Print

PrintEli Kasargod-Staub is Executive Director of Majority Action and the Climate Majority Project. This post is based on his Majority Action report. Related research from the Program on Corporate Governance includes The Agency Problems of Institutional Investors by Lucian Bebchuk, Alma Cohen, and Scott Hirst (discussed on the Forum here); Index Funds and the Future of Corporate Governance: Theory, Evidence, and Policy by Lucian Bebchuk and Scott Hirst (discussed on the forum here); and Social Responsibility Resolutions by Scott Hirst (discussed on the Forum here).

Key Climate-Related Shareholder Resolutions Would Have Passed with BlackRock and Vanguard Support

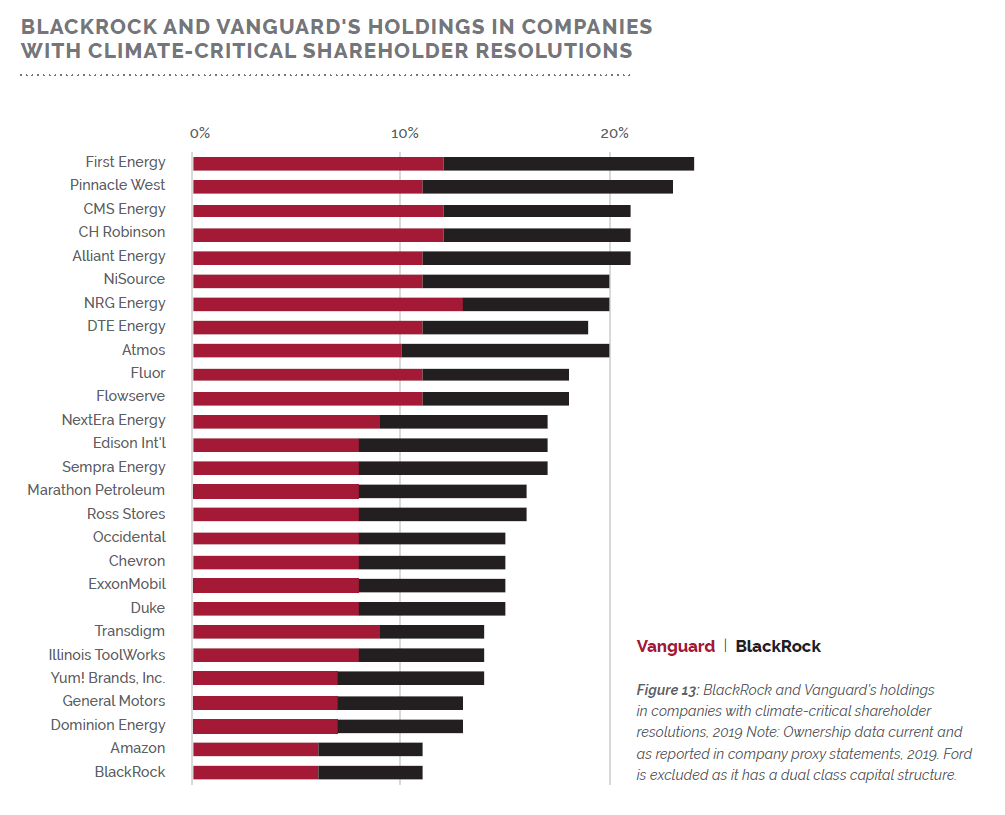

The world’s largest asset managers BlackRock and Vanguard control the largest blocks of shares in nearly every publicly traded firm in the U.S. The pattern of ownership is seen in the energy and utility industries, and across the companies at which there were critical climate votes in 2019 (see Figure 13). The two asset managers were both in the top five common stock shareholders at all 28 companies with critical climate resolutions.

BlackRock and Vanguard were the two largest shareholders at 18 of these 28 companies.

