Print

PrintOfer Eldar is an Associate Professor of Law and Finance at the Duke University School of Law and Michael Wittry is Instructor of Finance at the Fisher College of Business at The Ohio State University. This post is based on their recent paper. Related research from the Program on Corporate Governance includes Toward a Constitutional Review of the Poison Pill by Lucian Bebchuk and Robert J. Jackson, Jr. (discussed on the Forum here).

The poison pill, arguably the most effective anti-takeover device, is making a comeback in the wake of the coronavirus (COVID-19) crisis. As the virus spread around the globe and through the United States in late February and early March of 2020, stock prices plummeted and market volatility dramatically increased. As a result of the ongoing crisis, many corporations have found themselves dealing with unprecedented challenges and disruptions. Companies whose operations have stalled, such as airlines and brick-and-mortar retailers, are likely to suffer from cash flow problems, potential defaults, and suppressed revenues. Moreover, intense market volatility means that stock prices may be depressed due to bad news which does not reflect underlying firm fundamentals or the true continuation value of the firm.

The sharp decline in stock prices makes corporations particularly vulnerable to takeovers and interventions by hedge fund activists. The large volume of funds accumulated in recent years by private equity firms and hedge fund investors, which have struggled in recent years to find attractive targets, further increases the likelihood of a potential acquisition wave that exploits the recent decline in firms’ market valuations.

In response to this development, a large number of corporations have moved quickly to adopt poison pills to protect themselves from possible acquisitions, even when there is no known bid for the shares of the firm. Since March 2, 2020, at least 45 firms have announced the adoption of poison pills. These companies include household names in a wide range of industries, including Occidental Petroleum, Groupon, Barnes & Noble, Hilton and Spirit Airlines. Until the emergence of COVID-19, the number of active poison pills in US corporations was extremely low. Although historically popular, particularly in the merger waves of the late 1980s and 1990s, poison pills have fallen out of favor in the last two decades, in large part due to the influence of proxy advisors; at the end of 2019, only 25 S&P 500 public firms had an active positive pill.

Whether poison pills have any impact on shareholder value remains subject to extensive debate. However, as shown in recent work by Catan (2019), firms tend to adopt poison pills following a decline in market valuations. Thus, the recent adoptions of poison pills in the midst of a crisis (although not previously explored) is broadly in line with the historical patterns.

Nonetheless, the COVID-19 pandemic has some features that create a unique opportunity to shed more light on the way poison pills are used and their potential impact. In particular, the crisis has had widely varying effects on different types of companies. Firms that belong to industries with high exposure to the crisis, such as airlines and entertainment, suffered from a sudden negative shock, which could make them more vulnerable to opportunistic takeovers or activist interventions. Consistent with this rationale, even proxy advisors, such as the ISS and Glass Lewis, have indicated recently that they understand the potential justifications for pill adoptions in the wake of the pandemic. On the other hand, other firms may be affected less severely, and some, such as online retailers, may even benefit from the crisis.

To examine the renewed adoption of poison pills, we started documenting their adoptions in real time. Using SDC data and news search, we document 45 firms announcing the adoption of poison pills between March 2 and April 21, 2020. We classify these firms broadly into groups with high and low-to-moderate exposure to the current crisis based on a recent Moody’s report on the pandemic from March 17, 2020 (see Figure 1). We manually classify each firm as belonging to the industries described by Moody’s based on its three-digit SIC code and its business description. These classifications are mostly straightforward with a few exceptions. For example, although Global Eagle Entertainment Inc. is classified as a telecommunication firm based on SIC code, we classify it as a high exposure firm because it primarily provides services to the airline industry.

