Print

PrintKevin Chuah is a PhD Candidate at London Business School; and Isobel Mitchell is Networks Officer and Lily Tomson is Head of Networks at ShareAction. This post is based on their ShareAction report. Related research from the Program on Corporate Governance includes The Agency Problems of Institutional Investors by Lucian Bebchuk, Alma Cohen, and Scott Hirst (discussed on the Forum here); Social Responsibility Resolutions by Scott Hirst (discussed on the Forum here); and Reconciling Fiduciary Duty and Social Conscience: The Law and Economics of ESG Investing by a Trustee by Robert H. Sitkoff and Max M. Schanzenbach (discussed on the Forum here).

Executive summary

This analysis is the second of a two-part report exploring the role and influence of proxy advisors in the investment system, with particular reference to asset managers frequently used by UK- based charity investors. The first part, “Another Link in the Chain: Uncovering the Role of Proxy Advisors” provides an overview of who the major proxy advisors are, and what influence they have on asset managers’ voting decisions. This second part analyses proxy advisors’ recommendations on environmental, social and governance (ESG) shareholder resolutions from the 2019 AGM season, compared to 23 asset managers’ voting decisions, including commonly used charity and other major asset managers.

Proxy voting is a key right of asset ownership—an opportunity for asset owners to influence the strategic direction and governance of the businesses they own. This right has increasingly been outsourced by asset owners to asset managers, who are often in turn advised by proxy advisors that provide recommendations to institutional investors on how to vote at shareholder meetings.

A major concern raised by previous research on the role of proxy advisors relates to the potential overreliance of asset managers on “proxy advisors’ recommendations, with studies indicating they can sway anywhere in the range of 13-30% of shareholder votes for various corporate governance issues.” However, most of the practitioner and academic research on proxy advisors to date has focused on their impact on ‘traditional’ corporate governance topics—for example, appointments to the board of directors, and whether executive pay levels are appropriate. It is therefore unclear from the existing research what influence proxy advisors have on responsible investment proposals.

Such proposals, which include votes on environmental and social issues, are likely to attract a greater divergence of views than business-as-usual votes. For these votes it is therefore especially important that asset managers can demonstrate that they have the appropriate resources and capabilities to make informed, active voting decisions, and are not ‘sleepwalking’ their votes.

This analysis aims to shine a light on how proxy advisors are recommending investors vote on ESG shareholder proposals, and how this aligns with investors’ voting decisions on these crucial issues. Our key findings are:

Finding 1: ISS, the largest proxy advisor, is more supportive of environmental and social resolutions than the largest asset managers.

- The majority of asset managers in our study are less supportive of ESG issues than ISS, with the largest asset managers being the least supportive.

Finding 2: There is little evidence to suggest a systematic overreliance on the recommendations of proxy advisors for responsible investment resolutions.

