Print

PrintRodolfo Araujo is Senior Managing Director and Head of the Corporate Governance & Activism Practice; Paul Massoud is Senior Managing Director of Corporate Governance & Activism; and Kosmas Papadopoulos is Senior Director at the Corporate Governance & Activism practice at FTI Consulting. This post is based on an FTI memorandum by Mr. Araujo, Mr. Massoud, Mr. Papadopoulos, and Rasmus Gerdeman.

The COVID-19 pandemic is having a profound economic impact across the globe. Entire industries have ground to a halt and unemployment claims reached record highs, as demand has disappeared due to government-mandated restrictions. Not surprisingly, equity markets are pricing in this turmoil, with the S&P 500 index losing one third of its value from February 19 to March 23. As of April 15, the S&P continues to be down by 18% from its February 19 peak. As the global public health and economic crises continue to unfold, companies should consider more than just the impact on operations. Valuations have declined significantly across the board, and the resulting market dislocation will likely bring a rise in contentious situations in mergers and acquisitions (M&A). This raises new challenges for boards and executive teams as companies are more vulnerable to potential attacks as compared to normal market conditions.

This is Different but Also the Same

While every major economic crisis is unique, there are also common characteristics that often repeat. Similar to 2008, the current downturn is characterized by a severe slowdown in economic activity, elevated unemployment, and financial market declines. Governments and central banks are attempting to offset the economic impacts through fiscal stimulus and monetary easing, but due to the ongoing global pandemic driving the downturn, there remains great uncertainty about the duration and the severity of the crisis.

In response to prior crises, companies have typically adopted a familiar playbook of responses, including more conservative capital allocation policies and M&A strategy. The current situation is no different in this aspect, as many companies wasted little time in announcing immediate plans to weather the storm by conserving resources through reduced capital expenditures and suspended capital return to shareholders in the form of dividends or buybacks.

While M&A activity is expected to decline during the coming months, a closer look at 2008 offers some important observations that we anticipate may carry over in the current environment.

A Closer Look at Transactions During the Great Financial Crisis of 2008

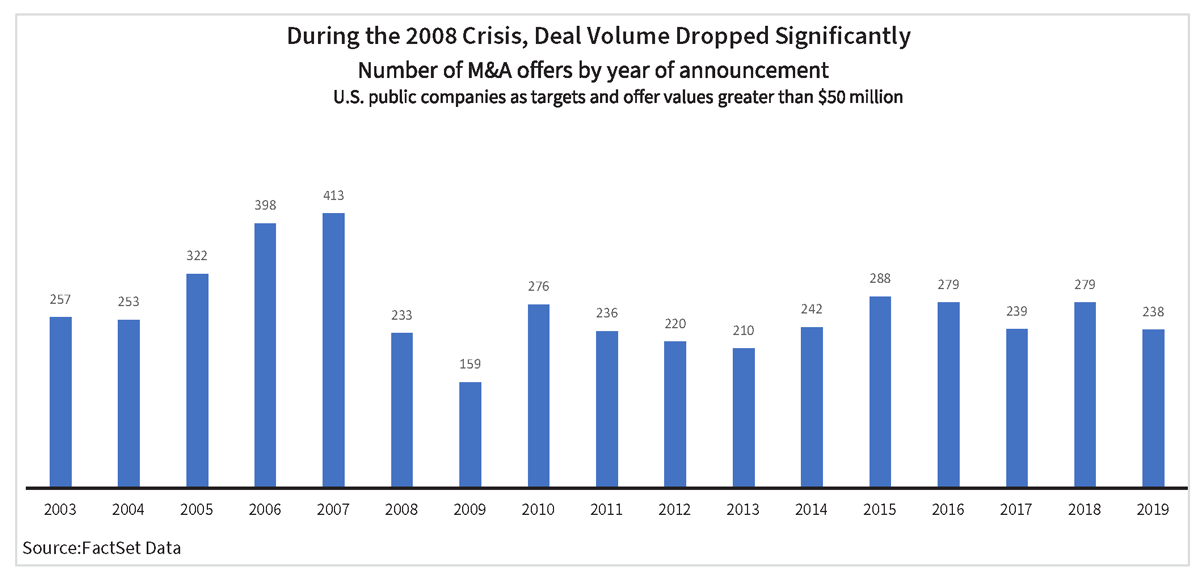

To identify patterns in M&A activity during the 2008 financial crisis, we reviewed proposed mergers and acquisitions from 2005 to 2019 with deal values of at least $50 million and U.S. public companies as targets. In our analysis, we found that the immediate impact of the credit crunch that culminated in the financial crisis was a wave of withdrawals by potential acquirers due to their inability to secure funding. As the credit crunch deepened, the number of announced deals almost halved in 2008 compared to 2007 and dropped even further as the recession took hold in 2009.

