Print

PrintAndrew G. Gordon is partner at Equilar, Inc.; David F. Larcker is the James Irvin Miller Professor of Accounting at Stanford Graduate School of Business; and Courtney Yu is Director of Research at Equilar, Inc. This post is based on a joint study by Equilar and Stanford University. Related research from the Program on Corporate Governance includes Paying for Long-Term Performance by Lucian Bebchuk and Jesse Fried (discussed on the Forum here).

We recently published a paper on SSRN, Sharing the Pain: How Did Boards Adjust CEO Pay in Response to COVID-19?, that examines how companies altered CEO compensation contracts and the payment of director fees in response to the COVD-19 pandemic.

CEO pay is routinely scrutinized for its size, structure, and relation to performance. Stakeholders want to know that CEOs are paid the correct amount, the structure of pay awards encourages the achievement of corporate objectives, and the amount ultimately realized is correlated with performance. Scrutiny is heightened during times of economic distress resulting from unexpected or exogenous forces. It is not clear how much pay CEOs should receive when corporate profitability suffers or how incentives should change to reflect an unforeseen decline in the operating environment. The issue of appropriate pay can gain extraordinary public attention when companies engage in cost-cutting actions, leading to layoffs, furloughs, or pay reductions for average employees who—like their bosses—did not cause the downturn.

In such times, the board must decide the correct course of action from an economic and societal perspective. On the one hand, the board might want to preserve the incentives offered to the CEO, recognizing that a decrease in pay punishes talented executives through no fault of their own and who have alternative career options with competitive firms. This viewpoint argues in favor of maintaining targeted compensation levels to the extent possible. The board might also award discretionary bonuses to make executives whole for missed bonus targets that have become unattainable, reprice or grant supplemental equity awards to compensate for lost value due to a declining stock price, or ease performance targets to preserve the value of outstanding long-term incentive programs (LTIPs).

On the other hand, maintaining or supplementing CEO pay while a company is laying off workers looks bad from a public perspective. The board and CEO might instead want to signal a willingness to “share the pain” by accepting a salary reduction, forgoing the annual bonus, or allowing long-term incentives to lapse without being fully achieved.

Related to this is the issue of whether a change in compensation is necessary or appropriate at all. All compensation arrangements have some element of risk embedded in their design. Sometimes a compensation award will not pay out, while other times it will substantially exceed original expectations. While negative exogenous events have a negative impact on performance, positive events can have an unexpected positive impact (so-called “pay for luck”). Rarely do we see a voluntary reduction in payout to reduce a windfall payout that was not really merited. Both positive and negative operating environments should be considered part of the risk imposed on executives.

The COVID-19 pandemic provides a unique opportunity to examine how the boards of U.S. public companies grappled with these issues during a system-wide economic slowdown. In contrast to previous recessions, including the 2008 financial crisis, CEOs are not accused of causing the current downturn, nor is the fallout attributed to faulty strategic decisions proposed by management and approved by the board. Instead, corporate executives have had to respond to an economic shutdown imposed on them by outside forces—with employees, shareholders, and other stakeholders bearing the cost.

How did companies respond? How many elected to modify CEO pay, and how many left it unchanged? What were the characteristics of companies that altered pay? Did the CEOs of these companies “share the pain” through salary reductions and forfeited bonuses, or did they receive adjustments to insulate them from lost value?

Prevalence of CEO/Director Pay Actions

To answer these questions, we examined the Forms 8-K and DEF-14A compensation disclosures of all companies in the Russell 3000 between January 1 and June 30, 2020, using data provided by Equilar.

We found that 502 companies (17 percent) made adjustments to CEO salary, bonus, or long-term incentive programs (LTIPs), or director fees during this measurement period.

The first SEC disclosure of a compensation change was filed by United Airlines on March 10:

Effective immediately, Oscar Munoz, the Company’s Chief Executive Officer and Scott Kirby, the Company’s President, are forgoing 100 percent of each of their respective base salaries through at least June 30, 2020.

Not to be outdone, Alaska Airlines was the second company to file such disclosure, announcing six days later that its chairman and president also agreed to reduce their salaries to zero. Alaska included the salary forfeitures among a long list of corporate actions to mitigate the impact of COVID-19 on its business, including 10 percent and 15 percent capacity reductions in April and May, respectively, additional borrowings to increase liquidity, a halt to nonessential capital spending, suspended share repurchases, a hiring freeze, and unpaid leaves of absences to employees for 30-, 60- and 90-day time frames. These actions were significantly escalated ten days later.

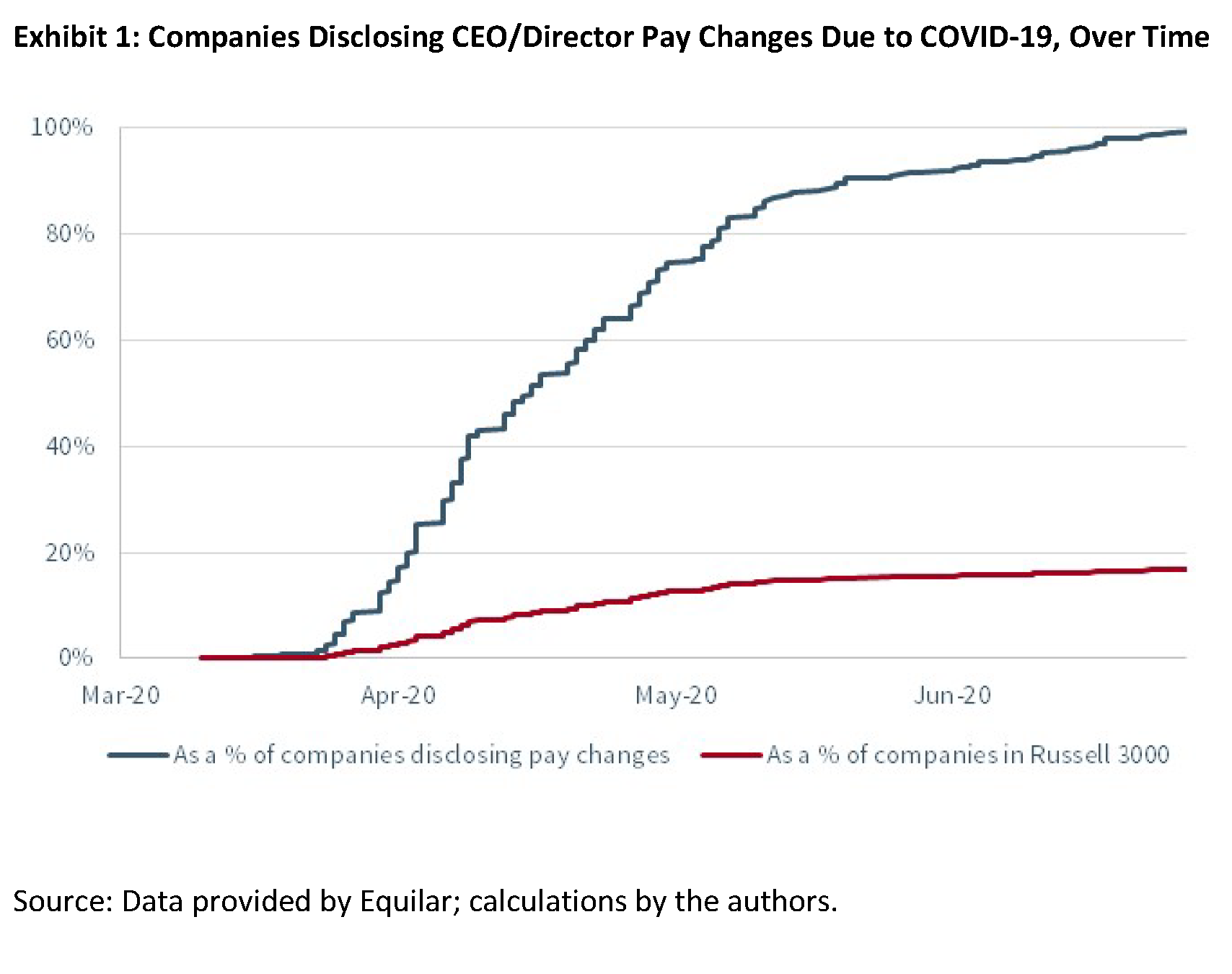

Other public companies announced pay actions in March, but the largest number were disclosed in April. By the end of March, only 14 percent of the companies that would eventually announce pay changes (by June 30, 2020) had done so. By the end of April, 73 percent had (see Exhibit 1).

