Print

PrintPaul Rose is the Robert J. Watkins/Procter & Gamble Professor of Law at Moritz College of Law at The Ohio State University. This post is based on his Manhattan Institute report. Related research from the Program on Corporate Governance includes The Agency Problems of Institutional Investors by Lucian Bebchuk, Alma Cohen, and Scott Hirst (discussed on the Forum here); Index Funds and the Future of Corporate Governance: Theory, Evidence, and Policy by Lucian Bebchuk and Scott Hirst (discussed on the forum here); and The Specter of the Giant Three by Lucian Bebchuk and Scott Hirst (discussed on the Forum here).

Executive Summary

In July 2020, the Securities and Exchange Commission (SEC) adopted a final Proxy Advisor Rule, establishing principles governing the conduct of proxy advisory firms, which help institutional investors execute voting on shareholder matters and advise them on how to vote their shares. The commission acted in response to growing concerns that two relatively small proxy advisory firms—Institutional Shareholder Services Inc. (ISS) and Glass, Lewis & Co. (Glass Lewis), each owned by private equity firms and together controlling more than 90% of the proxy advisory market—have assumed outsize influence over corporate voting matters. The commission’s new rule is intended to ensure that investment advisors are acting in the best interest of shareholders.

Among the issues implicated by the SEC’s Proxy Advisor Rule and concurrent Guidance Supplement is “robovoting,” whereby institutional investors mechanically follow a proxy advisor’s voting guidance without any independent review. In effect, an institutional investor transfers its fiduciary voting authority to a third party. Robovoting is a principal mechanism through which proxy advisory firms have assumed substantial influence over corporate shareholder voting outcomes.

This post is the first empirical assessment of robovoting in 2020, which, owing to the timing of the annual corporate “proxy season,” fell wholly after the SEC announced its proxy-advisor rulemaking process in November 2019 but mostly before the SEC released its final rule in July 2020. Because institutional investors are forward-looking, we can expect that at least some of these investors adjusted shareholder voting policies and disclosures in light of the commission’s rulemaking procedure.

Key Findings

- Overall, 114 institutional investors voted in lockstep alignment with either ISS or Glass Lewis in 2020: 86% of robovoting investors used ISS and 14% used Glass Lewis, reflecting the dominant market position of ISS.

- Robovoting institutional investors managed collectively more than $5 trillion in assets.

- Robovoting in 2020 declined marginally from 2019, in terms of the number of robovoting institutions (-5.79%), the total assets under management by robovoting institutions (-3.58%), and the total number of robovoted resolutions (-3.15%).

- Notwithstanding these declines, 33 institutional investors that did not robovote in line with a proxy advisor in 2019 did so in 2020. Fully 75% of these did so expressly, shifting toward a proxy advisor–driven voting strategy.

Nevertheless, among institutional investors that engaged in robovoting in 2020—either wholly or as part of an apparent custom voting plan—most did not make adequate disclosures to investors of their proxy voting strategies. Some institutional investors did, however—including those that adopted a robovoting strategy during the year, consistent with the SEC’s proxy advisory rule. This post highlights those examples, which other institutional investors may wish to consider as templates for their own disclosure regimes.

The modest trend away from robovoting in the 2020 proxy season may or may not portend more such movement in the future. Similar analyses of robovoting during the 2021 and 2022 proxy seasons should further illuminate the rule’s impact.

I. Introduction

Institutional investors own approximately 70% of all publicly traded equity shares. They dominate shareholder voting at U.S. publicly traded corporations, which is regulated by disclosure and other requirements set by the Securities and Exchange Commission (SEC). Executing shareholder voting requirements can be onerous for institutional investors. These investors rely heavily on proxy advisory firms to manage their proxy voting; these firms also provide institutional investors with research and vote recommendations on proxy-ballot voting issues. The evidence shows that proxy advisors can exert significant influence over voting outcomes. [1]

The role of these proxy advisory firms and how they influence shareholder voting have become a matter of public concern. In July 2020, the SEC adopted a final Proxy Advisor Rule designed to ensure that investment advisors— including institutional investors, as well as the proxy advisors who assist them—are acting in the best interest of shareholders. [2]

Because previous SEC actions effectively permitted investment advisors to outsource their voting obligations to proxy advisors, many institutional investors have tended automatically to follow these advisors’ recommendations—a phenomenon commonly called “robovoting.” This practice necessarily transfers fiduciary voting authority from institutional investors to two relatively small third parties: the proxy advisory firms Institutional Shareholder Services Inc. (ISS) and Glass, Lewis & Co. (Glass Lewis), each owned by private equity firms and together controlling more than 90% of the proxy advisory market.

Do institutional investors that robovote fulfill their fiduciary duty to shareholders? Evidence suggests that proxy advisory firms’ voting recommendations are subject to capture by voters with strong preferences for social concerns outside shareholder wealth maximization. [3] And evidence suggests, as well, the logical corollary: that proxy advisors’ shifts in voting recommendations are associated with stock-price drops. [4]

The role of proxy advisory firms and the impact of robovoting are matters of growing public concern. The incidence of robovoting has increased in recent years. [5] The growth of passive investing, [6] premised on a low-cost investment strategy tracking market aggregates, has shifted more investment dollars toward institutional investing firms that, almost by definition, cannot devote sizable resources to deploy on corporate governance matters, including shareholder voting.

The SEC’s initial proposal on proxy advisors, released in November 2019, considered disabling altogether pre-populated voting instructions on contested proxy matters—effectively precluding robovoting. Ultimately, it opted instead for a principles-based approach, predicated on ameliorating conflicts of interest and requiring disclosure to inform individual investors.

Although the summer 2020 Proxy Advisory Rule will not fully be in effect until the 2022 proxy season, we can expect that institutional investors might modify their practices in advance—both for the 2021 proxy season and, given the SEC’s November 2019 rulemaking release, during the 2020 proxy season. This post examines robovoting in the 2020 proxy season to identify and assess early trends. Section II summarizes the evolution of the SEC and other public reactions to the increasing influence of proxy advisors and the incidence of robovoting over the past decade. Section III summarizes institutional investors’ aggregate shareholder voting trends in 2020 and compares them with 2019, in order to identify changes in robovoting behavior during 2020’s proxy season—after the SEC had announced its rulemaking but before the July 2020 final rule was released (for the vast majority of shareholder votes). Section IV looks more granularly at how various institutional investors that have engaged in robovoting disclose their practices—and how, if at all, they have changed their policies and disclosures following the SEC’s November 2019 rulemaking announcement and July 2020 adoption of a final rule. Section V assesses how institutional investors that partially robovote a proxy advisor’s recommendations but partially adopt “custom voting” approaches have shifted their policies and approaches over the same period. Section VI concludes.

II. Recap of Regulatory and Congressional Involvement

Proxy advisors have been the subject of fierce debate and criticism for over two decades. They have been criticized for lacking transparency when developing and issuing vote recommendations, suffering from conflicts of interest that can taint their independence, and committing factual and analytical errors when researching and advising on proxy issues. The industry is also highly concentrated, with two firms—ISS and Glass Lewis—controlling over 90% of the market. Proxy advisors also wield powerful influence over corporate governance matters and have been demonstrated to significantly affect the outcome of shareholder votes.

