Print

PrintPeter Reilly is Senior Director, Corporate Governance at FTI Consulting; and, Aniel Mahabier is CEO of CGLytics. This post is based on a joint FTI Consulting and CGLytics paper authored by Mr. Reilly based on data from CGLytics. Related research from the Program on Corporate Governance includes Paying for Long-Term Performance by Lucian Bebchuk and Jesse Fried (discussed on the Forum here) and Socially Responsible Firms by Alan Ferrell, Hao Liang, and Luc Renneboog (discussed on the Forum here).

In recent years, the level of capital flowing into funds that incorporate ESG criteria has grown considerably and what was once an issue on the fringes of investment is increasingly part of the material financial analysis of a company’s value.

Consequently, ESG rating agencies (who help investors identify ESG risk) have grown in prominence; regulators have commenced a clampdown on so-called “greenwashing”; and, investors continue to pressurise companies to provide greater details on ESG factors likely to affect their business—either through engagement or, less frequently, shareholder proposals. Indeed, a recent report found that, at least based on publicly disclosed documents, climate change was the number one issue for institutional investors in their stewardship of investee companies.

In this post, we have analysed whether the ratcheting up of pressure on companies to enhance their ESG frameworks has permeated another important area—executive remuneration at UK and Irish companies. For three decades, pay has been identified as a key driver of C-suite behaviour. Despite what appears to be a relentless focus on ESG, the incorporation of ESG measures into executive pay packages has lagged somewhat.

While there has been a rise in the prevalence of such measures, they remain on the periphery. Only 27.4% of FTSE 350 and ISEQ 20 companies have included some form of measurable ESG criteria in incentive plans. Even at those companies, however, the proportion of pay being driven by ESG performance is small.

This is despite companies across Europe being required to include non-financial statements in their Annual Reports; and, every FTSE 350 company being expected to set out non-financial Key Performance Indicators (KPIs) in their Annual Reports. If a group of KPIs are not being replicated in incentive plans, there may be a danger that remuneration frameworks are becoming disconnected from corporate strategy. Or do Boards and investors see ESG measures as effective risk management tools as opposed to opportunities to drive value?

Market View—Investors on ESG

In both their marketing materials and their proxy voting guidelines, the world’s largest asset managers detail the importance of ESG to their investment strategies and approach to issuer engagement.

In that sense, for major institutional investors, the focus on ESG is doubly important. As asset owners demand more answers regarding the role ESG plays in investment decisions, it becomes increasingly central to attracting inflows and gaining market share while simultaneously reducing risk, or even driving superior investment returns. This trend is likely to continue as the EU implements more stringent measures requiring institutional investors to report on the impact of their investments to ultimate asset owners. In their public guidelines on investment and proxy voting, State Street and Legal & General refer to the importance of ESG; while BlackRock goes a step further and addresses the idea of incorporating ESG measures into incentive plans—albeit with a cautionary tone.

State Street: We engage with companies to provide insight on the principles and practices that drive our voting decisions. We also conduct proactive engagement to address significant shareholder concerns and environmental, social, and governance (“ESG”) issues in a manner consistent with maximizing shareholder value.

Legal & General: Assessing companies on their management of Environmental Social & Governance (ESG) issues is an important element of risk management, and therefore part of investors’ fiduciary duty. By incorporating ESG factors into investment decisions, we believe investors can gain an element of protection against future risks and the potential for better long-term financial outcomes. This is why we embed both top-down and bottom-up ESG analysis into our investment processes.

BlackRock: The performance measures should be majority financial and at least 60% should be based on quantitative criteria. Variable pay should be based on multiple criteria. We expect full disclosure of the performance measures selected and the rationale for the selection of such performance measures. If the board decides to use ESG-type criteria, these criteria should be linked to material issues and they must be quantifiable, transparent and auditable. These criteria should reflect the strategic priorities of the company. For that reason, the inclusion in ESG-indexes is generally not considered to be appropriate criteria. Where financial measures constitute less than 60% of performance measures a cogent explanation should be provided.

While the level of discourse and company reporting on ESG has grown recently, incorporating ESG or sustainability measures into incentive plans is not a new idea. In 2012, a Task Force for the UN PRI, comprised of some of the world’s leading investors, published a paper entitled Integrating ESG Issues into Executive Pay. That paper aimed to provide guidance for investors and companies on how best to incorporate ESG measures into short and long-term executive remuneration.

With institutional investors and other key market players demanding greater attention is paid to ESG factors, it appears that Boards have not yet fully reacted by implementing changes to the frameworks designed to drive executive behaviour—incentive schemes. As regulatory pressure grows on investors to demonstrate the ESG credentials of their investments, we anticipate greater pressure from investors on companies to align management incentives with ESG related metrics.