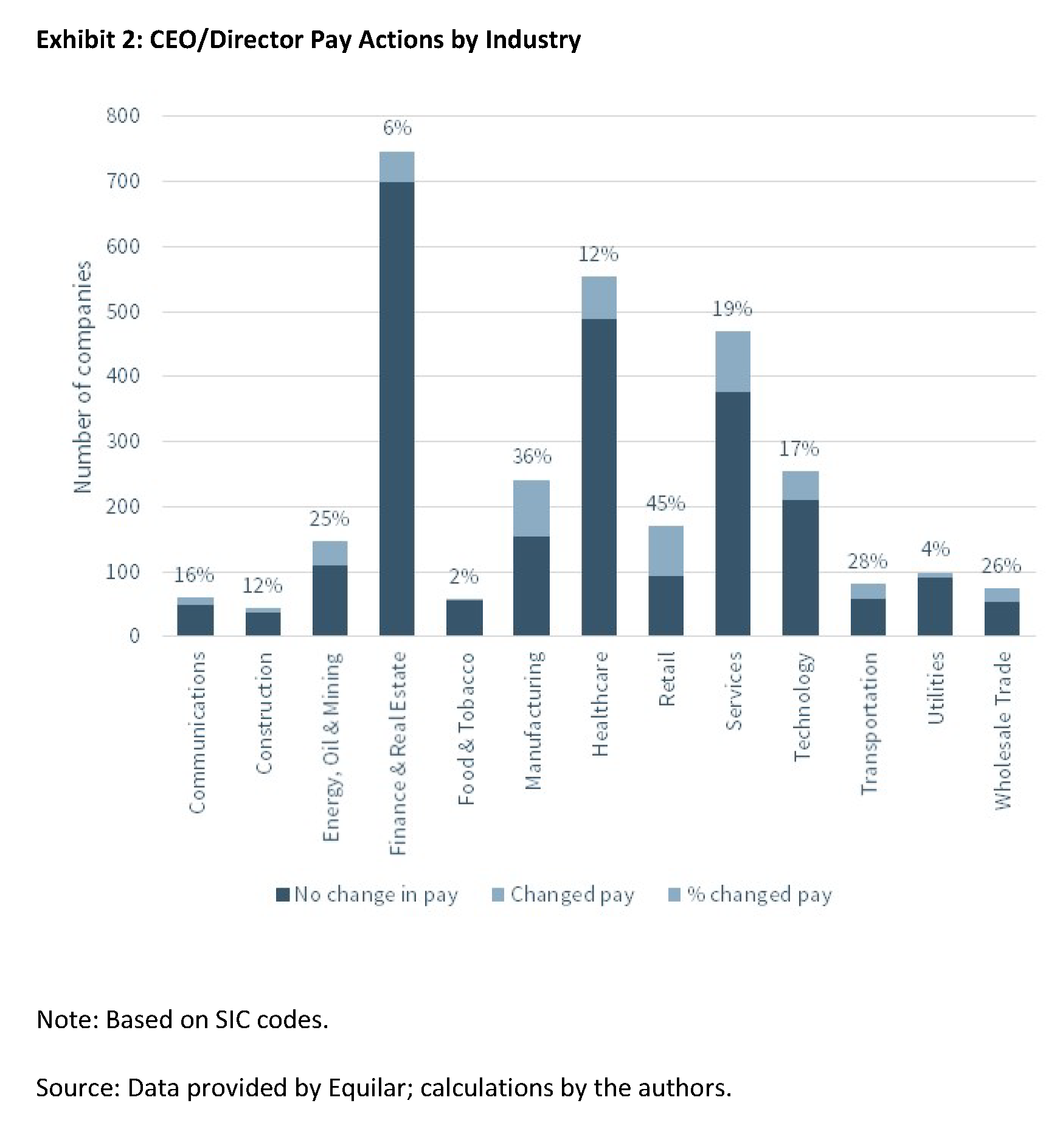

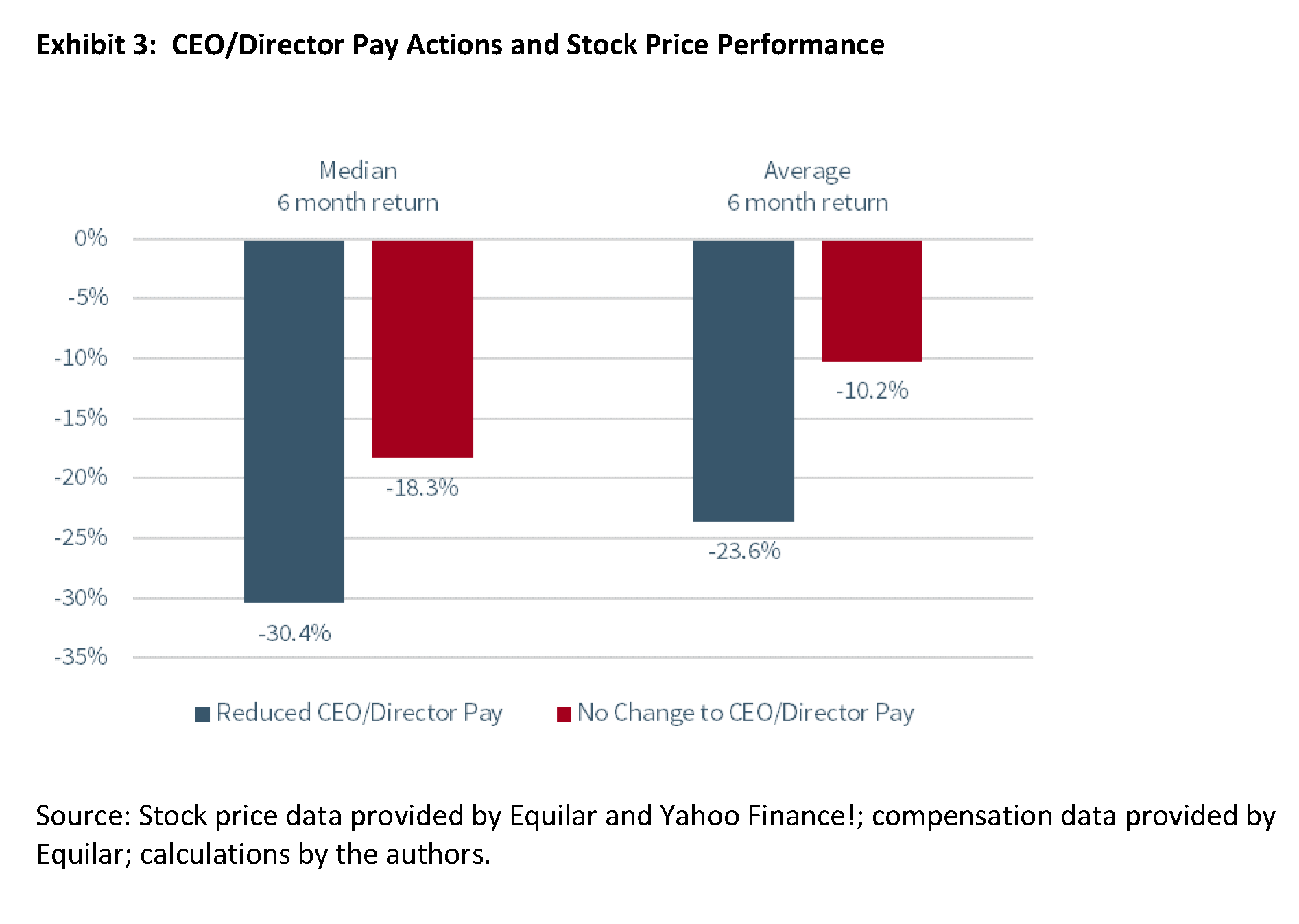

Industry and performance. In terms of industry concentration, retail (45 percent), manufacturing (36 percent), and transportation companies (which include airlines, 28 percent) were among the most likely to make CEO/director pay adjustments. Food and tobacco (2 percent) and utilities (4 percent) were among the least likely (Exhibit 2). Not surprisingly, companies that made CEO/director pay adjustments were among the hardest hit in terms of stock price performance. These companies exhibited an average (median) stock price decline of 23.6 percent (30.4 percent) over the six months ending June 30, compared with an average (median) stock price decline of 10.2 percent (18.3 percent) for companies that did not reduce CEO/director pay (see Exhibit 3).

