Print

PrintJeff Lubitz is Head of ISS Securities Class Action Services, Institutional Shareholder Services, Inc. This post is based on an ISS publication by Elisa Mendoza, Vice President with ISS Securities Class Action Services.

Well versed in claims filing for over fifteen years, ISS Securities Class Action Services (ISS SCAS), along with other third-party filers, has experienced new challenges due to a seemingly new requirement on the part of law firms and claim administrators for precise beneficial owner information. Previously, claim administrators accepted the account name and account number to begin processing claims without requiring the beneficial owner information specifically. Now, submitted claims will not even be processed by many claim administrators without precise, unabbreviated identification of the beneficial owner for each claim. Claims administrators have made clear they will no longer accept the account name as sufficient. This post explores the impact the increased scrutiny of the beneficial owner name has had on the claims filing process, how the increased scrutiny came about, and the challenges and benefits of requiring this information.

Purpose of Beneficial Owner Information

Since 1978, the SEC, under C.F.R. Title 17, Section 240.13d-3, has required that “all securities of the same class beneficially owned by a person, regardless of the form which such beneficial ownership takes, shall be aggregated in calculating the number of shares beneficially owned by such person.” [1] The policy behind this rule was to provide transparency on significant ownership of a company and to give insight into investment discretion of large shareholders and their voting authority. Ultimately, the rule helps safeguard the interests of issuers and of the public through a fair and orderly securities process. Although the Code of Federal Regulations has mandated this since 1978, there has been very little oversight of this requirement in the claims filing arena until recently.

Purpose of Requiring Beneficial Owner Information from the Law Firms’ Perspective

In the last two years, oversight for the beneficial ownership information requirement has increased dramatically. The claim submission process has developed to focus more on the beneficial owner information for each claim and how this information is presented. To gain some insight into this dramatic increase, ISS SCAS spoke to law firms and claims administrators that are now requiring this information as a standard part of the claims filing process. Darren Robbins, Esq. of Robbins Geller Rudman and Dowd, gives some insight into why this requirement is now being enforced more strictly. He explains, “in the two decades since the Private Securities Litigation Reform Act was enacted, various aspects of the securities class action practice have become much more refined, including the formulation of plans of allocation. What constitutes best practices with respect to claims filing has changed significantly over the years. While one could characterize certain claims filers as attempting to optimize claims, others might call it gaming the system.” Thus, it became necessary to rigorously review claims filing practices and put into place mechanisms that avoid improper “claim optimization,” according to Mr. Robbins, and in this way ensure that submitted claims actually yield payment to the beneficial owners harmed by the underlying securities fraud.

From the Claims Administrators’ Perspective

In ISS SCAS’ discussions with multiple claims administrators, they—like many law firms—cite prevention of fraudulent or duplicate payments, and improved efficiency in the administration process as factors supporting the need for increased scrutiny of the beneficial owner of a class action claim. They advise that plaintiff law firms have required this information to prevent fraudulent behavior like the practices alluded to by Mr. Robbins. They describe several scenarios, in which the beneficial owner’s identity is necessary to prevent overpayment, duplicate payments, and inaccurate claims. Under one scenario, claimants combine claims across an entire organization, but the claims do not ultimately belong to the same beneficial owner. This practice has resulted in claims being paid out under fraudulent circumstances, because the loss was shared by several beneficial owners who had no legitimate justification for combining their separate claims into one claim.

The opposite occurs too, whereby claims belonging to the same beneficial owner that should be combined are not. Some claimants file these claims separately. When the claims are filed separately, some are calculated to a huge loss and thus, become large payouts for claims that, were they properly combined, might have ultimately calculated to no loss or even a gain. Plaintiff law firms began noticing this issue and started requiring that claims administrators gather the beneficial owner information for each claim. Several plaintiff law firms also require the combination of claims at the beneficial owner level.

The third scenario is where duplicate claims are filed. If the same claim is filed by two different entities, then the claim potentially gets paid out twice to the same underlying beneficial owner. If the same claim is paid twice, albeit submitted by different filers, this reduces the remainder of the settlement left to pay to other qualifying claimants. Being able to quickly identify duplicate claims improves efficiency and prevents an unfair windfall for certain claimants. An increasing number of plaintiff firms are requiring this information, thus incentivizing claims administrators to make this a prerequisite to processing the claims.

