Print

PrintBrigid Rosati is Director of Business Development, Hannah Orowitz is a Managing Director, and Rajeev Kumar is Senior Managing Director at Georgeson LLC. This post is based a recent Georgeson memorandum by Ms. Rosati, Ms. Orowitz, Mr. Kumar, Don Cassidy, Talon Torressen, and Ed Greene.

Executive Summary

We are pleased to announce the publication of our 2019 Annual Corporate Governance Review. For the third year in a row, Georgeson partnered with Proxy Insight to coordinate voting data and analytics.

We have expanded our review of environmental, social and governance shareholder proposals that were subject to a vote during the period July 1, 2018 through June 30, 2019.

Governance Shareholder Proposals

The number of corporate governance-related proposals submitted during the 2019 proxy season continued to trend downwards, albeit on a relatively incremental basis. Approximately 71% of these proposals reached a vote, in line with the range of 62% to 75% over each of the past five years. Overall, of the 236 proposals that reached a vote, 43 received majority support across the following categories:

| Proposal Category | Number passed in 2019 |

|---|---|

| Proxy Access | 3 |

| Executive Compensation | 2 |

| Eliminate/reduce Supermajority voting/adopt simple majority for all items | 16 |

| Special Meeting (adopt or reduce threshold) | 4 |

| Shareholder right to act by written consent | 5 |

| Declassify the Board (all the Chevedden group) | 5 |

| Adopt simple majority vote for director elections | 4 |

| Other (amendments to organizational documents and shareholder approval of poison pill) | 4 |

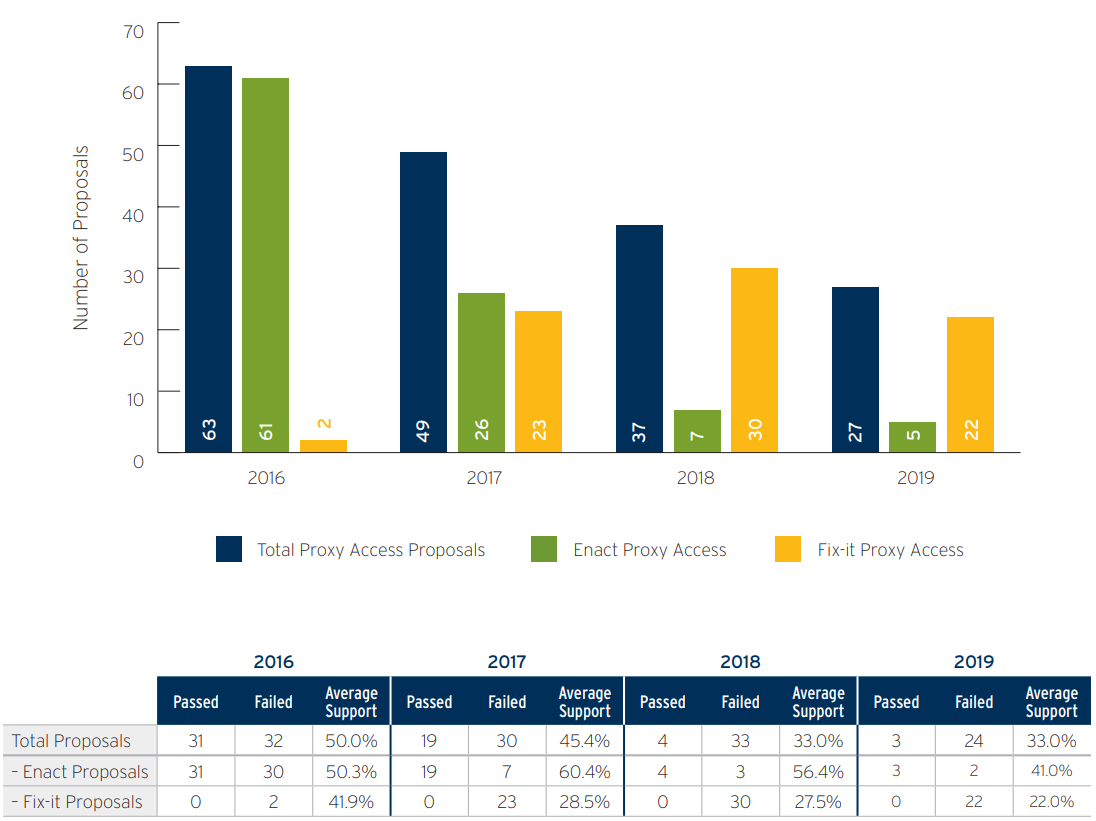

Proxy Access

The three proposals that received majority support this season all called for the adoption of market standard proxy access provisions. [1] Twenty-two of the remaining 24 proposals that failed to receive majority support were so called “fix-it” proposals filed by the Chevedden group. [2] We note that while ISS generally recommended in favor of these proposals, Glass Lewis recommended against them.