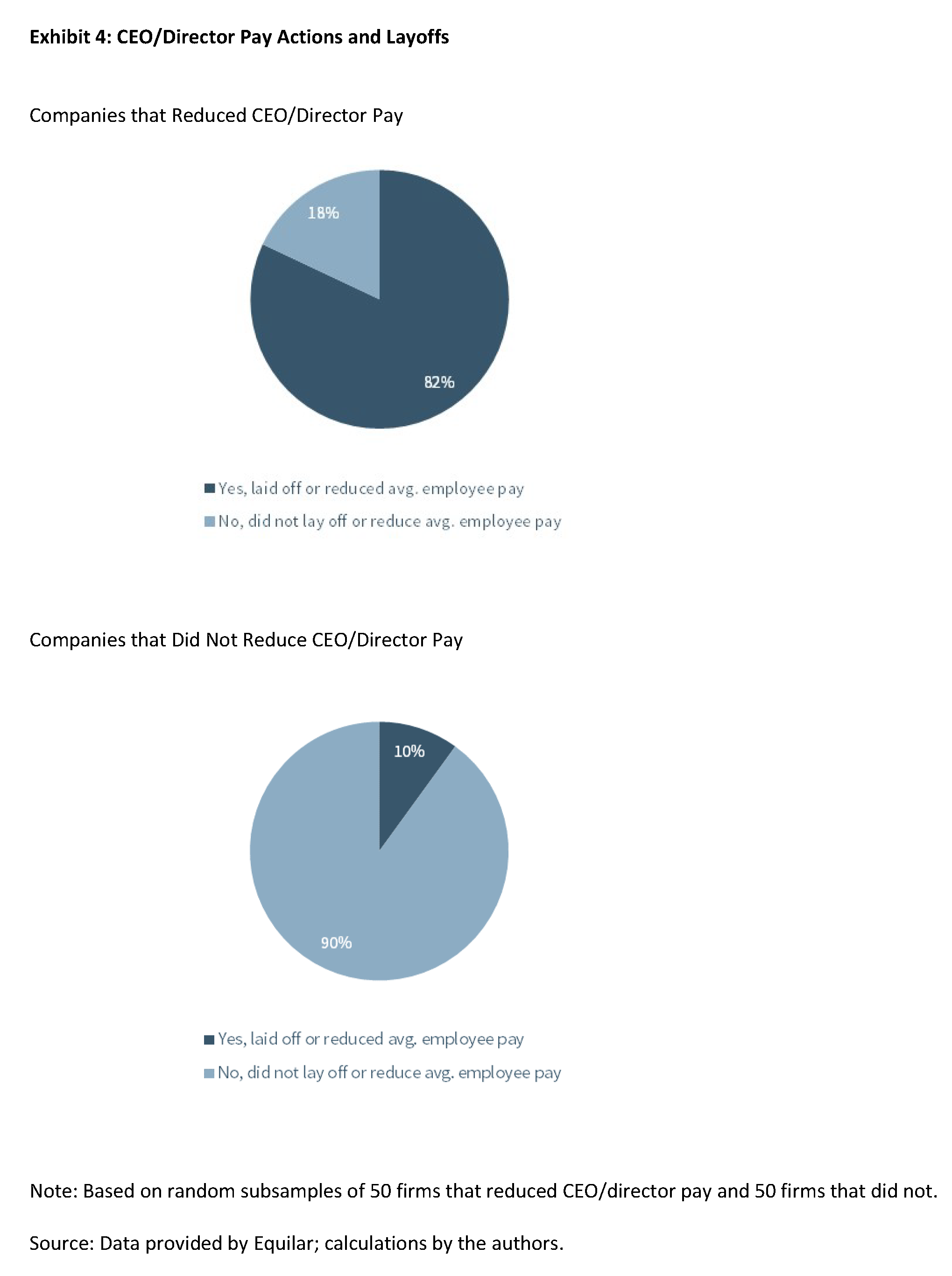

Layoffs. Companies that made CEO/director pay changes were much more likely to engage in layoffs and employee cost reductions. Based on two random subsamples of 50 firms, we found that 82 percent of companies that took CEO/director pay actions also reduced workforce costs through layoffs, furloughs, or salary reductions. (As with the examples of United Airlines and Alaska Airlines, these announcements were often made simultaneously.) By contrast, only 10 percent of companies that left CEO/director pay unchanged announced layoffs (see Exhibit 4).

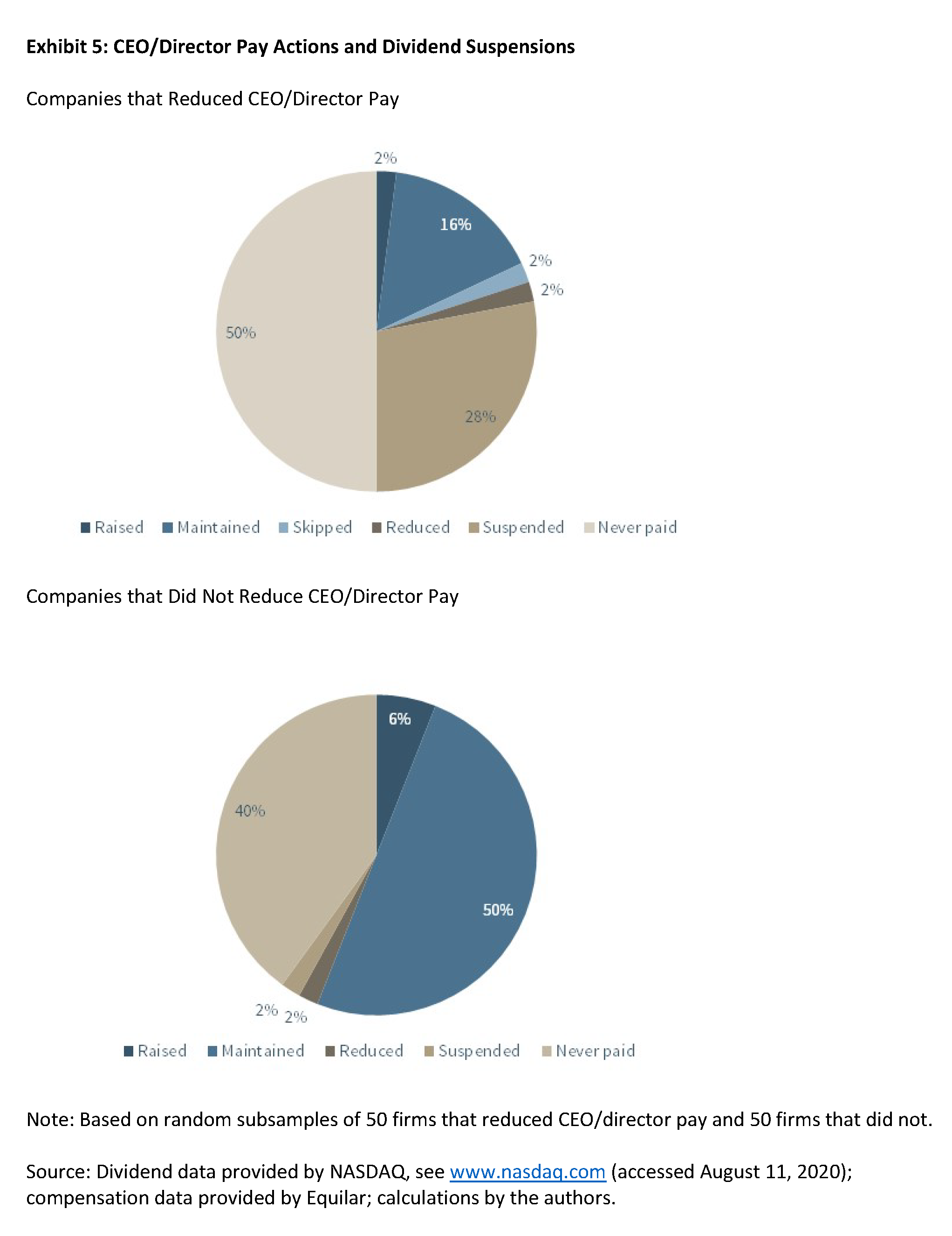

Dividends. Companies that took CEO/director pay actions were also more likely to curtail or eliminate their dividend. Based on the same 50 firm subsamples, we found that 32 percent of companies that modified CEO/director pay reduced, skipped, or suspended their dividend; 18 percent maintained or raised it. (50 percent of these firms did not have a history of paying regular dividends.) By contrast, only 4 percent of companies that did not modify CEO/director pay reduced or suspended their dividend, while 56 percent maintained or raised it. (40 percent did not have a history of making dividend payments. See Exhibit 5.)

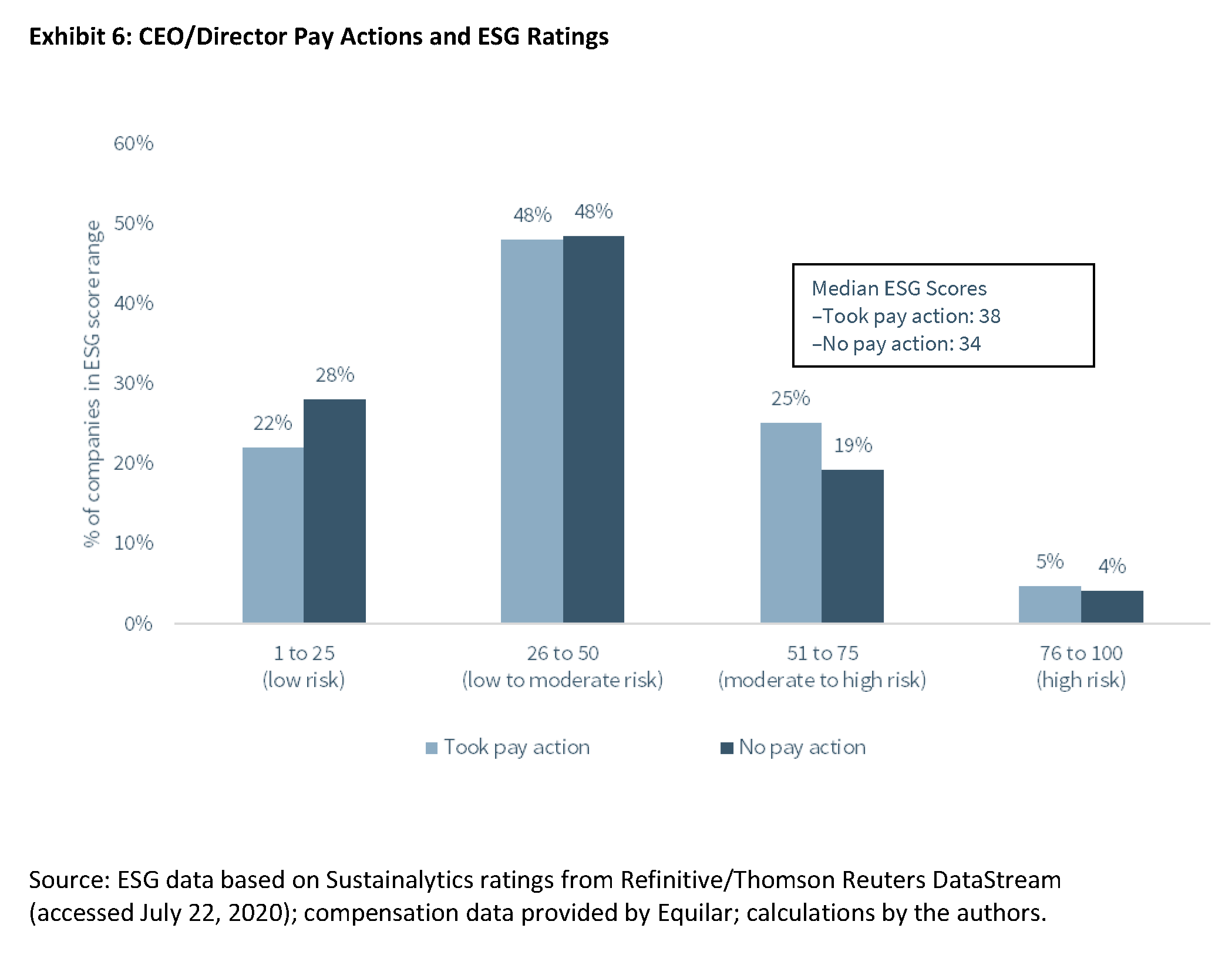

ESG Ratings. Surprisingly, CEO/director pay actions appear to have little relation to ESG (environmental, social, and governance) ratings for our sample of companies. Using ratings from Sustainalytics, we found that the median ESG rating of companies taking CEO/director pay actions was not significantly different from the median rating of companies that left pay unchanged (38 versus 34, respectively, with a rating of 1 indicating low ESG risk and a rating of 100 indicating high ESG risk—see Exhibit 6).