ESG Measures & Case Studies

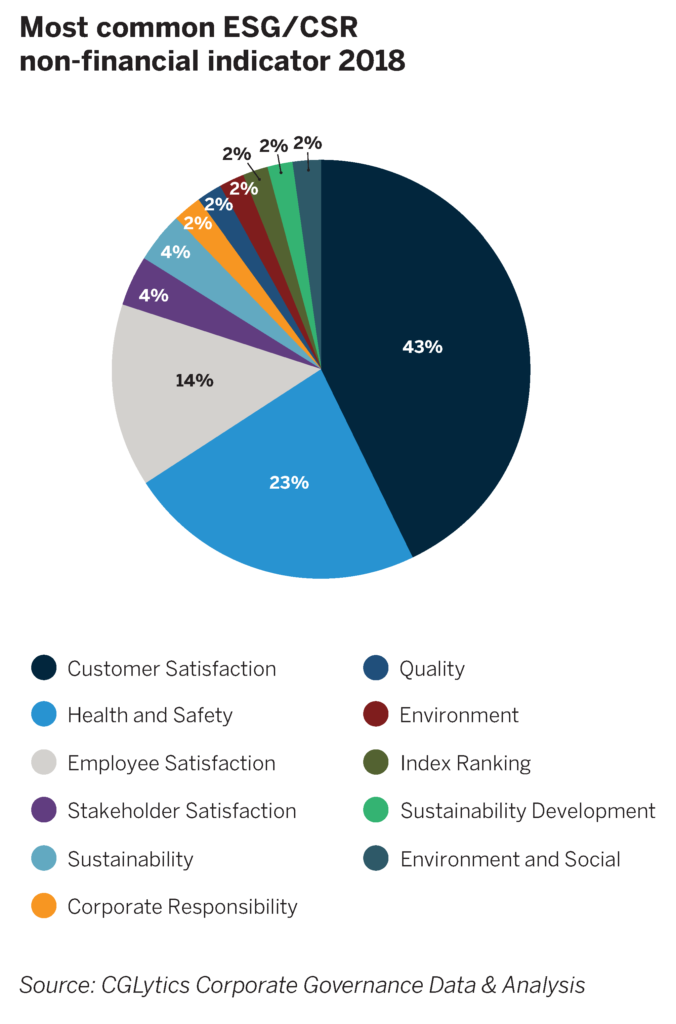

Most Common ESG-related Measures

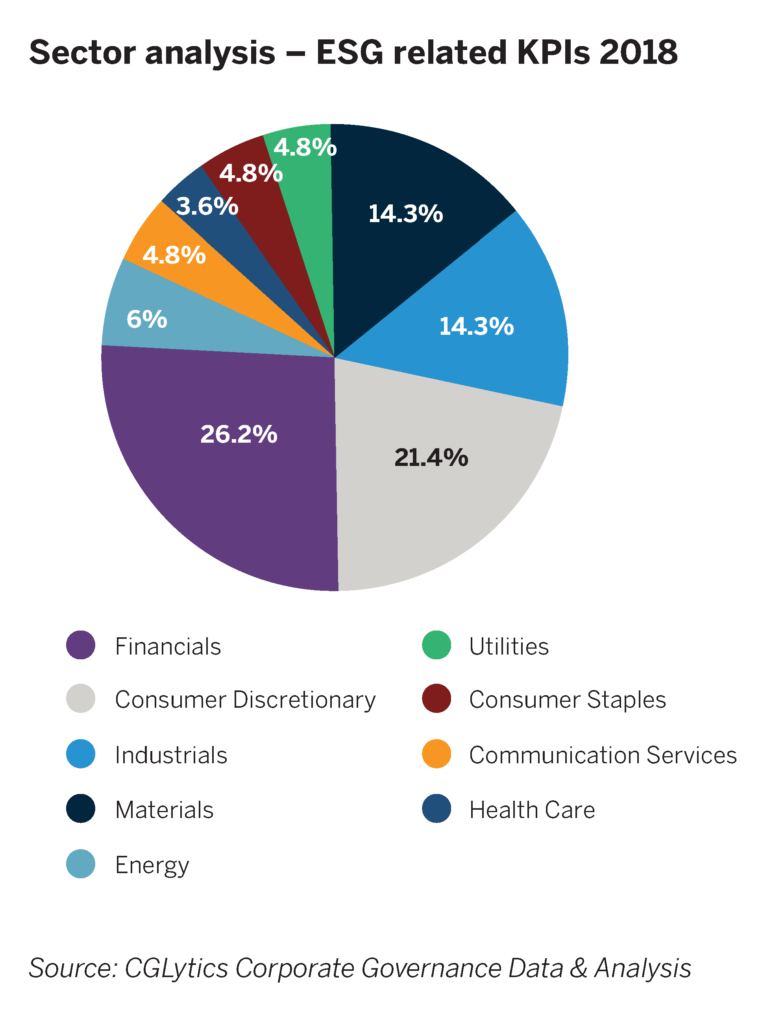

Despite the focus of regulators and investors, the integration of ESG measures into incentive plans has been progressing slowly—perhaps unsurprisingly given how rapidly the issue has come to the fore. From a review of FTSE 350 and ISEQ 20 companies from 2018 reporting, only 12.8% of UK and Irish companies have included ‘strict’ ESG measures in their incentive frameworks. This figure increases to 27.4% when customer satisfaction is included. While there is likely to be debate as to the ESG ‘credentials’ of customer satisfaction, any metric that measures management performance on engaging with a stakeholder group merits—in our view—inclusion:

While almost three-quarters of companies do not yet include ESG-related measures, there has been a marked increase in their use over the past decade:

- In 2008, 3% of companies included ESG related KPIs in bonus plans; and,

- In 2013, 19% of companies included ESG related KPIs in bonus plans.

Nonetheless, ESG measures continue to account for a tiny proportion of potential remuneration for the UK and Ireland’s listed companies; and, even at the 27.4% of companies incorporating them, they are often a very small portion of bonuses. On average, at the 27.4% of companies, ESG-related measures account for less than 15% of bonuses.

Despite the consistent focus on climate change, certain stakeholders will likely be disappointed to see the slow pace at which environmental targets are Integrated into incentive plans by companies. Of all potential ESG measures, reducing the impact on the environment seems to be one of the easier to include in incentive plans, as there are a number of metrics employed in measuring emissions, single use plastics and water usage, among others. Notably, such measures are far more frequently referred to as non-financial KPIs.

Having come under pressure from a coalition of investors, commitments from Shell and BP to incorporate climate-related measures into their incentive schemes over the coming year will further increase the number of companies adopting environmental performance targets into incentive plans. It is likely that this trend will gather pace, and not just in material intensive industries. Over the past year, there has been increasing pressure on financial institutions to detail their approach to lending and green finance, while companies in the agricultural and transport sectors are also under heightened scrutiny–in line with wider societal pressures. As businesses come under increased pressure to detail—and then reduce—their impact on the planet, there will be few sectors that escape investor spotlight.

