Print

PrintChris Miller is Vice President and Jelmer Laks is an Associate with ISS Governance Research, Institutional Shareholder Services, Inc. This post is based on their ISS memorandum. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance by Lucian A. Bebchuk and Roberto Tallarita (discussed on the Forum here); Companies Should Maximize Shareholder Welfare Not Market Value by Oliver Hart and Luigi Zingales (discussed on the Forum here); and Reconciling Fiduciary Duty and Social Conscience: The Law and Economics of ESG Investing by a Trustee by Max M. Schanzenbach and Robert H. Sitkoff (discussed on the Forum here).

Anthropocene:

“the current geological age, viewed as the period during which human activity has been the dominant influence on climate and the environment.”

Key Takeaways

- The 2021 U.S. proxy voting season marked an escalation of shareholder engagement on climate-related issues as well as an expansion of tactics.

- Many investors are moving beyond requests for disclosure to voting against directors for

perceived failures of climate risk mitigation - The 2021 season saw the advent of the Say-On-Climate proposal, an attempt to secure a

dedicated ballot item that would enable investors to express views on a company’s management of climate-related risks on a recurring basis. - The number of climate-related shareholder proposals as well as levels of support have grown over the past 3 years.

- The recent IPCC AR6 Synthesis report and 2021 US Proxy Season trends outlined in this report demonstrate that the days of regarding climate disclosure and risk as “non-financial” niche issues targeted by a relatively small number of activists and NGOs are over.

Introduction

On Monday, August 9th, the Intergovernmental Panel on Climate Change (IPCC) issued its Sixth Assessment Report (AR6). Released against a backdrop of wildfires in California, Greece, and Turkey, floods in Germany, Belgium, and China, and record heat in Canada and Siberia, the report states unequivocally that “human influence has warmed the climate at a rate that is unprecedented in at least the last 2000 years,” and that “global warming of 1.5°C and 2°C will be exceeded during the 21st century unless deep reductions in CO2 and other greenhouse gas emissions occur in the coming decades.” [1]

Responding to the report’s findings, United Nations Secretary-General Antonio Guterres stated that “the climate crisis poses enormous financial risk to investment managers, asset owners, and businesses,” and added that “these risks should be measured, disclosed and mitigated.” [2] The ability of investors to assess climate risks, such as whether companies are taking steps to reduce emissions at a rate consistent with 1.5°C and 2°C scenarios, depends on a variety of factors, including regulatory frameworks and market norms related to disclosure and engagement. In Europe, investors have been able to review disclosures generated by the EU’s Non-Financial Reporting Directive (NFDR) since 2018. In addition to the NFDR, the EU’s Sustainable Finance Disclosure Regulations (SFDR) and Taxonomy regulation impose a level of transparency and consistency that allows for a degree of benchmarking. In the US, by contrast, climate-related disclosure is largely voluntary. While the US Securities and Exchange Commission (SEC) recently initiated a climate change disclosure rulemaking process, it is not yet clear whether the framework that emerges will enable investors to “measure” and “mitigate” climate-related risks on a consistent, market-wide basis. During the 2021 US proxy season, investors in US companies seeking to “measure” and “mitigate” climate-related risks were compelled to focus on individual companies, using tactics that have evolved in the absence of a mandatory disclosure framework.

Climate-Related Shareholder Engagement During the 2021 Proxy Voting Season

The 2021 U.S. proxy voting season marked an escalation of shareholder engagement on climate-related issues as well as an expansion of tactics. In addition to submitting shareholder proposals,

shareholders and shareholder advocacy groups launched a large number of vote-no campaigns as well as a successful proxy contest at Exxon resulting in the election of 3 operation and climate-focused board members. [3] The number of climate-related shareholder proposals has grown over the past 3 years and the 2021 season saw the advent of Say-On-Climate proposals, an attempt to secure a dedicated ballot item that would enable investors to express views on a company’s management of climate-related risks on a recurring basis. In addition to shareholders asking for a right for regular review of a company’s climate transition plan, Moody’s Corporation and S&P Global put forth a management proposal asking for shareholder approval of their transition plans.