To explore this further, we regressed the probability of observing a CEO/director pay action on ESG rating, controlling for stock-price performance and industry. We found that an increase in ESG risk is associated with a higher probability of CEO/directors taking a pay reduction. That is, companies with better ESG scores are less likely to make compensation changes, even when economic performance is held constant. This finding is unexpected. We would expect CEOs and directors of companies that truly value ESG to be more (not less) likely to reduce their pay during times of economic stress, but this is not what we found. This suggests either that firms with better ESG scores are less likely to reduce pay or that ESG scores do not accurately predict compensation actions (an element of social behavior or “S”).

Analysis of CEO/Director Pay Actions

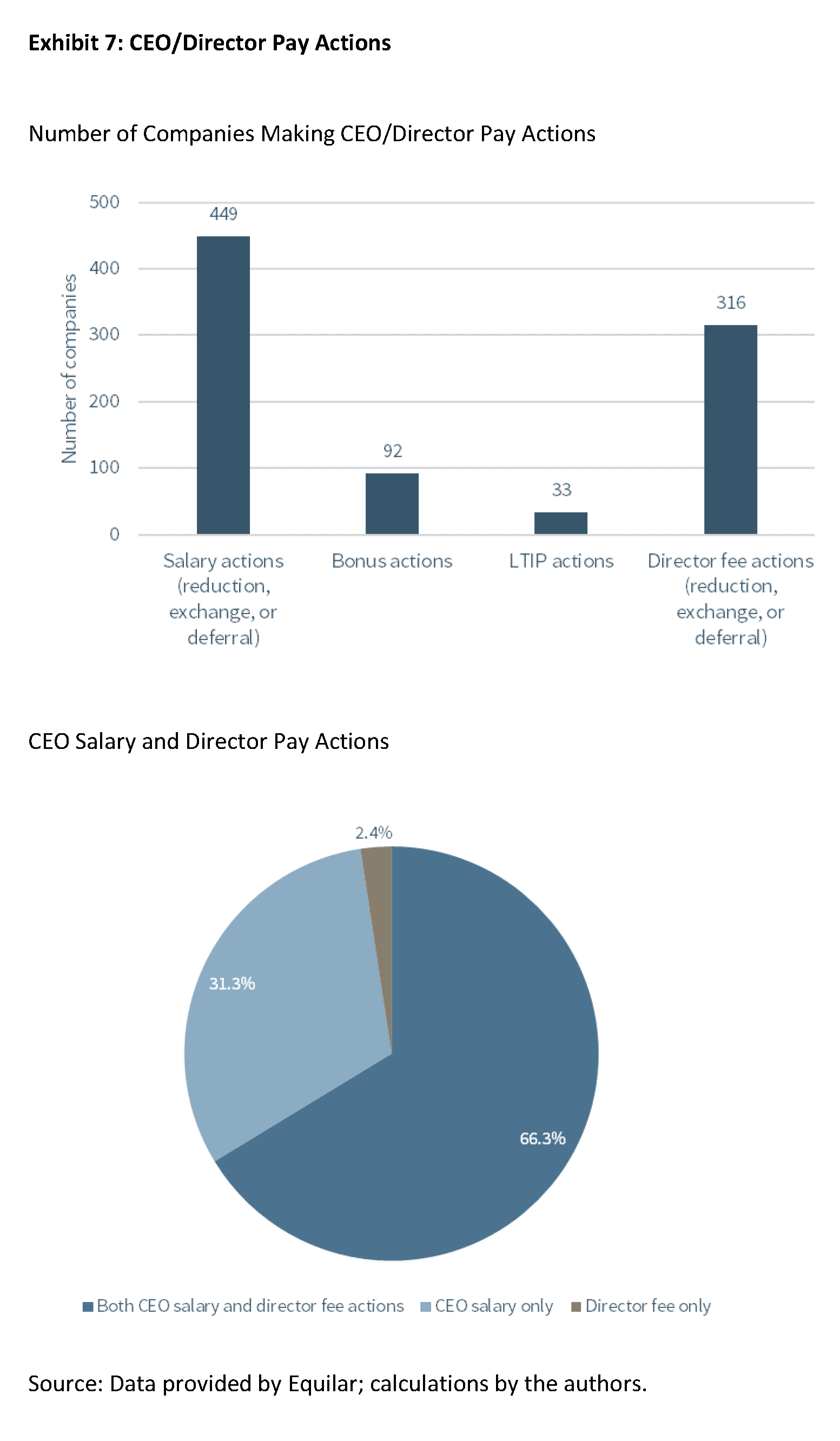

The vast majority of pay alterations were made to CEO salaries (449 companies) and to director fees (316 companies). To a lesser extent, they were made to annual bonuses (92 companies) and long-term incentive programs (33 companies). Most companies that altered director fees did so alongside a CEO salary change; rarely did a company alter director fees without reducing CEO salary (see Exhibit 7).

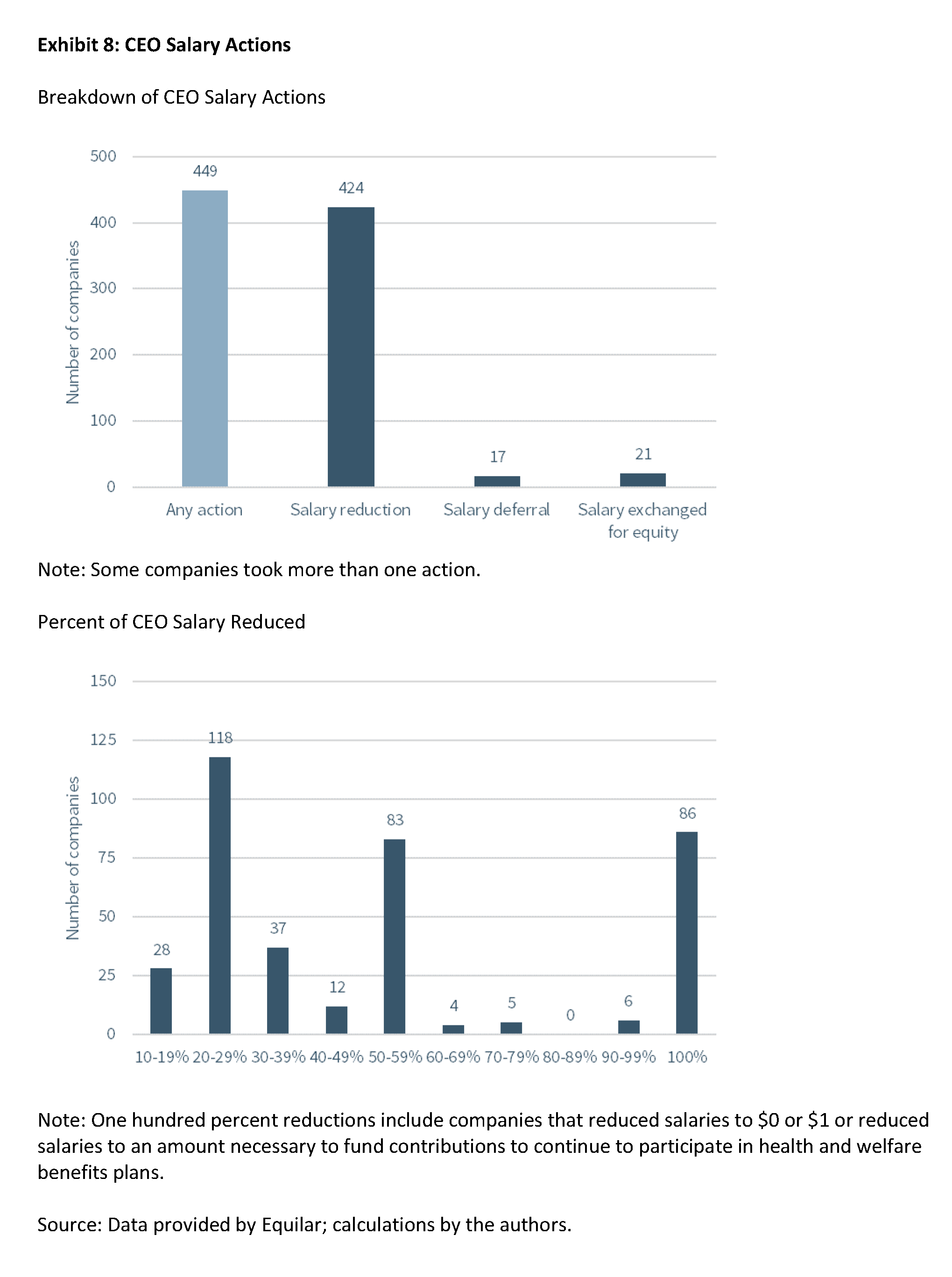

CEO salary actions. Companies that altered CEO salaries did so in at least one of three ways. The vast majority reduced the salary rate (424 companies). The remainder either deferred salary payments (17 companies) or required/offered an exchange of salary for equity (21 companies). A few companies took more than one action, such as reducing salary and paying it in equity. For example, Ford Motor elected to defer 50 percent of CEO salary through September 2020. Flotek Industries (an equipment manufacturer in the energy and chemical industries) approved a voluntary exchange of salary for restricted stock with the stock valued at a 20 percent discount to the CEO’s previous annual salary. Commodity producer Freeport-McMoRan reduced its CEO’s salary by 25 percent with 90 percent of the reduced amount payable in stock and the remaining 10 percent in cash.