While the “E” in ESG is key in certain sectors, in others, the “S” is to the fore. Whether it be in employee heavy industries; those where Health & Safety is paramount; or, where the workforce is the company’s most important intellectual property, an engaged workforce has consistently been shown to improve productivity and risk management.

Engaged employees are those fully invested in their firm and their work. They are the ones who actively think about the firm’s processes—and identify improvements. Their enthusiasm reflects a corporate culture that encourages engagement. Most importantly, they are productive. Conversely, disengaged workers impact productivity and value creation, but are also a risk which can permeate throughout the organisation. Consequently, it is not surprising to see employee engagement and satisfaction used in a relatively high number of incentive plans, as well as being one of the most prominent non-financial KPIs. It is likely that this measure will become more prevalent in incentive plans for a number of reasons: since 1 January 2019, UK & Irish companies have been required to increase their focus on employee engagement under the new UK Corporate Governance Code; in the search for quantitative ESG-related measures, there are a number of established workforce metrics; and, there appears to be a growing recognition from Boards and management of the importance of favourable employee policies.

Supplementing those metrics with qualitative assessments would aid investors’ understanding of the importance of employee engagement to Boards. In this space, the Pensions and Lifetime Savings Association (PLSA), the UK trade body, and ShareAction, the responsible investment campaign group, have developed two separate tools (Understanding the Worth of the Workforce and the Workforce Disclosure Initiative, or WDI) to assist with this type of analysis. Ease of measurement may have presented challenges for companies and investors, causing the E- and G-factors to gain more traction than the S-factor initially, which had often been confined to employment rights. The S does not stop at employees, however, and extends to how companies interact with wider society. Social and human capital issues are on the rise, as diversity, data privacy, and the treatment of labour in supply chains are looked at with a closer lens. Meanwhile, pharmaceutical companies are facing pressure from a number of stakeholders, as drug pricing and wider impacts on society become hot button issues.

The complete publication, including footnotes, is available here.