Print

PrintJulian Hamud is Senior Director of Executive Compensation Research at Glass, Lewis & Co. This post is based on his Glass Lewis memorandum. Related research from the Program on Corporate Governance includes the book Pay without Performance: The Unfulfilled Promise of Executive Compensation, by Lucian Bebchuk and Jesse Fried; and Executive Compensation as an Agency Problem by Lucian Bebchuk and Jesse Fried.

The COVID-19 pandemic has not changed Glass Lewis’ approach to executive pay. We start from each company’s specific circumstances, evaluating compensation programs through the lens of pay and performance alignment, and the extent to which companies have been able to tie any program changes to this alignment going forward. It’s a pragmatic, contextual approach that applies in good times and bad.

However, the landscape for issuers and investors has shifted markedly. The many uncertainties faced by companies and their shareholders highlight the need for effective pay programs. Strong linkages between pay and performance remain crucial despite market-wide disruptions, and demonstrating this alignment to shareholders is all the more important. Moreover, the scope of topics to be considered in relation to executive pay is widening, with E&S issues drawing exponentially increased focus in 2020, and human capital management becoming particularly relevant during a time of global economic downturn.

Further, issuers would do well to consider that the pandemic has made executive pay a more salient issue for many investors. All companies, especially those seeking special support from governments or executing significant employment cuts, should consider the reputational risk associated with poor pay decisions, particularly quantum payouts. Even those companies who have managed to perform well during this time may face additional challenges in justifying high executive payouts to their shareholders.

Given the increased level of interest in public company pay decisions and related proxy voting recommendations, this post is intended to provide illustrative guidance on the intended application of Glass Lewis’ existing policy approach to executive compensation at U.S. and Canadian companies under various scenarios expected in the wake of the coronavirus pandemic.

Pay-for-Performance Analysis

Glass Lewis’ proprietary pay-for-performance model provides the foundation of our quantitative analysis. We do not expect the macroeconomic climate to have a drastic impact on our pay-for-performance model. The use of a three-year weighted average for measuring pay and performance, and the strong relationship between our peer methodology and industry, serve to smooth out recent volatility and discrepancies between companies.

However, we recognize that potential disparities across industries will not be eliminated entirely. In consideration of potentially inequitable economic impacts, Glass Lewis considers a variety of additional factors in our analysis, including:

- Executive pay levels. Relatively low pay levels, along with consideration for industry-specific performance impacts, may mitigate our concern with a pay-for-performance disconnect generated by the Conversely, relatively high pay levels may exacerbate our concern with a disconnect, particularly if the company has underperformed against peers that have in large part performed well despite the broader macroeconomic climate.

- The strength of the company’s performance, in the context of significant macroeconomic This may mitigate concerns with any disconnect attributable to relatively high pay levels.

- Direction of travel, and whether the company has recovered more dramatically than peers in recent months. Our concerns with a disconnect between prior year pay decisions and performance may be mitigated if the decisions are supported by the company’s post-year-end performance.

Even prior to the impact of COVID-19, Glass Lewis has always considered the grade results generated by the pay-for-performance model within the context of a qualitative assessment of the company and its pay program. During our most recent proxy season, Glass Lewis recommended supporting the say-on-pay programs of 71% of U.S. companies who received a “D” grade, and of 40% of U.S. companies who received an “F” grade, in our pay-for-performance model. We will continue to exercise a holistic approach in evaluating the alignment of executive pay and performance within the context of the pay-for-performance model in the wake of the COVID-19 pandemic.