2021 U.S. Shareholder Proposals

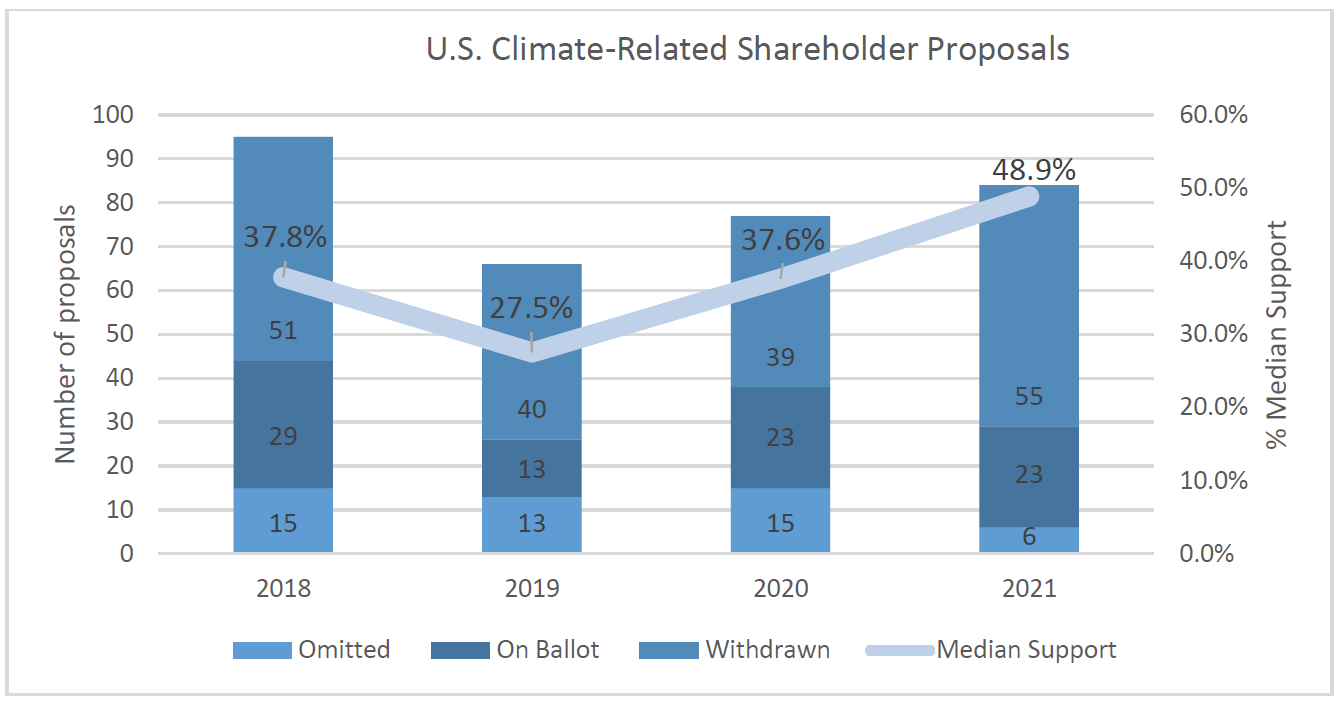

In addition to an increase in the overall number of shareholder proposals and initiatives targeting additional ballot items, the levels of support for climate-related shareholder proposals continued to increase. Median support of such proposals hit 48.9 percent during 2021 season, up from 37.6 percent in the previous year. This continued increase in the level of support for a variety of climate-related proposals signals a high level of engagement from many shareholders on this topic.