In July 2020, the SEC issued a final rule and commission-level guidance that are the culmination of many years of effort by regulators, market participants, Republicans and Democrats in Congress, academics, and others to reform the proxy advisory industry. Several developments over the past decade helped inform the commission’s recent rulemaking and guidance:

- The SEC’s 2010 “proxy plumbing” concept release examined all aspects of the U.S. proxy system and highlighted a number of issues that market participants had raised over the proxy advisory industry. [7] The release specifically noted concerns of proxy advisory firm conflicts of interest, a lack of accuracy and transparency when formulating vote recommendations, and institutional investor overreliance on proxy advisory firms. SEC Commissioner Kathleen Casey noted at the time that “we … allow institutional investors to set their voting preferences in advance, to be executed on their behalf by … proxy advisers—in some cases to be voted automatically in conformity with the recommendations of those advisers.” Commissioner Casey was describing a practice that would now be termed “robovoting.” [8]

- The House Financial Services Subcommittee on Capital Markets and Government Sponsored Enterprises held the first congressional hearing on the proxy advisory industry, “Examining the Market Power and Impact of Proxy Advisory Firms,” in June 2013. [9]

- SEC Commissioner Daniel Gallagher called for the commission to take action on proxy advisors and clarify the voting responsibilities of asset managers, stating in 2013 that “the last thing we should want is for investment advisers to adopt a mindset that leads to them blindly casting their votes in line with a proxy advisor’s recommendations, especially given the fact that such recommendations are often not tailored to a fund’s unique strategy or investment goals.” [10]

- The SEC held a public roundtable on proxy advisors in December 2013, at which participants discussed conflicts within the industry, the quality of vote recommendations, and institutional investors’ reliance on proxy advisory firms. [11]

- In June 2014, the SEC provided a staff legal bulletin (SLB 20) regarding proxy voting responsibilities of investment advisors. [12] SLB 20 reaffirmed that fiduciary responsibilities permeate all aspects of proxy voting and provided guidance for investment advisors to fulfill their duties to shareholders. [13] The guidance also served as a reminder to investment advisors that their fiduciary duty obligates them to monitor the proxy advisory firms that they hire to ensure that vote recommendations are based on accurate information and that conflicts of interest are identified and addressed.

- In 2015, the House Financial Services Committee approved bipartisan legislation that would require proxy advisory firms to register with the SEC and to regularly demonstrate their ability to manage conflicts of interest and develop objective and accurate voting recommendations. A similar version of that legislation was approved by the full House of Representatives in 2017, again on a bipartisan basis.

- In September 2018, SEC staff withdrew two no-action letters that had been issued to proxy advisors Egan-Jones and ISS in 2004. [14] Critics argued that these letters led to an overreliance on proxy advisory firms in part by allowing investment advisors to cleanse any conflict of interest by casting votes in line with the recommendation of a third party. The withdrawal of the letters set the stage for subsequent SEC guidance and rulemaking related to proxy advisors.

- In November 2018, the SEC held another roundtable on the proxy process, with Chairman Jay Clayton stating that the roundtable would discuss “[w]hether various factors, including legal requirements, have resulted in investment advisors to funds and other clients relying on proxy advisory firms for information aggregation and voting recommendations to a greater extent than they should, and whether the extent of reliance on these firms is in the best interests of investment advisors and their clients, including funds and fund shareholders.” [15]

- Also in November 2018, Sen. Jack Reed (D., RI) introduced the Corporate Governance Fairness Act, which would establish an oversight regime and fiduciary standards for proxy advisors under the Investment Advisers Act. [16]

- In March 2019, SEC Commissioner Elad Roisman remarked: “Regardless of which voting policies and procedures an asset manager decides to adopt, there is a matter of implementing them when voting. I have seen some evidence indicating that asset managers may be relying heavily on proxy advisory firms in this area. Some have characterized this as ‘robo-voting,’ suggesting that proxy advisory firms are going too far in acting on behalf of their clients.” [17]

All these developments pointed to a broad consensus for changes to the proxy voting system and for the SEC to ensure that the votes of institutional investors are always cast in the best interest of individuals invested in mutual funds, exchange-traded funds, and other vehicles.

In August 2019, and as a result of the earlier withdrawal of the Egan-Jones and ISS no-action letters, the commission provided updated guidance regarding the proxy voting responsibilities of investment advisors under Rule 206(4)-6 of the Investment Advisers Act of 1940 (2019 SEC Guidance). [18] While the 2019 SEC Guidance recognized that proxy advisors provide a number of useful services to their clients, it emphasized that investment advisors are fiduciaries and owe each client “a fiduciary duty with respect to services undertaken on the client’s behalf, including voting.” [19] The 2019 SEC Guidance provides some direction with respect to robovoting, suggesting that investment advisors should consider additional steps to ensure that the voting determinations are “consistent with its voting policies and procedures and in the client’s best interest before the votes are cast.” [20] These additional steps might include:

- Assessing the “pre-populated” votes shown on the proxy advisory firm’s electronic voting platform before such votes are cast (such as by periodic sampling of the proxy advisory firm’s pre-populated votes); [21]

- Adopting policies and procedures that provide for consideration of additional information that may become available regarding a proposal (such as an issuer’s [a company’s] or a shareholder proponent’s subsequently filed proxy materials or other information conveyed by an issuer or a shareholder proponent to the investment advisor that would “reasonably be expected to affect the investment adviser’s voting determination”); [22] and

- Where the investment advisor’s voting policies and procedures “do not address how it should vote on a particular matter, or where the matter is highly contested or controversial,” potentially adopting a higher degree of analysis to assess whether any votes that it casts are in the clients’ best interests. [23]

The 2019 SEC Guidance noted that as part of the investment advisor’s compliance program, it should “review and document, no less frequently than annually, the adequacy of its voting policies and procedures to ensure that they have been formulated reasonably and implemented effectively, including whether the applicable policies and procedures continue to be reasonably designed to ensure that the adviser casts votes on behalf of its clients in the best interest of such clients.” [24]

SEC Proxy Advisor Rulemaking

In November 2019, the SEC issued a formal rule proposal that considered whether investment advisors that robovote are acting in the best interest of shareholders. [25] One potential solution raised in the proposal was the disabling of pre-populated voting instructions on contested proxy matters. [26] This would effectively have changed the default position on contested matters for proxy advisory firm clients to “abstain” and would increase the likelihood that investment advisors consider both the proxy firms’ and issuers’ points of view before casting their vote.

When the SEC adopted its final rule (Proxy Advisor Rule) in July 2020, however, it did not directly address robovoting and instead adopted a principles-based approach toward compliance. [27] The SEC recognized that “pre-population and automatic submission functions may enable proxy voting advice business clients to vote their proxies prior to registrants being able to provide a response to the proxy voting advice.” [28] Further, disabling or suspending robovoting when registrants have indicated that they intend to file responses to voting advice “could benefit the clients of proxy voting advice businesses to the extent that it increases the likelihood that the clients of the proxy voting advice businesses would review the registrants’ responses, and take them into consideration, before voting their proxies.” [29] Ultimately, the SEC determined that disabling or suspending robovoting in such cases could “give rise to timing pressures and other logistical challenges” and “increase costs for clients if they need to devote greater resources to managing the voting process as a result, which may in turn also reduce the value of the services of the proxy voting advice businesses.” [30] The commission said that it intends to “see how practice develops in light of the changes being adopted.” [31]

Concurrent with the Proxy Advisor Rule, the SEC adopted a commission-level guidance (Guidance Supplement) to help institutional investors better understand their responsibilities with respect to proxy voting. [32] The Guidance Supplement specifically identified two prevalent types of robovoting behavior by investment advisors. First (as also noted in the 2019 SEC Guidance), proxy advisory firms will sometimes provide investment advisors with electronic voting platforms that allow the proxy advisory firm to “populate each client’s votes shown on the proxy advisory firm’s electronic voting platform with the proxy advisory firm’s recommendations based on that client’s voting instructions to the firm,” a process the commission refers to as “pre-population.” [33] Proxy advisors also give investment advisors the option to “automatically submit the client’s votes to be counted,” a process the commission refers to as “automated voting.” [34] The SEC notes that pre-population and automated voting generally occur before the submission deadline for proxies to be voted at the shareholder meeting—in other words, the shares will be robovoted according to preset instructions, or simply in accordance with the proxy advisor’s general policies, if the investment advisor agrees and provides no other special instructions, regardless of the ultimate content of the proposals.

