Print

PrintTara Tays is a managing director in Deloitte Consulting LLP’s National Compensation Strategies Practice; Abby Dunleavy is a manager at Deloitte Consulting LLP; and Robert Lamm is an independent senior advisor at the Center for Board Effectiveness, Deloitte LLP. This post is based on their Deloitte memorandum. Related research from the Program on Corporate Governance includes Paying for Long-Term Performance by Lucian Bebchuk and Jesse Fried (discussed on the Forum here).

When COVID-19 first began impacting the US economy, many companies faced unclear financial forecasts and uncertainty on whether incentive plans would appropriately reward executives and employees for their contributions, pre– and post–COVID-19. Rather than overhaul in-flight incentive plans at a time of great uncertainty, many companies decided to take a “discuss now, act later” approach. Now, companies nearing their fiscal year-ends must “act” by determining whether incentive plan designs and performance targets established before the pandemic will reasonably reward executives and employees for their contributions, especially given the many challenges posed by COVID-19.

A quick look at companies’ actions

Many companies significantly impacted by the COVID-19 pandemic took swift steps to reduce compensation expense in response to economic conditions while also prioritizing the safety of employees and customers and stabilizing their businesses. Other challenges faced by management and compensation committees included retaining and engaging employees despite unknown or unattainable performance goals in annual incentive plans and performance-based long-term incentive awards, out-of-the-money stock options, depreciated full value equity awards and declines in retirement account balances.

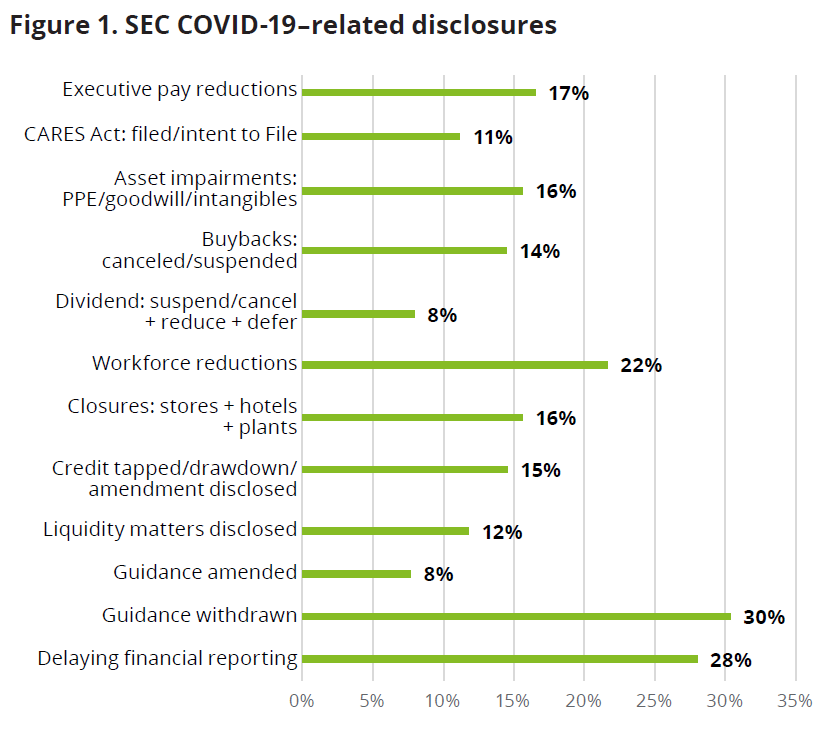

Based on Deloitte’s COVID-19 Sensing Events Tracker, between February 2 and October 23, 2020, 3,404 companies disclosed one or more COVID-19–related events in Securities and Exchange Commission (SEC) filings (see figure 1). While 30% withdrew/suspended earnings guidance, 28% delayed financial reporting, and 8% amended/revised earnings guidance, very few companies reported overhauling their outstanding incentive plans or adjusting the performance metrics/goals in incentive plans despite the lack of line of sight in financials and business operations.

