Print

PrintSarah Keohane Williamson is CEO, Ariel Babcock is Head of Research, and Allen He is Associate Director at FCLTGlobal. This post is based on their FCLTGlobal memorandum. Related research from the Program on Corporate Governance includes The Myth that Insulating Boards Serves Long-Term Value by Lucian Bebchuk (discussed on the Forum here); Short-Termism and Capital Flows by Jesse Fried and Charles C. Y. Wang (discussed on the Forum here); and Share Repurchases, Equity Issuances, and the Optimal Design of Executive Pay, by Jesse Fried (discussed on the Forum here).

Returning capital to shareholders is an important and legitimate goal of many corporations. Buybacks are often an effective way to distribute capital, but care must be taken to mitigate downfalls related to personal gain and enrichment, poor timing, and excess leverage.

Buybacks have experienced a meteoric rise in popularity since the turn of the twenty-first century, overtaking dividends as the preferred means to return capital to shareholders in jurisdictions like the US. In 2019 alone, corporations spent more than USD 1.2 trillion globally on buybacks.

But the rise of buybacks has been riddled with controversy. Academics, practitioners, and politicians alike have maligned the use of buybacks, taking issue with their potential contribution to income inequality, underinvestment in innovation, and use for personal enrichment. Buybacks and their implications for the long-term strength of the economy are controversial but not well understood. A deeper look at the topic reveals the following:

- Buybacks have become a global phenomenon over the past 20 years, with many companies viewing them as an attractive alternative to dividends in returning capital to shareholders. They are flexible, recycle excess cash to the economy, and provide tax advantages in certain

- Buybacks have a number of pitfalls if not used carefully and in the right circumstances. These include:

- being used for personal gain and enrichment

- poor timing of investment decisions

- contributing to excess leverage, leading to lower levels of resilience

- Buybacks can add long-term value when the issues above are mitigated and key criteria are met. These criteria include:

- alignment with a company’s long-term plan

- adequate liquidity buffers

- fulfillment of additional investment needs in talent, R&D, CapEx, and M&A

The complete publication provides a fuller explanation of these findings, beginning with an examination of why buybacks are attractive to companies, followed by a deeper look at their pitfalls, and concluding with practical tools and guidelines for companies, investors, and policymakers to evaluate buybacks on their long-term merits.

The Rise of Buybacks

Buybacks (share repurchases) are an increasingly popular capital allocation tool to return cash to shareholders, rising to prominence in the past 20 years.

Buybacks by themselves are neither magic bullets to increase a company’s earnings per share (EPS) nor a nefarious means of enriching executives or shareholders. Buybacks, or share repurchases, are simply a financial tool. In a buyback, a company purchases its own shares from existing shareholders in the marketplace. This direct purchase of shares by the issuing company provides an alternative to dividends for the company to distribute capital to shareholders.

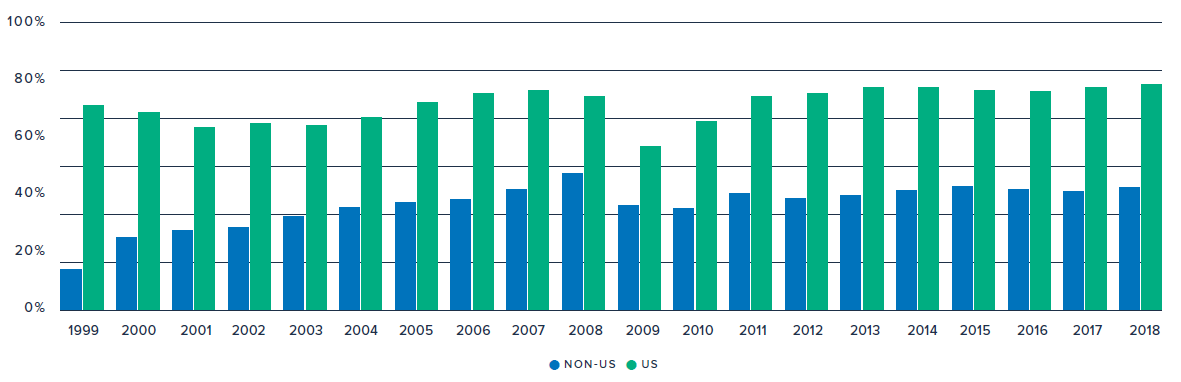

Buybacks are a fairly new phenomenon and have been gaining in popularity relative to dividends recently. All but banned in the US during the 1930s, buybacks were seen as a form of market manipulation. Buybacks were largely illegal until 1982, when the SEC adopted Rule 10B-18 (the safe-harbor provision) under the Reagan administration to combat corporate raiders. This change reintroduced buybacks in the US, leading to wider adoption around the world over the next 20 years. Figure 1 (below) shows that the use of buybacks in non-US companies grew from 14 percent in 1999 to 43 percent in 2018.