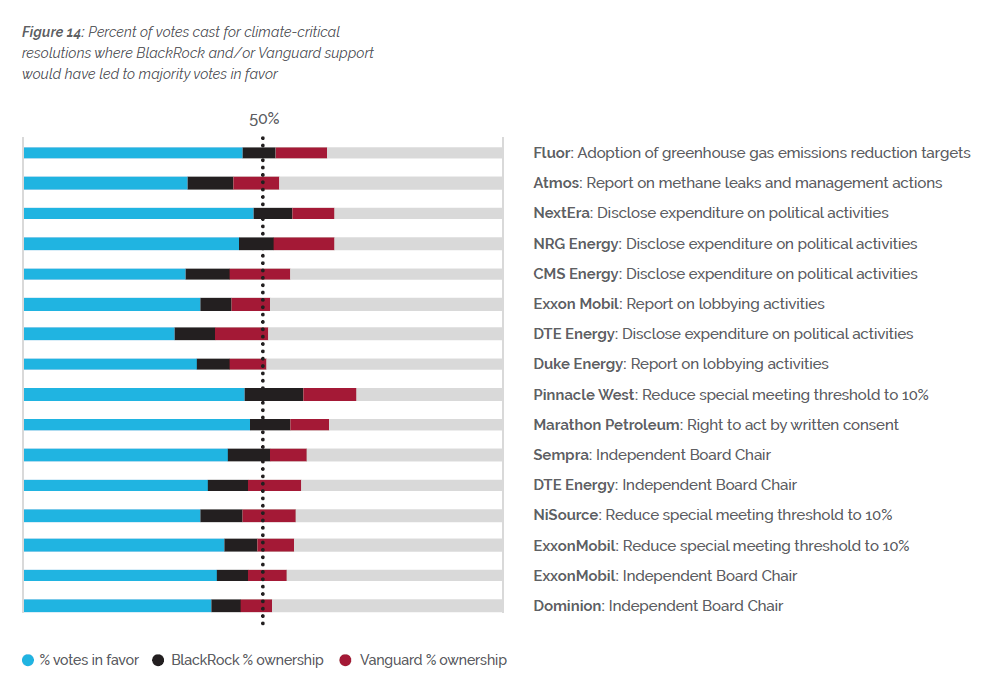

Yet BlackRock and Vanguard were among the asset managers least likely to support these critical climate-related resolutions. BlackRock and Vanguard’s holdings are so significant that at least 16 of these critical climate votes would have received majority support if both of these asset managers had voted in favor of them. In several cases, support from just one manager would have been enough to swing the vote to majority support. Instead, BlackRock and Vanguard voted against them, and they failed to pass. (see Figure 14).

Key Climate Risk Votes

At two of the companies with resolutions relating directly to climate risks and planning, BlackRock and Vanguard’s votes could have swung the proposals to majority vote in favor.

At gas utility Atmos Energy, shareholders requested the company provide a report regarding the company’s actions to reduce its methane emissions. Methane is a potent greenhouse gas, and as the proponents demonstrated, Atmos had not implemented key management practices to mitigate the climate risks associated with it, including failing to commit to Paris Agreement-aligned methane targets and having long or undisclosed timelines for identifying and repairing leaks. The proponents argued that Atmos’ prior reports on this topic were insufficient. This proposal received significant shareholder support, with 34.4% of shareholder votes cast in favor. But both BlackRock and Vanguard voted against, with holdings of 9.5% and 9.6%, respectively, and the measure failed to achieve majority support.

Shareholders at Fluor Corporation, an engineering and construction firm, proposed the company adopt targets to reduce its greenhouse gas emissions and issue a report on its plans to do so. The proposal noted that while Fluor had long disclosed its global carbon footprint, it lacks goals or targets for measuring its progress. A significant number of Fluor shareholders agreed, with 45.9% of votes cast in favor of this proposal. Despite this substantial support by other shareholders, neither BlackRock nor Vanguard supported this resolution.

Given that BlackRock holds a position of 6.9% in the company, and Vanguard 10.6%, votes in favor by either asset manager would have delivered majority support for the proposal.

Key Lobbying and Political Spending Disclosure Votes

Of the 13 resolutions related to lobbying and political activities, six had sufficient shareholder backing that had BlackRock and Vanguard voted in favor, they would have received majority support.