However, in the course of a reasonable investigation of proxy issues for which the investment advisor has voting responsibility, the advisor “may become aware that an issuer (the company) that is the subject of a voting recommendation intends to file or has filed additional soliciting materials with the Commission setting forth the issuer’s views regarding the voting recommendation.” [35] These materials may have an impact on the investment advisor’s voting decision and may become available after the investment advisor’s votes have been pre-populated but before the submission deadline for proxies to be voted at the shareholder meeting. In such a case, the Guidance Supplement provides direction on the steps that an investment advisor should take “to demonstrate that it is making voting determinations in a client’s best interest.” [36]

The Guidance Supplement states that an investment advisor should consider “whether its policies and procedures, including any policies and procedures with respect to automated voting of proxies, are reasonably designed to ensure that it exercises voting authority in its client’s best interest.” [37] This assessment should include whether the investment advisor’s policies and procedures address circumstances where the investment advisor becomes aware that an issuer intends to file, or has filed, additional materials pertinent to a voting matter with the SEC after the investment advisor has received the proxy advisory firm’s voting recommendation but before the submission deadline. In such cases, the Guidance Supplement states that “the investment adviser would likely need to consider such information prior to exercising voting authority in order to demonstrate that it is voting in its client’s best interest.” [38]

The Guidance Supplement suggests that investment advisors consider how the timing of pre-population and automated voting may result in proxy advisory firms possessing nonpublic information regarding how an investment advisor intends to vote a client’s securities, and the investment advisor “should also consider reviewing its agreements with any proxy advisory firms to determine whether the agreements would permit the proxy advisory firms to utilize this information in a manner that would not be in the best interest of the investment adviser’s client.” [39]

The Guidance Supplement clarifies that an investment advisor has an obligation, as a result of its duty of loyalty to clients, “to make full and fair disclosure to its clients of all material facts relating to the advisory relationship.” [40] This disclosure obligation includes material facts related to the exercise of voting authority with respect to client securities; further, the SEC notes, Rule 206(4)-6 and Form ADV require an investment advisor to describe to clients its voting policies and procedures. Specifically, the Guidance Supplement suggests that investment advisors consider disclosing:

- the extent of that use and under what circumstances it uses automated voting; and

- how its policies and procedures address the use of automated voting in cases where it becomes aware before the submission deadline for proxies to be voted at the shareholder meeting that an issuer intends to file or has filed additional soliciting materials with the Commission regarding a matter to be voted upon. [41]

The Guidance Supplement notes that these disclosures “may be necessary for the investment adviser to provide sufficiently specific information so that a client is able to understand the role of automated voting in the investment adviser’s exercise of voting authority.” [42]

III. Tracking Robovoting over Time

Background

Previous research has identified the prevalence of robovoting among institutional investors. The American Council for Capital Formation, for example, identified 175 asset managers, controlling more than $5 trillion in assets under management, that voted with ISS more than 95% of the time. [43] Its report also identified 82 asset managers, controlling over $1.3 trillion in assets, that voted with ISS 99% of the time. Similar research that I conducted identified nearly complete vote alignment from some investors, who voted in line with ISS over 99.5% of the time on at least 5,000 management resolutions. [44]

Recent research by Chong Shu reinforces earlier findings of the extensive influence of ISS and Glass Lewis. [45] In the study, he finds that both proxy advisors exert “strong influence,” with negative recommendations from ISS or Glass Lewis reducing clients’ votes by more than 20% in both director elections and say-on-pay proposals. Shu finds that “the influence is stronger on funds with smaller assets and on fund families that provide an index product,” [46] again suggesting that many funds—particularly those that are not able to afford extensive in-house corporate governance teams, due to small size or cost-sensitive business models, such as passive index funds—will tend to outsource their governance to proxy advisors. Unsurprisingly, then, the study finds that “the practice of robo-voting is increasing in prevalence, especially among ISS customers.” [47] In 2017, for example, 23% of ISS customers, with over $200 million in assets under management, followed ISS recommendations “almost entirely,” a dramatic increase from the 5% that almost entirely adopted ISS recommendations in 2007.

Because of the prevalence of robovoting, it is important to understand how proxy advisors develop recommendations. An analysis of proxy advisor policy development by David F. Larcker, Allen L. McCall, and Brian Tayan highlighted significant questions about how proxy advisors craft voting guidelines for their clients. [48] They note that while ISS, for example, touts an “open and transparent” process for developing proxy voting guidelines, “a careful examination does little to clarify the information they rely on in deciding to adopt a policy.” [49] It is unclear how ISS and Glass Lewis determine that a specific policy is “correct” and in the best interests of shareholders. The authors note that while proxy advisors obtain feedback from a wide variety of market participants, including trade groups, issuers, and investors, their review of an ISS policy survey revealed that ISS reported responses from only 97 institutional investors, many of which were likely its own clients. [50]

Such a finding is not surprising, of course. ISS and Glass Lewis are for-profit businesses that must respond to the interests and preferences of their clients; proxy advisors help shape corporate governance practices, but their policies are also shaped by the governance preferences of their clients. Shu’s work on this issue is instructive: “[P]roxy advisors cater to investors’ preferences—adjust their recommendations to align with fund preferences—because doing so can attract and retain customers.” Interestingly (and troublingly), Shu’s study finds that such catering is not aligned with shareholder wealth maximization, as stock prices drop when ISS changes a recommendation to match the preferences of investors it is trying to retain as clients. [51]

John Matsusaka and Chong Shu highlight similar concerns in another study. In their analysis of the impact of investors’ ESG (Environmental, Social, and Corporate Governance) interests on proxy advice, they argue that “the problem with proxy advice … does not stem from conflict of interest within advisory firms, but rather from their tendency to slant their advice toward the preferences of investors with intense preferences.” [52] They note that robovoting is likely to exacerbate non-wealth-maximizing behavior:

Because passive funds are unwilling to pay for high-quality advice—being primarily interested in vote execution services—our model implies that the consolidated proxy advisory firms would tilt their advice away from policies that maximize issuer value toward policies that give more weight to social issues. This provides an explanation for why proxy advisor recommendations may be disconnected from value maximization, and potentially slanted toward policy positions favored by [socially responsible investment] funds. [53]

The Amount and Directional Trend of Robovoting

Leveraging data from the most comprehensive source of shareholder voting data (Proxy Insight), it is possible to track historical, current, and future levels of proxy advisor alignment. For the purposes of this paper, and to properly track and monitor the observable changes in the market year-over-year, it is critical to determine an appropriate method of comparison.

To do so, strict thresholds were adopted for the analysis in order to ensure no false-positive identifications. To qualify in the analysis as a “robovoter,” an institutional investor must: 1) vote on a minimum of 100 separate resolutions in both 2019 and 2020; and 2) align with at least 99.5% of ISS or Glass Lewis “FOR” recommendations in 2019 and 2020. Importantly, the lower-limit threshold for the number of resolutions ensures a robust sample of total voting outcomes while the percentage threshold pairs with near-total vote alignment.