The “act later” approach in determining what to do when it comes to incentive arrangements is evident in SEC disclosures filed in 2020, or the lack of disclosures, related to executive incentive pay decisions. The choice to delay implementing changes to incentive plans is likely due to a number of factors, including uncertainty about the impacts of COVID-19 on financial and/or operational performance goals, uncertainty regarding the timing of a recovery, and concern about how shareholders and proxy advisers would react to changing incentive plans in the middle of a performance cycle.

Based on Deloitte’s review of publicly available information and our professional experience, we have observed the following changes in outstanding incentive arrangements:

- Annual incentive plan changes: While not a prevalent practice, some companies have reported suspending incentive programs, modifying strategic performance measures, deferring bonus payments, or reducing incentive opportunities. A handful of companies with new fiscal years starting in the middle of 2020 disclosed adopting two six-month incentive plan performance periods rather than the traditional full-year period, establishing new performance goals and/or performance curves to determine incentive payouts, and capping bonus payout opportunities. Our discussions with companies strongly suggest that these types of plan design changes are also being discussed between management and compensation committees with a new fiscal year just around the corner.

Deloitte perspective: It seems likely that in certain industries many annual incentive plans will result in below target formulaic results for 2020, despite the countless hours executives and employees have spent on various COVID-19–related issues. In order to make sure incentive plan participants’ efforts and accomplishments do not go unnoticed, compensation committees should consider performing a robust review of the actions taken by executives to protect the financial and nonfinancial health of their companies and employees and the countless hours spent by employees to push forward COVID-19–related plans and acclimate to the new work environment. Rather than simply relying on incentive plan financial performance results, committees should consider COVID-19–related contributions and nonfinancial results before approving incentive plan payouts despite potential financial shortfalls. Additionally, any plan payouts need to be reasonable in the context of developments over the course of the incentive plan performance year.

- Long-term incentive plan changes: In comparison to all COVID-19–related actions taken by companies, changes to long-term incentive programs were notably less prevalent. A minority of companies suspended their long-term incentive programs, provided equity awards in lieu of base salary reductions, or granted special equity awards to retain critical talent in these uncertain times.

Deloitte perspective: Long-term incentive programs are designed to reward executives and employees for long-term results, such as increased company stock price over a three-year period; achievements of synergies in light of an acquisition; environmental, social, and governance accomplishments; or simply improved financial performance.

Given the focus behind long-term incentive awards, it is important that companies not make rash decisions with outstanding awards (e.g., canceling underwater stock options and replacing them with new awards, cancelling performance-based awards when the majority of the performance period has not completed, etc.). Compensation committees should also pay particular attention to preventing undesirable windfalls for executives. For example, committees need to be mindful of the number of shares granted at temporarily depreciated stock prices.

On the other hand, there are some instances whereby committees may want to act quickly, such as in situations where out-of-the-money stock options are about to expire. In this instance, committees may want to ask management to provide an inventory of vested stock options set to expire in six months to one year and see how much value has been lost and determine if a time-vested award should be provided to offset a drastic decline in stock price value. To the extent permitted by the underlying plans, companies may also want to consider allowing terminated or retired employees more than 90 days to exercise vested stock option awards and perhaps extend the exercise period to 12 or 24 months. These actions can help employees feel like they are not being penalized for circumstances completely outside of their control.

High-level summary of key considerations for applying discretion on formulaic incentive arrangements

As the 2021 proxy season gets underway, we anticipate an uptick in disclosures around compensation committees exercising discretion (i.e., not strictly following incentive plan formulas) to determine the incentive payments needed to reward executives and employees for their contributions. It is important that committees take into account financial, operational, and market impacts before determining if applying discretion is appropriate.