Beneficial Owner Definition

Because the emphasis on identifying the beneficial owner is a more recent development, many claimants have asked the question—how can one determine who the beneficial owner is when there are a variety of account structures? One place for guidance on the definition of “beneficial owner” is the SEC’s rules for determining beneficial ownership. Title 17 C.F.R. § 240.13d-3 states:

“A beneficial owner of a security includes any person who, directly or indirectly, through any contract, arrangement, understanding, relationship, or otherwise has or shares

- Voting power which includes the power to vote, or to direct the voting of such security; and/or

- Investment of power which includes the power to dispose, or to direct the disposition of, such security.” [2]

The rules for providing beneficial owner information are very precise, and they extend to almost every type of fund, including trusts. For additional guidance on identifying the beneficial owner, ISS SCAS discussed the terminology with Grant Lambert, a Senior Business Analyst from Epiq Global, an active claims administrator. Mr. Lambert supplied the following explanations of what would be expected for each of several different legal structures:

Mutual fund—Each distinct fund is its own beneficial owner.

Hedge fund—Each distinct fund is its own beneficial owner, but the identity of beneficial owners may also depend on the structure of the hedge fund.

Corporation—A retirement plan is a distinct beneficial owner, separate from the corporation.

Trust—Trusts are distinct legal entities and need to be named, as opposed to naming the trustee. The trustee is not the beneficial owner.

While the above categories do not cover each type of organization of accounts, they serve as a good starting point to identify the beneficial owner for the majority of non-retail claims.

Impact of Beneficial Owner Requirement—Downstream Effects

While identifying the beneficial owner presents challenges, there are additional downstream effects implicit in the requirements of identifying and combining claims at the beneficial owner level. For example, an account name may be different from the beneficial owner’s name, and therefore this information must be collected and stored separately.

Moreover, claim administrators require that all claims with the same beneficial owner are combined into one single claim. This approach may seem logical and straightforward; however, it creates ripple effects when the claim is processed and paid. When a claim is eligible, the claim administrator makes only one payment per claim.

The challenge becomes on how to split the one payment across multiple accounts that were combined into the one claim. In which account should recoveries be deposited? Does one do a pro-rata division of the losses? Although combining the accounts for filing is simple, some claimants face challenges when distributions for the claims occur, because they have trouble determining how to apportion the money. There are currently no hard and fast solutions to this dilemma and claim administrators have demonstrated that they are not planning on making any exceptions to their beneficial owner requirements or how they distribute the funds per claim.

Conclusion

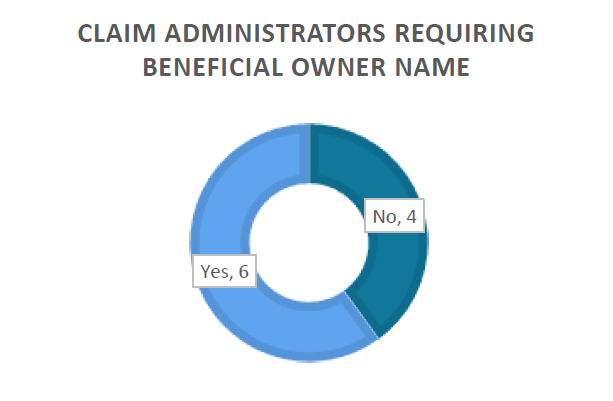

As a main player in the third-party filings arena, ISS SCAS has worked with many, if not all, claims administrators over the years. At present, six of the ten primary claim administrators with whom ISS SCAS works and submits claims require beneficial owner information to process a claim. These claim administrators will reject the entire claim if the beneficial owner information is not provided in a correct, complete, and unabbreviated form. Furthermore, if the claims administrators see that there is more than one claim with the same beneficial owner, they will require these claims be combined and aggregated, regardless of the structure of underlying accounts that were combined to create the ultimate claim. This is regardless of whether the accounts are sleeves of the same fund or whether the underlying accounts are housed at different custodians. Some claimants have felt frustrated at the downstream impact of these requirements. In an effort to assist ISS SCAS’ clients and be responsive to the challenges described, ISS SCAS continues to develop and facilitate a streamlined process for fulfilling this requirement. To provide transparency and to prevent fraudulent actors from misusing the claims filing process, third party claims filers and their underlying claimants must comply with the beneficial owner filing requirements. Although this is a more difficult process, these efforts are worthwhile to minimize fraud, prevent overpayment, and maximize recoveries for those that file legitimately. ISS SCAS is committed to gathering the relevant details to ensure clients’ claims are properly processed, and their recoveries are maximized in a fair, accurate, and legitimate claims-filing process.

Endnotes

117 C.F.R. § 240.13d-3 (1978)(as revised in 1998).(go back)

217 C.F.R. § 240.13d-3 (1978)(as revised in 1998).(go back)