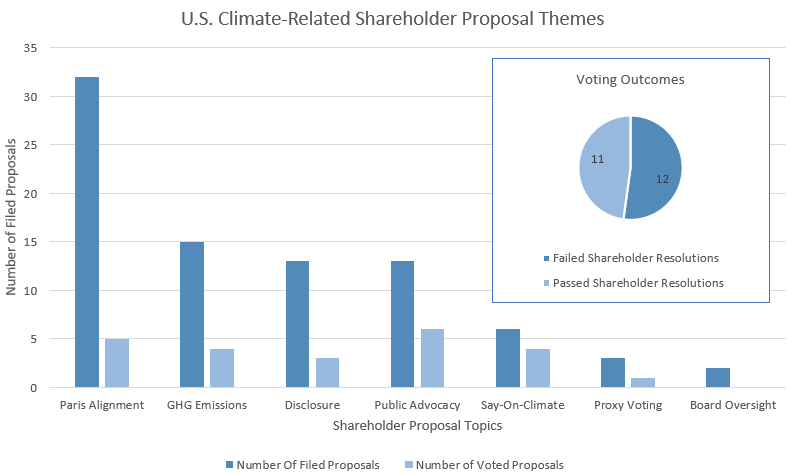

84 climate-related shareholder proposals were filed at companies whose AGMs were held as of this report. The vast majority of filed shareholder proposals focused on the reporting on or achievement of targets aligned with Paris Agreement goals. Many shareholders have a strong focus on reporting and targets aligned with Net Zero by 2050 (consistent with a 1.5-degree scenario) and 2 degrees pathways, thresholds set by the scientific community as critical to preventing large scale and severe impacts of climate change. The low number of proposals making it to a vote indicates that companies and boards are sensitive to this issue and willing to engage with shareholders on a resolution. A significantly lower number of proposals were filed requesting disclosure and reduction of GHG emissions more generally; disclosure around climate topics not specific to emissions; and reporting on lobbying and public advocacy efforts related to potential climate regulations undertaken by companies.

The 2021 season also saw the advent of an entirely new type of shareholder proposal requesting regular review and opportunity to vote on a company’s climate plans, the so-called say-on-climate proposal. Several proposals were also submitted targeting company policies on proxy voting relating to climate as well as insight and disclosure regarding board oversight. Of the 84 climate-related shareholder proposals filed in 2021, 23 made it to a vote. Almost half of the voted proposals received majority support from shareholders.

