Print

PrintCathy A. Birkeland, Mark D. Gerstein, and Laurence J. Stein are partners at Latham & Watkins LLP. This post is based on a Latham & Watkins memorandum by Ms. Birkeland, Mr. Gerstein, Mr. Stein, Ryan J. Maierson, Pardis Zomorodi, and Alexa M. Berlin.

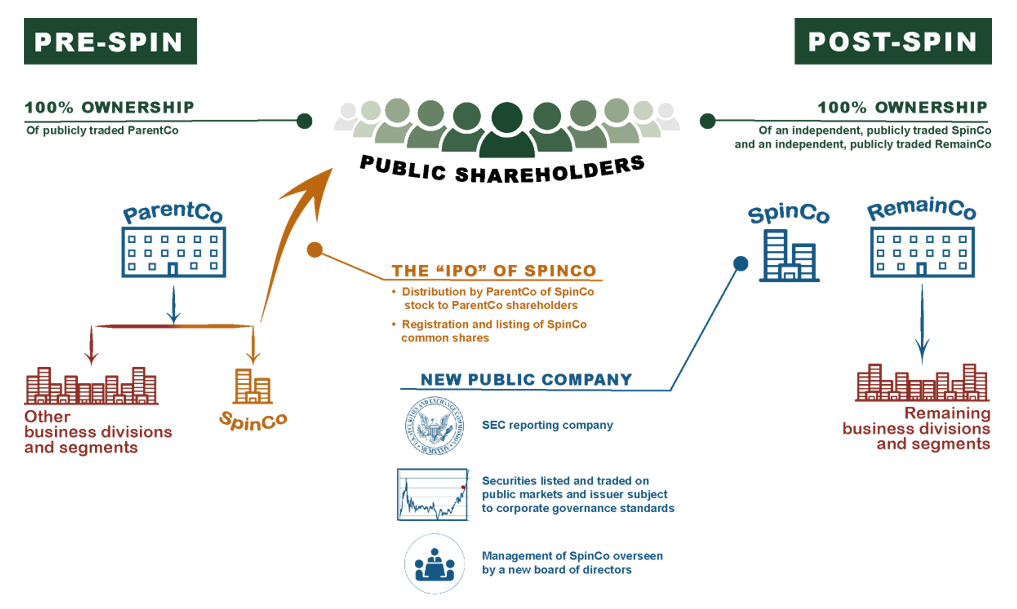

In a spin-off, a public company separates one or more of its businesses into a new, publicly traded company. For the public company that initiates it, a spin-off can achieve a number of critical business and financial objectives, including:

- Potentially achieving a greater valuation multiple and unlocking shareholder value by disposing of lower-valuation business segments

- Permitting investors to evaluate and make investment decisions based on the separate investment characteristics of each company

- Allowing the management teams of the separate companies to focus on their distinct core business, unhindered by the needs of the other business, leading to superior performance and results

- Providing the separate companies the flexibility to pursue distinct capital allocation strategies based on their respective business needs and priorities, and potentially achieving a more favorable cost of capital and greater access to the capital markets

- Allowing the divestment of a non-core business in a tax-efficient manner

A spin-off requires advanced planning across a number of disciplines, incorporating elements of capital markets, tax, finance, intellectual property, and mergers and acquisitions. This post identifies some of the primary considerations companies may wish to take into account to help ensure a successful spin-off.

Overview

In a traditional spin-off transaction, the board of directors of the parent company (ParentCo) authorizes and declares a distribution of stock of the entity owning the assets and liabilities of the business to be spun (SpinCo) to its stockholders on a pro rata basis to form a stand-alone, independent publicly traded company.