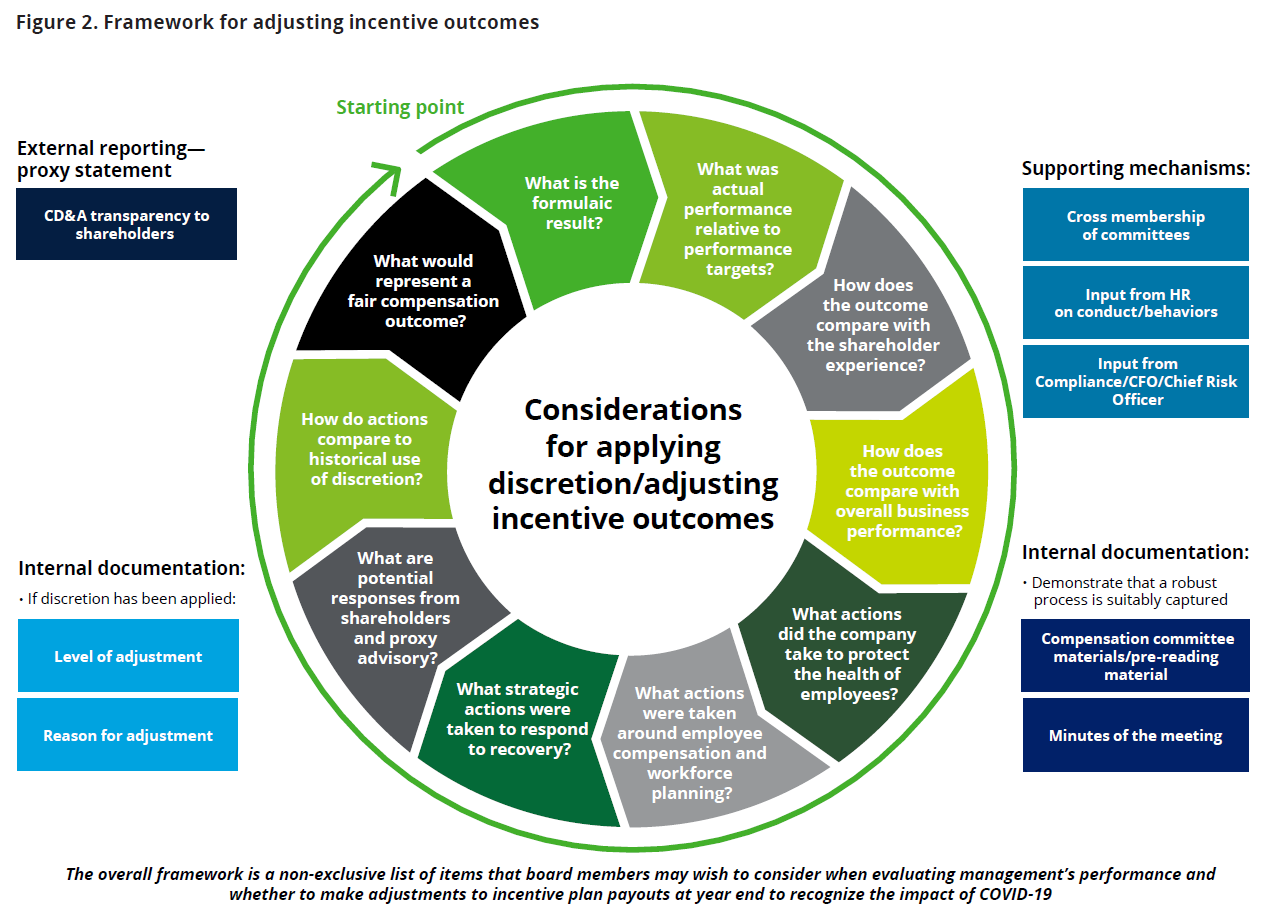

While institutional shareholders may be willing to accept changes to the design of go-forward annual and long-term incentive plans to align current economic conditions with executive and employee compensation programs, compensation committees will be faced with determining how much discretion should be used to settle in-flight incentive arrangements. Deloitte has prepared a framework that both management and compensation committees can use to take full measure of everything that has happened before determining if discretion or adjustments to the incentive plan formula should be used in determining an appropriate level of incentive payouts at the end of the performance period (see figure 2).