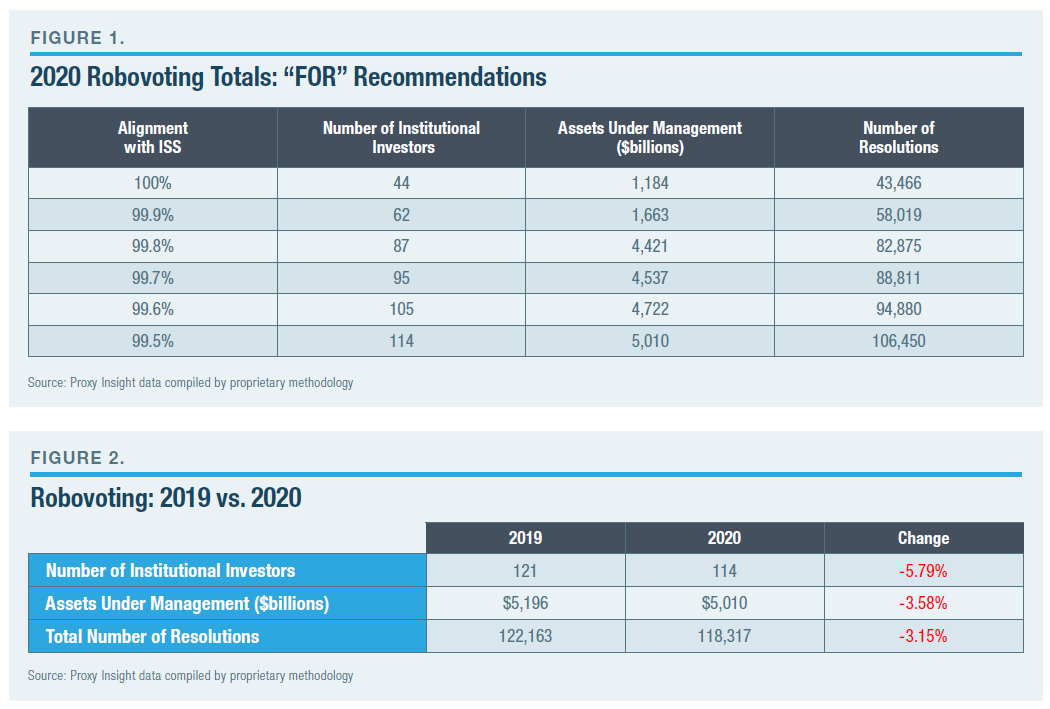

In total, 114 institutional investors voted in lockstep alignment with either ISS or Glass Lewis in 2020. Of the subset, 86% used ISS vs. 14% for Glass Lewis, reflecting the dominant market position of ISS (Figure 1).

The number of robovoting institutional investors in 2020 declined from 2019 by -5.79% (Figure 2). Similarly, the year-over-year decline in the total assets under management utilizing robovoting was -3.58%; and the total number of robovoted resolutions declined by -3.15%. This decline may reflect more oversight regarding proxy voting compliance, perhaps spurred by 2020’s ongoing SEC rulemaking. However, the key data to observe will be in the coming years, as the SEC’s

regulatory framework becomes effective. The total amount of assets under management robovoting with one of the two principal proxy advisors was still $5.01 trillion in 2020, demonstrating the oversize direct influence of proxy advisory firms.

Robovoting Policy Trends

To assess trends in institutional investors’ robovoting, it is necessary to go beyond tracking aggregates and examine more granularly the specific set of robovoting investors. How many of the 114 robovoting firms in 2020 also robovoted in 2019? Which firms updated their proxy voting policy to reduce their reliance on proxy advisors? What disclosure changes are observable when a firm adopts standard ISS policies to replace its previous policy? The key categories are in Figure 3.

The analysis shows 33 new robovoting institutional investors in 2020, with more than 75% of those being firms that updated their policy to match the ISS Proxy Voting Guidelines. One such firm is Chicago-based Segall Bryant & Hamill (SB&H), which manages over $20 billion in assets. In 2019, SB&H voted in alignment with ISS 97.2% of the time on more than 1,500 resolutions; but in 2020, its alignment with ISS jumped to 99.7%. In reviewing SB&H’s proxy policy, which was updated in 2020, the firm heavily updated its policies to include a robust definition of its delegation to ISS and to provide additional context to the responsibility and legal requirements of proxy voting decisions:

Previous Policy: The Adviser uses an outside service provider, Institutional Shareholder Services (“ISS”), to vote proxies.

Instructions are provided to the custodian to forward all proxies to ISS. ISS receives all proxies and votes them in a timely manner and in a manner consistent with the determination of the client’s best interests. Although many proxy proposals can be voted in accordance with ISS’ established guidelines (see “Guidelines” below), it is recognized that some proposals require special consideration which may dictate that the ISS and/or Adviser makes an exception to the Guidelines. ISS is also responsible for ensuring that all corporate action notices or requests which require shareholder action received are addressed in a timely manner and consistent action is taken across all similarly situated client accounts.

Updated 2020 Policy: The Board has delegated responsibility for decisions regarding voting for securities held by the Fund to the Fund’s Adviser. The Adviser relies on a thirdparty vendor, Institutional Shareholder Services (“ISS”), to research, vote and record all proxy ballots for the security positions maintained on clients’ behalf and for which the Adviser has voting authority. Annually, the Adviser reviews ISS’ independence and its Proxy Voting Guidelines. The Adviser follows ISS’ General Guidelines on most issues for shareholder votes.

These practices seek to respect shareholder rights and provide appropriate transparency, taking into account relevant laws, customs, and best practice codes of each market and region, as well as the right and responsibility of shareholders to make informed voting decisions. [54]

Figure 3. Robovoting Changes in 2020 (“FOR” Recommendations Only)

| Category | Definition | Number of Firms* | Assets Under Management in 2020 ($billions) | Total Resolutions |

|---|---|---|---|---|

| New Robovoter: Changed Policy to Follow Proxy Advisor | Investor (firm) was not a robovoter in 2019 but was a new robovoter in 2020, changing policy to match proxy advisor guidelines | 25 | 800 | 19,201 |

| New Robovoter: 2019 Voting History Missing | Firm with newly available proxy voting data for 2020 but 2019 data are missing | 4 | 81 | 3,837 |

| New Robovoter: Previously Below Qualification Thresholds | In 2019, firm voted on fewer than 100 resolutions and below 99.5% in alignment with a proxy advisor | 4 | 374 | 2,193 |

| Total New Robovoters | Newly identified robovoting firms in 2020 | 33 | 1,255 | 25,231 |

| Consistent Robovoter: Newly Met Size Threshold | Firm voted in alignment with proxy advisors in 2019 and 2020 but failed to vote on 100 resolutions in 2019 | 3 | 3 | 314 |

| Consistent Robovoter | Firm met alignment and resolution thresholds in 2020 and 2019 | 78 | 3,752 | 80,905 |

| Total Robovoters | Total robovoting firms, 2020 | 114 | 5,010 | 106,450 |

| Ceased Robovoting in 2020 | Firm ceased 2019 robovoting pattern in 2020 | 24 | 1,061 | 18,176 |

While the previous example shows the delegation in alignment with a proxy advisor, 24 investors updated their proxy policies in 2020 to vote independent of their proxy advisor. Firms that ended 2019 robovoting behavior in 2020 might have done so in anticipation of the ongoing SEC rulemaking.

IV. Review of Investment Advisor Proxy Voting Disclosures

In previous research, I noted how some asset managers disclose that their proxy voting practices are essentially outsourced to the guidelines and recommendations of proxy advisors, resulting in observed full voting alignment with proxy advisor guidelines. [55] For example, Sterling Capital Management, which voted 99.7% in line with Glass Lewis in 2019 and 2020, provides the following disclosure of its proxy voting policy:

The Proxy Group has engaged an Industry Service Provider (“ISP”) to: (i) provide research and vote recommendations; (ii) perform administrative tasks of receiving proxies and proxy statements; (iii) submit votes on behalf of Sterling; (iv) retain proxy voting records and information; and (v) report to Sterling on its activities. Sterling retains final authority and fiduciary responsibility for the voting of proxies. The Proxy Group has adopted the ISP’s Proxy Guidelines (the “Guidelines”). By following the ISP’s guidelines, Sterling seeks to mitigate potential conflicts of interest Sterling may have with respect to the proxies. [56]

Teacher Retirement System of Texas, which voted in line with ISS 100% of the time, similarly states:

To assist and advise TRS to vote its proxies prudently, the TRS Board shall retain a reputable, independent proxy advisory service (the “Proxy Advisor”) to analyze proxy issues, make voting recommendations, and vote proxies as TRS’ agent. In selecting the Proxy Advisor, the Board will have determined that the Proxy Advisors’ voting guidelines are reasonably designed to help ensure that TRS fulfills its fiduciary responsibilities governing proxy voting, with the exclusive objective of maximizing the longterm economic benefits of TRS pension plan participants and beneficiaries. [57]

The largest institutions, as well as those with a greater focus on corporate governance and proxy voting, tend to provide far greater detail on their use of proxy advisors and limitations to the relationship. Vanguard, which uses both ISS and Glass Lewis, states:

The Investment Stewardship team does not vote in lockstep with recommendations from proxy advisors (such as Institutional Shareholder Services (ISS) or Glass Lewis) when voting on behalf of the funds. Data from proxy advisors serve as one of many inputs into our research process. Even when a fund’s vote happens to be consistent with a proxy advisor’s recommendation, that decision is made independently. For some proxy proposals (which predominantly relate to corporate governance) the evaluation could result in overlapping voting outcomes. [58]

In addition to the engagement policy, Vanguard provides detailed policies on a range of corporate governance and proxy voting issues. [59] In voting on almost 800,000 proposals, Vanguard voted in line with ISS 94% of the time and Glass Lewis 86% of the time.