The IPO

Marketing SpinCo’s Growth Story and Market Opportunity—Beyond the Tax Business Purpose

In essence, spin-off transactions are another form of taking a business public. Though no securities are being sold, the Form 10 registration statement can serve the same purpose as an IPO S-1 registration statement. The Form 10 is an opportunity to market SpinCo’s growth story and to identify SpinCo’s competitive strengths, strategy, position in the industry, and market opportunity. To create the most compelling story, SpinCo should involve investment bankers who are familiar with the relevant industry, peer companies, and market dynamics, as well as SpinCo’s go-forward management team, who will sell the story to both existing and new investors during any non-deal roadshows and post transaction. In addition to serving as a marketing document, the Form 10 will also provide the basis for future investor presentations and SpinCo’s ’34 Act disclosure (i.e., Annual Report on Form 10-K), once SpinCo is a stand-alone public company. The Form 10 should not be viewed simply as a disclosure document that meets specified rule requirements, but rather as a marketing opportunity to sell SpinCo’s story to the investment community.

In contrast to IPOs, one advantage of a spin-off transaction is ParentCo does not need to time “market windows,” due to the fact that a spin-off is a distribution of stock as opposed to a capital raise. As a result, ParentCo is able to dictate timing and have greater certainty of execution.

The Disclosure Regime

Form 10 Registration Statement

Form 10 is a ’34 Act registration statement (unlike an IPO S-1 which is a ’33 Act registration statement) filed by SpinCo under SpinCo’s EDGAR filing codes. Like an S-1 registration statement used in a pure IPO, a Form 10 may be confidentially submitted, and will go through a full comment process with the SEC before being declared effective. Similar to the prospectus in an S-1, the information statement, which is filed as an exhibit to the Form 10 registration statement, is the primary disclosure document SpinCo will file with the SEC. The information statement will also be mailed to all of ParentCo’s stockholders in advance of the distribution and spin-off. While the formal rules applicable to Form 10 are less onerous than an S-1, common practice is to include fulsome disclosure and to mimic the structure of an S-1. A key gating issue with respect to the Form 10 will be determining which financials are required—this can be a time-consuming process and should be one of the first issues the deal team addresses.

Notwithstanding the fact that legal opinions on the disclosure in a Form 10 are not given, and comfort letters are not provided by the accountants as in a traditional IPO, SpinCo will still have liability on the Form 10 and will want to conduct a rigorous process to ensure accuracy of the disclosure. Treating the information statement in a similar manner to a capital markets offering document will also position the company for future transactions, in which they will be required to deliver legal opinions and comfort letters to underwriters.

The Separation and Distribution Agreement, Transition Services Agreement, Tax Matters Agreement, and Employee Matters Agreement discussed below are all traditionally filed as exhibits to the Form 10.

Corporate Governance—Key Considerations

After the bell at the Exchange has been rung and the champagne has stopped flowing, SpinCo will need to be ready to live life as an independent, public company. In parallel with the Form 10 registration process, SpinCo will need to determine a number of corporate governance matters and implement important governance policies and procedures. SpinCo will need to finalize the board composition, including identifying which of ParentCo’s board members, if any, will move over and serve on SpinCo’s board, as well as identifying new directors who meet applicable independence requirements. SpinCo will also want to adopt a public company charter and bylaws with well-thought-out and appropriate takeover defense provisions (replacing the bare bones versions implemented at SpinCo’s formation), and adopt and implement a myriad of corporate governance policies—including SEC- and exchange-compliant board committee charters, corporate governance guidelines, and insider trading and Regulation FD policies, among others. Additionally, SpinCo will need to begin building effective internal controls over financial reporting and implementing disclosure controls and procedures. In connection with SpinCo’s second 10-K filing, SpinCo’s management will be required to assess the effectiveness of SpinCo’s internal controls over financial reporting, and, unless SpinCo is an emerging growth company (EGC), its auditor will be required to attest to, and report on, such assessment.

A natural tendency and common mistake is for ParentCo to simply “dupe” ParentCo’s governance structure at SpinCo, rather than give specific thought as to which governance structure is best suited to SpinCo as a new, stand-alone public company. ParentCo’s governance structure is likely based on best practices for a mature, public company, having evolved over the course of ParentCo’s history as a result of shareholder and board engagement

and aligned with best practices advocated by proxy advisory firms such as ISS and Glass-Lewis. However, best practice for a public company at ParentCo’s stage of corporate life may not be desirable for a newly spun-off public company that may have a one-, two-, or three-year ramp to achieve profitability, execute on its business plan, or simply get its sea legs. Newly spun-off companies regularly receive shareholder proposals on corporate governance matters one or two years following their debut as a public company. As a result, SpinCo must have a governance structure in place that gives SpinCo the runway it needs for its management team to execute on SpinCo’s long-term business strategy and to prove themselves as an independent management team running a stand-alone business.