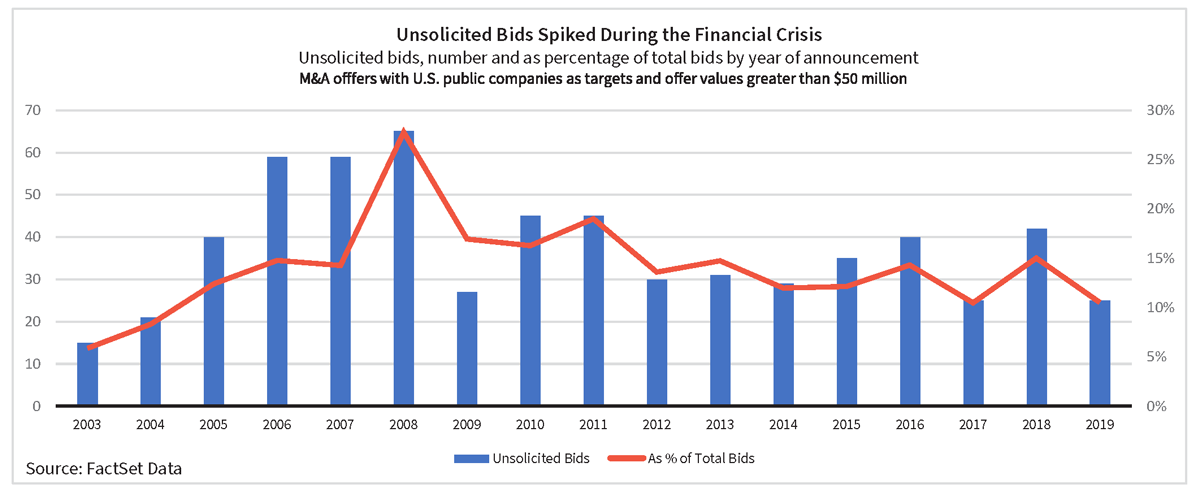

Declining deal volume is certainly no surprise. But a deeper look at the makeup of those transactions reveals a more nuanced and very important point. Because of the selloff in equities, depressed valuations created significant opportunities for buyers willing and able to take advantage of apparent bargains. As a result, despite the decline in aggregate deal volume, there was a material increase in unsolicited overtures, with a higher absolute number of bids for targets being made without prior discussions or negotiations. The percentage of unsolicited bids in 2008 peaked at 28% of all proposed transactions, as compared to 14% observed in 2007 and an average of approximately 11% over the previous five-year period. The percentage of unsolicited offers in 2009, while not at record levels, stood at 17%, significantly higher than the years preceding the market meltdown.