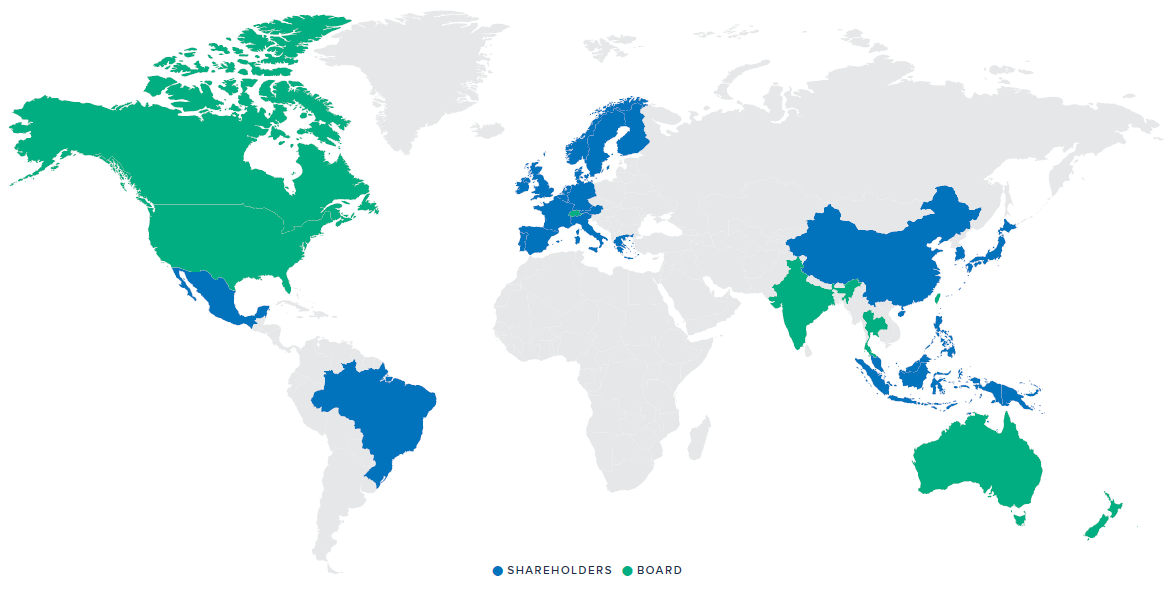

Buyback mechanisms vary, depending on the jurisdiction. While the board approves of buybacks in many jurisdictions, shareholders do have a say in certain countries, typically through an annual general meeting (AGM) vote. Figure 2 (page 6) shows the split between countries where the board approves of the buyback plan and countries where shareholders approve of the plan.

There are also multiple methods of stock repurchase, not just the repurchasing method achieved directly through the open market. While more than 95 percent of shares repurchased are through the open market, some companies also have purchased shares through tender offers and Dutch auctions.

Overall, companies’ use of buybacks is related to their capital intensity, firm age, and financial position. While each company is unique and idiosyncratic, trends over the last decade show the following:

Figure 1. Percentage of Firms Using Buybacks, US vs. Non-US

Figure 2. Party Approving Share Repurchases

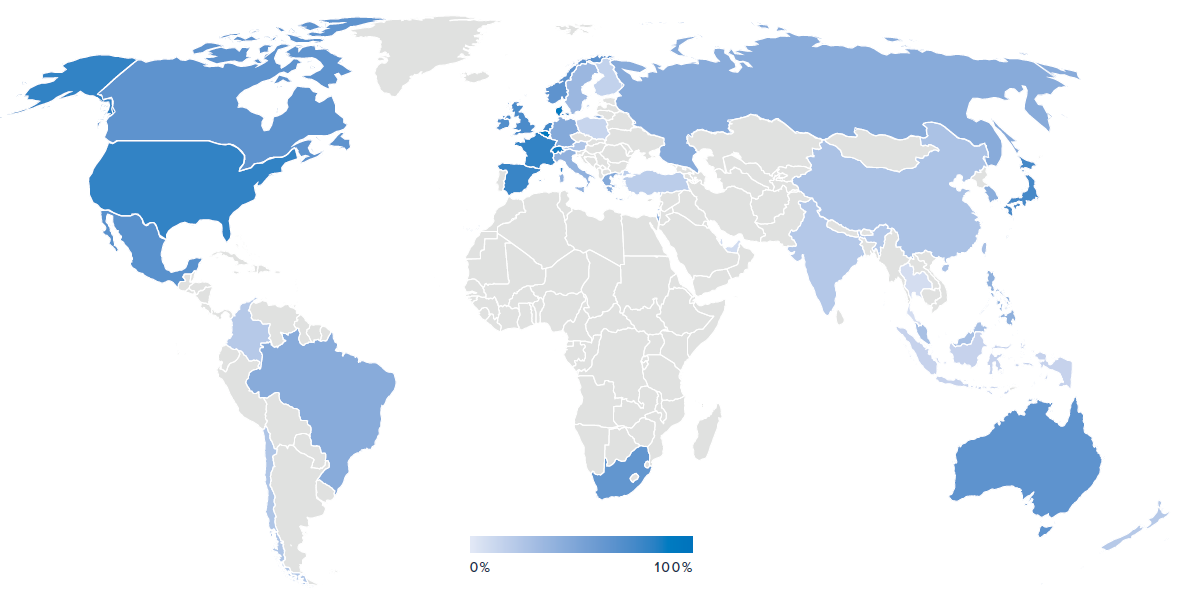

1. Buybacks have become a global tool—in 2018, their usage rate topped 50 percent in 16 different countries across six continents. (see Figure 3)

Figure 3. Percent of Companies in a Country that Executed a Buyback (2018)

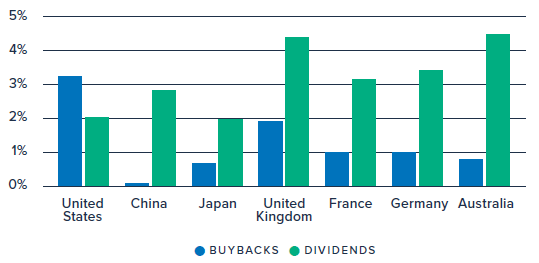

2. The US is by far the leader in buyback activity, and is the only country where money spent on buybacks exceeds dividends. (see Figure 4)

Figure 4. 2018 Dividends and Buybacks as a Percentage of Total Country Market Cap

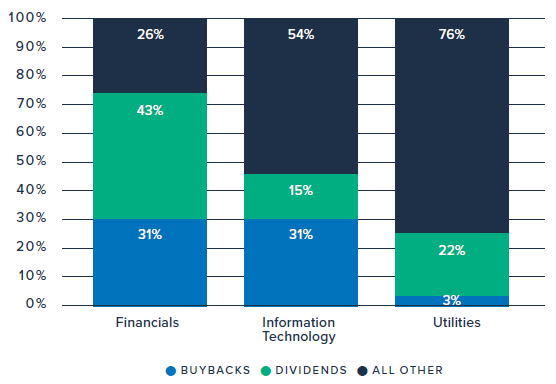

3. Capital intensive sectors like utilities spend less of their earnings on buybacks as compared

to fixed asset-light sectors like financials and information technology (see Figure 5).

Figure 5. 2018 MSCI All Country World Index Uses of Capital by Sector

Advantages

Buybacks are a technical capital allocation tool and an attractive alternative to dividends for the

following reasons.

Flexibility

Unlike dividends, buybacks can be turned on and off. Whereas there is an implicit expectation that dividends generally are not cut, buybacks can fluctuate based on business results and the company’s strategy.

Buybacks also provide shareholders with flexibility. Unlike dividends, which are paid out to all shareholders, buybacks only create a transaction for those who choose to sell their shares; others can opt out if they believe their shares will rise in value.

Signaling

Several academics have posited that companies use buybacks to signal that their stock price is undervalued. Unlike dividend signaling, companies are not committed to a constant payout at a higher level. This is most effective for small-cap companies due to information asymmetry.