At Duke Energy, investors called on the company to provide additional disclosures regarding its lobbying activities, particularly those related to climate change. Duke Energy is the largest U.S. electric utility by market capitalization, and has the highest level of CO2 emissions of any U.S. electric utility because of its size and its reliance on coal and natural gas. In 2017, the most recent year for which comprehensive data exists, Duke Energy generated more electricity from coal than any other U.S. utility.

While the company’s disclosed lobbying and political expenditures in 2018 totaled less than $5 million, a study by advocates found that the company had spent over $80 million a year to influence policy in its home state of North Carolina. The proponents argued that Duke’s current disclosures are inadequate and do not allow shareholders to assess whether its lobbying expenditures are aligned with the company’s stated commitment to a lower-carbon future.

For example, Duke was one of the largest funders of efforts by the Utility Air Regulatory Group (UARG) to lobby against regulations addressing climate change. UARG is now under investigation by the U.S. House Energy and Commerce Committee for improper connections to EPA leadership. Following the opening of the investigation and public reporting on the matter, Duke ceased its membership in the organization in recent months. Similarly, Duke does not disclose its membership in the American Legislative Exchange Council (ALEC), the controversial group whose model legislation regularly works against climate regulation and energy transition.”

The lobbying disclosure proposal at Duke received support of 36.2% support—but both BlackRock and Vanguard, with 6.8% and 7.9% of shares, respectively, voted against the measure. If they had supported the proposal, it would have received majority support.

Shareholders at NextEra Energy submitted a proposal calling for the company to report on its political expenditures and related policies. NextEra brands itself as a leading clean energy company and the world’s largest producer of wind and solar energy. However, in recent years, its subsidiary Florida Power and Light, along with other Florida energy companies, spent millions in support of a misleading constitutional amendment that would have the effect of limiting rooftop solar expansion. A near-majority of voting shareholders supported the proposal, with 48.2% voting in support. This is an increase from 2018, when a similar proposal received 42.4% support. Both BlackRock and Vanguard voted against this proposal, as they did in 2018. BlackRock holds 7.9% of NextEra’s shares, and Vanguard 8.9%. Had either one of them voted for this proposal, it would have received majority support.

Resolutions calling for further disclosure of policies regarding use of corporate funds to influence election outcomes, as well as specific expenditures, came to a vote at CMS Energy and DTE Energy. CMS and DTE are two Michigan-based electric utilities and the top donors to the “Clean Affordable Renewable Energy for Michigan Coalition” created to oppose a 2012 ballot measure that would have required utilities to obtain at least 25 percent of their electricity from renewable energy sources by 2025. Given the misalignment between this spending on political activities and the long-term shareholder interest in rapid decarbonization at these firms, further disclosure in this area would be useful to shareholders. These resolutions received support of 34.1% and 31.7% respectively. BlackRock and Vanguard hold a combined position of 21.5% at CMS and 19.6% at DTE; and had they chosen to support these resolutions, each would have received majority support.

Similarly, at NRG Energy, shareholders proposed greater disclosure of political expenditures. As noted by the New York City Comptroller in proposing this resolution, NRG only provides disclosures of political expenditures where required, leaving out a range of significant political activity, including trade association involvement. While NRG currently has set a long-term emissions reduction target of reducing its emissions by 90% by 2050, former CEO David Crane was forced out at the urging of hedge fund Elliott Management, and the subsequent restructuring plan involved significant sell-offs of renewable energy assets. These actions call into question NRG’s commitment to its emissions targets, and given the level of uncertainty about NRG’s strategy in this regard, greater transparency about the company’s political activities, particularly with respect to climate change, is warranted. This resolution received significant support, with 45.2% of votes cast in favor—but again, neither BlackRock nor Vanguard voted for the resolution. With holdings of 7.1% and 12.5% respectively, the support of either asset manager would have given the resolution majority support.