Among those that reduced salary, the average reduction was approximately 50 percent. However, there was considerable dispersion around this average, with reductions as little as 10 percent and as high as 100 percent (see Exhibit 8).

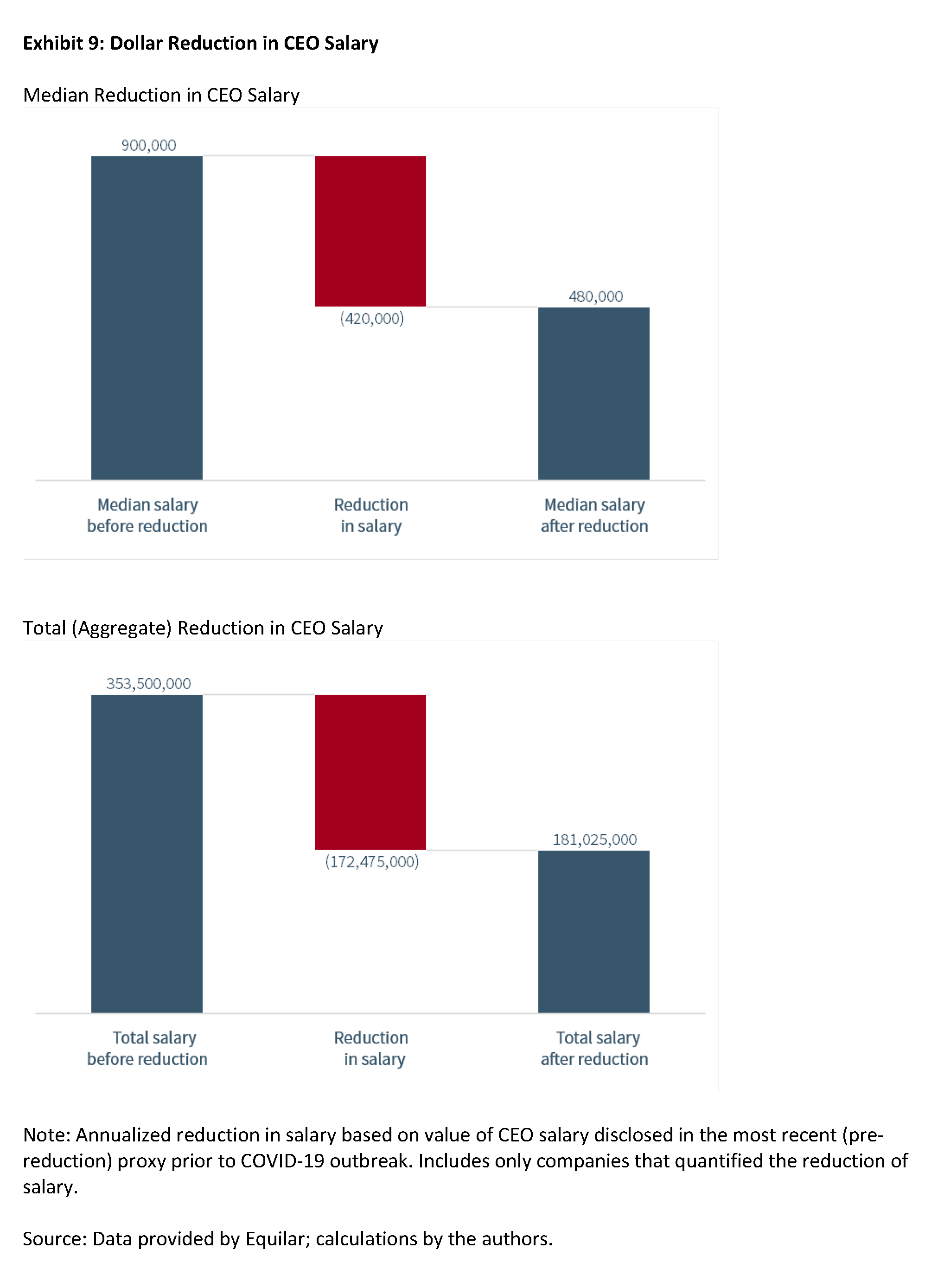

In terms of dollar amounts, the typical CEO had a median pre-COVID-19 salary of $900,000 (out of a total compensation of $5.5 million reported in the proxy statement). Following salary reduction, the median CEO salary declined to $480,000. This constituted a 47 percent decline in salary, but only an 8 percent decline in total targeted compensation. (However, as we will examine later, the total wealth lost by CEOs was much greater because of stock price declines.) Taking into account the entire population of companies that reduced pay, aggregate annual CEO salary declined from $353.5 million pre-COVID-19 to $181.0 million as a result of COVID-19—a $172.5 million reduction (see Exhibit 9).

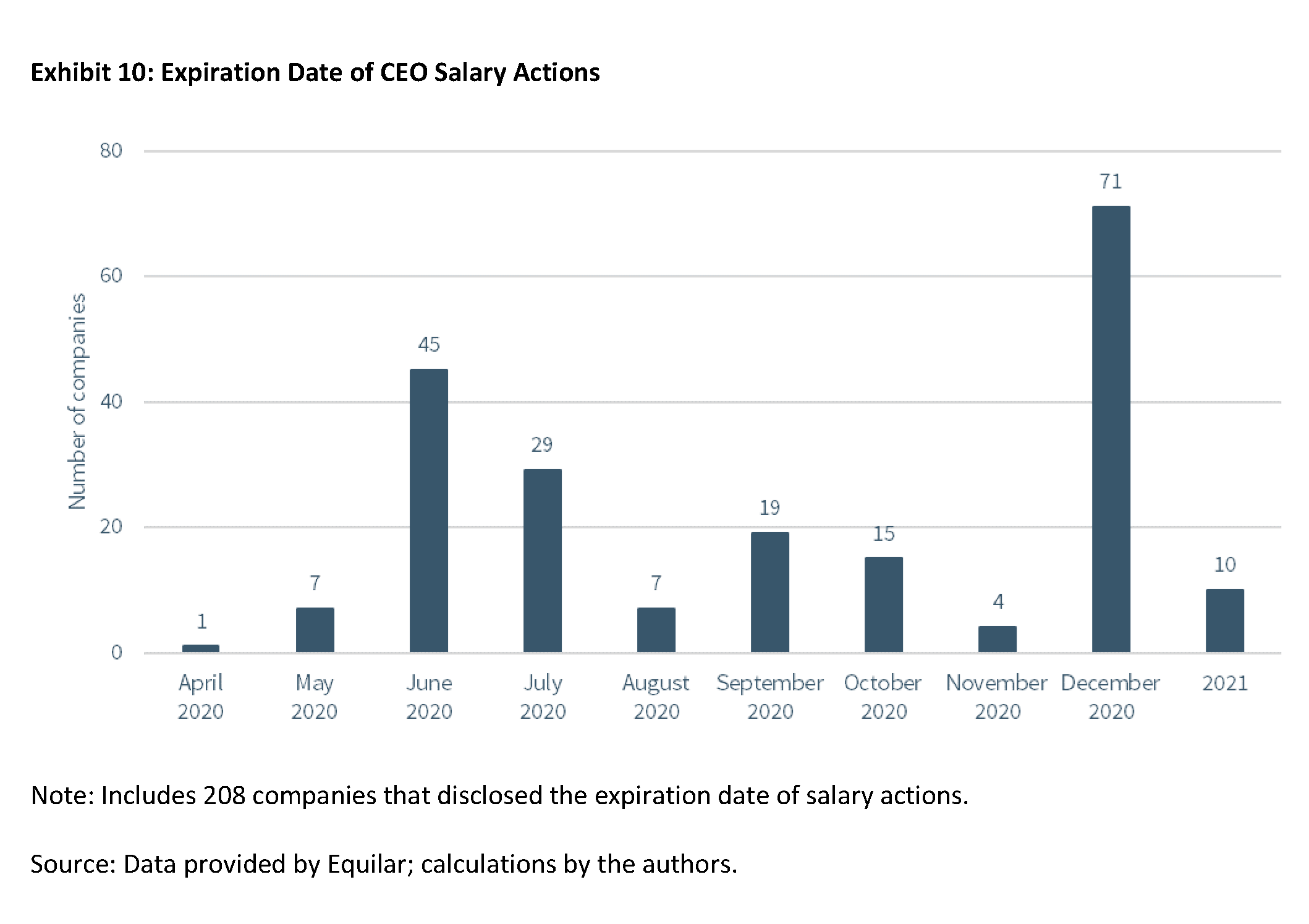

Half of companies disclosed an expiration date for salary reductions, with June 30 and December 31, 2020, being the most common. The remaining companies did not specify an end date (see Exhibit 10).