Other firms that also rely heavily or entirely on ISS do not always disclose the degree of their reliance. Stone Ridge Asset Management, for example, points to the ability of portfolio managers to override recommendations from the proxy advisors, despite voting in alignment with ISS 100% of the time in 2019 and 2020:

The ISS Guidelines are intended to provide a general overview by highlighting the key policies that ISS applies to companies listed in the applicable geographic region. However, ISS’ analysis is on a case-by-case basis, taking into consideration sector, industry and business performance factors. These guidelines have been approved by the Adviser and, although the Adviser intends to vote consistently with the voting recommendation of the Proxy Voting Service, upon the recommendation of the applicable portfolio managers, the Adviser may determine to override any recommendation made by the Proxy Voting Service or abstain from voting. [60]

Similarly, the New Mexico Educational Retirement Board, which voted in line with ISS 99.8% of the time in 2020 and 100% in 2019, states:

NMERB’s objective in proxy voting is to support proposals that maximize the value of the Fund’s investments over the long term. Proxy voting guidelines have been developed to ensure that the Fund is able to provide adequate assets to pay retirement benefits to the members of the Plan. NMERB believes that each portfolio’s Investment Manager is in the best position to assess the financial implications presented by proxy issues and the impact a particular vote may have on the value of a security. Consequently, NMERB generally assigns proxy voting responsibility to the Investment Managers responsible for the management of each Fund portfolio. The duty of loyalty requires that the voting fiduciary exercise proxy voting authority solely in the interests of members and beneficiaries of the NMERB. NMERB may retain the services of a proxy voting service to advise and assist staff in voting proxies for internally managed portfolios. Proxy voting will be in accordance with the guidelines listed below except in cases where the proxy voting service advice conflicts with the guidelines. [61]

From these disclosures, it appears that, at least so far in 2021, those same actors have not updated their approaches to proxy voting or their stated reliance on proxy advisors’ recommendations.

Changes in Proxy Vote Disclosures

The observed changes in proxy robovoting policies and disclosures do not tell the whole story. Many institutional investors will likely continue to revise their approaches in light of the recent rulemaking and other developments, which may not have been fully reflected in the proxy voting policies of investors. There may be further changes as the revised regulatory structure becomes established.

For example, Fisher Investments published the following proxy voting policy in August 2018, which resulted in an alignment of 99.8% with ISS’s recommendations:

Many proxy issues fall into well-defined, standardized categories, and as a result we have developed guidelines in conjunction with ISS for these categories. We currently work with ISS to further refine our Guidelines and to track and vote our clients’ proxies according to these Guidelines. While FI’s IPC utilizes ISS for shareholder vote recommendations, they reserve the right to override ISS recommendations as they see fit. Any IPC override is logged by the Securities Team Leader and reported to the Proxy Committee on a quarterly basis.

The Committee conducts an annual due diligence analysis on ISS, which includes a review of ISS’ SSA16 audit report and an annual visit with ISS to review any pertinent procedural updates or changes to their proxy voting guidelines. Furthermore, the Securities Operations and the Securities Analysis Team Leaders perform an annual review of the proxy voting recommendations of select strategies at the end of the first quarter to ensure ISS recommendations are in line with our overall voting guidelines.

FI votes proxies according to environmental resolution guidelines, as developed and maintained by Institutional Shareholder Services Inc. (ISS) in the Fisher Investments ESG strategies and in select accounts given account specific mandates regarding voting in accordance with ESG principles. [62]

Following the publication of revised engagement policies in line with European regulations, which included updated details on proxy voting, Fisher’s voting alignment with ISS fell by 2.5%, to 97.3% alignment, outside robovoting parameters. The reduced reliance potentially indicates the impact that regulations can have on how institutional investors utilize proxy advisors’ voting advice. [63]

Overall, however, the investors most likely to robovote tend not to provide meaningful disclosures, making it difficult to pinpoint any material impact on the guidelines from recent SEC regulations. On the other hand, the publication of voting guidelines around the time of the revised guidance from the SEC may provide a window into market practice as the regulatory structure develops.

Published in June 2020, one month before the initial guidance from the SEC, the following sets out the voting policy that resulted in RMB Capital voting increasingly in line with ISS, from 99.4% to 99.9% alignment between 2019 and 2020:

For clients who do not retain their right to vote proxies, RMB has contracted with a proxy advisory firm (the “Proxy Firm”) to handle administration and voting of client proxies. Additionally, the Proxy Firm provides research on proxy proposals and vote recommendations based on written guidelines, which are reviewed and approved from time to time by RMB’s SubCommittee (the “Committee”). The Committee is made up of executives of RMB. RMB, as a general matter, follows the voting recommendations of the Proxy Firm, though RMB retains the right to determine the vote on a particular proxy issue. Accordingly, there may be instances, including those in which the Proxy Firm recommends a vote in line with management, in which the Asset Management team or a Portfolio Manager for a private fund managed by RMB will provide the Committee with its written analysis as to why RMB should not vote as recommended by the Proxy Firm on a particular proxy issue. In those instances, the Committee may decide to vote contrary to the Proxy Firm recommendation if it is determined to be in the best interests of the clients. As a matter of course, members of the Committee will also review issues for which the Proxy Firm does not provide a recommendation. [64]

Even later in the year, in August 2020—after the SEC’s Proxy Advisor Rule in July but before its Guidance Supplement in September—Counsel Portfolio Services published its revised proxy voting guidelines, stating:

We may engage a third party to consult and provide recommendations, or to vote proxies on behalf of the Funds in a manner that is consistent with our policy. Counsel may also delegate to the sub-advisors, the authority to make all voting decisions concerning the securities held in the Counsel Funds they sub-advise on a discretionary basis in accordance with the applicable subadvisory agreement. [65]

Granted, the Proxy Advisor Rule had been only recently published, and the Guidance Supplement was yet to be finalized. Nonetheless, the aims of the SEC did not initially appear to be incorporated into the updates to Counsel’s approach, as alignment with ISS’s recommendations rose from 99% to 99.6% year-over-year. Indeed, even outside the level of robovoting, the lack of transparency over what third party was voting shares on behalf of the advisor’s clients is notable.

RMB and Counsel Portfolio Services are both new robovoters in 2020, despite updating guidelines while the SEC was attempting to address this practice. While it may be later in the year before there is evidence of policy impacts, it is somewhat concerning that not only did institutional investors continue to automatically follow proxy advisors during 2020, but other firms commenced similar practices during ongoing regulatory updates. Going forward, it will be important to observe disclosure updates provided by such firms to their investors as the SEC’s new rules and guidance on automated voting take hold.

V. Automated Custom Voting

Proxy advisors provide investment advisors, institutional investors, and other clients with a suite of voting recommendations in line with benchmark voting recommendations (a “benchmark policy”), or specialty voting policies (a “specialty policy”) that include policies tailored to specific investor classes and issue areas. ISS, for example, offers numerous specialty policies, including a U.S. Benchmark Policy, a European Benchmark Policy, a National Association of Pension Funds Policy (for the U.K.), an International Benchmark Policy, a Taft-Hartley Labor Policy, a “Socially Responsible” Policy, a Faith-Based Policy, and a Sustainability Policy. [66] In addition, proxy advisors’ clients may develop custom policies based on their own particular governance preferences.