Twenty-one institutional investors filed a proposal at ExxonMobil asking the company for greater disclosure regarding payments for lobbying. The proponents cited their concern that the company’s undisclosed lobbying is misaligned with its publicly stated positions on climate, among other risks to shareholder value They noted that while ExxonMobil claims that the company supports the Paris Climate Agreement, analysis by InfluenceMap found that ExxonMobil was among the three global corporations spending the most to oppose the goals of the Paris Agreement. ExxonMobil was also listed in a report by the Center for Public Integrity on the hypocrisy of companies that claimed to support the Paris Agreement but funded efforts to block its policies. As recently as the 2018 U.S. midterm elections, ExxonMobil led an effort that spent $2 million in ads on Facebook and Instagram opposing pro-climate ballot initiatives.

The proponents argued that ExxonMobil is out of step with its peers in ensuring that its public positions match its private lobbying and trade association activity, with Royal Dutch Shell committed to ensuring that its industry association memberships do not undermine its support for the Paris Agreement goals. This resolution received support of 36.9% from shareholders. If BlackRock and Vanguard had voted in favor, with holdings of 6.7% and 8.0% respectively, this resolution would have achieved majority support.

Key Governance Votes

Sixteen proposals relating to improving governance, independent oversight and shareholder rights were put to a vote at major companies in the energy, utility, and automotive sectors. Of these, eight would have received majority support if BlackRock and Vanguard had voted for them. Vanguard has indicated that in general it supports independent board leadership and may vote to separate the Chair and CEO roles in cases where independent oversight or shareholder responsiveness is lacking. BlackRock has stated that in the absence of significant governance concerns, it defers to boards to determine whether to separate the roles.

BlackRock and Vanguard’s consistent opposition to the proposals outlined below implies that they believe there are no significant governance issues at the companies or that independent oversight and shareholder responsiveness is sufficient—despite these proposals offering strong evidence to the contrary.

At the same time they were calling for shareholders to vote against the ExxonMobil board, some shareholders also spearheaded a resolution to require an independent chair of the board. In support of that resolution, the proponents asserted that ExxonMobil’s inadequate response to climate change was in part driven by lack of independent board oversight and that an independent chair would improve communication with investors and provide crucial checks and balances on the company’s decision-making with regard to climate change. Shareholders also proposed reducing the ownership threshold for calling a special meeting at ExxonMobil down to 10%.

The independent chair resolution received substantial support from shareholders, with 40.4% voting in favor. The special meeting resolution obtained similar support, with 42.0% of votes cast in favor. Together, BlackRock and Vanguard would have had the ability to ensure these proposals received majority support—BlackRock holding 6.7% of the company, and Vanguard 8.0%—but they voted against both of them.

At Dominion Energy, shareholders proposed an independent chair policy to provide additional oversight. As a major electric utility, Dominion’s long-term success depends on its ability to undertake the rapid transformation necessary to meet the challenges and risks posed by climate change. Dominion’s current decarbonization targets fall short of what is required, largely because it continues to invest heavily in gas generation assets, many of which risk early closure and costly writedowns. In pursuing these investments in gas, the company has also generated significant public backlash, in particular to decisions related to its Atlantic Coast Pipeline (ACP).

The delays and legal challenges faced by the project mean that it now faces substantially different economic conditions than when it was approved, calling into question whether it will ever be completed, and if so, whether regulators will agree to allow the utility to recoup the costs of the investment from consumers. At the same time, Dominion’s lead independent director has longstanding ties to the pipeline project, raising questions as to whether he can act as an effective representative of shareholders as lead independent director. The resolution received substantial shareholder support, with 39.4% voting in favor. Combined, BlackRock and Vanguard hold 12.4% of Dominion’s stock, and had they supported the resolution, it would have achieved majority support.

At DTE Energy, shareholders also filed a resolution calling for the creation of an independent chair, citing climate change-related and other environmental challenges, including concerns regarding its new gas pipelines. As with Dominion, DTE’s long-term success depends on its ability to undertake the rapid transformation of its business to meet the challenges and risks posed by climate change, including full decarbonization of its electricity generation by 2050. Its current decarbonization commitments fall short of this goal. In response to new laws and regulatory and consumer pressure in Michigan, DTE submitted long-range capital plans that would phase out coal, but retain plans to build new gas infrastructure. DTE’s continued long-term commitment to gas infrastructure, in the face of pressure from lawmakers, regulators, and consumers, significantly increases the risks that such assets will be stranded through early closure.