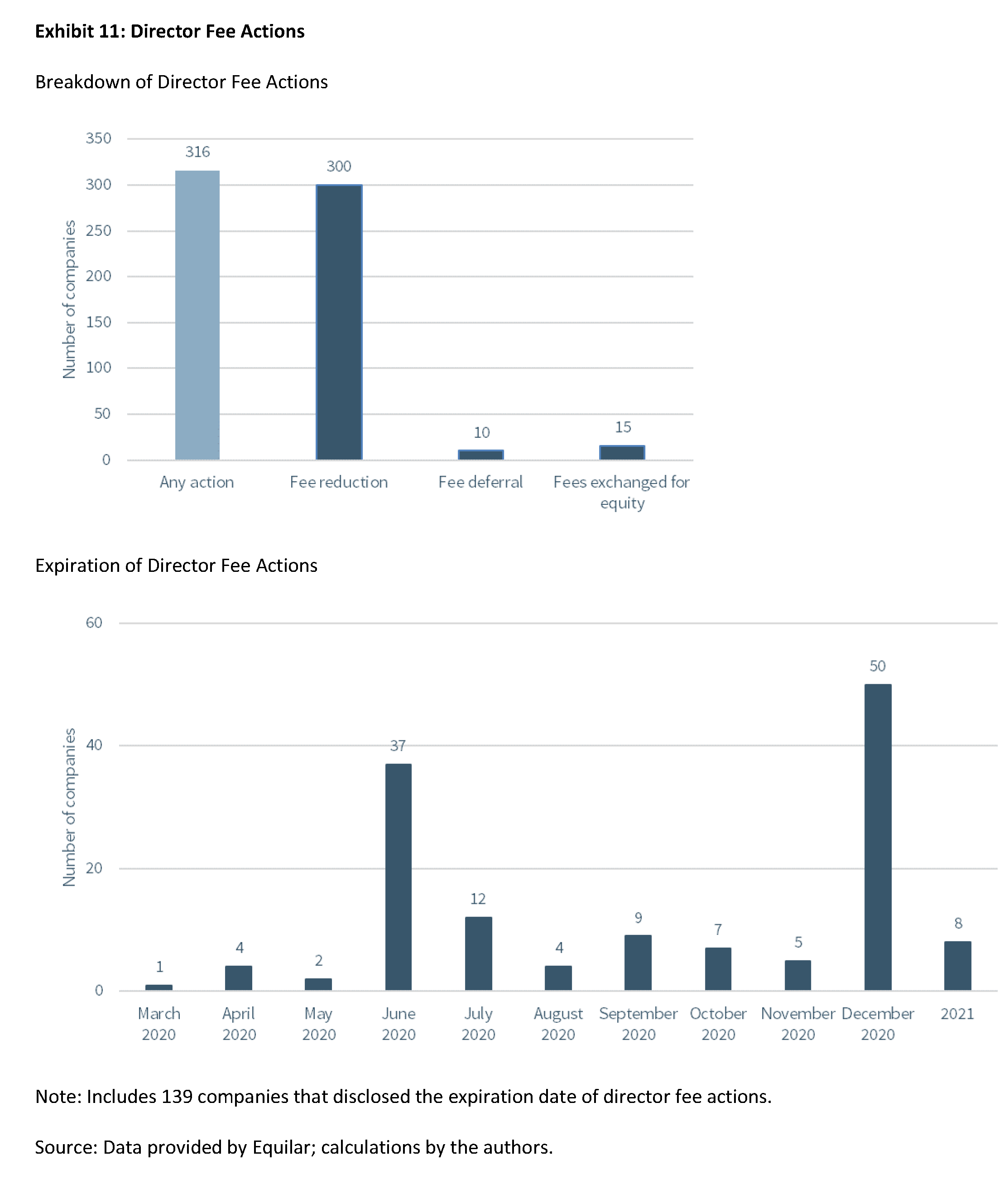

Director fee actions. Director fee actions tended to mirror CEO salary actions. Most companies (300 companies) directly reduced director fees. The remaining companies deferred the payment of fees (10 companies) or exchanged them for equity (15 companies). For example, Marriott International reduced board fees to zero. (It also reduced the salary of its CEO to zero). Groupon deferred the payment of board compensation to December 31, with the cash portion payable in equity. Just under half of companies that reduced director fees disclosed expiration dates, the most common of which were also June 30 and December 31, 2020 (see Exhibit 11).

Annual bonus actions. Changes to annual bonus programs were less frequent, with only 92 companies in the Russell 3000 making adjustments. Among these, 44 companies reduced current- or previous-year bonus payments, and 17 companies deferred the payment of previously earned payments. Ten companies exchanged the payment of bonuses from cash to equity. For example, casino operator Golden Entertainment elected not to pay 2019 bonuses in order to “conserve cash and help mitigate the impact of the COVID-19 outbreak on our business.” The company did not specify whether the bonuses would be paid at a later date. Advertising agency Omnicom Group deferred bonuses that historically would be paid in April to later in the year. Biotechnology company Athenex deferred bonuses and offered named executive officers the right to receive payment in cash or equity.

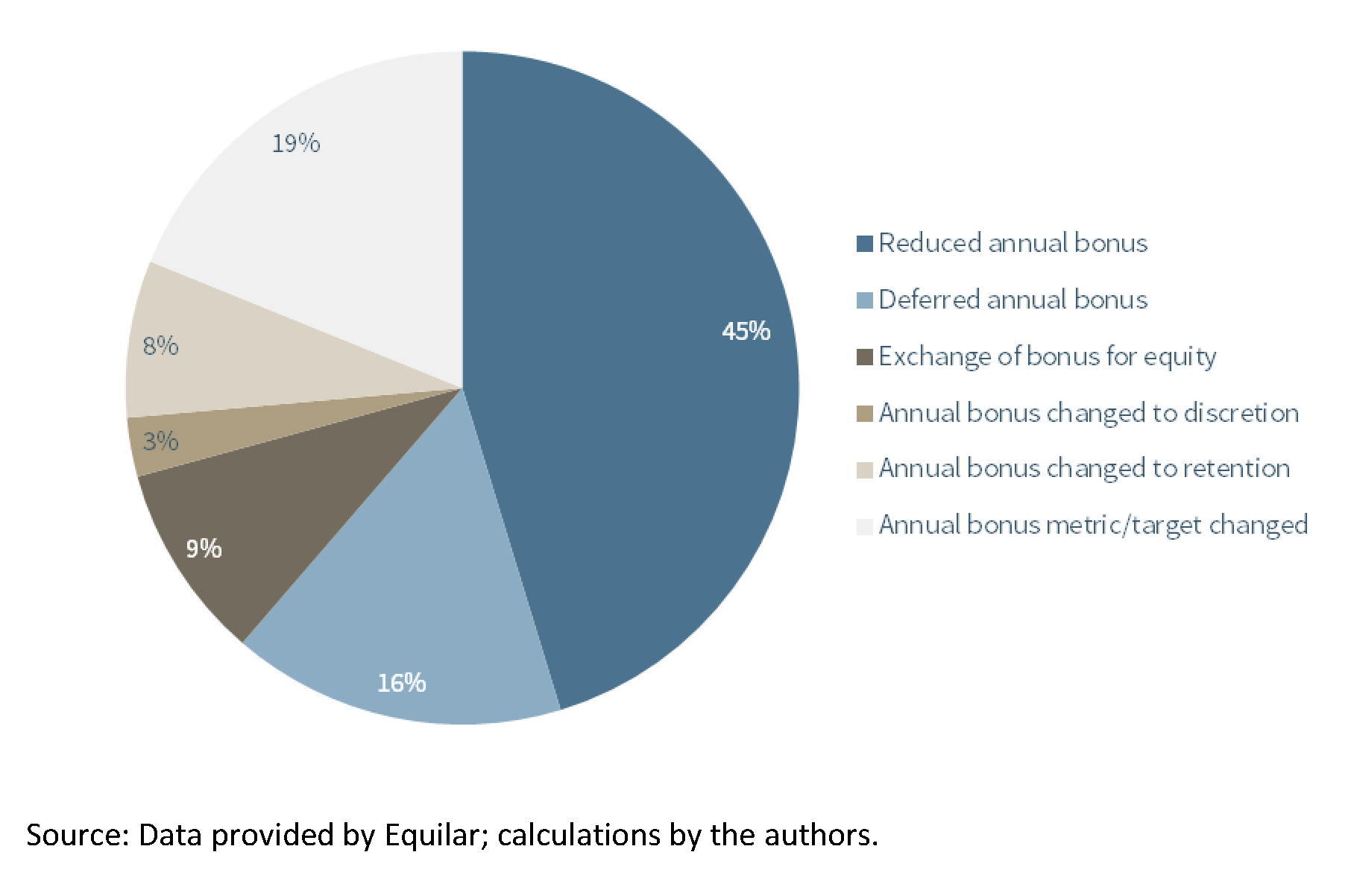

Only 31 companies made changes to the structure of the current-year bonus to provide potentially favorable offsets to the CEO: 3 companies changed the current-year bonus from a target-based award to a discretionary award, 8 changed it to a retention award (meaning the bonus would be paid upon continuous employment rather than the achievement of performance targets), and 20 changed the metrics used to award bonuses by reducing targets relative to what they had been prior to the outbreak of COVID-19 (see Exhibit 12). For example, Retail Opportunity Investment Corp (a REIT) changed its current-year bonus program to a discretionary award, and Whiting Petroleum changed it to a retention award. Home furnishing company At Home Group changed the metrics to its bonus plan to align with reduced budget targets, while leaving the targeted amounts unchanged. Similarly, Darden Restaurants disclosed that it intended to change its bonus formula and would use predetermined goals, but those goals would be established later in the year when the company had greater visibility into the operating environment.