Capital recirculation

Buybacks recycle cash, freeing “trapped cash” from firms in mature or capital-light industries with limited investment opportunities, allowing shareholders to reinvest in the next growing company. No matter how much money cash-rich companies like Apple invest back into their own company, at some point they will be left with more cash than they can productively spend. Constraining a company’s ability to return cash to shareholders could lead a company to make poor investments in the absence of good ones, producing an inefficient allocation of resources, shrinking the overall economic pie.

Tax advantages

Buybacks often receive preferential tax treatment compared to dividends in certain jurisdictions. In these jurisdictions, buybacks are taxed as capital gains while dividends are taxed as ordinary income, meaning investors could prefer to receive buybacks over dividends.

Long-term excess returns

Instead of having “millions of dispersed shareholders, whose stakes are too small to motivate them to look beyond short-term earnings,” buybacks concentrate ownership and increase the equity held by large, continuing shareholders. These “blockholders” may buy into the company’s vision and have an incentive to look at long-term growth opportunities and intangible assets instead of short-term earnings.

Pitfalls

Buybacks are often associated with long-term value-destroying behaviors, including several means of personal gain and enrichment, poor timing of investment decisions, and excess leverage.

As attractive as buybacks may be as a method to return cash to shareholders, they are a powerful tool that can lead to serious dangers.

Executive compensation gaming

A common criticism of buybacks is that they can be used by management to manipulate earnings per share (EPS), which could be used to inflate their own compensation metrics and hit quarterly guidance targets. Indeed, according to Institutional Shareholder Services (ISS), as recently as 2019, more than 30 percent of all compensation plans were linked to EPS.

By using buybacks to reduce the denominator (shares outstanding), management can boost a company’s EPS in the short run, assuming the numerator (earnings) remains unchanged.

While increasing EPS may look attractive, doing so via buybacks alone is hard to sustain in the long run: companies create more value through organic revenue growth and margin improvement. Artificially boosting EPS can be short-term in nature, and can even siphon capital away from growth initiatives.

While buybacks can contribute to executive compensation gaming, it is worth noting, however, that the problem in this instance would lie within the structure of a poorly designed compensation plan. EPS targets in compensation plans, not buybacks, could be the underlying cause of short-termism. Excessive buyback activity in this case is a symptom, not the root cause, of the problem.

Employee trading

One reason buybacks were all but illegal in many jurisdictions up until the 1980s was that they were considered a form of stock manipulation. The concern was that employees with inside knowledge of the company, usually executives, could trade around a buyback announcement. Rule 10B-18 legalized share repurchases under specific conditions to discourage employees from insider trading.

While regulations to deter employee trading still exist, many have found loopholes around them, especially in the US. As an example, current rules prevent employees from trading on the same day as a buyback announcement, but executives can announce a buyback, then sell their shares a few days later. A 2018 US Securities and Exchange Commission (SEC) study found that insiders were twice as likely to sell on the days following a buyback announcement as they were in the days leading up to the announcement, and that at companies where insiders sell heavily, stocks delivered subpar returns in the long term.

It is worth noting, however, that outside the US, there has been little evidence of employee stock manipulation. In jurisdictions such as the UK and Japan, regulations mandate that all employee transactions be disclosed by the end of the next day, with no trading in the weeks or months leading up to closing periods. Under these rules, such employee trading actions would simply not be possible.

Table 1 below, adapted from Kim, Schremper, and Varaiya, offers a view of current global buyback regulations.

Contribution to income inequality

One great danger of buybacks is that they could be used to accentuate income inequality. Instead of redistributing earnings to the company’s workers, or investing in projects and equipment to support future growth, companies use the money for buybacks— returning cash to already wealthy executives and shareholders. Evidence, however, is mixed on this issue, and a case can be made for both sides.

On one hand, buybacks indirectly contribute to the issue of executive compensation gaming while only benefiting shareholders instead of all stakeholders.

Academics argue that when pressured to generate near-term profits, management teams use buybacks as a short-term band-aid to boost profitability metrics, nefariously taking away capital from workers for their own personal gain. Regulators also have lamented that the current governance environment has contributed to a large increase in stock buybacks, a decline in gainsharing of corporate profits with workers, and growing inequality.

On the other hand, as a capital allocation tool, buybacks return cash to shareholders the same way dividends do, and in theory are no worse than dividends at contributing to income inequality. McKinsey & Company research found that there is no empirical difference between whether distributions take the form of dividends or share repurchases. By this logic, if dividends and buybacks contribute equally to income inequality, the issue is with the underlying structure of the share ownership rather than with buybacks themselves.