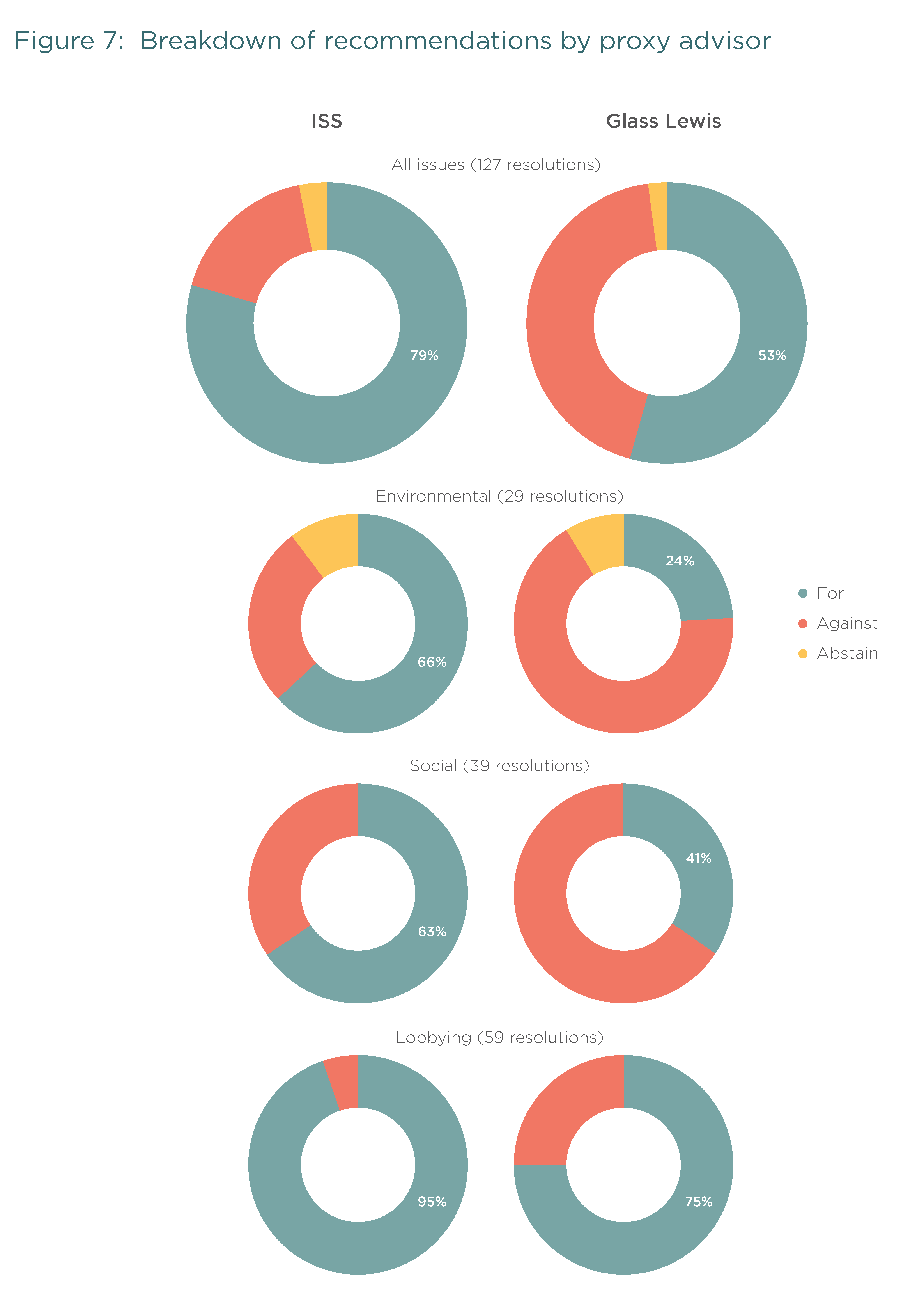

Finding 3: ISS is more likely to recommend that investors support environmental and social shareholder resolutions than the second largest firm, Glass Lewis.

- ISS recommended that investors vote “For” a shareholder resolution 79% of the time, which was much higher than the 53% of votes supported by Glass Lewis, in our sample.

In aggregate, these findings suggest that previously-raised concerns about the overreliance of asset managers on proxy advisors may need reconsideration. Instead of focusing on degree of overlap between proxy advisors’ recommendations and asset managers’ votes, our findings suggest that the onus should firmly be placed on asset managers to vote in a manner which fosters a more responsible investment system and world. We conclude with recommendations for asset owners.

Findings

1. ISS are more supportive of environmental and social resolutions than the largest asset managers

The majority of asset managers in our study are less supportive of ESG issues than ISS, with the largest asset managers being the least supportive.