The need for a governance structure is particularly pressing for SpinCo’s procedural and structural activism and takeover defenses. As a commercial matter, SpinCo is often “immature” on many levels at the point of separation and may face the following challenges:

- The equity markets will not have fully and efficiently valued SpinCo, as ParentCo’s legacy shareholders may sell off shares due to differences in status with ParentCo (index inclusion, capitalization, sector, or geography)

- The management team is just getting their sea legs both operationally and in interacting with institutional investors

- SpinCo will be burdened with the often high hurdles for future performance that ParentCo set when marketing the spinoff to its shareholders and analysts

- SpinCo’s directors may have just joined the board, and are unfamiliar with SpinCo’s operations and longer-term strategies, as well as each other

Further, there is no “honeymoon period” for SpinCos with activists and acquirors—a point exemplified by the unsolicited offer for Baxalta days after its spin from Baxter and the intense activism by Starboard Value at Cars.com within months after completion of its separation from Tegna. As a consequence, providing SpinCo with both procedural and structural protections against unsolicited bids and activism during this vulnerable post-spin window will protect and enhance shareholder value at SpinCo, not diminish it. Implementing many of the required protections in a spin-off is particularly easy—including a classified board, prohibitions on the calling of special meetings, or actions by written consent, by shareholders, and omit majority vote, proxy access, and similar “shareholder friendly” mechanisms—as such protections will not have a particularly adverse impact on shareholder approval or “purchase” decisions by investors in the spin-off distribution paradigm. Similarly, employment agreements with market-level protections for executive officers and severance programs for other key employees often provide the comfort needed for leadership to focus on long-term value creation for shareholders.

SpinCo’s full board is typically not constituted until the spin-off occurs, but will inherit the governance structure and transaction agreements put in place by ParentCo. Therefore, as a practice point, ParentCo should consider holding an informal meeting of the to-be-constituted SpinCo board prior to the date of the spin-off to walk them through these agreements, including the Separation and Distribution Agreement, and to describe the governance structure in an effort to obtain “buy in” from the new SpinCo board.

Interacting With Equity Research Analysts

In a traditional IPO, companies host an analyst day to share management’s financial model (including detailed, long-range projections (i.e., three-year projections)) with the research analyst at each of its lead investment banks, to allow the research analyst to produce his or her proprietary model on the company prior to the commencement of the investor road show and closing of the transaction. However, in a spin-off transaction, companies are not permitted to share management’s model and projections with research analysts as sharing such information would be in violation of Regulation FD, which broadly prohibits public companies from selectively disclosing material non-public information (MNPI). ParentCo is a public company subject to Regulation FD, and in most spin-off transactions the division or segment being spun off represents a material portion of ParentCo’s business, therefore, projections regarding such division or segment constitute MNPI. As a result, analyst day meetings are typically not held in a spin-off transaction.

A consequence of not being able to share such projections with research analysts in a spin-off transaction is that some research analysts, including analysts who already cover ParentCo, may take a period of time post-closing before they initiate coverage on SpinCo. During this time, analysts will diligence SpinCo, wait for SpinCo to provide guidance to the Street, and build their own proprietary models.

When Is Guidance Provided?

In most spin-off transactions, SpinCo management often waits until SpinCo’s first quarterly earnings call post-closing of the transaction before providing annual guidance. This timing allows SpinCo management to review its guidance policy and actual guidance figures with SpinCo’s board of directors, which will be newly-constituted at closing of the transaction. As an alternative, some SpinCos choose to publish their forecasted guidance figures immediately prior to the closing of the transaction so that they can discuss the guidance with investors during non-deal roadshows. These non-deal roadshows are typically held a couple of weeks prior to the closing and during the “when-issued” trading period (discussed below). It is common practice for both ParentCo and SpinCo to file the investor deck to be used at such non-deal roadshows on a Current Report on Form 8-K to satisfy Regulation FD requirements.