The incremental decline in proxy access proposals this year is additional evidence that the current widespread adoption of proxy access among the S&P 500 is unlikely to carry over into the broader S&P 1500 or Russell 3000 indices at a similarly rapid pace. However, we expect this proposal will continue to be filed selectively at companies, often in situations where other performance or governance concerns exist. For example, following shareholders’ disappointment with American Outdoor Brands’ response to a 2018 majority-supported shareholder proposal related to gun safety measures and industry risks, it received a proxy access shareholder proposal. [3]

Chart: Proposals Relating to Proxy Access—2016 to 2019, Figure 7 in 2019 ACGR

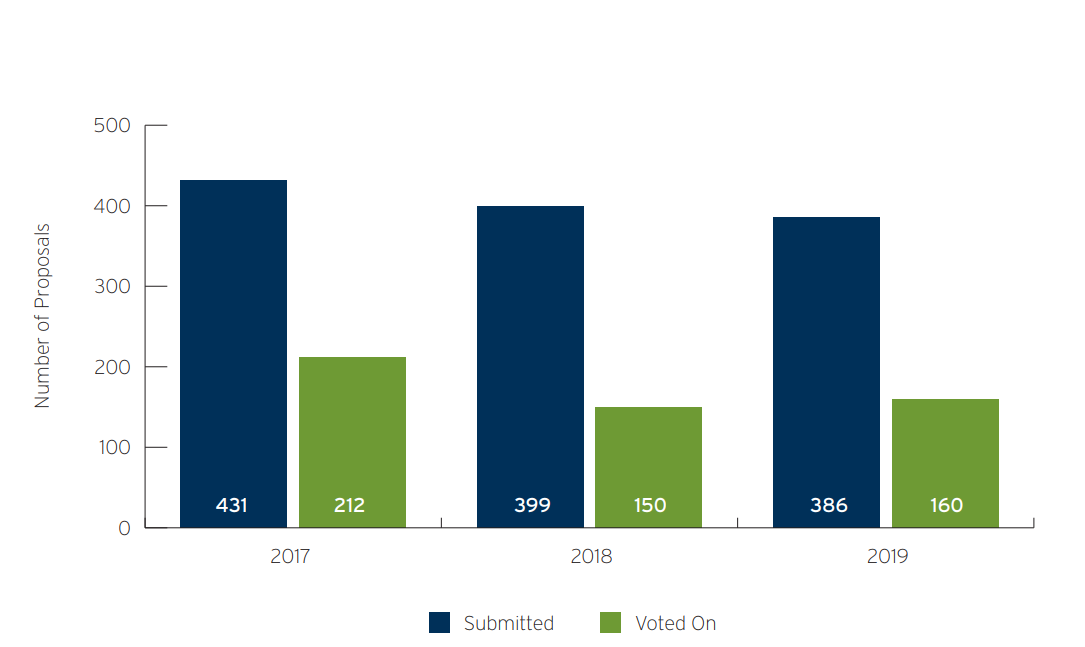

Environmental and Social Shareholder Proposals

In 2019, shareholders submitted over 380 E&S-related proposals to S&P 1500 companies; 160 of these proposals reached a vote. As shown below, this number is slightly up from 2018 but significantly below 2017 where 212 proposals reached a vote.

Chart: Number of Environmental and Social Proposals Submitted and Voted On—2017 to 2019, Figure 10 in 2019 ACGR

Lobbying/Political contributions

Much of corporate America now believes disclosure of political donations is important to good governance. However, given the focus on the 2020 U.S. presidential election, it is unsurprising that shareholder proposals relating to political lobbying payments and/or contributions were a significant topic in 2019.

The proponents of these proposals varied, with the majority coming from individual shareholders, faith-based groups and pension funds. The variety of sponsors suggests this issue is important to a broad spectrum of investors.

The Center for Political Accountability noted that many proposals were withdrawn this year due to successful agreements between companies, boards and proponents. [4] Even so, 64 proposals on this topic went to a vote in 2019. These measures attracted an average support level of 33%, which is the highest average level of support across all E&S shareholder proposal types. In 2017 and 2018 no such proposals received majority support. In contrast, this season, the proposal received majority shareholder support at three companies.

Director Elections

The investor spotlight continues to shine on directors. Consistent with the trend we identified last year, votes against director elections continues to increase. BlackRock and Vanguard, as well as other large investors, supported fewer incumbent directors this year compared to last. Investors continue to update voting policies related to director votes.