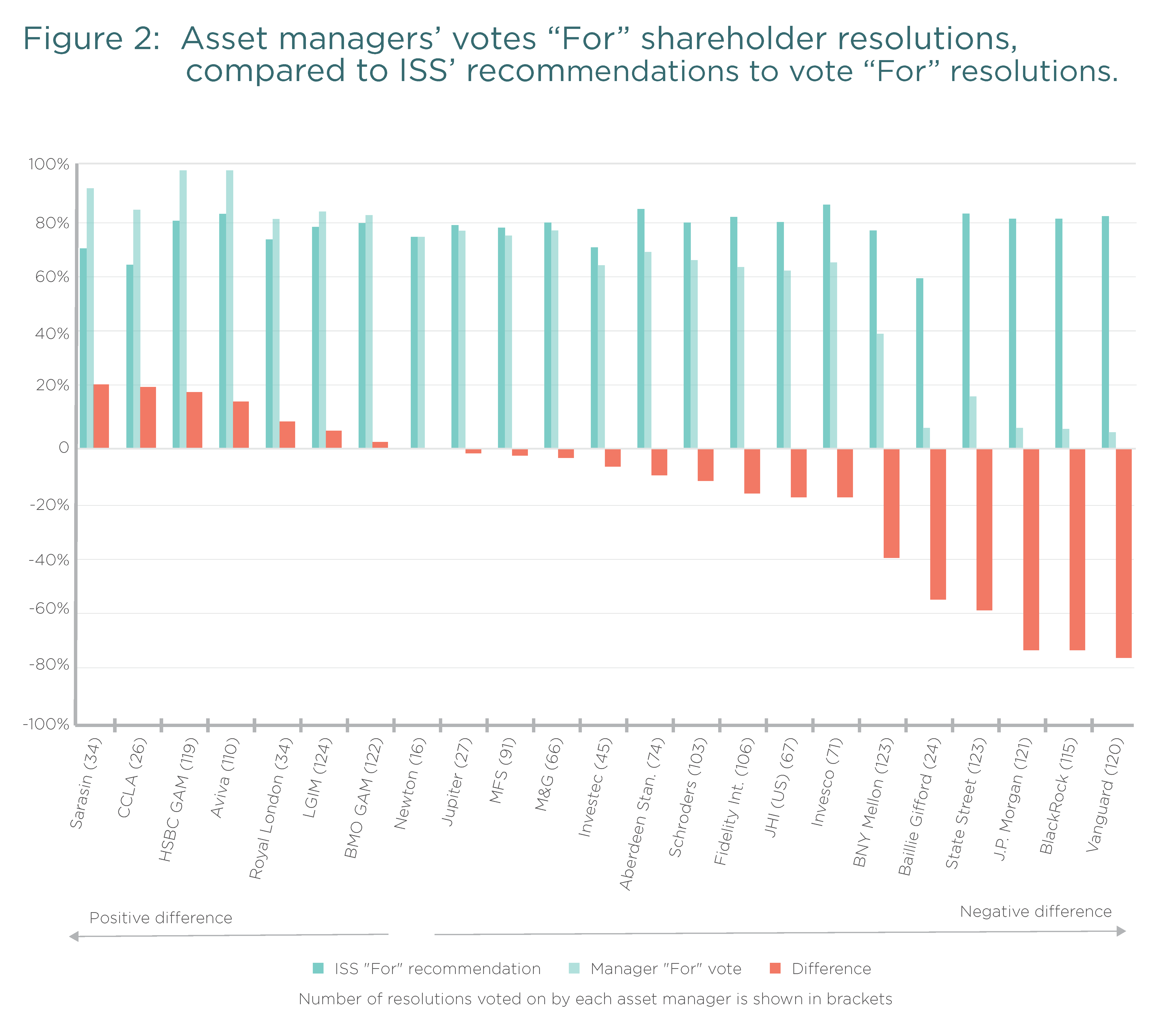

As shown in Figure 2, only 35% of asset managers voted “For” these resolutions more or equally often than they were recommended to, with 65% showing less support than their proxy advisor. This is concerning as it shows that asset managers, including those commonly used by charities, have implemented voting policies which are less progressive than ISS.

While it is positive that asset managers do not appear to be over-reliant on their proxy advisors, the bigger issue is many asset managers are not proactively supporting resolutions compelling companies to improve their ESG practices. In other words, asset managers routinely ignore the recommendations of their proxy advisor in order to vote down action on these important issues.

This is especially concerning when it comes to the ‘Big Three’ asset managers (BlackRock, Vanguard, and State Street) who collectively control an average of around 25% of the votes cast at S&P 500 firms. The direct power of these asset managers is at the upper end of the estimated scale of 13-30% indirect influence attributed to proxy advisors.

Strikingly, the largest asset managers fall overwhelmingly behind the level of support advised by ISS compared to the other managers in our sample (a similar trend is evident for Glass Lewis—see Figure 8 in Appendix of the complete publication). For instance, Vanguard supported only 6% of the 120 resolutions that they voted on, compared to ISS recommending support for 80% of the 120 resolutions. Likewise, BlackRock and J.P. Morgan only indicated support in 8% of their votes (115 and 121 resolutions respectively), compared to 79% by ISS.

For the other asset managers that do vote broadly in line with ISS, around half are more supportive of these resolutions than ISS, with the other half being less supportive. For example, Aviva Investors voted for these resolutions 96% of the time, compared to 84% support from ISS.

In contrast, Invesco showed support for 68% of their cases, while ISS indicated 85%, a shortfall of 17%. This 17% difference pales in comparison to the largest asset managers (State Street, J.P. Morgan, BlackRock, and Vanguard) who supported fewer than 25% of these resolutions, lagging behind ISS by a range of 58-74%. Notably, the five asset managers with the greatest negative difference compared to ISS also represent the majority of assets under management of our sample—a total of US $15.5 trillion, or 65%.