Figure 1: Moody’s Classification of Industries Based on Exposure to the Crisis

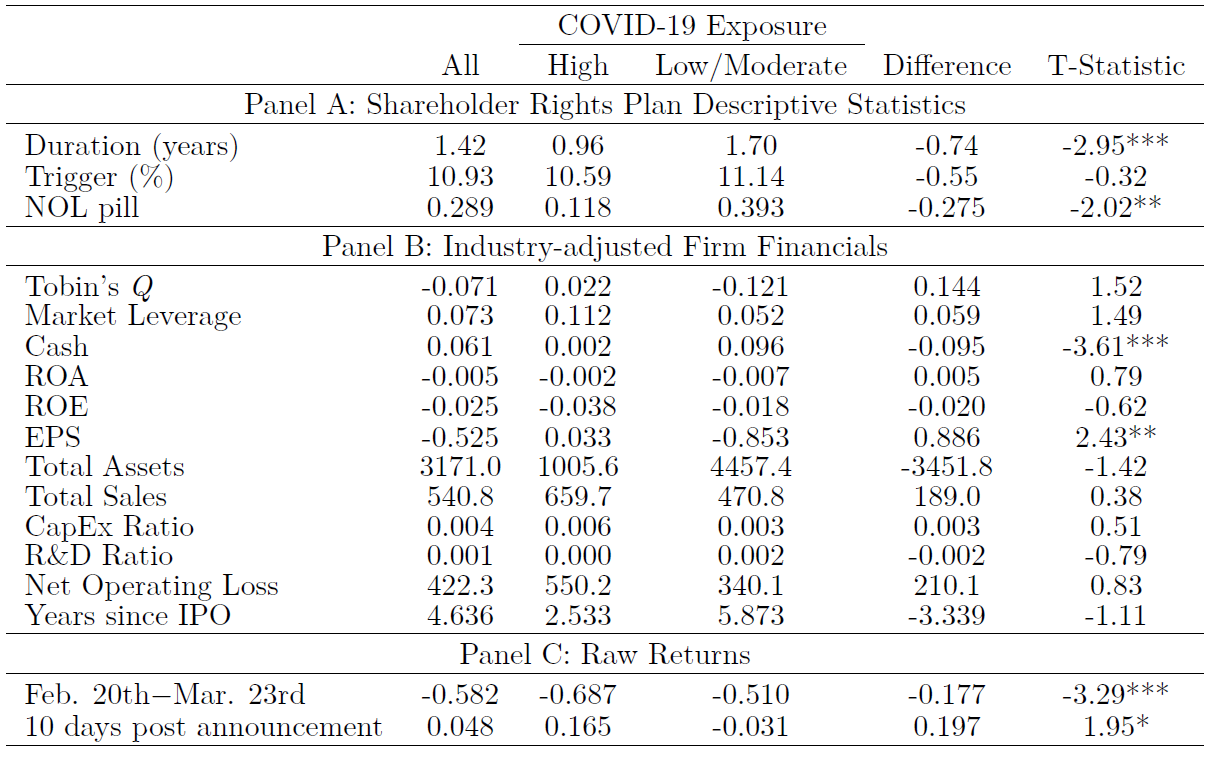

In table 1, we show industry-adjusted descriptive statistics for crisis pills. The interesting preliminary findings are from the comparison of high exposure to low-to-moderate exposure firms. First, the duration of pills of high exposure firms seems to be shorter on average by about nine months. Also, high exposure firms are much less likely to adopt poison pills in order to protect the net operating loss of the firm. Moreover, there are differences in the characteristics of adopting firms. The adopting firms in high exposure industries appear to have more leverage and lower cash, but also higher earnings per share, suggesting that these are firms whose business models are based on a large amount of debt but also revenues.