Once the formulaic incentive plan results are in and management and the compensation committee believe some level of adjustment to the plan formula is warranted, they should consider the following questions:

Overall performance

- How do the incentive plan formula results compare with overall financial and operational business performance? How did the company perform relative to prior years?

- Were shortfalls in incentive plan performance due to factors other than COVID-19 (e.g., poor synergies from acquisitions)?

- Did management take the appropriate steps to reduce costs in a timely and well-thought-out manner?

- Did the company maintain a strong balance sheet (e.g., sufficient cash on hand)?

Shareholder experience

- How did the company’s stock price perform (excluding and including the COVID-19 time period)? Were dividends reduced or suspended?

- What was the company’s total shareholder return relative to both its peers and the market in general?

- How did the company’s financial performance compare with its peers?

Workforce and workplace safety

- Did the company take practicable steps to protect the health of its employees and customers?

- Were plans put in place in a timely manner and well-planned?

Workforce pay decisions/planning

- Did the company reduce employees’ salary and/or hourly wage, reduce hours worked, or conduct furloughs or layoffs?

- Was the company able to retain key talent and maintain levels of employee engagement?

- Was management transparent (and timely) in communicating with employees?

- Did management take appropriate steps to provide that the right talent was in place to take advantage of the economic recovery?

Response to the recovery

- How has management prepared the company for recovery?

- Were proper steps taken to deal with issues uncovered by the pandemic (such as supply chain issues, cash flow reserves, etc.)?

- Was the company able to ramp up quickly to take advantage of the “surge” in demand (if applicable)?

- Did management keep the board well-informed throughout the economic crisis?

- Was management responsive to input from the board?

- Was the company proactive in communicating with investors, suppliers, and customers?

In addition to discussing the answers to these questions, compensation committees may want to evaluate how discretion has been used in the past, specifically in response to prior economic recessions, negative macroeconomic events, or events completely outside of management’s control. This can help determine if applying discretion to incentive arrangements would be inconsistent with past practice and result in an unintended precedent.

For public companies, a final but critical consideration to utilizing discretion or adjusting the incentive plan formula is the potential response from shareholders and proxy advisers. According to COVID-19–related guidance published by Institutional Shareholder Services (ISS) on April 8, 2020, [1] ISS encourages companies to provide “contemporaneous disclosure to shareholders” in the event there are changes to their annual incentive plans’ performance metrics and performance goals in response to the economic environment. When it comes to long-term incentive awards, ISS’s voting policy is generally not supportive of changes to outstanding long-term incentive awards, since awards are intended to reward plan participants over a performance period greater than one year. However, ISS will look at changes to outstanding long-term incentive awards on a case-by-case basis to determine if compensation committees’ application of discretion was appropriate, reasonable, and properly explained to shareholders in the proxy statement.

Glass Lewis (GL) generally has a similar view on the application of discretion to incentive arrangements. Specifically, effective proxy statement disclosures and rationales will be critical in GL’s evaluation. GL will also review whether executive pay decisions are aligned with employee experiences and shareholder interests.

In other words, in the event discretion is utilized to determine incentive plan payouts, compensation committee members not only need to have a rationale for the use of discretion, but also need to provide robust disclosure in the proxy statement on their rationale.

Ultimately, compensation committees will have to determine what decisions will result in fair compensation outcomes. There are brand and reputational risks associated with making adjustments to incentive compensation arrangements before the full impact on all stakeholders is known. There can also be risks in doing nothing, as employee engagement and retention may be negatively affected. The most reasonable approach for each organization to take in rewarding employees will need to be carefully evaluated. Each company will need to review the extent to which discretion is applied to incentive payments based on the specific effects of the COVID-19 impacts on its workforce, business, and rewards and talent strategies.

Endnotes

1ISS Global Policy Board, ISS Policy Guidance, “Impacts of the COVID-19 Pandemic,” April 8, 2020.(go back)