A focus on lobbying

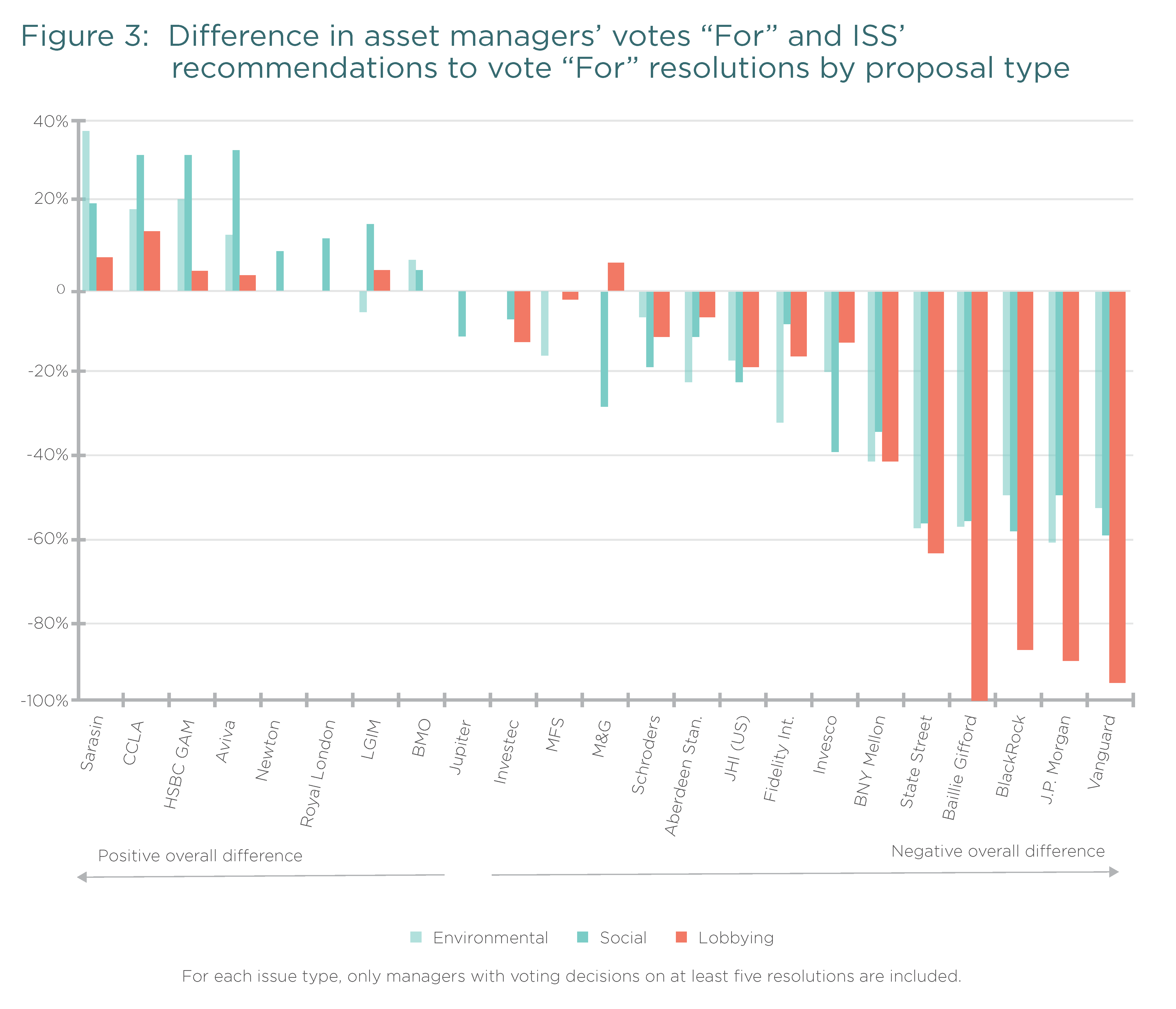

When we drill down into different thematic issues, an identical trend is evident: ISS indicates greater support for shareholder resolutions than most asset managers in our sample, with the largest players lagging by the greatest amount.

The most dramatic differences are evident for shareholder resolutions calling on firms to provide greater transparency on their political lobbying activities, as illustrated in Figure 3. Such reports provide crucial insights for investors into whether a company’s lobbying activities are aligned with their public statements on issues such as climate change. For example, many companies might publicly support the goals of the Paris agreement, yet be members of trade associations that lobby against progressive environmental policies. The majority of asset managers voted in support of these resolutions over 80% of the time, which was also consistent with the recommendations of ISS.

The outliers are notable. Vanguard Asset Management did not support lobbying transparency in any of their 58 votes, while BlackRock and J.P. Morgan supported it in less than 5% of their votes (Ballie Gifford only voted on five resolutions). These three firms lagged behind the level of support indicated by ISS by an average of 93% for lobbying resolutions compared to 53% for environmental and social issues. BNY Mellon and State Street also significantly lagged behind the level of support that ISS advised.