Table 1: Descriptive Statistics of Poison Pills and Adopting Firms

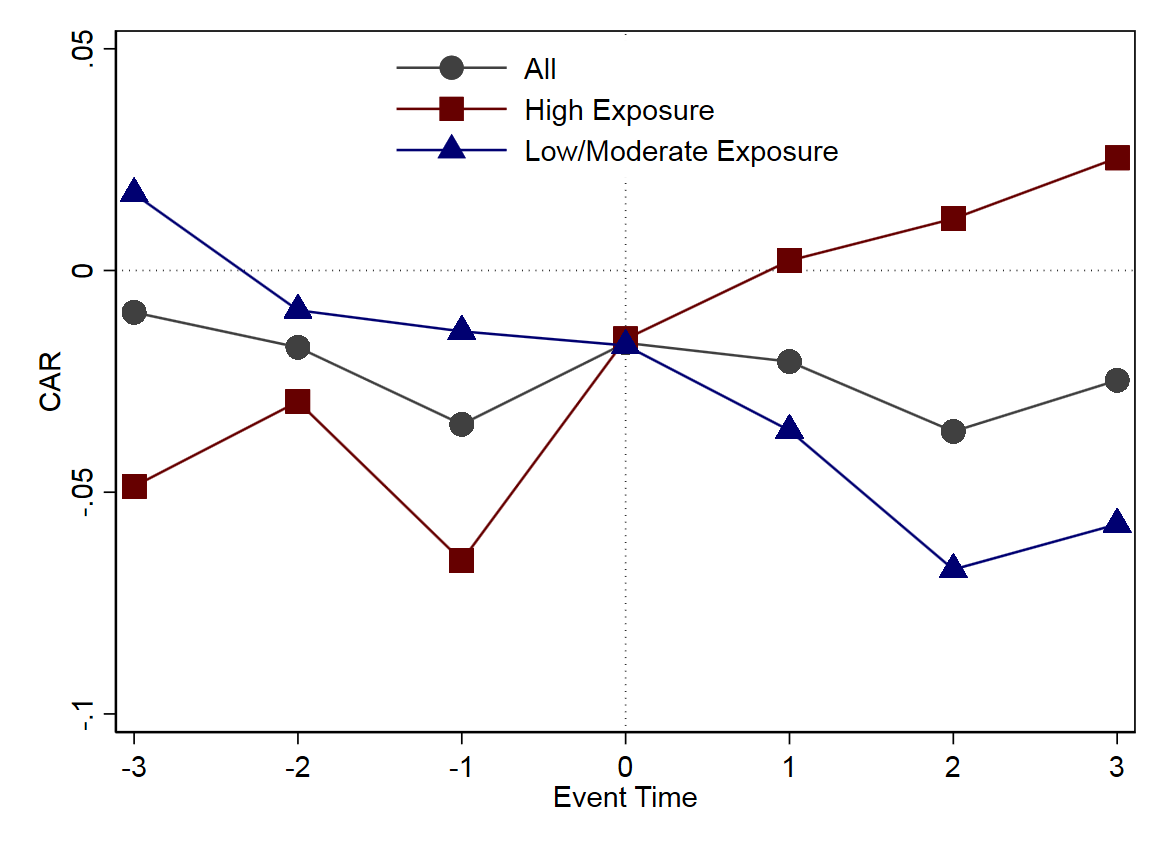

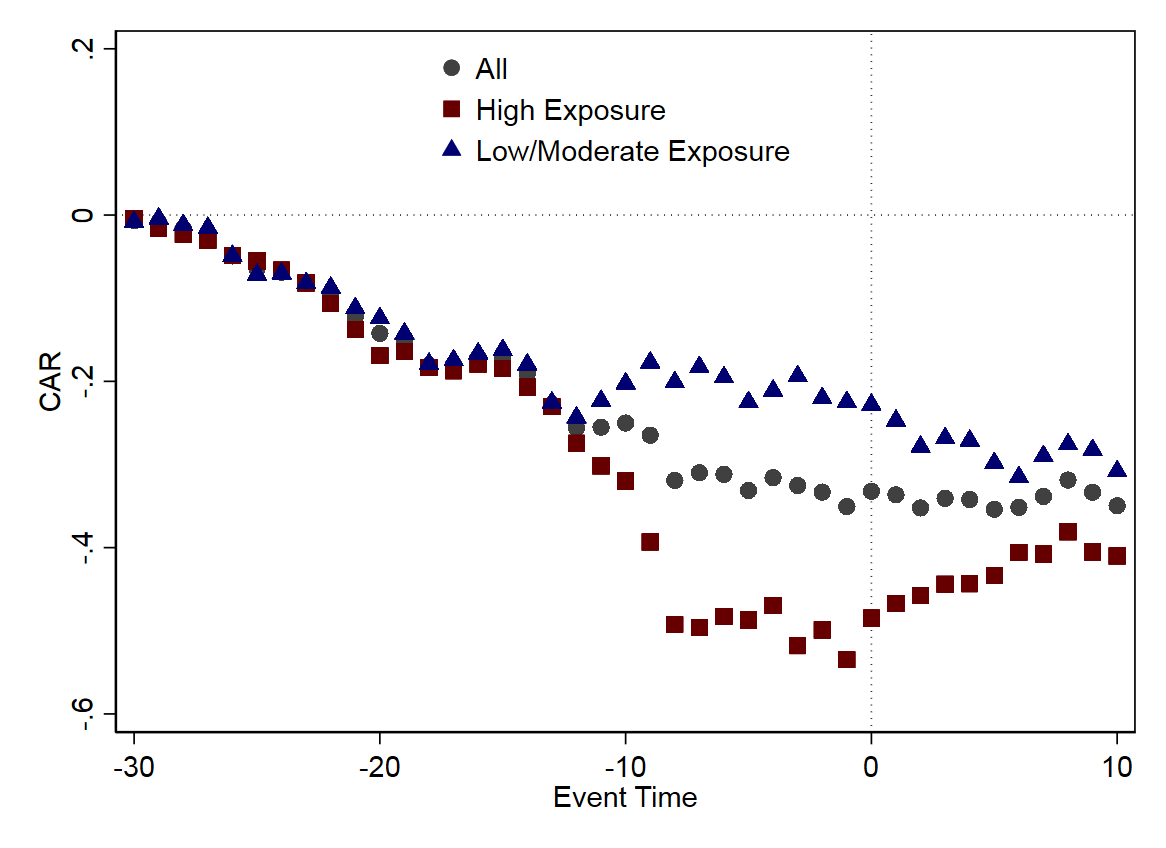

We also do an event study around the time of adoption. These are very preliminary findings as more firms continue to adopt poison pills every day, and the results are based on the market model using the S&P return as the market return (as the Fama-French portfolios are not yet available for April). We focus on two main event windows, [-3,+3] and [-30,+10], and we compute the cumulative abnormal returns for each day on these event windows. We show the results in Figures 2 and 3. As shown in the figures, the pattern for all adopting firms looks largely the same as those for historical pills reported in Catan (2019). That is, pill adoptions follow a decline in cumulative abnormal returns, but there is no meaningful stock price effect after their adoption.

The interesting results, however, relate again to the split samples between high exposure and low-to-moderate exposure firms. The high exposure firms adopt the pill following a much steeper decline in market value than the low-to-moderate exposure firms. Moreover, following adoption, the high exposure firms experience a dramatic positive stock price effect of 5% on the day of adoption and 12.8% after 10 days. In contrast, the low-to-moderate exposure firms experience a large negative stock price effect in most event windows. This suggests that the circumstances of adoption and the aftermath depend on the extent to which firms were affected by the crisis.

Figure 2: Cumulative Abnormal Returns in Event Window [-3,+3]

Figure 3: Cumulative Abnormal Returns in Event Window [-30,+10]