In its recent rulemaking, the SEC addressed cases of custom voting. In its initially proposed rule, the SEC moved to classify proxy advisors’ voting recommendations based on custom criteria as “solicitations” under Rule 14a-1(l)(1)(iii). [67] Proxy solicitations—organized efforts to sway investors to vote for or against a shareholder voting matter—are subject to significant regulatory voting requirements. By reclassifying custom voting requirements as solicitations, the proposed rule would have required proxy advisors issuing custom voting recommendations to meet the same requirements to disclose conflicts of interest and notify companies as other proxy solicitations.

Over the course of its rulemaking, the SEC received feedback recommending the exclusion of advice based on institutional investors’ custom policies from the definitions of “solicit” and “solicitation.” [68] Many commenters’ concerns were based on subjecting individual investors’ custom policies to the proposed review and response mechanism outlined in the SEC’s proposed rules. Ultimately, acknowledging potential costs identified by commenters and satisfied that “benchmark policy proxy voting advice contains the bulk of the data, research, and analysis underlying custom policy proxy voting advice,” the commission opted to exclude custom advice from new Rule 14a-2(b)(9)(ii) requirements—or the required review and feedback period for voting advice. [69]

As Commissioner Allison Herren Lee noted in her dissent on the rules, a number of questions remain about the extent to which custom policies are based in large part or entirely on benchmark or specialty policies and the corresponding applicability of new Proxy Advisory Rule requirements. [70] At the same time, Republican commissioners continued to raise concerns about the potential for automatic voting in cases where custom voting is used. [71] During the comment process, Glass Lewis noted that while it works with clients to implement custom criteria, “it is not uncommon for an investor client to elect to implement the same policy as Glass Lewis for some or all of the issues up for vote.” [72] While custom advice now has a special regulatory status, to what extent is it similar to other advice that advisors may set and forget?

Robovoting Implications

Robovoting may result from the application of a variety of benchmark and specialty policies available to institutional investors, along with the automatic voting of custom set preferences by advisors. In the case of custom voting, as the SEC notes in its final rule commentary, “the relationship between proxy votes cast and voting recommendations provided to clients using clients’ custom policies has not, to date, been the subject of academic study.” [73] However, a number of concerns arise about the specific case of custom voting preferences, particularly in light of the SEC’s decision in the final rule to exempt custom voting from certain disclosure and notice requirements.

As mentioned, when formulating custom voting policies for their investors, proxy advisory firms allow clients to select preferences on a variety of governance matters and policy frameworks. According to proxy advisors, these preferences inform individual customization for proxy matters on a case-by-case basis. The growth of custom voting policies is marked. In 2019, ISS noted that it implemented more than 400 custom

voting policies on behalf of its clients and that as of October 1, 2019, approximately 88% of ISS’s top 100 clients used a custom proxy voting policy. [74] While not all governance matters merit special analysis and voting recommendations, evidence points to persistent automatic custom voting—notably, on material shareholder resolutions at several large investment funds and institutions.

Example of Custom Voting Policies: SWIB and State Street

A number of large asset managers, as noted above, will align with proxy advisor recommendations for most voting matters but employ custom voting policies for specific issues. The State of Wisconsin Investment Board (SWIB), for example, states that it will “generally follow the recommendation of its proxy advisor unless it has developed custom proxy voting guidelines.” [75] Although SWIB is not subject to regulation as an investment advisor by the SEC, it and other public pension plans are often heavily reliant on proxy advisors—which are regulated as investment advisors— and robovote according to their recommendations. Robovoting is thus a problem among institutional investors that calls for attention from more than the SEC and the U.S. Department of Labor. Other investment fiduciary regulators, including state legislatures and regulators overseeing public pension funds, should consider how these fiduciaries are using proxy advice.

Among its custom policies, SWIB will withhold votes for a director nominee under certain circumstances, including:

- For all countries other than Japan, the nominee is non-independent and board independence falls below 50%;

- The nominee is the CEO if he/she is serving as board chair unless he/she is the company founder; and

- The nominee is a non-independent director if he/she serves on key oversight committees (audit or compensation). [76]

Accordingly, SWIB’s alignment with ISS in 2020 measured 94.0% on all “FOR” recommendations— below the selected robovoting threshold of 99.5%. This would seem a result of independent analysis, unless SWIB’s alignment with ISS is analyzed with respect to specific-proposal issues, measuring specific governance items where the SWIB defaults to ISS voting recommendations year-over-year.

Figure 4. SWIB ISS Voting Alignment on Proposal Topic Categories Since June 2015*

| Customized Vote | Partial Robovote (FOR or AGAINST) | Full Robovote (All) | Total | |

|---|---|---|---|---|

| Management Proposals | 50 | 41 | 43 | 134 |

| Board of Directors | 9 | 5 | 4 | 18 |

| Committees & Reporting | 14 | 5 | 4 | 23 |

| Corporate Structure | 7 | 12 | 21 | 40 |

| Environmental & Social | 1 | – | 1 | 2 |

| General Governance | 5 | 3 | 11 | 19 |

| Remuneration | 14 | 16 | 2 | 32 |

| Shareholder Proposals | 11 | 12 | 18 | 41 |

| Board of Directors | 3 | 3 | 4 | 10 |

| Committees & Reporting | – | 1 | 1 | 2 |

| Corporate Structure | – | 2 | 2 | 4 |

| Environmental & Social | – | 5 | 7 | 12 |

| General Governance | 5 | – | 4 | 9 |

| Remuneration | 3 | 1 | – | 4 |

| Grand Total | 61 | 53 | 61 | 175 |

Source: Proxy Insight data compiled by proprietary methodology

*Full details are available in the Appendix to the complete publication (available here).

Figure 4 is an aggregate analysis of SWIB’s proxy voting over the past five years, exclusive of proposal topics that did not appear in at least 30 corporate annual meetings (to eliminate small samples). Proposal topics identified as “customized” indicate a field where the manager’s votes align with less than 99.5% of votes in both FOR & AGAINST recommendations. Proposal categories labeled as “Full Robovote” align with 99.5% or more of an advisor’s FOR & AGAINST “Partial Robovote” recommendations, while “Partial Robovote” topics are those where one recommendation direction exceeds the 99.5% threshold.

Data show that SWIB robovotes in alignment with ISS on 34% of proposal topics, while voting in partial lockstep an additional 30% of the time. It would appear that in these cases, SWIB is voting without independent analysis of advisor recommendations, potentially on material topics.

On management-sponsored proposals, SWIB robovotes in alignment with ISS on 32% of proposal topics. These include topics that have elicited greater variation of proxy advisor recommendations, not just issues wherein governance best practices dictate one particular recommendation. For example, in a review of management proposals for “Approval of Director Non-Compete Restrictions,” SWIB has followed ISS’s recommendation in 246 FOR recommendations and 29 AGAINST recommendations, a perfect 275-for-275 over the past five years.

Despite using custom policies, SWIB voted in lockstep with ISS on 43% of shareholder-sponsored topics and partially robovoted an additional 29%. Many of the topics are material to firm governance and concern important shareholder empowerment proposals. For example, SWIB robovotes on shareholder proposals to adopt or amend shareholder meeting policies, as well as on proposals to amend the right to call a special meeting. [77] SWIB also has historically voted in alignment with its proxy advisor on social reports, deferring all decisions on such matters to a third party.

Figure 5. SSGA ISS Voting Alignment on Proposal Topic Categories Since June 2015*

| Customized Vote | Partial Robovote (FOR or AGAINST) | Full Robovote (All) | Total | |

|---|---|---|---|---|

| Management Proposals | 125 | 44 | 30 | 199 |

| Board of Directors | 14 | 8 | 3 | 25 |

| Committees & Reporting | 14 | 11 | 10 | 35 |

| Corporate Structure | 48 | 11 | 9 | 68 |

| Environmental & Social | – | 1 | 2 | 3 |

| General Governance | 18 | 9 | 3 | 30 |

| Remuneration | 31 | 4 | 3 | 38 |

| Shareholder Proposals | 38 | 13 | 3 | 54 |

| Board of Directors | 8 | 3 | 1 | 12 |

| Committees & Reporting | 6 | – | – | 6 |

| Corporate Structure | 5 | 2 | – | 7 |

| Environmental & Social | 12 | 3 | – | 15 |

| General Governance | 5 | 3 | 1 | 9 |

| Remuneration | 2 | 2 | 1 | 5 |

| Grand Total | 163 | 57 | 33 | 253 |

Source: Proxy Insight data compiled by proprietary methodology

*Full details are available in the Appendix to the complete publication (available here).