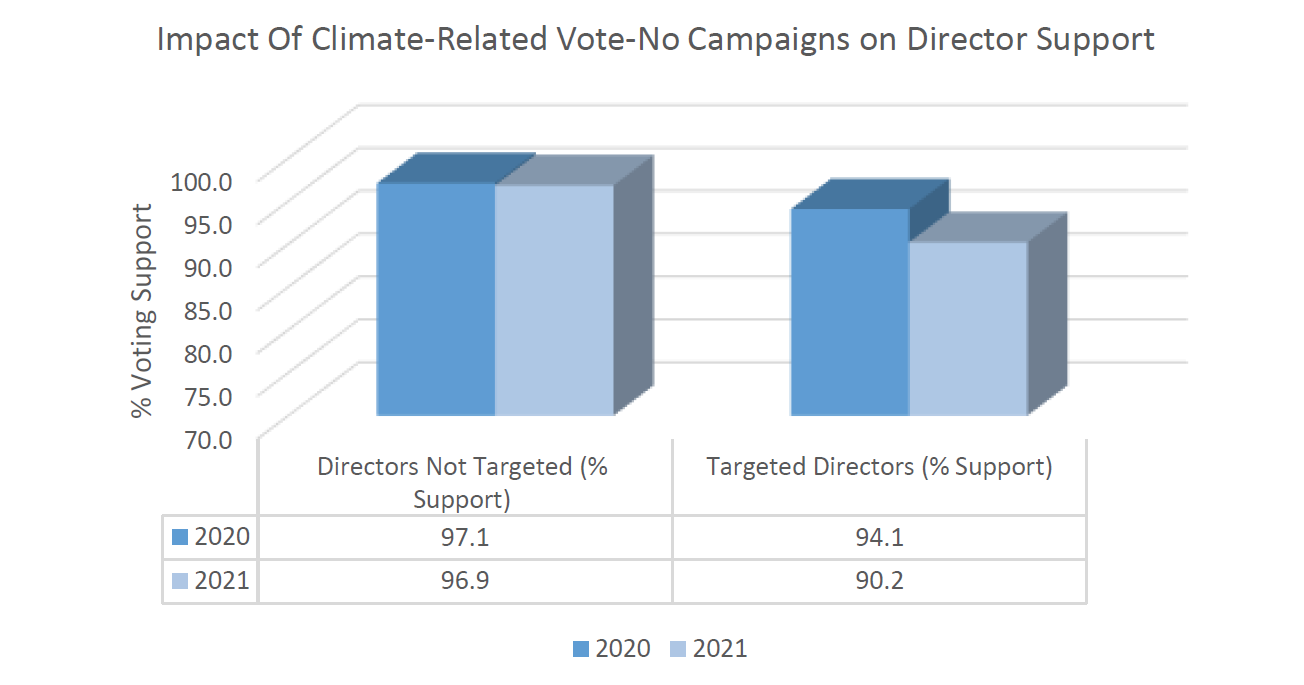

Climate Driven Vote-No Campaigns

The 2021 season saw a high-profile proxy contest at Exxon initiated by Engine No.1, targeting specific directors for reasons at least partially motivated by climate-related concerns. In addition, 19 climate-related vote-no campaigns were pursued at companies in the Electricity Generation, Oil and Gas, and Banking sectors. The vote-no campaigns were all run by Majority Action, “a nonprofit, non-partisan organization that empowers shareholders to hold corporations accountable to high standards of corporate governance [4] and long-term value creation.” The organization argues that votes are warranted against directors at companies for failing to implement plans consistent with limiting global warming to 1.5 degrees.

While widely publicized, [5] the vote-no campaigns did not have an overall significant impact on vote outcomes of director elections targeted by the campaign versus those that were not. However, the outcome of the Exxon proxy contest suggests that seeking to hold companies and specific directors accountable for perceived failures of climate-related risk management could be a tactic used again in the future.

The Future of Climate-Related Voting Actions

As the effects of the climate crisis become more widespread and difficult to ignore, governments, NGOs, businesses, and investors will face increasing pressure to address the threats posed by global warming. In the US, while it is not yet clear what impact the SEC’s climate disclosure rule making process will have on investor’s ability to assess risk, it is likely that shareholders will continue to file and support proposals seeking additional information concerning issuers’ decarbonization strategies. In addition, while the Vote-No campaigns initiated by Majority Action did not result in significantly lower levels of support for targeted directors in 2021, the tactic of holding directors accountable for perceived failures of climate-risk mitigation has not only been embraced by NGOs and activist investors: in its most recent Stewardship Report, BlackRock reported voting against 255 directors for climate-related reasons in the period ended June 30th, up from 55 a year earlier. [6] Indeed, the outcome of the Exxon proxy contest suggests investors will see many more attempts to hold directors accountable for climate-related issues going forward.

It is too early to know whether the addition of a dedicated ballot item related to climate transition plans, as called for by the Children Investment Fund’s Say on Climate initiative, will impact the number and support levels of shareholder proposals or relieve pressure on directors at companies perceived as failing to adequately manage climate-related risks. What is certain, however, and what the IPCC report and 2021 US Proxy Season demonstrate, is that the days of regarding climate disclosure and risk management as “non-financial” niche issues targeted by a relatively small number of activists and NGOs are over.

Endnotes

1https://www.ipcc.ch/report/ar6/wg1/downloads/report/IPCC_AR6_WGI_SPM.pdf(go back)

2https://www.un.org/sg/en/content/secretary-generals-statement-the-ipcc-working-group-1-report-the-physical-science-basis-of-the-sixth-assessment(go back)

3https://corpgov.law.harvard.edu/2021/07/05/why-exxonmobils-proxy-contest-loss-is-a-wakeup-call-for-all-boards/(go back)

4https://www.proxyvoting.majorityaction.us/(go back)

5https://www.majorityaction.us/press(go back)

6https://www.blackrock.com/corporate/literature/publication/2021-voting-spotlight-full-report.pdf(go back)