Given these risks and challenges, the proponent argued that greater independent oversight in the form of an independent chair was warranted. This resolution received 38.5% support overall. Both BlackRock and Vanguard voted against the proposal, and their stakes of 8.4% and 11.2% respectively could have jointly swung the vote to majority support.

A proposal at Pinnacle West Capital called for a reduction in the ownership level required to call a special meeting to 10%. Pinnacle West and its main subsidiary, the utility Arizona Public Service, have been mired in scandal in recent years for improper connections to the state regulator, federal investigations related to financing of elections, and allegations of millions spent in ‘dark money’ for elections to the state regulator.98 In addition, Pinnacle West and APS spent $11 million in a failed attempt to keep a referendum to increase Arizona’s renewable energy mandate from appearing on the ballot.99 The company then spent an additional $30 million to defeat the initiative at the polls. Given this severe misallocation of company resources in opposition to pro-climate initiatives, shareholders demanded greater rights to intervene at the company. This resolution received high levels of support, with 46.1% of votes cast in favor—but again, neither BlackRock nor Vanguard voted for the resolution. With holdings of 12.3% and 11.2% respectively, the support of either asset manager would have put support at greater than 50%.

At Sempra Energy, an electric and gas utility serving Southern California, investors proposed the creation of an independent board chair. The proponent of this resolution cited a number of challenges facing the company that require additional independent oversight, including costs reaching $1 billion related to the explosion at a gas well owned by the company, and many hundreds of millions of dollars in writedowns and impairments in gas and other assets. Holders of 42.6% of shares supported this proposal. BlackRock and Vanguard, which voted against the resolution, held 8.8% and 7.7% respectively. As such, either asset manager could have delivered majority support for this proposal.

At the oil and gas company Marathon Petroleum, a proposal sought to give shareholders the right to act by written consent. The proponents cited a number of troubling climate-related issues at the company, including numerous lawsuits related to the company’s contribution to climate change, proposed class action suits resulting from pollution and health impacts, and substantial penalties related to Clean Air Act violations in recent years. While Marathon has acknowledged that it explicitly recognizes climate change as a relevant risk and opportunity for the company, it has yet to set any targets in relation to its carbon emissions, and according to the Transition Pathway Initiative, has not integrated climate change planning into its operational decision making. This resolution was very close to achieving majority support without BlackRock and Vanguard, with 47.5% of votes cast in favor. Given that BlackRock and Vanguard each held 8.1% of the company, either one would have been sufficient to reach majority support for this proposal.

Finally, at the electric and gas utility NiSource, shareholders proposed reducing the ownership level required to call a special meeting to 10%. NiSource is facing significant costs and risks related to safety failures at its gas infrastructure assets, having recently settled a series of class action lawsuits for $143 million. The settlement is only a small part of the $1 billion the company must dedicate to customers and communities affected by a series of gas explosions in Massachusetts last year. Moreover, NiSource has come under criticism for its ties to ALEC, which as noted above has proposed model legislation that works against climate regulation and the energy transition. The proponents also cited concerns regarding the long tenure of several current board members in support of the case for greater shareholder rights at the company. Shareholders voted 37.0% in favor of this proposal. BlackRock and Vanguard combined hold 19.9% of the company, and could together have delivered majority support for the proposal.

What Is Driving the Largest Asset Managers To Vote with Management?

A number of forces influence the largest asset managers to vote with company management and not support accountability on climate change. These factors include a lack of accountability to individual investors on whose behalf asset managers invest and conflicts of interest stemming from the fact that asset managers seek business, such as advising 401(k) plans, from the very companies in which they invest. At the same time, major asset managers such as BlackRock and Vanguard claim to undertake extensive engagement with companies, instead of taking strong stances via proxy voting. However, this engagement is opaque and lacks demonstrable results in changing company behavior.

Structural Conflicts of Interest

BlackRock, Vanguard, and other fund managers do not make their investment stewardship decisions in a vacuum; indeed, asset managers may be voting in line with their own short-term institutional interest instead of the long-term interests of the beneficiaries of the funds they manage. As corporate governance experts have long noted, BlackRock, Vanguard and other fund managers face powerful and structural conflicts of interest that arise from both providing services to corporate issuers and casting proxy votes at those same corporations.