Say-on-Pay Proposals

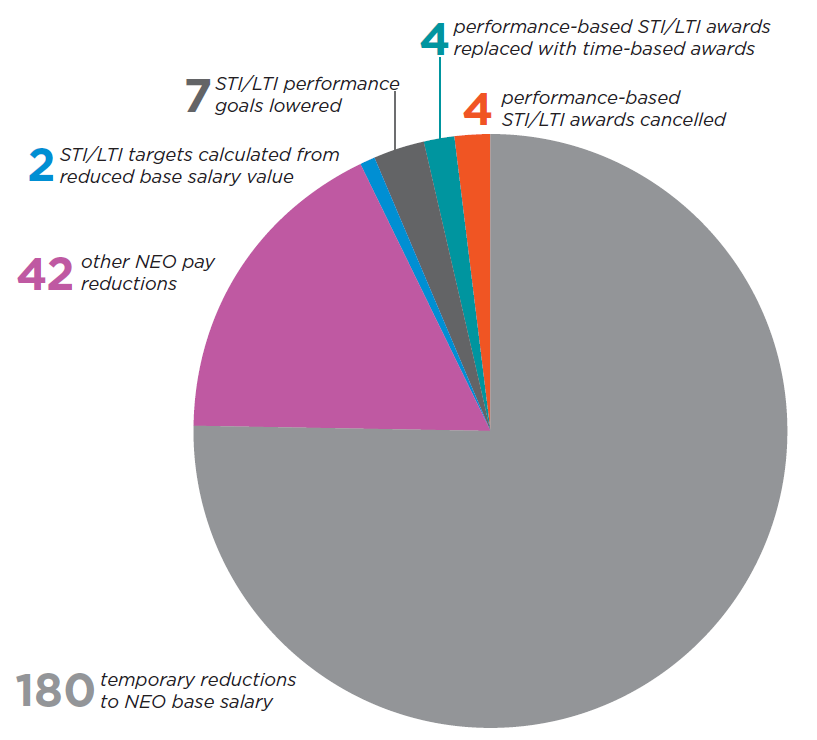

The question of how companies respond to changed macroeconomic conditions resulting from the COVID-19 pandemic will dominate upcoming say-on-pay votes. Due to the timing of proxy season, as of August 2020, just 273 of the 5,000+ public U.S. and Canadian companies within Glass Lewis’ coverage have already disclosed COVID-related compensation adjustments in their proxy statement. To date, the most common response has been a temporary reduction in NEO base salaries, reported by 180 companies (though only two of the 180 clarified that incentive awards would be calculated off the reduced salary levels).

We acknowledge that lowering executive base salaries may be viewed as a token of solidarity, but we will consider such gestures in the context of total executive compensation. Given the insignificant portion of total executive compensation that salary typically accounts for, most reductions will be of minor consideration in our analysis.

Rather than token gestures, we will be looking closely at overall pay levels, and particularly at any significant increases to target or actual payouts. Similarly, we will closely scrutinize mid-cycle adjustments to performance awards or their replacement with time-based awards. In all contexts, the overarching concern is whether pay is aligned with performance. That said, we recognize there are multiple exacerbating or mitigating factors to these broad potential pay scenarios, and therefore we have provided a more granular synopsis of our approach in evaluating say-on-pay during this time:

1. Increases to Quantum. Unless companies have performed very well on a relative and absolute basis, we will view increases to short-term pay levels or above-target payouts with great scrutiny. Moreover, companies that have adjusted their programs to provide enhanced outcomes will have a high bar to prove the appropriateness of their actions.

- If relative and absolute performance are not aligned, we expect boards to disclose their considerations in balancing these levels, for example negative discretion or caps to govern pay outcomes.

- If the company has removed caps or otherwise made excessive adjustments to metrics or calculation methodologies, we expect them to disclose a cogent rationale. Regardless, these companies will be viewed with extreme caution.

- If the company has exercised upward discretion on performance or payouts more directly, we

would expect an accompanying thorough and compelling justification. Final payouts should appear reasonable relative to the company’s performance during the year in review. - If performance is largely measured on a qualitative or nonfinancial basis, boards should ensure

that actual payouts remain clearly linked with overall firm performance.

2. Forwards vs Backwards. We generally view year-over-year increases to target incentive payout opportunities more tolerably than high payouts for backward-looking performance, as we recognize the need to incentivize executives going forward. However, this allowance is contingent on the incentive plan incorporating robust performance requirements that are reflective of executive efforts.