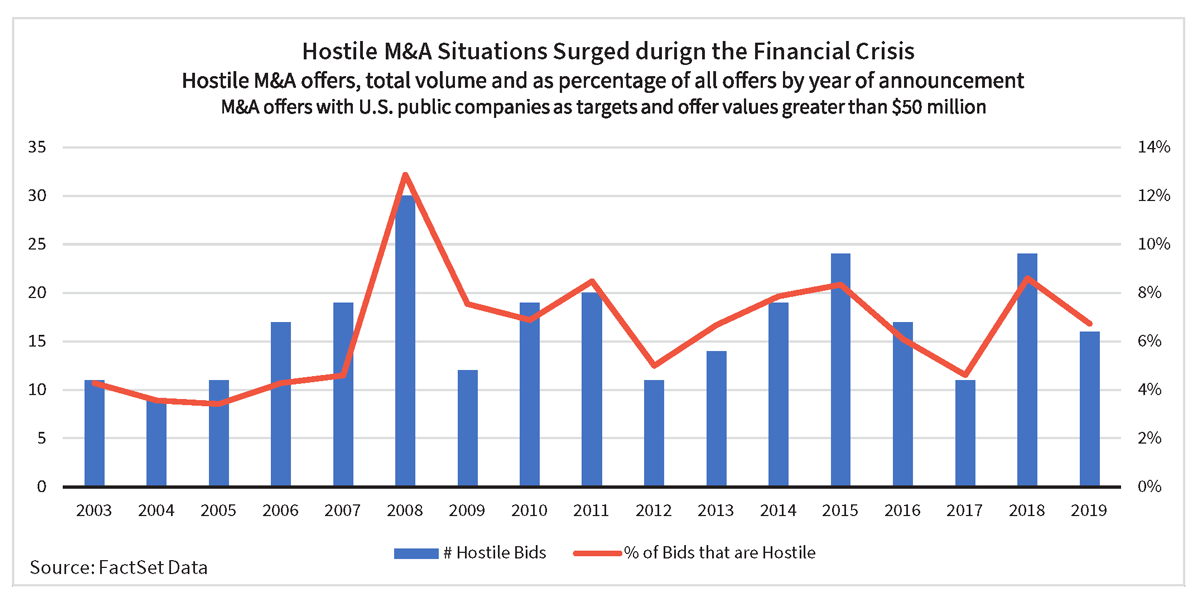

The spike in unsolicited overtures in 2008 corresponded with a sharp increase in hostile situations, with a record number of targets rejecting the initial proposed bids. The percentage of hostile M&A situations increased to 13% of offers in 2008, compared to only 5% in 2007.

Some Factors May Suggest an Increase in Unsolicited Offers

In addition to depressed valuations, companies are also more vulnerable today as a result of fewer active takeover defenses compared to twelve years ago. Only 3% of S&P 1500 companies have a poison pill in place today, [1] compared to 34% in 2008. [2] Over the last decade, companies have let shareholder rights plans expire in response to strong investor opposition to such measures. But given the decline in valuations, a spike in limited-duration poison pill introductions should come as no surprise. In fact, according to FactSet data, in the first quarter of 2020, 41 companies adopted or amended poison pills, compared to only 23 poison pill adoptions or amendments during the same period in 2019.

Another important factor is the amount of dry powder at private equity firms. Since 2008, global private equity cash reserves have ballooned to $1.5 trillion in 2019, an increase of nearly 50%, underscoring a significant source of capital for M&A.

Preparing for Unsolicited Overtures

Executives and directors of public companies must consider the impact of the ongoing crisis beyond near-term operational disruptions. As lower stock prices render public firms more vulnerable, companies should prepare for the possibility of an unsolicited bid by a peer or a private equity firm with a substantial war chest. We highlight three key action items.

Understand Your Company’s Value

A significant portion of the preparation for this market environment involves reviewing strategic alternatives, so that directors have a clear understanding of the intrinsic value of the enterprise. Companies should conduct this type of analysis proactively, so that they are not forced to prepare for a valuation discussion in reaction to an offer by a third party. Even if the board does not believe it needs to run a formal process, ongoing discussions among board members should take place to allow directors to reach consensus on what threshold should drive additional engagement following an unsolicited bid.

Assess Vulnerabilities and Develop a Response Strategy

Companies should also prepare for a potential unwanted approach by understanding the factors that make them vulnerable to such overtures. Beyond the financial incentive offered by a premium, shareholders may view the lack of a viable strategy or a reliable management team as good reasons to sell the company. In times of market dislocation, it is imperative for companies to proactively construct a narrative that addresses any identified weaknesses while highlighting the strengths of the business and the standalone case.

Engage with Your Shareholders

Effective and continuous engagement with shareholders is always a sound strategy, especially during times of uncertainty. A lack of engagement and communication about the long-term prospects of the standalone entity raises the risk of some shareholders being enticed by offers at a premium to the current stock price, even if the offer stands significantly below the company’s intrinsic value.

Advice to Acquirers

For companies with strong balance sheets that are considering acquisitions in the current environment, the threshold for perceived success will be set to a much higher standard, as investors and analysts more closely scrutinize transactions. While explaining the rationale, premium, and how a process developed is of great importance in normal circumstances, these tenants of M&A communications, along with proactive shareholder engagement, become vital during periods of market dislocation and volatility.

Communicate Your Capital Allocation Philosophy Well Ahead of an Acquisition

Investors don’t like to be surprised, especially when it comes to significant M&A events. Companies should be explicit about their capital allocation strategies when communicating with investors long before a significant acquisition is announced. A consistent message addressing how capital is allocated not only prepares investors for the possibility of an opportunistic acquisition but also instills in investors a sense of confidence that the board and management are effectively stewarding the company and its resources

Rationale Should Be About More Than Price

Over the last two decades, investor sentiment has soured on companies that operate several seemingly disparate businesses. In today’s environment, investors are increasingly requiring a coherent and compelling strategic rationale for an acquisition that goes beyond a target’s depressed valuation. Adequately addressing the strategic rationale and the synergies to be realized from the proposed transaction will drive stronger support from shareholders, inspire confidence in management and underscore the board’s commitment to efficient capital allocation and shareholder value creation.

Endnotes

1Source: FactSet Data(go back)

2Source: Institutional Shareholder Services, 2018, “U.S. Board Study: Board Accountability Practices Review,” https://www.issgovernance.com/library/board-accountability-practices-review(go back)