LTIP actions. Very few companies (33 companies) made changes to their long-term incentive programs (LTIPs). Nine companies reduced the target value of the LTIP. Other changes included reweighting award vehicles such as decreasing the portion of performance units and increasing restricted units (9 companies), changing the metrics to award the LTIP (8 companies), and changing the LTIP to a retention award (7 companies) or discretionary award (1 company—see Exhibit 13). For example, Inspired Entertainment, which leases betting and gaming equipment to restaurants and bars, elected not to award additional LTIP awards in 2020 under its 2018 program and not to create an LTIP structure for 2021 to 2023. Apparel retailer Hibbett Sports decided not to grant value-based awards (awards of a specified dollar amount with the number of units determined by the stock price at the time of grant) because “the depressed price of our common stock could yield an unintended windfall to our executive officers.”

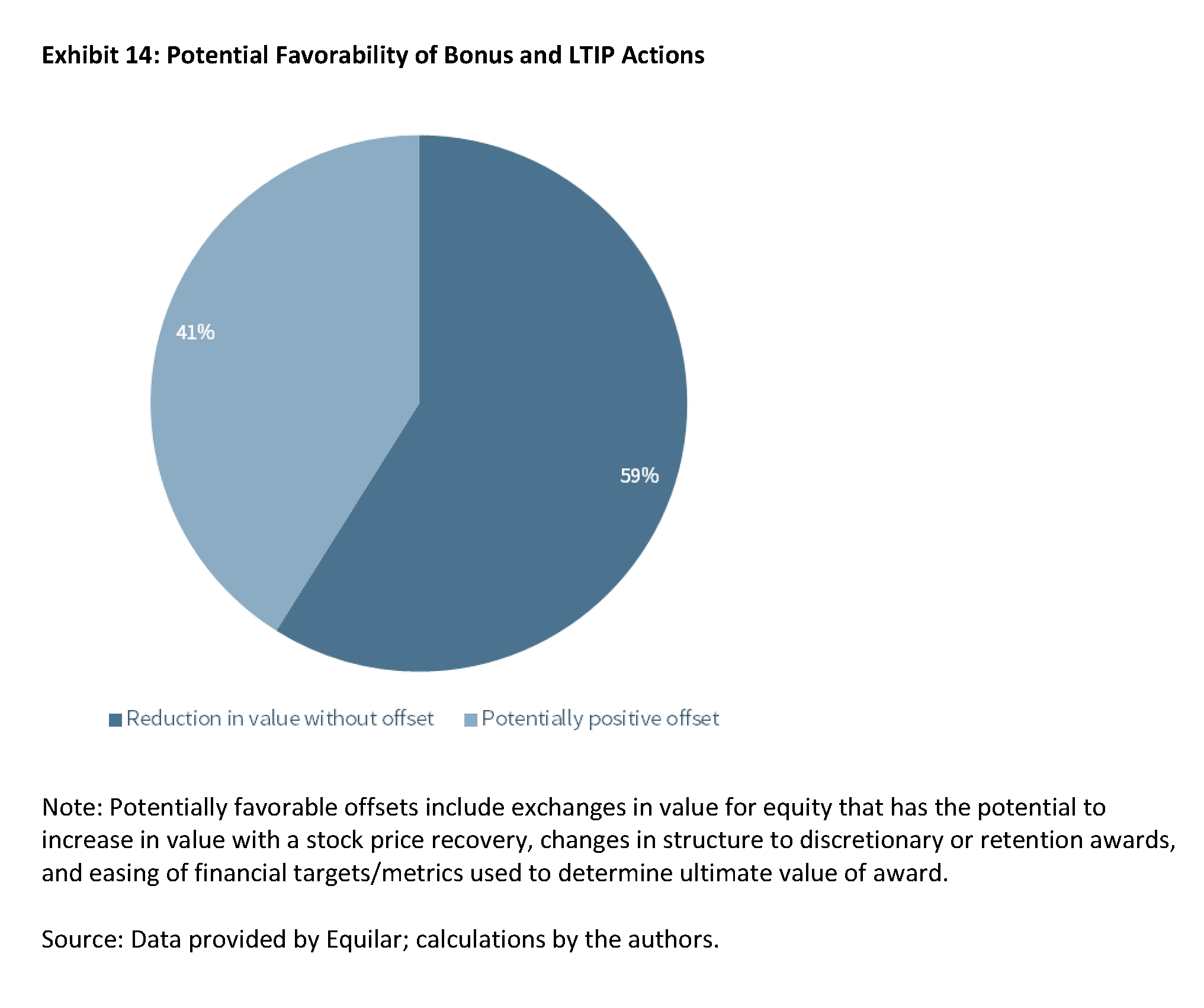

Value-increasing actions. Looking at annual bonuses and LTIPs together, we found that approximately 60 percent of changes resulted in a clear-cut reduction in value for the CEO. The other 40 percent were changes that gave the CEO the opportunity to earn value they might otherwise have lost, such as by exchanging cash awards to equity with the potential to increase in value through a stock price recovery, changing structure to discretionary or retention awards, or easing financial targets/metrics to determine the ultimate value of awards (see Exhibit 14).

Unusual salary and bonus actions. Included in the above data are unusual salary and bonus actions that are worth highlighting:

- Independence Contract Drilling. In addition to reducing the salaries and fees of senior executives and directors, the company reduced the size of its executive team—terminating two members—and shrunk the size of its board from seven to five to conserve cash. Eliminating board members is about as extreme a measure of cost reduction a company can take, and it signals the strain on the business.

- Yelp. This company not only reduced the salary of its CEO to zero but also effectively eliminated all forms of realizable pay for the CEO for the remainder of 2020, including forfeiting previously awarded restricted stock and performance-based restricted stock under its LTIP that were expected to vest during the year.

- Signet Jewelers. In one of the most comprehensive responses that a company took with regards to CEO pay, Signet Jewelers reduced its CEO’s salary by 50 percent with half of the reduced salary payable in stock; deferred the payout of the previous year’s bonus from April to June to conserve cash; split the current year bonus into two halves, with the first portion payable based on liquidity goals and the second half based on adjusted operating income targets whose levels were not yet determined; delayed the grant of long-term performance shares until the second half of the year; and froze matching of its deferred compensation and 401(k) programs.

- Meritor. This company implemented salary reductions. In addition, it has an annual bonus program that is unlikely to pay out but which it also does not intend to modify. To provide new incentives to executives, the company created a supplemental bonus plan based on liquidity and cost reduction metrics. If executives happen to achieve the targets of the original annual bonus plan, the supplemental bonus would be reduced one-for-one so that participants do not receive additional windfall payouts.

- Wesco International. In what looks to be a strong need for executive retention, this company reinstated in June salaries that had been reduced in April and increased them above pre-COVID-19 levels. It also increased annual bonus target percentages, granted specialty equity awards, and introduced severance/change-in-control provisions for senior executives. The company recently completed a large merger that likely adds new challenges to an already difficult operating environment.

In summary, it appears that fewer than 2 percent of the Russell 3000 took actions to try to preserve the incentive value of compensation offered to their CEO during the first six months of 2020 by replacing or modifying short- or long-term bonus programs. Fifteen percent of companies appear to have reduced pay to CEOs and directors either to conserve cash or to signal to shareholders, employees, and stakeholders that corporate leadership intended to share their economic burden. The remaining 83 percent of the Russell 3000 made no changes to CEO pay that required disclosure. However, it is worth noting that additional companies might reduce compensation in the future. Others might award supplemental awards to compensate executives for lost equity value after the pandemic has receded. It is also possible that, during our measurement period, companies awarded larger than usual (or larger than previously planned) stock grants that would not be picked up in our analysis.