When Does SpinCo’s Stock Typically Trade at a Multiple That Represents Fully-Distributed Value?

As a result of SpinCo’s inability to provide research analysts with long-term projections and the typical timeframe in which SpinCo provides annual guidance to the Street, it often takes two to three quarters post-closing for SpinCo’s stock to trade at a multiple that represents fully-distributed value.

The When-Issued Trading Market

The when-issued trading market refers to the period of time after the spin-off has been authorized and a record date has been established, but prior to the actual issuance of shares of SpinCo’s stock (which occurs on the distribution date) when SpinCo’s stock trades on a conditional or when-issued basis. The when-issued market commences on the trading date immediately prior to the record date for the distribution and ends on the distribution date, typically at the close of market. The when-issued trading market typically lasts for 7–10 business days (and cannot be more than two weeks), and trading volume tends to be light until the day or two leading up to the distribution date. During this time, in addition to the when-issued market for SpinCo, two markets are established for ParentCo—a “regular-way” market, in which ParentCo shares trade along with the right to receive shares of SpinCo’s stock on the distribution date, and an “ex-distribution” market, in which RemainCo shares trade without such right. Regular-way trading for SpinCo stock commences on the trading date immediately following the distribution date. The exchanges designate when-issued trading by adding the symbol “WI” to the end of SpinCo stock’s expected trading symbol (i.e., SPIN-WI) and, with respect to ParentCo’s ex-distribution trading, to the end of RemainCo stock’s expected trading symbol. The following is an example of the potential trades that investors can make during the when-issued trading market:

- ParentCo Ticker = ParentCo shares and right to receive SpinCo shares on the distribution date (equivalent to the combined company shares)

- RemainCo Ticker WI = RemainCo shares without the right to receive SpinCo shares on the distribution date

- SpinCo Ticker WI = The right to receive SpinCo shares on the distribution date

Investors who purchase RemainCo Ticker WI or SpinCo Ticker WI in the when-issued market between the record date and the distribution date receive a “due bill,” and such trades are settled two days following the distribution date.

The benefits of a when-issued trading market are that it can indicate the demand for SpinCo and RemainCo stock and attract investors who don’t own ParentCo stock by allowing them to begin trading the right to receive shares in the spin-off on a when-issued basis. The when-issued trading market can also reduce volatility in SpinCo and RemainCo stock once the stocks trade on a regular-way basis, and can provide liquidity for the sale of fractional SpinCo shares by the transfer agent prior to the distribution date.

From a governance perspective, under the listing requirements SpinCo must have at least one independent director on its Audit Committee at the time when-issued trading commences. As the SpinCo board of directors is typically not constituted until the distribution date, companies should be mindful of this requirement to appoint an Audit Committee member in advance of closing the transaction.

Successfully Executing SpinCo’s IPO—Timeline and Key Dates

Clearing a Form 10 with the SEC follows the same process as clearing an S-1, with the same 30-day window for initial comments and approximate 10–14 day window for subsequent comments. The end stages of a spin-off do offer more timing flexibility than a traditional IPO, however certain considerations should be kept in mind.

Declaration Date

The declaration date is the date the spin-off is declared, when the ParentCo board formally approves the spin-off and sets the record date, distribution date, and distribution ratio. The two primary considerations when selecting the distribution date are the status of the SEC process and Exchange notice requirements. Though the Form 10 does not have to be completely cleared with the SEC prior to the declaration date, ParentCo and SpinCo should have confidence by the declaration date (including conversations with their SEC examiner) that all comments from the SEC will be resolved prior to the intended record date, to avoid any date changes subsequent to board approval.

Additionally, for example, the NYSE has a strict 10-calendar-day notice requirement in advance of the record date. As the NYSE has clarified in recent years, only one small exception exists to this requirement—notice can be provided to the public eight calendar days prior to the record date (via press release) provided that private notice has been provided to the NYSE at the requisite 10 calendar days. Public notice should not be given until there is board approval, so the declaration date should be at least 10 calendar days prior to the intended record date.