Poor timing of investment decisions

Management teams often say they like to buy their stock when it is undervalued, but companies do a poor job of timing the market, often buying at market peaks rather than troughs. Two factors contribute to this tendency.

Table 1. Global Buyback Regulations

| Jurisdiction | Timing Restriction | Price Restriction | Volume Restriction | Separate Disclosure | Insider Trading |

|---|---|---|---|---|---|

| United States | None | None | None | None | None |

| Japan | Week before year’s end | No higher than last day’s price | 25 percent of daily volume | Daily | Yes |

| United Kingdom | None | No higher than 5 percent of day’s price | 15 percent of total shares | Daily | Yes |

| France | 15 days before earnings announcement | No higher than daily high | 10 percent of total shares, 25 percent of daily volume | Monthly | Yes |

| Canada | None | No higher than most recent price | 5 percent of total shares, 10 percent of public float | Monthly | Yes |

| Hong Kong | One month before earnings announcement | None | 10 percent of total shares, 25 percent of monthly volume | Daily | Yes |

First, managers suffer from an overconfidence bias. Just like the classic driving example in which 80 out of 100 people in a poll believe that they are above average at driving, executives tend to believe that their company is undervalued. Executives believe in their own abilities to enhance the value of their company. This overconfidence bias leads managers to believe share repurchases at current valuation levels would be a good investment.

Second, companies typically engage in share repurchases when the firm is doing well and generating excess capital, often when the stock is at or near its peak—the opposite of “buy low, sell high.” From an investment point of view, it is best to do a buyback when market valuations are depressed— but rare is the company willing to announce a buyback program in the depths of a stock correction.

Buyback timing effectiveness may depend on the size of the firm. Some studies suggest that companies are good at taking advantage of undervalued stock prices during buybacks. Further examination by McKinsey & Company, however, concludes that this finding is driven almost entirely by small-cap companies with large information asymmetry.

Unlike small-cap firms, many mid- and large-cap companies display poor timing of their buybacks. A 2019 study by Fortuna Advisors shows that 64 percent of companies in the S&P 500 had negative buyback effectiveness, implying that a company’s buyback return on investment (ROI), though positive, was lower than its total shareholder return (TSR), usually due to poor buyback timing and suboptimal capital allocation decisions. However, the same study suggests that this problem can be mitigated by taking a long-term dollar-cost averaging approach to repurchasing stock, adopting rules related to market conditions, and employing a break-even scenario analysis.

Excess leverage

Within the past decade, interest rates have fallen to historically low levels, and the cost of debt financing has never been cheaper. Academics and practitioners alike have been concerned that an increasingly large portion of buybacks are funded via debt, leading to excess leverage on companies’ balance sheets.