Academic research has shown that the “volume of business that investment managers receive from corporate pension funds is associated with their voting more frequently in support of corporate managers on shareholder proposals, as well as on executive compensation matters.” Beyond these specific conflicts, experts with the Harvard Law School’s Program on Corporate Governance believe that the general practice of earning revenue from companies while voting at those very same companies likely leads index fund managers to “set [their] general principles, policies, and practices so as to enhance the likelihood of supporting management in votes across all portfolio companies.”

BlackRock faces its own climate-specific conflicts, which may be hindering the company’s ability or willingness to assume the mantle of climate leadership that is so urgently needed. As reported by the Institute for Energy Economics and Financial Analysis, six out of BlackRock’s 18 board members have backgrounds in the fossil fuel sector, including BlackRock’s lead independent director. BlackRock has not even separated the positions of Chair and Chief Executive Officer, ignoring a widely recognized best practice of corporate governance and further concentrating power in the hands of CEO Larry Fink.

Greenwashing “Engagement”

BlackRock claims it fulfills its investment stewardship responsibilities through the shareholder engagement it conducts bilaterally with its portfolio companies. While BlackRock has long promoted this bilateral activity as a superior alternative to supporting shareholder resolutions, there is no evidence that their engagements have actually led to widespread positive behavioral change among companies on climate change. As noted above, many major energy companies have yet to make the commitments and plans necessary to meet the challenges posed by climate change. Moreover, these private engagements are notorious for their lack of transparency, leaving BlackRock’s clients and the broader investor community with no means of assessing their efficacy. BlackRock’s disclosures contain no information about what bright lines it draws with companies on climate change or other issues, and does not indicate how company responses to engagements would lead BlackRock to support or reject company nominees for a corporation’s board. Unfortunately, all that is clear is that BlackRock systematically fails to back up its “engagement” efforts with action.

In their 2019 reports, both BlackRock and Vanguard highlight the importance of disclosure in relation to climate risks. However, neither BlackRock nor Vanguard emphasize ensuring that those risks are not only disclosed, but managed and mitigated through strategy and planning that aligns to global decarbonization targets and protects long-term shareholder value. In its 2019 engagement report, Vanguard goes so far as to disavow direct intervention at companies in relation to the material risks caused by climate change. Vanguard asserts that instead of engaging directly on specific climate strategy and outcomes, it seeks to promote “robust board oversight and meaningful company disclosure.” This approach is belied by Vanguard’s voting record in 2019, when it voted against governance reforms at the full range of oil and gas and utility companies surveyed in this report.

The 2019 engagement reports from both asset managers provide little in the way of additional guidance to asset owners and other shareholders regarding their voting decisions on particular issues, beyond anonymized anecdotes at certain companies. For example, Vanguard describes its engagement with a company that appears to be now bankrupt, PG&E, saying, “after incidents involving a U.S. utilities company resulted in deaths and considerable property and environmental damage, we held numerous engagements with the company to understand its board’s role in overseeing the remediation of the crisis.” However, this leaves open the question of what role Vanguard’s engagement or more forward-looking accountability efforts could play in advancing responsible climate action to mitigate the risk of further crises like this.

For its part, BlackRock seeks to minimize the perception of its influence at major companies in the U.S. by pointing to its average ownership in the global equities market, while failing to acknowledge the significant stakes the asset manager holds in the largest U.S. companies and the fact that it is often one of the largest shareholders at companies where ownership is highly dispersed. Similarly, BlackRock claims it does not have the power to ‘swing’ votes at companies where it has substantial holdings, pointing to the fact that the vast majority of votes are uncontroversial and not subject to close votes. This may be true, given the very high votes cast in favor of directors in uncontested elections, which make up the lion’s share of ballot items, but it does not negate the fact that the asset manager is choosing to vote against shareholder efforts on key issues and at key companies that would help promote long-term shareholder value in the face of climate change.

The complete publication, including footnotes, data sources, and methodology, is available here.