Form 10 Effective Date

Similar to a traditional IPO, any confidentially filed Form 10 must be publicly filed 15 days prior to going effective (since a spin-off does not involve an offering-related roadshow, the 15-day requirement relates to effectiveness of the registration statement instead of a roadshow launch). Upon expiration of that 15-day period, effectiveness can be requested any time after the Form 10 and information statement are in final form (including, with some limited exceptions, spin-related details like dates, distribution ratios, and share counts). Effectiveness is advisable, though not required, prior to printing the information statement for stockholder mailing, as no changes should be made after printing has begun. Effectiveness is required prior to the commencement of when-issued trading as well as any non-deal roadshow, and is also required for the transfer agent to initiate eligibility conversations with DTC.

Record Date

As noted above, the record date should be at least 10 calendar days after the declaration date, but can be later. When-issued trading will always begin the trading day immediately prior to the record date. The record date will also impact logistics related to the mailing of the information statement. Broadridge, who will coordinate mailings to all beneficial holders whose shares are held through DTC, requires approximately three business days following the record date to finalize the stockholder list and begin the mailing process.

Distribution Date

The amount of time between the record date and distribution date is usually driven by the desired length of when-issued trading—traditionally 7–10 business days, and capped at two (calendar) weeks by the Exchanges. The distribution date is also driven in part by DTC. SpinCo’s shares must be DTC-eligible by the distribution date, and DTC requests 10 calendar days’ advance notice for eligibility (though occasionally they do not require the full amount of time). Assuming notice and all required documents are sent to DTC on the effective date (see above), then the distribution date should be no earlier than 10 days after the effective date. Additionally, the information statement should at least be mailed to, but ideally delivered to, all stockholders prior to the distribution date. As a practical matter, first-class mailing of the information statement is often necessary.

Sample Spin-Off Timeline

Wednesday, April 24, 2019 – Public Filing of Form 10 (Flip to Public)

Wednesday, May 1, 2019 – Declaration Date

Thursday, May 9, 2019 – Form 10 Effective Date

Friday, May 10, 2019 – Start of When-Issued Trading on Exchange

Monday, May 13, 2019 – Record Date

Wednesday, May 22, 2019 – Distribution Date (Separation Occurs)

Thursday, May 23, 2019 – Start of Regular-Way Trading on Exchange

The Carve-Out

Defining the Business to be Separated—What’s In / What’s Out?

As an initial matter, ParentCo has the ability to define the scope of the business SpinCo will conduct. ParentCo will have two primary goals in this regard. First, ParentCo, in consultation with its financial advisor, will seek to delineate SpinCo’s business in a manner that will create a compelling investment thesis for both SpinCo and RemainCo. Second, ParentCo will want to ensure that the nature of the business being spun off relative to the business being retained supports ParentCo’s underlying rationale for conducting the spin. For example, if ParentCo desires to separate the two businesses in order to reduce ParentCo’s cost of capital, it should demarcate SpinCo’s business in a manner that is designed to achieve that goal.

Once ParentCo has identified the business that SpinCo will conduct, it will outline the structural steps needed to transfer that business into SpinCo. This process may involve moving ParentCo subsidiaries, transferring specific assets and liabilities (including contracts, intellectual property, and real estate), and selecting the employees who will support the SpinCo business. Once the spin-off steps have been defined, ParentCo will divide these steps a number of functional workstreams; these workstreams may require involvement from the treasury, tax, financial reporting, human resources, supply chain, and investor relations functions at ParentCo. ParentCo and its counsel also will begin preparing the legal documentation (i.e., Form 10 and related transaction documentation) to effect the transfers that are required to establish SpinCo’s business.

Capital Structure

Along with identification and transfer of SpinCo’s business, ParentCo must consider the appropriate initial capital structure of SpinCo. In particular, ParentCo must determine both the nature and amount of debt at SpinCo at the time of the spin-off, which will depend in large part on the nature of SpinCo’s business and the reasons for ParentCo’s desire to undertake the spin-off. If ParentCo is seeking to conduct the spin-off as a means of de-levering itself, for example, it may seek to either transfer debt to SpinCo or cause SpinCo to incur new debt and distribute the borrowings to ParentCo. Whether SpinCo’s new debt takes the form of a credit facility, newly issued bonds, or assumed debt from ParentCo also will depend on SpinCo’s ability to access new bank debt or debt capital markets around the time of the spin-off.