This voting pattern contrasts with State Street Global Advisors (SSGA), which exhibits significantly more independence on corporate governance issues (Figure 5). For example, SSGA robovotes with ISS only 6% of the time on shareholder proposal topics, as compared with 43% for SWIB.

Custom Voting Disclosure

In the current regulatory environment, investment managers that combine custom voting policies along with other benchmark and specialty voting often fail to disclose the specific criteria used on a given voting matter to their investors. In a public comment to the SEC, SWIB stated: “SWIB, like many other pension funds and large institutional investors, allocates resources internally to track and determine votes using their own proxy voting guidelines. This is illustrated by the fact year over year SWIB routinely cast votes in opposition to our proxy advisor’s policy.” [78] The details of criteria and policies used in any given vote decision, however, remain undisclosed. Furthermore, asset managers are not required to disclose the extent to which they differ on proxy advisor recommendations on any issue-specific basis.

Further solutions are needed to provide investors with adequate disclosure as to how final votes are aligned with any proxy advisor employed by their investment manager. In a past paper, [79] I proposed requiring investment advisors—when issuing their annual N-PX forms detailing how they cast their votes at general meetings—to disclose how often their final votes aligned with any proxy advisor they employed, as well as to disclose what percentage of proxy advisor recommendations were reviewed internally by an investment manager. Such requirements would probably exempt state-run pension plans like SWIB; but in the general case, they would make it clear how reliant an investment advisor is on the advice of proxy advisors and thus better inform investment decisions.

SWIB’s policy again contrasts with State Street’s, which acknowledges the use of ISS but also clarifies how it employs an independent analysis. Importantly, the policy also describes how State Street manages information received after a proxy advisor recommendation has been received, as suggested by the Supplemental Guidance:

In order to facilitate our proxy voting process, we retain Institutional Shareholder Services Inc. (“ISS”), a firm with expertise in proxy voting and corporate governance. We utilize ISS to: (1) act as our proxy voting agent (providing State Street Global Advisors with vote execution and administration services), (2) assist in applying the Guidelines, (3) provide research and analysis relating to general corporate governance issues and specific proxy items, and (4) provide proxy voting guidelines in limited circumstances.

The Asset Stewardship Team reviews with ISS its Guidelines and the services that ISS provides to State Street Global Advisors on an annual or case-by-case basis. As part of its role as proxy agent and prior to providing vote execution services, ISS pre-populates on an electronic platform certain preliminary proxy votes in accordance with the proxy voting guidelines identified by State Street Global Advisors. On most routine proxy voting items (e.g., ratification of auditors), ISS will shortly before applicable submission deadlines use an automated process to affect the pre-populated proxy votes. To the extent the Asset Stewardship Team becomes aware of material new information within a reasonable period of time before ISS affects such votes, the Asset Stewardship Team will assess whether the pre-populated votes should be updated. [80]

VI. Conclusion

Proxy voting and the duties surrounding it have evolved from a relatively esoteric issue to one that is front and center for the SEC. Both public companies and institutional investors increasingly grapple with an ever-growing array of issues during annual meetings. Instead of weighing in only on core governance, board composition, or executive compensation matters, institutional investors now find themselves casting more votes on issues of an inherently social or political nature. Indeed, the commission under the Biden administration has already indicated that it is likely to increase focus on ESG issues as they relate to proxy voting and corporate disclosure. [81] It is more critical than ever that institutional investors are always casting votes in the best interest of the ultimate shareholders and Main Street investors whose savings are actually at risk.

Proxy advisors have played, and will continue to play, an important role in the proxy ecosystem, and their research and recommendations will remain a valuable tool for institutional investors. However, given the inherent flaws that have existed in the proxy advisory industry and the SEC’s efforts to address those flaws through the Proxy Advisor Rule, institutional investors should be reviewing and updating, as necessary, their policies and procedures regarding proxy voting.

While most provisions of the SEC’s Proxy Voting Rule and Supplemental Guidance will not be in place until the 2022 proxy season, the Proxy Advisor Rule and Supplemental Guidance together reaffirm that investment advisors have a fiduciary obligation to conduct sufficient due diligence when proxy voting and to always vote in a manner that enhances economic value for shareholders. This post is intended to help inform policymakers, public companies, and investors regarding the practice of robovoting and the need for ongoing regulatory scrutiny. The Manhattan Institute, through its Proxy Monitor project, plans to release subsequent data and research regarding robovoting and the voting behavior of institutional investors during the upcoming 2021 proxy season.

Proxy advisors are likely to increase in their reach and influence in the coming years, and institutional investors will continue to use robovoting strategies to lower their own costs. The clients of institutional investors—the Main Street investors who are the ultimate beneficiaries of fiduciary shareholder voting obligations—deserve full and fair information on how institutional investors are using proxy advisory services, including through robovoting practices.

The complete publication, including appendix, is available here.

Endnotes

1See James R. Copland, David F. Larcker, and Brian Tayan, “Proxy Advisory Firms: Empirical Evidence and the Case for Reform,” Manhattan Institute (MI), May 2018.(go back)

2Exemptions from the Proxy Rules for Proxy Voting Advice, 85 FR 55082, Sept. 3, 2020 (Release No. 34-89372, July 22, 2020).(go back)

3John G. Matsusaka and Chong Shu, “A Theory of Proxy Advice When Investors Have Social Goals,” USC Marshall School of Business Research Paper, ssrn.com, Oct. 26, 2020.(go back)

4Chong Shu, “The Proxy Advisory Industry: Influencing and Being Influenced,” USC Marshall School of Business Research Paper, ssrn.com, Mar. 19, 2021.(go back)

5Ibid.(go back)

6A recent Federal Reserve study notes that “passively managed funds hold a rising share of total financial assets”:

“As of March 2020, U.S. stocks held in passive mutual funds (MFs) and exchange-traded funds (ETFs) accounted for about 14 percent of the domestic equity market, up from less than four percent in 2005. The aggregate passive share, including passively managed holdings outside of MFs and ETFs, is still larger. For example, BlackRock estimated that passive investors owned 18 percent of all global equity at the end of 2016, with most of the holdings outside the MF and ETF sectors.”(go back)

See Kenechukwu Anadu et al., “The Shift from Active to Passive Investing: Risks to Financial Stability?” Federal Reserve Bank of Boston, Working Paper SRA 18–04, May 15, 2020.

7Concept Release on the U.S. Proxy System, 75 FR 42982, July 22, 2010 (Release Nos. 34-62495, IC-3052, IC-29340, July 14, 2010).(go back)

8Commissioner Kathleen L. Casey, “Statement at Open Meeting on Proxy Mechanics Concept Release,” U.S. Securities and Exchange Commission (SEC), July 14, 2010. In a letter submitted for the concept release, Johnson & Johnson stated that over the course of three proxy seasons, 13.4%– 17.9% of its shares had been voted in line within one day of its proxy advisor’s recommendation.(go back)

9Subcommittee on Capital Markets and Government Sponsored Enterprises, “Examining the Market Power and Impact of Proxy Advisory Firms,” June 5, 2013.(go back)

10Commissioner Daniel M. Gallagher, “Remarks at Society of Corporate Secretaries & Governance Professionals,” SEC, July 11, 2013.(go back)

11“Proxy Advisory Services Roundtable,” SEC, Dec. 5, 2013.(go back)

12SEC, Staff Legal Bulletin No. 20 (IM/CF), “Proxy Voting: Proxy Voting Responsibilities of Investment Advisers and Availability of Exemptions from the Proxy Rules for Proxy Advisory Firms,” June 30, 2014.(go back)

13Ibid.(go back)

14SEC, “Statement Regarding Staff Proxy Advisory Letters,” Sept. 13, 2018.(go back)