3. One-Off Awards. Glass Lewis continues to be wary regarding one-off awards granted outside a company’s regular incentive schemes, as such awards have the potential to undermine the integrity of a company’s regular incentive plans, the link between pay and performance, or both. We will view with caution any one-off awards granted to offset executive base salary reductions or below-target incentive payouts. We expect companies to provide thorough disclosure regarding the structure of one-off awards, their perceived necessity and their appropriateness in the context of aligning executive pay with corporate performance. Certain factors we may consider in evaluating one-off awards include:

- Whether the quantum of the award is reasonably sized relative to peer levels and to the company’s past pay levels. One-off awards should not result in an outsized year-over-year increase to total executive compensation or in total compensation that outpaces peer levels.

- Whether the awards are subject to additional performance criteria or vesting criteria. We generally believe performance criteria to be most effective in directly tying executive pay to corporate performance, and that awards should be subject to sufficiently long performance or time-vesting criteria to ensure retention of executives.

- The company’s history of one-off grants. Companies that have historically over-relied on onetime awards will need to address why their regular incentive programs could not be redesigned to adequately compensate their executives.

- Whether companies adhered to predetermined agreements regarding severance-based one-off award payments.

4. Major Structural Changes. We will view any major structural program changes with caution. Glass Lewis believes that boards should be thoughtfully restrained regarding sweeping, long-term changes, which may appear preemptive given ongoing market uncertainties and may only serve to heighten shareholder concerns.

When assessing committee discretion in relation to short-term matters, Glass Lewis will be mindful of

the need for increased flexibility during this time – along with a corresponding burden on issuers for

thorough disclosure and convincing rationale to accompany any such use of discretion.

While increased near-term flexibility may be prudent, we may still view certain program changes as potentially problematic, including, as iterated above, any decisions to replace performance-based awards with guaranteed or time-based awards, and any changes made to performance-based awards near the middle or end of their performance cycle, such as switching metrics or retroactively shortening the length of a performance period. Factors we will consider in conjunction with such decisions include:

- The strength of the Company’s disclosure and rationale, and whether these changes continue to align pay and performance; and

- In the case of any performance-based awards replaced with guaranteed or time-based awards, we will evaluate the granting basis and quantum. We would expect that granting practices are not adjusted for enhanced long-term outcomes, and that the lowered risk associated with the elimination of performance-based conditions would be offset, for example by a lowered award value.

5. Potential Windfalls. We will evaluate the potential for any program changes, particularly to equity-based grants, to result in windfall benefits to executives, should the company’s prospects improve over time as a result of improving conditions that lie outside of executive control. Specific circumstances that will warrant additional consideration include:

- Companies that have deviated from historic equity granting practices, or priced equity awards at the lowest stock price in recent history; and

- Companies that have removed performance-based equity awards from their incentive programs or replaced them with time-based equity awards. This decision may be mitigated by applying longer vesting conditions as a guard against short-term macro-economic windfalls.

6. No Penalty For Late Bloomers. From the broad strokes of program review to details of annual grants, we recognize that different companies are on different timeframes. We will not penalize firms which did not provide extensive discussion of their broad response to the pandemic in their 2020 proxy season filings—but we will credit companies that did provide some insight into the board’s approach for their willingness to address the proverbial elephant in the room.

In particular, for firms which made significant adjustments to the pay program in the first months of 2020, we will review the overall framework of the program in the context of boom and bust times. We view short-sighted concessions negatively, particularly if the company has recovered meaningfully and no counterbalance to windfalls or compromises can be identified.

In cases where Glass Lewis opposed a pay program in 2020 based on adjustments in that year with respect to the pandemic, we will review the sum of the firm’s actions for the relevant fiscal year. In cases where a meaningful response to shareholders or even-handed actions later in the year are identified, we may refrain from basing a repeated negative voting recommendation on the same factors.

For strictly one-off decisions, we will avoid issuing recommendations solely on the same basis twice in almost all circumstances.

Less concern or credit will be assigned where changes or measures were tied to a defined time period. For example, a move to strictly time-based long-term incentives will be viewed less negatively if it is explicitly tied to only one grant cycle. Similarly, we will not penalize a company that rolls back its bonus deferral program on a temporary basis. That said, we will apply particularly close scrutiny to companies (and specific compensation committee members) that deviate from these defined temporary arrangements.