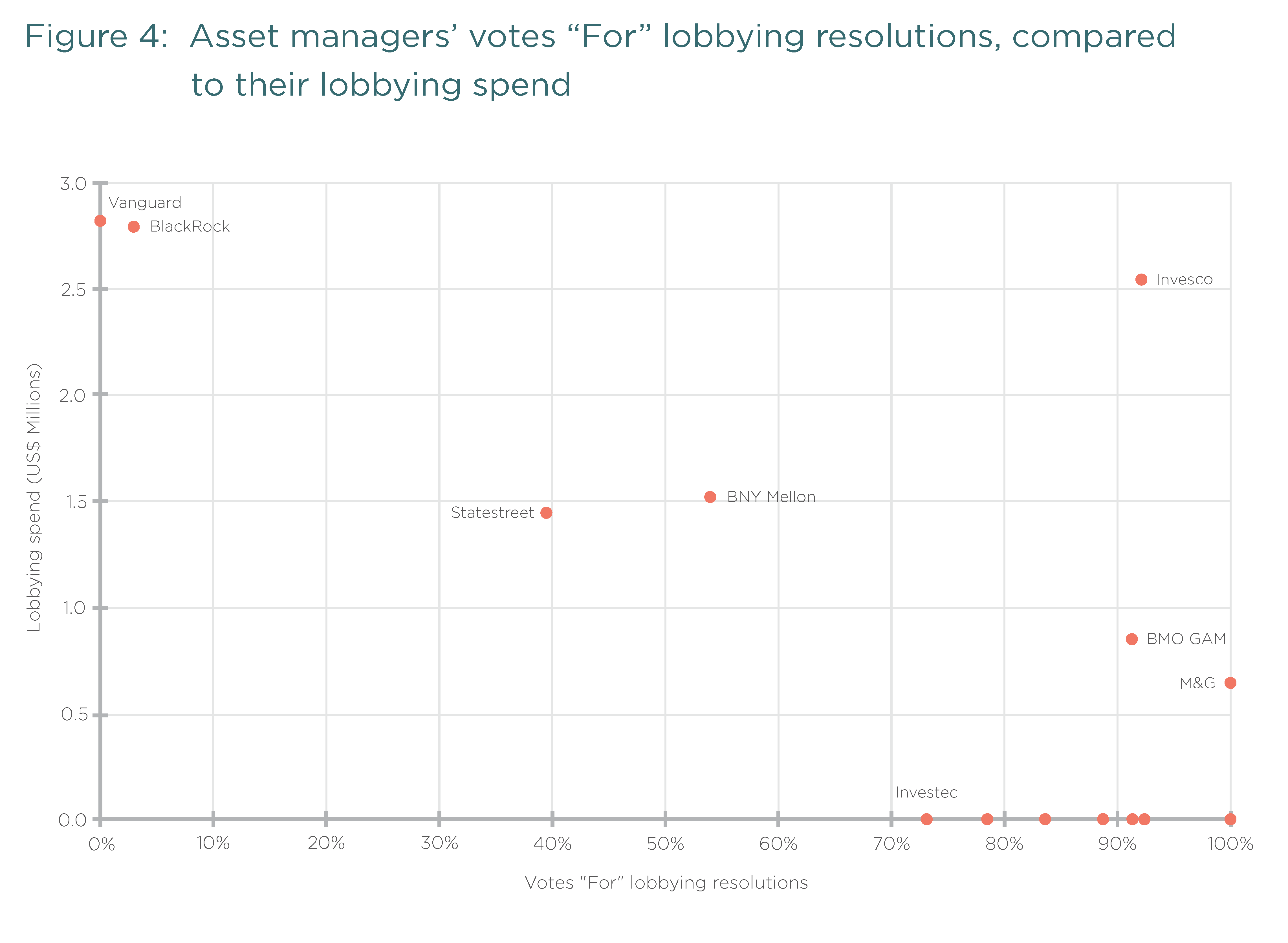

To understand this voting behaviour, we sourced data on asset managers’ lobbying spend in the US for the 2018 calendar year (the most recent data on investors’ lobbying spend publicly available). As shown in Figure 4, those asset managers who showed the least support for lobbying resolutions were themselves heavily engaged in political lobbying. This suggests one of two options. Firstly, that asset managers’ own lobbying practices may encourage (or at least not discourage) investee firms to participate in similar activities. Secondly, that asset managers who lobby don’t have a problem with the lobbying activities of their investee companies.

Interestingly, Invesco buck the general trend, as they engage heavily in lobbying but also voted in favour of greater transparency around investee firms’ lobbying activities. From this snapshot of data, it’s difficult to say much about why this is. With this exception, the evidence suggests that a significant influence on asset managers’ voting decisions could be their own practices and behaviours, rather than an overreliance on the recommendations of proxy advisors as is often claimed.