Separation and Distribution Agreement

The Separation and Distribution Agreement establishes the framework for the separation of SpinCo as an independent company and the relationship between ParentCo and SpinCo post-transaction. This agreement will define the business to be spun and allocate assets and liabilities between ParentCo and SpinCo. In some transactions, this agreement can provide an opportunity for ParentCo to offload unwanted liabilities to SpinCo, though ParentCo should keep in mind SpinCo’s solvency requirements. To the extent restructuring steps are required in order to position such assets and liabilities with the appropriate entity, this agreement will also traditionally outline such steps, and can include their completion as a closing condition to the spin-off. The agreement includes a number of other conditions to close, such as the satisfaction of regulatory requirements, the listing of SpinCo with the applicable exchange, effectiveness of the Form 10 registration statement, and more. The Separation and Distribution Agreement will also contain indemnification provisions between the parties that often survive indefinitely post-closing and can be the subject of post-closing disputes.

Though the actual negotiation of the Separation and Distribution Agreement commonly occurs later in the process to minimize the impact of oft-challenging dynamics between ParentCo and SpinCo, the parties must identify the allocation of assets and liabilities early in the process. Doing so will allow sufficient time to determine the often-complicated mechanics of the separation and facilitate drafting of the Form 10 and the creation of its required financial statements. As ParentCo’s board and management team control the spin-off, the terms of the separation are typically established by ParentCo and inherited by SpinCo and its board.

Transition Services Agreement

In most spin-off transactions, ParentCo frequently provides certain transition services to SpinCo for a period of time post-closing. The breadth and length of these services often depends on how intertwined the two businesses were pre-closing, and typically most transition services last between three and 18 months. The Transition Services Agreement is the agreement pursuant to which ParentCo and SpinCo agree on the transition services, and parties usually schedule the scope of services to be provided, as well as the term and pricing. This schedule is typically excluded from the Transition Services Agreement, which is filed as an exhibit to the Form 10. Understanding which transition services will be needed, how they will be provided, and how long the services will last can be a long lead-time item in the process.

Establishing the Management Team and Other Employee and Cultural Matters

The ultimate outcome of a spin-off transaction is to create a stand-alone, independent, publicly traded company, with SpinCo having its own board of directors, management team, employees, and corporate headquarters. At some point in the transaction it will be necessary to determine who will form the leadership of SpinCo (i.e., Chairman of the board, CEO, and CFO), which officers and employees are joining SpinCo, and who is remaining with RemainCo. Sometimes it is obvious when the business being spun off is a segment or division that has operated largely independently with a clearly identifiable management team, and other times it is not so clear cut when the business being spun is intertwined to a meaningful degree with the overall business. Particular challenges may arise across shared corporate functions and with regional or international leadership teams, in particular if the combined organization typically engaged with government officials or ministries as a “single face” for the organization.

The timing of when these decisions are made and announced is important as inevitably once the “teams” are selected, a dynamic of “us versus them” can begin to develop, leading to potential conflicts of interest and cultural issues. In addition, care should be taken from a change management perspective to recognize that, for many individuals, the separation into teams impacts long-standing personal and professional relationships or may present a meaningful change to career development planning. There may also be a perception of “winners” and “losers” that will need to be managed from a retention and incentive perspective.

To ensure a successful execution of the transaction for both SpinCo and RemainCo, both companies need everyone rowing in the same direction. As a result, ParentCo’s board and senior management team must balance the need to make decisions with respect to SpinCo, so that SpinCo is well-positioned to successfully operate as a stand-alone company and, at the same time, that decisions are not made too early in the process to potentially negatively impact deal dynamics and the company’s culture. It is common for ParentCo to name SpinCo’s Chairman, CEO, and CFO earlier on in the process (often at the time of the announcement of the intention to spin off the business) to enable pre-planning for SpinCo’s financial profile and strategic and cultural frameworks, with decisions on the management team and employee base coming later in the process. While this approach is effective in maintaining business continuity, if the allocation of employees between RemainCo and SpinCo is unclear, an unreasonable gap in communication may create unnecessary anxiety and potential retention issues among the employee base. One potential mitigation for this risk is to make decisions on a staged, leveled basis, determining layers of leadership one at a time, from most senior to junior. This method enables each management level to engage in the allocation of headcount to best preserve high-performing teams and ensure equitable allocation of talent to set up both companies for success. Regardless of the process selected, consistent communication to employees is critical—even if only to communicate that no decisions have been made yet—as employees will fill an information void with their own predictions or suspicions.

