is based on the 77 companies on the 2019 Fortune 100 list that filed proxy statements in 2016 and in 2019 as of 1 July 2019. All other data is full year and based on the Russell 3000 index unless otherwise specified.(go back)

2See California SCR-62 and the New Jersey bill.(go back)

3H.R. 1018—Improving Corporate Governance Through Diversity Act of 2019. H.R. 3279 – Diversity in Corporate Leadership Act of 2019.(go back)

4Illinois Bill HB3394(go back)

5See our How the new class of 2018 independent directors shows that change is on the way for more information on the multiple dimensions of diversity the 2018 new class of independent directors is bringing to the boardroom.(go back)

6See our 2019 proxy season preview for more related information.(go back)

7See our How long-term value is being redefined and communicated for more related information.(go back)

8SEC Agency Rule List—spring 2019, https://www.reginfo.gov/public/do/eAgendaViewRule?pubId=201904&RIN=3235-AM49. SEC To Propose Shareholder Proposal and Proxy Advisory Firm Rule Amendments, Gibson Dunn, 24 May 2019.(go back)