7. We Will Take Past History Into Account. Companies that have exhibited a healthy track record of good governance, pay-for-performance alignment and appropriate use of board discretion prior to the COVID-19 pandemic will likely be viewed through a more accommodating lens than companies that have not.

Equity Plan Proposals

Glass Lewis recognizes that the COVID-19 pandemic has created urgent near-term needs for many companies, who will have to make decisions that balance the competing needs to conserve cash, to continue to compensate employees, and to prevent excessive cost and dilution for shareholders. This may lead companies to take a different approach to equity granting, which can provide incentives for employees without drawing on cash reserves.

Our general approach to equity plan proposals, which includes both a quantitative assessment and a qualitative analysis, remains unchanged. However, in the context of COVID-19, certain proposal features may be flagged more frequently by our quantitative analysis.

Because many of the tests are relative and measured on a multiyear basis, we are not expecting to see dramatic swings for individual companies -but we do expect to see higher dilution levels as companies’ share prices drop, and we expect that most firms will need a bit more equity than they requested last year. Our model uses multiyear measurements and relative comparisons to smooth out some of this noise, but we remain cognizant of the challenges associated with prior year comparisons, and we will consider the following factors in analyzing share-requests:

- We will continue to require clear, sufficient justification for large share requests that result in significant dilution to shareholders, with our justification threshold set higher for companies that have made multiple large share requests within the past two Circumstances that we would consider sufficient justification in this regard may include:

- An urgent need to conserve cash; or

- The exhaustion of reasonable alternatives to compensate employees.

- We will consider whether the equity is being awarded to executives, or other Executive pay practices will factor more heavily into our analyses in cases where the majority of equity grants have historically been allocated to named executive officers. In these cases, our evaluation of executive pay practices in the say-on-pay proposal or pay-for-performance model may inform our recommendation for the equity plan proposal.

Repricing and Option Exchange Proposals

While Glass Lewis remains firmly opposed to the repricing of executive and director options, our guidelines recognize that there are certain circumstances in which macroeconomic or industry-wide trends may render repricing to be an acceptable course of action. The volatility of the market and the long lives of most options suggest that, for companies in less directly impacted, repricing would be premature. On the other hand, given the significant macroeconomic impacts of the COVID-19 pandemic, companies in highly affected industries may cite unforeseeable downturns outside of their executives’ control in seeking repricing approval. We will still expect these companies to demonstrate that they have explored an exhaustive list of alternatives, and that any eligible options are late enough in their term that a meaningful stock price recovery would be unlikely.

Where sufficient justification has been provided, we will continue to evaluate these proposals based on the specific company circumstances, and will only recommend support if the proposal meets certain additional conditions as listed in our guidelines.

Golden Parachute Proposals

The pressures of the pandemic may lead many companies to seek strategic alternatives, but the backdrop of a massive drop in value for many stakeholders simply cannot be ignored. While the common motivation cited for golden parachutes is to ensure executives negotiate the best deal possible, the option of a quick cash-out in volatile times raises the specter of pay-for-failure outcomes. When reviewing golden parachute proposals, Glass Lewis will consider the background of merger-related payments, along with the impact and treatment of earlier pay adjustments made in response to COVID-19.

Glass Lewis’ approach to executive pay has not changed. We will generally support proposals that effectively manage to align executive pay and performance, while also considering overall pay quantum, the quality of a company’s disclosure, and its responsiveness to material shareholder concerns. The guidance above is not intended to be prescriptive: there are a variety of decisions that boards may take to be successful, with their appropriateness dependent on each company’s specific circumstances. Our pragmatic, contextual approach provides us the flexibility to evaluate these compensation decisions even amid a global pandemic.

Regardless of a company’s particular circumstances, the effects of the COVID-19 pandemic have been felt to some extent by issuers and investors alike. As such, the burden on issuers will be higher than ever to provide thorough disclosure that allows their stakeholders to understand and evaluate any compensation-related decisions.