Once employee allocation decisions have been made and communicated, having a formal process in place to manage inevitable appeals of placement decisions and “back room” recruiting efforts is vital. A dedicated talent management committee (with representation from both RemainCo and SpinCo) may be useful in managing these activities, but a clear decision-making process with a near-zero tolerance for exceptions is crucial to maintaining order and focus among the employee base.

Employee Matters Agreement

The Employee Matters Agreement governs ParentCo’s and SpinCo’s compensation and employee benefit obligations relating to current and former employees of each company, and generally allocates liabilities and responsibilities relating to employee compensation and benefit plans and arrangements. This agreement will specify how outstanding ParentCo equity-based compensation awards are treated in connection with the separation. For example, ParentCo awards may “follow” the employee, with ParentCo awards held by employees of SpinCo converted into SpinCo awards and ParentCo awards held by employees remaining with ParentCo continuing to represent ParentCo awards. Alternatively, all employees may be treated the same, regardless of which entity will be the holder’s employer after the separation, in which case either (i) all awards may be split into two awards, one representing an award in ParentCo and one representing an award in SpinCo, or (ii) all awards may continue to represent a ParentCo award. Irrespective of which approach is adopted, the aggregate intrinsic value of the award immediately prior to the separation will be preserved immediately after the separation through adjustments to the awards that reflect the change in value of ParentCo resulting from the separation and, if applicable, the new value of SpinCo.

Duties of ParentCo’s Board of Directors

ParentCo’s board must satisfy its duties of care and loyalty to ParentCo and its stockholders in making the decision to distribute SpinCo’s stock to its stockholders and satisfy itself that the distribution is a permissible dividend.

In determining to distribute SpinCo’s stock and effectuate the distribution and separation, under Delaware law, ParentCo’s board of directors and executive officers do not owe any fiduciary duties to SpinCo or its future stockholders. As a consequence, the directors of ParentCo are free, as a fiduciary matter, to consider the interests of only ParentCo’s shareholders in establishing the terms of the spin-off and separation arrangements. However, as ParentCo’s shareholders will receive the SpinCo shares, setting up SpinCo for commercial failure, or establishing a capitalization under which SpinCo cannot practically operate (or might even lead to its insolvency), could lead to a breach of fiduciary duty claim by ParentCo shareholders or possible claims of fraudulent conveyance.

A traditional spin-off transaction is a distribution, or dividend, under state law and the declaration of the dividend must comply with the requirements of the law of the state in which the parent company is organized. For Delaware corporations, boards of directors must determine that ParentCo has sufficient “surplus” (the amount by which net assets exceed capital) from which to pay the dividend. In the case of a spin-off the dividend is composed of the value of the equity interests in SpinCo being distributed.

For purposes of this calculation, actual current value, not book value, should be used—this ordinarily results in a substantial increase in surplus relative to book. In Delaware, a board may utilize third-party experts to validate the calculation of assets (defined as the amount by which total assets exceed liabilities) in calculating adequate surplus; as directors can bear personal liability for an improperly declared dividend, use of third-party advisors or reasonable reliance on well-founded management analysis of net assets and solvency is recommended. Stockholder approval of the dividend is typically not required under the laws of most states.

Achieving the Tax Objectives

Qualifying as a Tax-Free Spin-off

The benefit of a tax-free spin-off is that there is no tax at either the ParentCo level (with respect to the appreciation in SpinCo) or at the shareholder level (with respect to the value of the SpinCo stock received). In order for a spin-off to qualify as tax-free, the transaction has to meet a number of requirements. A detailed description of all of the requirements is beyond the scope of this article, but the principal tests in brief are as follows:

- Active Business Test. ParentCo and SpinCo must have each actively conducted a business for at least five years, and not have acquired such business in a taxable transaction within the past five years (unless such acquisition qualifies as an “expansion” of an existing business).