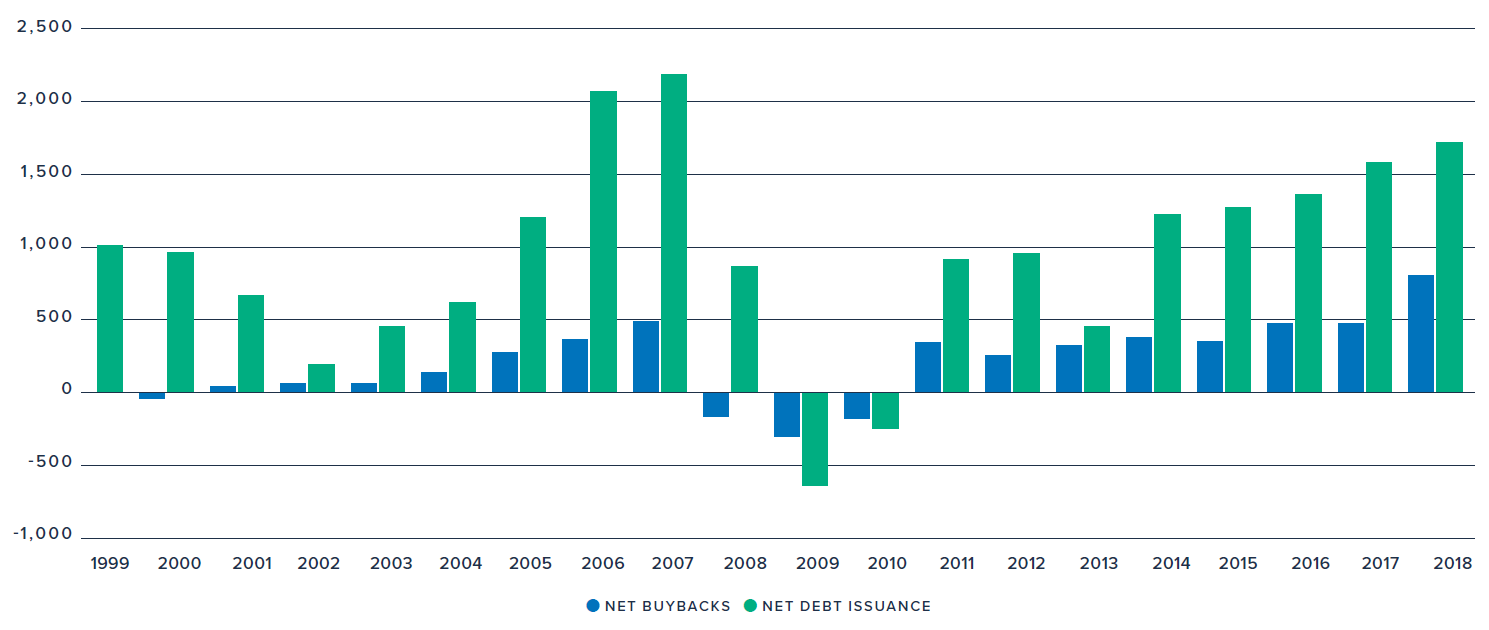

As seen in Figure 6 (below), there is almost no correlation between net debt issuance and buyback levels. In fact, in 2018 the level of debt-financed buybacks was at a historical low of 14 percent, and in the preceding years, at no point did this level rise above 33 percent. This corroborates previous evidence that companies mainly finance buybacks with excess cash, not debt.

Figure 6. MSCI All Country World Index Debt Issuance vs. Buybacks ($B USD)

While most buybacks are financed by excess cash, companies do need to ensure that they still have enough of a rainy-day cushion. Ultimately, flexibility is key, and our previous research has shown that repeatedly returning more than 100 percent of earnings to shareholders is an indicator of short-term behavior.

Our research has shown that chronic overdistribution of capital is associated with lower return on invested capital. While returning capital to shareholders makes sense in some circumstances, overdistribution can be problematic, potentially leaving firms with thin cash buffers and negative book equity. Faced with a crisis like COVID-19, companies that played too close to the edge had lower levels of corporate resilience.

Buybacks are a powerful but dangerous tool. Understanding their pitfalls and mitigating their downsides is critical to companies’ using buybacks in a manner that furthers their long-term goals.

Mitigating Common Pitfalls

In the right circumstances, buybacks can further long-term goals. They can be a useful capital allocation tool, provided companies take careful steps to mitigate the issues described above. Ultimately, the following measures should be adhered to:

- Companies must ensure that any buyback is aligned with their long-term strategy, including having adequate liquidity buffers and capital for other needs.

- Investors must hold companies accountable for their actions.

- Policymakers must establish a level playing field.

To find the right balance, the following tools and guidelines could help companies, investors, and policymakers evaluate the merits of buybacks for the long term.

Companies

Companies can consider a buyback’s implications for strategy and performance, executive compensation, and investor relations communications in order to evaluate a buyback on its merits.

Strategy and performance

When it comes to strategy and performance, corporate boards can assess whether the buyback plan makes sense in light of the overall capital allocation strategy. For an apples-to-apples comparison, buyback return-on-investment (ROI) can be compared to the discounted future ROI from other uses of cash—including investments in talent, R&D, CapEx, and M&A. Firms could choose to pursue buybacks in situations in which there are no superior investment alternatives. To avoid the pitfalls of poor repurchase timing, studies from Fortuna Advisors have shown that buybacks are more effective when taking a price-average approach in calculations.

We’ve seen that companies do a poor job of timing the market when they repurchase stock. This isn’t to say that buyback ROI has been negative, just lower than TSR (suggesting that potentially better uses for this capital exist). In fact, 78 percent of S&P 500 companies have had positive buyback ROI from 2013–2018. To raise their purchasing effectiveness, companies can take a price-average approach over a longer time horizon to execute a buyback. Fortuna has found that 62 percent of companies would have benefited from spending equal amounts on share repurchases every quarter

instead of trying to time the market. All else equal, these “dividend-like buybacks” would have saved the sampled companies a collective $159 billion.