2. Little evidence to suggest a systematic overreliance on the recommendations of ISS for responsible investment resolutions

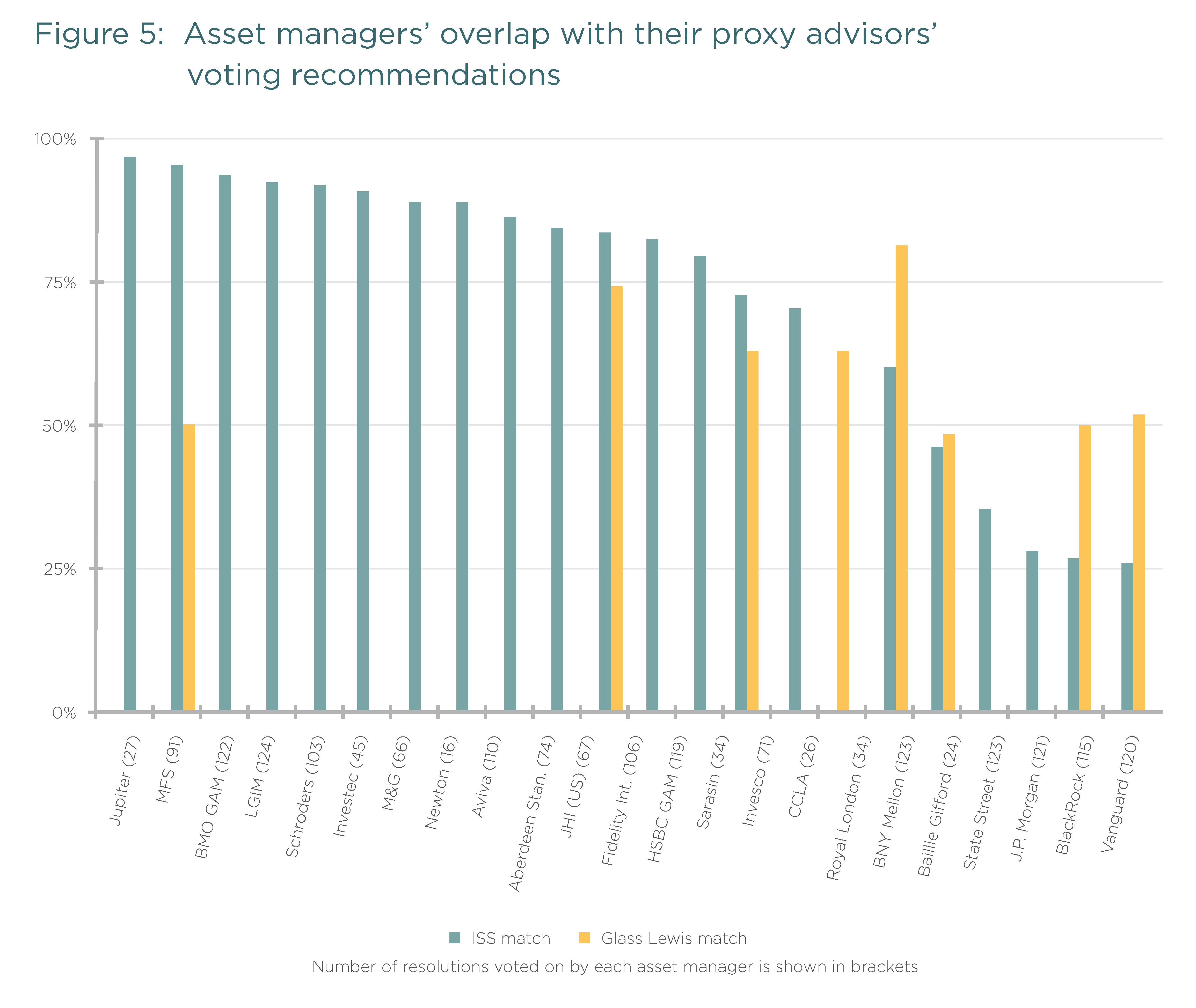

Asset managers invest in large numbers of companies, often numbering into the hundreds or thousands, which means that they face enormous monitoring challenges when voting on a range of issues including climate change, board diversity and executive remuneration. Proxy advisors can therefore act as a useful resource to help investors fulfill their obligation to vote in their clients’ best interests. However, a major concern raised by previous research on the role of proxy advisors relates to the potential overreliance of asset managers on proxy advisors’ recommendations, i.e. ‘sleepwalking’ their votes. As illustrated in Figure 5, our data supports this concern in part. The majority of asset managers in our sample (57%) have at least 80% overlap with the recommendations of ISS on these issues. Also, BNY Mellon have an 80% overlap with the recommendations of Glass Lewis, who they also use for proxy recommendations.

Asset managers who ‘sleepwalk’ their votes by blindly relying on the recommendations of proxy advisors risk accusations of outsourcing proxy voting—a key right of asset ownership—and hence their fiduciary duty, to proxy advisory firms.

Another implication from our data is that the largest asset managers (State Street, J.P. Morgan, BlackRock, and Vanguard) are not that reliant on their proxy advisors. This is consistent with studies, which have shown that larger and better resourced asset managers are more likely to deviate from the recommendations proxy advisors.

However, as established above, this is far from the whole story. The largest asset managers show a lack of support for the resolutions in our sample, while ISS is generally supportive.