- Corporate Business Purpose. The spin-off must be motivated by a corporate level business purpose (other than the saving of federal taxes) that cannot be efficiently achieved through any other nontaxable transaction. Note that shareholder-level business purposes (g., to increase shareholder value) are not sufficient (though they may provide a basis for demonstrating a valid corporate business purpose). Examples of common business purposes include the following:

- To facilitate access to capital (for either ParentCo or SpinCo)

- To enhance “fit and focus” of the ParentCo and SpinCo businesses

- To provide an equity interest in either the ParentCo or SpinCo business to current or prospective employees

- To facilitate the use of equity as an acquisition currency (where spin-off is expected to increase equity value and thereby reduce dilution)

- To facilitate a tax-free acquisition of ParentCo or SpinCo (g., a “Reverse Morris Trust” transaction)

- Distribution of Control. ParentCo must distribute at least an 80% interest in SpinCo to ParentCo shareholders. Note that there are additional requirements to satisfy if ParentCo retains any stock ownership in SpinCo.

- Device Test. Spin-off cannot be used principally as a device to distribute earnings and profits. A key factor that tends to show a possible device is a plan or intent at the time of the spin-off to sell ParentCo or SpinCo in a taxable disposition after the spin-off.

- Limitations on 50% Purchases of Stock in Five Years Preceding Spin. There cannot have been a 50% or more “purchase” of ParentCo or SpinCo stock within the past five years.

- Limitations on Acquisitions of ParentCo or SpinCo Stock as Part of a “Plan” with the Spin-Off. One or more persons cannot acquire 50% or more of either ParentCo or SpinCo as part of a “plan” with the spin-off, or else the spin-off is taxable (though only at the corporate level). Any acquisition that occurs from two years before the spin-off to two years after the spin-off is presumed to be part of a “plan,” but the presumption is rebuttable, and there are several helpful safe harbors.

A related consideration is whether to seek a ruling from the IRS on the tax-free nature of the spin-off, or to instead rely on any opinion of counsel. While historically most public companies sought rulings, in recent years the trend has been to rely on an opinion of counsel (which eliminates the timing variable of waiting to obtain an IRS ruling).

Tax Matters Agreement

The Tax Matters Agreement has two basic functions. The first is to govern ParentCo’s and SpinCo’s respective rights, responsibilities, and obligations after the separation and distribution with respect to tax liabilities and benefits arising in the ordinary course of business during the pre-spin period, including the division of tax attributes, the preparation and filing of tax returns, the control of audits, and other tax matters. The second is to safeguard the tax-free treatment of the spin-off and to allocate responsibility for the resulting taxes should the spin-off ultimately be found to be taxable. In particular, the Tax Matters Agreement typically lists a number of post-spin transactions (e.g., disposition of assets, acquisition or issuance of SpinCo stock) that SpinCo cannot engage in within two years after the spin-off without first obtaining an opinion of counsel acceptable to ParentCo. The agreement also imposes an indemnification obligation on SpinCo should it cause the spin-off to be taxable regardless of whether it obtains an opinion. The agreement typically does not have a symmetrical set of restrictions on ParentCo, since ParentCo is already incentivized not to cause the spin-off to be taxable given that ParentCo is the liable party vis-à-vis the IRS for any tax liabilities resulting from the spin-off being taxable.

Conclusions

Spin-offs require many of the same business and legal preparations as an IPO—with the added complexity of separating a business in two. ParentCo must not only register SpinCo with the SEC and successfully market SpinCo stock to investors and analysts, it must also prepare SpinCo to operate as a stand-alone public company and address employee, cultural, and business changes that go along with separating a business unit. This complex method of IPOing a new company benefits from legal advice that pairs technical sophistication with a deep understanding of all the commercial, legal, tax, and regulatory hurdles that could arise. Latham combines premier capital markets and transactional tax practices with many years of experience advising on spin-off transactions to offer clients market-tested, practical advice to navigate the spin-off process successfully.