What can we learn from these very preliminary findings? Can poison pills mitigate the impact of financial crisis? Of course, we have to be careful in interpreting these preliminary results, which are based on a small sample. We cannot overrule the possibility that the stock prices are simply mean-reverting for firms that were hit harder in the first few weeks of the pandemic. However, it is also possible that the market views poison pills favorably when they are adopted by high exposure firms because they likely signal managers’ determination to stave off acquisitions that could exploit temporary negative shocks induced by the crisis. This is consistent with the signaling rationale for pill adoptions (Coates, 2000). These may be firms that have viable business models that are simply not well-suited for unexpected extreme conditions. On the other hand, it is possible that the firms in low-to-moderate exposure industries are more likely to be underperforming firms that benefited from a surge in stock prices in recent years, but are now being exposed by the crisis.

Does this mean that firms in high exposure industries should adopt poison pills? Obviously, pill adoptions are endogenous events, and thus we cannot attribute causal impact to their adoption. That is, these findings (even if they turn out to hold in larger samples as we update the data) do not imply that firms should adopt pills. Rather, they suggest that each pill should be evaluated based on the individual circumstances of the adopting firm, rather than on broad one-size-fits-all guidelines. It is possible that crisis conditions make it feasible to identify observable characteristics that make pill adoptions more conducive to shareholder value. We are continuing to explore this in a broader context of other crises, and will report as soon as possible.

The complete paper is available for download here.