While this could be interpreted as the largest asset managers not ‘blindly’ following the advice of proxy advisors, other factors could be at play. For instance, these asset managers could be underestimating environmental and social risk factors, or concerned about accusations of hypocrisy for their own practices (e.g. around lobbying, as explored above).

A focus on social reporting

To better gauge the extent to which proxy advisors recommendations influence asset managers’ voting decisions, we looked for categories of issues where ISS was relatively equally split between supporting and not supporting similar shareholder resolutions.

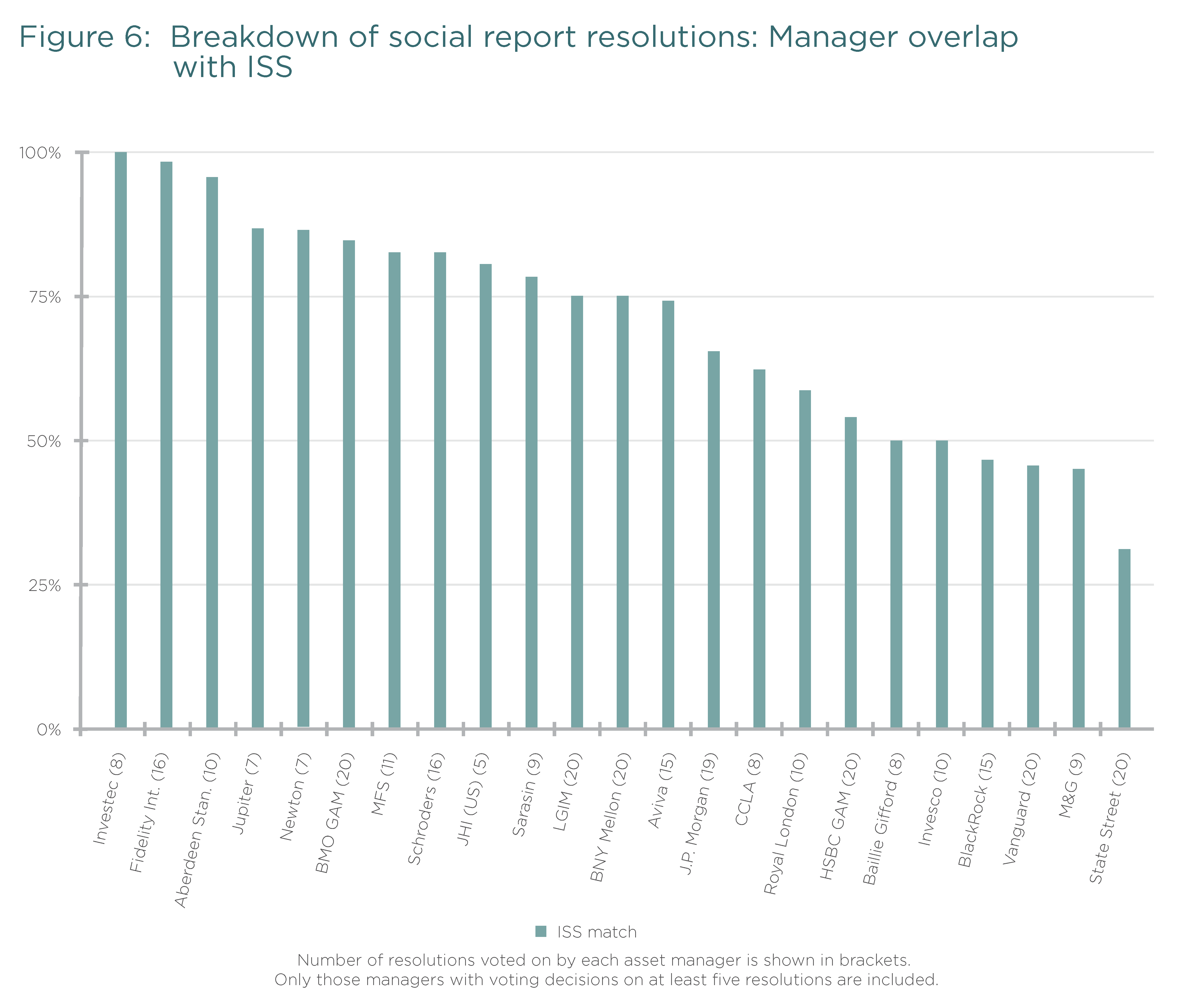

Across most sub-categories, ISS were generally quite consistent in the direction of their recommendations, either uniformly supporting or not supporting resolutions of a similar nature. The sub-category with the highest variation in recommendations was for resolutions asking firms to publish a report on a social issue. There were 20 of these resolutions in our sample, with ISS supporting 11 and not supporting nine.

Due to the low number of resolution types where there is both a high variance in ISS’ recommendations and a reasonable number of resolutions in a given year, our sample size here is small (20 resolutions), and even smaller in cases where managers only hold or voted on some of the resolutions. However, this overview nevertheless gives a sense of voting alignment with ISS by managers.