Of note, in looking at the go/no go decisions for buybacks, companies are right to be aware of maintaining healthy liquidity and leverage ratios by not overdistributing capital.

Executive compensation

To avoid executive compensation gaming, boards can evaluate the potential side effects of buybacks and implications for incentive compensation. Plans themselves could be restructured to minimize the potential effects of buybacks, stripping out or minimizing links to EPS and considering the costs of any associated share repurchase to offset dilution.

Investor relations communication

The investor-corporate dialogue on capital distribution decisions is critical. Companies that engage effectively use a roadmap with a long-term plan. Within it, executives and board members clearly articulate the company’s long-term vision, and how each aspect of capital allocation, including buybacks, supports that vision. In doing so, companies cultivate trust from investors, who in return benefit from having a clearer understanding of why shares are being repurchased.

Investors and Shareholders

Investors and shareholders can evaluate the likely implications of a buyback by engaging with companies and voting their shares accordingly.

Engaging with corporates

Investors can encourage the use and disclosure of long-term corporate roadmaps. By holding companies accountable for clearer explanations and disclosures on why companies engaged in buybacks and how such actions align with the long-term vision of the company, informed long-term investors serve as helpful moderators of corporate buyback behavior.

Voting

Based on all available information from the company, investors and shareholders can evaluate whether buybacks are the most efficient use of capital in the long run. Regardless of jurisdiction, investors can have a strong say in the company ’s direction through their votes. For countries where shareholders approve buybacks, investors can use their votes directly to support or oppose a buyback program. For countries where the board approves buybacks, shareholders can still use their votes to influence other issues related to buybacks, such as executive compensation structure and metrics (say on pay), or in their re-election of directors.

Regulators and Policymakers

Regulators and policymakers can examine their jurisdictions’ stances on tax treatment, executive trading, and disclosure when evaluating buyback activity.

Tax treatment

As we’ve seen, buybacks and dividends both return capital to shareholders. But shareholders themselves are often not agnostic between receiving capital in the form of a buyback or dividend. In many jurisdictions, buybacks receive preferential tax treatment, leading many shareholders to prefer them to dividends. Leveling the tax treatment so that shareholders are truly indifferent between receiving dividends and buybacks would solve this problem.

India has taken steps to achieve this level playing field. In 2014, the Indian government levied a dividends tax on corporates, prompting a surge in buybacks in the coming years. This disparity was rectified in 2019, when the government equalized the tax treatments of dividends and buybacks on corporates. Buyback levels subsequently returned to pre-2014 levels.

In addition to leveling the tax playing field, policymakers and regulators also could consider how best to reconcile offering tax advantages with existing anti-buyback rhetoric from lawmakers. It is ironic that in jurisdictions like the US, buybacks enjoy favorable tax treatment while also being a behavior that authorities disparage.

Executive trading

While jurisdictions like Hong Kong prohibit employee trading in specific circumstances, there are no mandated blackout dates in the US. To curb insider trading, regulators and policymakers could mandate blackout windows on employee stock trading around buyback announcement and execution, effectively setting up a firewall. That isn’t to suggest that employees aren’t allowed to trade their own stock.

Authorities could designate legal trading windows for corporate employees, (e.g., during the middle of the quarter) following the approach of many asset management firms today.

Improvements To Disclosure

Policymakers and regulators also can consider adopting stricter disclosure requirements around share repurchases. Such regulations include, but are not limited to, the following:

- Timing restrictions: restricting trading in the days leading up to the year’s end or earnings announcements

- Pricing restrictions: limiting the purchase price to be no higher than the most recent price (company is not allowed to buy on an uptick)

- Volume restrictions: limiting repurchases to a certain percentage of average daily volume

- Separate announcements and disclosures: requiring daily or monthly disclosures of share repurchase activity

Conclusion

Buybacks are a popular tool and in many cases are both misused and misunderstood. They can be an effective way to return capital to shareholders, but have several potential pitfalls.

Companies, investors, and policymakers could each take steps to understand how buybacks affect them and the overall financial ecosystem in order to mitigate the downsides of buybacks. Ultimately, buybacks are a useful capital allocation tool that can be wielded thoughtfully and, in rare, specific circumstances, in support of long-term value.

The complete publication, including footnotes, is available here.