Loss of CEO Wealth

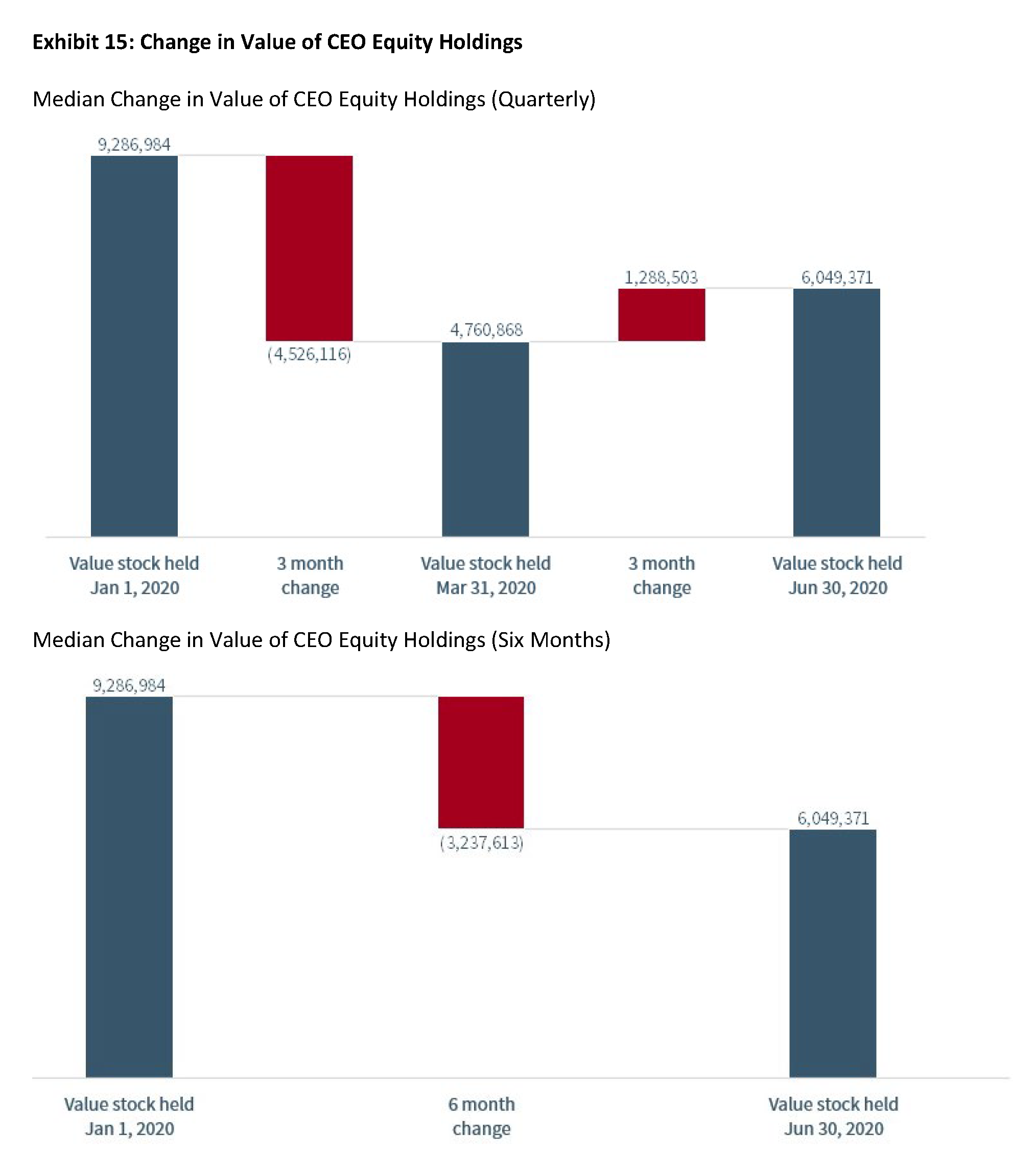

Finally, we measured the total change in CEO wealth of the 502 companies that implemented compensation changes. Having noted above that the average CEO forfeited 47 percent of salary but only 8 percent of targeted total compensation, we wanted to see how much wealth these CEOs lost due to declining stock prices.

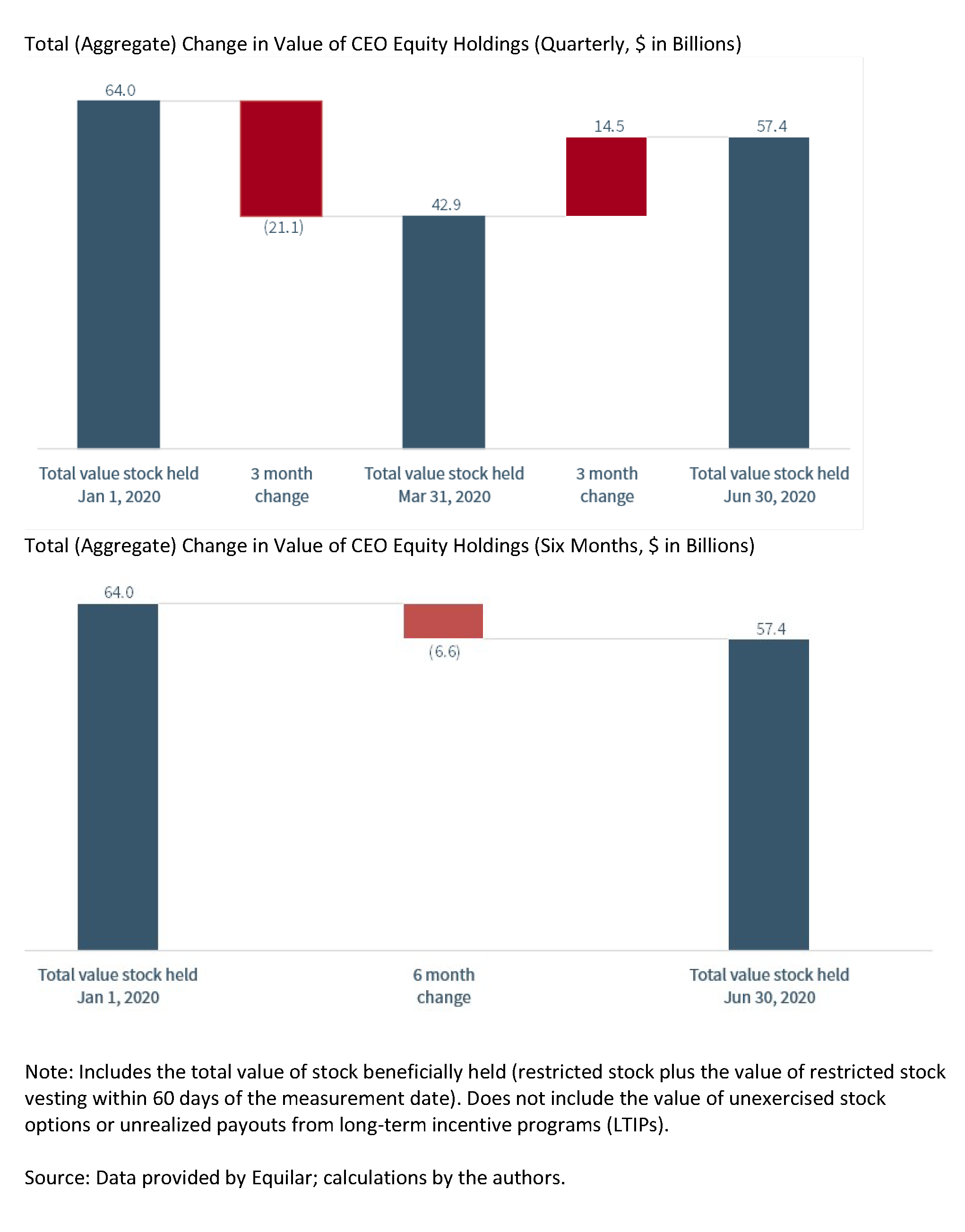

The median CEO in our sample held $9.2 million in stock on January 1, 2020. This includes stock beneficially owned plus the value of restricted shares expected to vest within 60 days. By March 31, when COVID-19 shutdowns were beginning to occur across the country and the stock market traded at sharply lower values, median CEO wealth had shrunk by 49 percent to $4.8 million—a paper loss of $4.5 million. Following the partial stock market recovery in the spring, median CEO wealth was $6.0 million on June 30—a 35 percent reduction from where it stood at the beginning of the year. In aggregate, these 502 CEOs lost a combined $6.6 billion in wealth over a 6-month period (Exhibit 15).

Regardless of the value of annual compensation adjustments that companies made, CEOs suffered considerable wealth loss through their direct ownership of company stock.

Why This Matters

- Following COVID-19, fewer than 20 percent of public companies elected to make changes to their executive and director compensation programs. Depending on the lens through which these changes are measured—change in salary, total compensation, or loss of wealth—this can be viewed as a relatively modest sacrifice or a significant forfeiture of value. How much economic pain did the typical CEO really suffer? In general, does this signal the success or failure of compensation program design?

- Companies that experienced economic hardship were significantly more likely to reduce CEO and director pay than those that did not. Are these CEOs responsible for putting their companies in a position of greater risk that resulted in greater loss, or was their economic hardship due to factors such as industry exposure that were outside the CEO’s control? If the latter, should the CEOs of these companies receive supplemental awards in the future to compensate for their losses? What is the correct thing to do from an economic perspective? A societal perspective?

- CEOs typically benefit from positive economic environments and rising overall stock market valuations. Should CEOs be sheltered from reversals in these same factors? If so, what implications does this asymmetry have on CEO incentives? Does it create a condition in which the CEO benefits from any exogenous event?

- The concept of ESG (environmental, social, and governance) centers on the fact that companies that truly embrace their stakeholders and invest in their needs have lower risk and higher performance. These companies are expected to suffer less economic loss in a downturn, and also to “do the right thing” by their employees. However, we found no observable difference in the ESG scores of companies that voluntarily reduced CEO/director pay and those that did not—despite differences in performance. Nor did we find a difference in ESG scores based on whether or not they chose to lay off employees. What does this say about our ability to accurately measure ESG? Are companies with more favorable ESG scores actually “better” companies from a stakeholder perspective?

The complete paper is available for download here.