Say-on-Pay

Say-on-pay vote results for 2019 continued to be strong with the average support for the S&P 500 companies at approximately 91% of votes cast in favor (excluding abstentions). Approximately 79% of the S&P 500 companies received 90% or more shareholder support compared to the approximately 81% of the companies in 2018. Similar support levels were seen for the S&P 1500 companies with approximately 91% average votes cast in favor and 80% of the companies receiving greater than 90% vote support. 2019 results for the S&P 1500 companies were comparable to those in 2018.

CEO Pay Ratio

Commencing in 2018, companies with a fiscal year beginning on or after January 1, 2017 were required to include in their 2018 proxy statements the CEO Pay Ratio. In 2019, average pay ratio across the Russell 3000 companies was 157:1, up from 143:1 average in 2018. The Consumer Cyclical and Utilities sectors continued to have the highest (478:1) and lowest (68:1) average pay ratios, respectively.

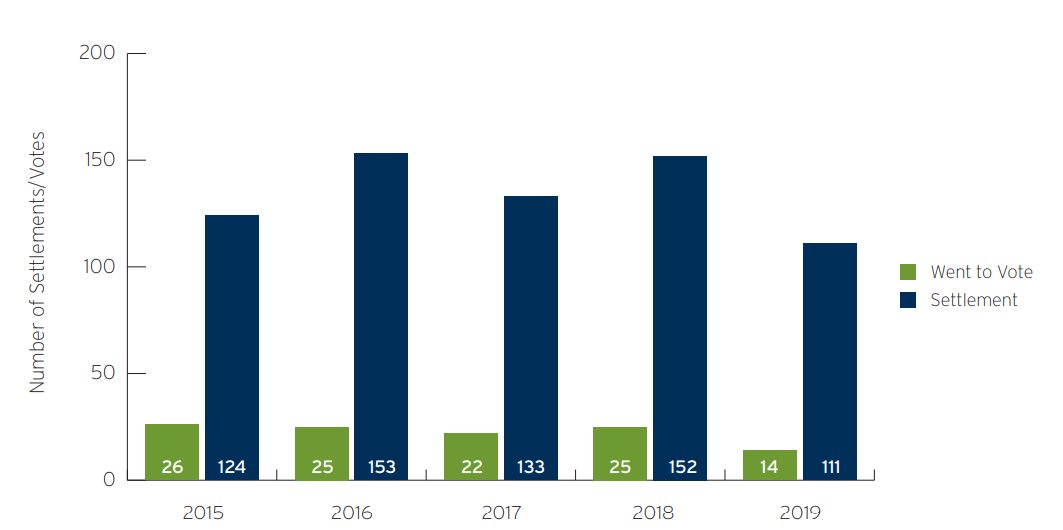

M&A and Activism

Total M&A activity in the U.S. has remained strong over our reporting period. Although most deals do not require shareholder approval, there was an increase in deals that did necessitate a shareholder vote over the past year as compared with the prior season. The ripe environment for M&A has been influenced in part by U.S. tax reform, which has freed up capital for companies to deploy in deals. Additionally, the M&A market has been buoyed by a supportive US regulatory environment. By contrast, cross-border transactions have slowed as recent trade tensions and government sensitivity on these types of deals has increased.

Traditional activism remained strong over the past year but decreased from the record pace set in the year prior. The main demands continued to be improvements to governance practices, M&A and board representation. In many cases, an activist may obtain one or more board seats via a settlement agreement with the target. Indeed, one industry commentator described this practice as “the bread and butter” of activism during 2019. [5]

Chart: Outcomes of Activist Demands for Board Representation at U.S. Companies—2015 to 2019, Figure 34 in 2019 ACGR

* * *

The complete report is available here.

Endnotes

1Since the 2014 proxy season, the majority of proxy access provisions adopted have the following terms: (1) a 3% ownership threshold (2) for a three-year holding period (3) for up to the greater of 2 board seats or 20% of the board (4) with a nominating group size limit of 20. In recent years, the percentage standard sought by proponents relating to the board cap has shifted upwards to 25%.(go back)

2Fix-it Proxy Access – Shareholder proposals that seek to amend the terms of a company’s existing proxy access by-law.(go back)

3https://www.iccr.org/sites/default/files/page_attachments/aobc_proxy_access_resolution_2019_final_1.pdf. It appears that the company amended its bylaws to implement proxy access in April 2019. We note that American Outdoor Brands is not included within the S&P 1500 generally covered herein. (go back)

4Bruce Freed, Dan Carroll, Karl Sandstrom, A Banner Proxy Season for Political Disclosure and Accountability (July 23, 2019), https://corpgov.law.harvard.edu/2019/07/22/a-banner-proxy-season-for-political-disclosure-and-accountability/.(go back)

5The Activist Investing Half-Year Review, Activist Insight, July 2019, page 4. (go back)