15SEC, “Roundtable on the Proxy Process,” Nov. 15, 2018. Some commenters to the roundtable, including the National Investor Relations Institute (NIRI), expressed concern with robovoting policies. The NIRI letter argued, e.g.: “A proxy advisory firm should not be permitted to offer a voting service that allows a client to establish, in advance of receiving proxy materials for a particular shareholder meeting, general guidelines or policies that the proxy advisory firm is then authorized or permitted to apply for the purpose of making and executing voting decisions on behalf of the client” and that “investment advisers should not be permitted to ‘outsource’ their voting decisions in this manner.”(go back)

16S. 3614, 115th Congress.(go back)

17Commissioner Elad Roisman, “Keynote Remarks: ICI Mutual Funds and Investment Management Conference,” Mar. 18, 2019.(go back)

18Commission Guidance Regarding Proxy Voting Responsibilities of Investment Advisers, 84 FR 47420, Sept. 10, 2019 (Release Nos. IA-5325, IC-33605, Aug. 21, 2019) [hereinafter “2019 SEC Guidance”].(go back)

19Ibid.(go back)

20Ibid.(go back)

21Ibid.(go back)

22Ibid.(go back)

23Ibid.(go back)

24Ibid.(go back)

25Amendments to Exemptions from the Proxy Rules for Proxy Voting Advice, 84 FR 66518, Dec. 4, 2019 (Release No. 34-87457, Nov. 5, 2019).(go back)

26Ibid., 66: “Should we amend Rules 14a-2(b)(1) and 14a-2(b)(3) so that the availability of the exemptions is conditioned on a proxy voting advice business structuring its electronic voting platform to disable the automatic submission of votes in instances where a registrant has submitted a response to the voting advice? Should we require proxy voting advice businesses to disable the automatic submission of votes unless a client clicks on the hyperlink and/or accesses the registrant’s (or certain other soliciting persons’) response, or otherwise confirms any pre-populated voting choices before the proxy advisor submits the votes to be counted?”; and 116: Reasonable Alternative #5: “Require disabling of pre-populated and automatic voting mechanisms.”(go back)

27Exemptions from the Proxy Rules for Proxy Voting Advice, 85 FR 55082.(go back)

28Ibid.(go back)

29Ibid.(go back)

30Ibid.(go back)

31Ibid.(go back)

32Supplement to Commission Guidance Regarding Proxy Voting Responsibilities of Investment Advisers, 85 FR 55155 (Sept. 3, 2020).(go back)

33Ibid.(go back)

34Ibid.(go back)

35Ibid.(go back)

36Ibid.(go back)

37Ibid.(go back)

38Ibid.(go back)

39Ibid.(go back)

40Ibid.(go back)

41Ibid.(go back)

42Ibid.: “In those cases, the client may not, without this disclosure, have sufficiently specific information to provide informed consent with respect to the use of automated voting as a means of exercising voting authority either (a) for purposes of agreeing to the scope of the relationship or (b) as it relates to the investment adviser’s obligation, under its duty of loyalty, to provide full and fair disclosure relating to the advisory relationship.”(go back)

43Timothy M. Doyle, “The Realities of Robo-Voting,” American Council for Capital Formation, November 2018.(go back)

44Paul Rose, “Robovoting and Proxy Vote Disclosure,” ssrn.com, Nov. 13, 2019.(go back)

45Shu, “The Proxy Advisory Industry.”(go back)

46Ibid., 23.(go back)

47Ibid.(go back)

48David F. Larcker, Allen L. McCall, and Brian Tayan, “And Then a Miracle Happens!: How Do Proxy Advisory Firms Develop Their Voting Recommendations?” Stanford Graduate School of Business Research Paper, ssrn.com, Oct. 28, 2013.(go back)

49Ibid.(go back)

50Ibid.(go back)

51Shu, “The Proxy Advisory Industry.” When examining “proxy advisor’s recommendations on firms’ [cumulative abnormal returns] for proposals where they do or do not change recommendations,” Shu finds that “there is a negative 2% abnormal return if the vote outcome adopts ISS’s changed recommendations. This suggests that most shareholders do not appreciate ISS’s changed recommendations, or in other words, ISS’s catering is not aligned with value-maximization.”(go back)

52Matsusaka and Shu, “A Theory of Proxy Advice.”(go back)

53Ibid.(go back)

54The new policy: Segall Bryant & Hamill Trust, Statement of Additional Information, Feb. 19, 2021. The old policy: Segall Bryant & Hamill Trust, Statement of Additional Information, Jan. 27, 2017.(go back)

55Rose, “Robovoting and Proxy Vote Disclosure.”(go back)

56Sterling Capital Management, “Statement of Additional Information,” Feb. 1, 2021, 157. 57 Teacher Retirement System of Texas, Proxy Voting Policy, effective from Apr. 7, 2017. 58 Vanguard’s Engagement Policy.(go back)

57Teacher Retirement System of Texas, Proxy Voting Policy, effective from Apr. 7, 2017.(go back)

58Vanguard-Engagement-Statement.pdf.(go back)

59Vanguard’s Corporate Governance Principles.(go back)

60Stone Ridge Trust, Statement of Additional Information, Appendix B: Stone Ridge Asset Management LLC Proxy Voting Policies and Procedures, Mar. 1, 2021.(go back)

61New Mexico Educational Retirement Board, Investment Policy Statement, Dec. 4, 2020.(go back)

62Fisher Investments, Proxy Voting, August 2018.(go back)

63Fisher Investments, Engagement Policy.(go back)

64RMB Capital Management, LLC, Disclosure Brochure (Form ADV Part 2A), June 22, 2020.(go back)

65Counsel Portfolio Services Inc., Annual Information Form, Aug. 6, 2020, Offering Series O Securities.(go back)

66ISS, Custom Policy and Research.(go back)

67Exemptions from the Proxy Rules for Proxy Voting Advice 85 FR 55082. As courts and the SEC have long noted, the definition of “solicitation” broadly encompasses any communication with shareholders in a manner reasonably calculated to result in the procurement, execution, or revocation of a proxy. Ibid., 55088.(go back)

68Ibid.(go back)

69Ibid., 114. In its discussion of commenter concerns, SEC stated (ibid., 120): “Commenters also argued that requiring proxy voting advice businesses to share with registrants proxy voting advice that is based on custom policies would unconstitutionally compel them to disclose confidential client information. Our decision to exclude such advice from Rule 14a-2(b)(9)(ii) should eliminate that concern.”(go back)

70Commissioner Allison Herren Lee, “Paying More for Less: Higher Costs for 55155, Less Accountability for Management,” July 22, 2020.(go back)

71“Supplement to Commission Guidance Regarding Proxy Voting Responsibilities of Investment Advisers,” 85 FR 55155.(go back)

72Comment Letter of Glass Lewis Re File No. S7-22-19, Amendments to Exemptions from the Proxy Rules for Proxy Voting Advice Release, Feb. 3, 2020.(go back)

73Exemptions from the Proxy Rules for Proxy Voting Advice, 85 FR 55082.(go back)

74Comment Letter of ISS Re File No. S7-22-19: Amendments to Exemptions from the Proxy Rules for Proxy Voting Advice, Jan. 31, 2020.(go back)

75State of Wisconsin Investment Board, “Corporate Governance, Proxy Voting Guidelines,” Aug 28, 2018.(go back)

76Ibid., 1.(go back)

77See Appendix, SWIB 5-Year Voting Alignment with ISS by Topic.(go back)

78Comment Letter of State of Wisconsin Investment Board Re File No. S7-22-19, Amendments to Exemptions from the Proxy Rules for Proxy Voting Advice, Feb. 3, 2020.(go back)

79Rose, “Robovoting and Proxy Vote Disclosure.”(go back)

80State Street Global Advisors, “Global Proxy Voting and Engagement Principles,” March 2021.(go back)

81Andrew Ross Sorkin et al., “When Doing Well Means Doing Good: The S.E.C. Is Making E.S.G. a Priority,” New York Times, Mar. 21, 2021.(go back)