For this sub-sample of resolutions, we provide a breakdown of asset managers’ votes and their overlap with ISS in Figure 6. Only Investec voted consistently in alignment with ISS for both “For” and “Against” recommendations (on eight resolutions). Other asset managers with a high overlap on both “For” and “Against” votes included Fidelity International and Aberdeen Standard Life, each matching the ISS recommendation over 80% of the time. Our more significant

finding is that for the vast majority of asset managers, there is little evidence to suggest a systematic overreliance on the recommendations of ISS for these resolutions, and we see a more heterogeneous pattern of voting. This is consistent with claims that a majority of investors receive recommendations based on their own custom voting policies (including the asset managers in our sample).

3. ISS, the largest proxy advisor, is more likely to recommend investors support environmental and social shareholder resolutions than the second largest firm, Glass Lewis

Our analysis reveals differences between the voting recommendations of the two largest proxy advisors, ISS and Glass Lewis. In our sample, ISS recommended that investors vote “For” a shareholder resolution 79% of the time, which was much higher than the 53% of votes supported by Glass Lewis.

Given that ISS is estimated to have a 24 percentage point larger market share than Glass Lewis, this level of support is generally positive for fostering a financial system that takes into consideration environmental and social issues.

However, this still leaves 19% of responsible investment resolutions not supported by ISS (2% received an “Abstain” recommendation). These included resolutions calling for Facebook to report on how the firm governs content on its platform asking Coca-Cola to report on the impact of sugar in their products on consumers’ health outcomes, and a call for Exxon to report on risks of petrochemical operations in flood prone areas. For these resolutions 2.1%, 1.5% and 1.1% of issued share capital auto-voted with ISS respectively, according to data from Proxy Insight.

Turning to Glass Lewis, it is clear that Glass Lewis can do a significantly better job of promoting environmental and social considerations in their voting recommendations. As illustrated in Figure 7, Glass Lewis was much less supportive of environmental shareholder resolutions than ISS. Environmental resolutions Glass Lewis recommended against included asking Chevron to report on how the company could align itself with the Paris Agreement, and calling on Duke Energy to report on the public health impact of the company’s use of coal.

For social and lobbying resolutions, Glass Lewis were also less likely to issue a “For” recommendation compared to ISS.

As highlighted in the first part of this report on the role of proxy advisors, asset owners and managers can engage with and influence proxy advisors’ voting policy development through participating in surveys, roundtables and meetings. Proxy advisors seem to respond to the views of investor clients that participate in their external consultation mechanisms: In 2019, ISS updated their US, UK and continental Europe benchmark policies to generally recommend voting against the chair of the nominating committee at companies with no female directors. ISS highlighted that the policy was changed in response to 69% of investor respondents to their annual survey indicating they would consider it problematic if there were no female directors on a company board, showing strong preference for gender diverse boards.

Through these mechanisms, asset owners who are concerned about environmental, social and lobbying issues can emphasize their views to proxy advisors, or ask their asset manager(s) to do so on their behalf, so that recommendations on these issues may be changed in the future.

Conclusion

Our analysis shows that—for environmental, social and lobbying resolutions—the greatest concern is not whether asset managers are over reliant on their proxy advisors. Instead, the larger worry is that asset managers are routinely ignoring ISS’ recommendations to support social, environmental and lobbying resolutions and voting down action on these issues.

More strikingly, the largest managers overwhelmingly vote against these important issues. In fact, for these resolutions, asset owners who are concerned with environmental and social issues would probably prefer the largest asset managers to simply follow the recommendations of their proxy advisors! This is especially important for the, “Big Three”, asset managers (BlackRock, Vanguard Asset Management, and State Street Global Advisers) who collectively control an average of around 25% of the votes cast at S&P 500 firms. The direct power of the ‘big three’ asset managers is therefore at the upper end of the estimated 13-30% indirect influence attributed to proxy advisors.

Our analysis leads us to have three recommendations for asset owners concerned with asset manager voting on environmental, social and lobbying issues. These are especially important if your asset manager is routinely voting against shareholder resolutions that their proxy advisor is recommending they vote for.

- Ask your asset manager to vote to support all independent ESG resolutions, providing a published rationale to explain if any are not supported (‘comply or explain’ approach to voting).

- Ask your asset manager to demonstrate how they determine their proxy voting decisions on environmental, social and lobbying resolutions, and what inputs go into that decision, including the role of proxy

- Ask your asset manager how they reflect the expectations and demands made on companies in which they invest in their own boards and senior leadership. For example: How did they vote on lobbying resolutions in the last AGM season, and what do they spend on lobbying?

The complete publication, including footnotes and appendix, is available here.