Print

PrintHolly Pettingale is Director and Stéphane de Maupeou and Peter Reilly are Senior Directors at FTI Consulting. This post is based on an FTI Consulting memorandum by Ms. Pettingale, Mr. de Maupeou, Mr. Reilly, and Joel Kuenzer. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) and Will Corporations Deliver Value to All Stakeholders?, both by Lucian A. Bebchuk and Roberto Tallarita; and For Whom Corporate Leaders Bargain (discussed on the Forum here) and Stakeholder Capitalism in the Time of COVID, both by Lucian Bebchuk, Kobi Kastiel, and Roberto Tallarita (discussed on the Forum here).

While the period up to 2018 was marked by an absence of ESG and sustainability focused regulatory pressure, in the period since, there have been efforts across the globe to ensure investors, financiers and companies pursue more sustainable business practices. At the forefront of those efforts has been the EU, which is seeking to become the ‘first climate-neutral continent’. [1] A core component of those efforts is the EU Taxonomy (the ‘Taxonomy’) [2], which is part of a suite of wider regulation of market participants, including the Sustainable Finance Disclosure Regulation (SFDR) [3] and the Corporate Sustainability Reporting Directive (CSRD). [4]

Corporates have, over the past two years in particular, made significant strides to respond to investor and regulatory pressure on ESG reporting. From 2022, however, that pressure is likely to ramp up further, with a number of regulations being adopted or coming into effect. Among them, the Taxonomy will attempt to, for the first time, determine what is and what is not ‘green’. While some companies will remain outside of those designations over the short-term, the Taxonomy is the starting point for the development of the regulatory labelling of businesses—and their activities—as ‘green friendly’ or ‘green hostile’. In the face of what is likely to be an ever-more regulated aspect of corporate reporting, all companies should be looking at these latest steps to evaluate business activities and be prepared to report against more demanding regulations in the period ahead.

As a starting point, we attempt to set out a path for all companies, with activities within or outside of the Taxonomy’s current scope.

What is the EU Taxonomy?

The Taxonomy is a classification system for organisations to identify which of their economic activities, or the economic activities they invest in, can be deemed ‘environmentally sustainable’. The Taxonomy defines environmentally sustainable activities as economic activities that make a substantial contribution to at least one of the EU’s environmental objectives, while, at the same time, not significantly harming any of these objectives and meeting minimum social safeguards. All financial market participants, all large companies and listed SMEs businesses will need to report against the Taxonomy. (Subject to the outcome of the EU political negotiations on the Corporate Sustainability Reporting Directive.)

In order for an economic activity to meet the definition of environmentally sustainable and thus be considered Taxonomy-aligned, it must:

- Contribute substantially to one or more of the six environmental objectives, and comply with the relevant technical screening criteria

- Do no significant harm (DNSH) to any other environmental objective

- Comply with minimum social safeguards

Nonetheless, an “intermediate” stage of compliance is allowed, by which activities can just be considered “taxonomy-eligible”. The distinction between these requirements and those of taxonomy-alignment is that for an activity to be taxonomy-eligible it only has to contribute to one of the environmental objectives.

The six environmental objectives are:

- Climate change mitigation.

- Climate change adaptation.

- Sustainable use and protection of water and marine resources.

- Transition to a circular economy.

- Pollution prevention and control.

- Protection of healthy ecosystems.

The disclosure requirements apply from 1 January 2022 in relation to the climate change objectives (a and b above), and from 1 January 2023 in relation to the other four environmental objectives. Reporting covers the previous financial year. (Except for the activities related to nuclear energy and natural gas currently under review to be added in the Taxonomy, which shall apply from 1 January 2023.) (See Figure 1.)

The implementation of the Taxonomy signals an enhancement of mandatory sustainability reporting in the EU by driving capital towards activities that are ‘irrefutably’ green. The Taxonomy is designed to play an important role in the transition to a low carbon economy, providing a dynamic framework that creates transparency and comparability for markets. One of the aims is to provide objective criteria to evaluate action on ESG and sustainability, as opposed to companies demonstrating ESG performance just through reporting.

Figure 1

| January 2022 |

|

|---|---|

| January 2023 |

|

| January 2024 |

|

| January 2025 |

|

| January 2026 |

|

Source: European Commission

*Companies who report their financial statements in 2022 are commonly referred to as Fiscal Year Ending (FYE) data sets. They can refer to activities conducted in the prior or current year, depending upon when in the year the statement is submitted.

Figure 2.

Source: European Commission

While the current Taxonomy has an environmental focus, the EU is also considering creating a social Taxonomy, which will similarly identify socially sustainable activities. (See Figure 2. above.)

The Taxonomy is part of a suite of sustainability reporting legislation, designed to encourage material change in business activities across the EU. While aspects of the suite relate to reporting, the EU is trying to drive increased transparency as a means of ensuring that genuinely sustainable companies and activities outlast those companies unwilling to evolve to meet the pressing needs of climate change and environmental disruption.

As is often the case, the EU is leading the world by developing a green classification system with other jurisdictions likely to follow suit. In particular, the UK is looking to develop a taxonomy regulation and is currently interrogating the EU’s technical screening criteria. Meanwhile the Chinese government have developed their own taxonomy and are working together with the EU to find alignment between the two approaches with the aim of standardising a green finance system. As the EU implement their full suite of sustainability reporting legislation, we may see the ‘Brussels effect’ in full force with many nations and regions following the EU’s example.

Limitations of the EU Taxonomy

The Taxonomy currently provides technical screening criteria for 70 climate change mitigation and 68 climate change adaptation activities. Technical screening criteria for activities under the remaining four environmental objectives will be developed in 2022, with reporting due to begin in 2023. Currently, only 13 sectors are covered with significant industries missing, including agriculture. Additionally, debate rages within the EU regarding the designation of certain activities in the energy sector. The EU plans to enhance the current list over the coming years; however, given the limited list of activities, organisations may find that none of their activities are eligible under the Taxonomy, despite possessing demonstrably sustainable credentials or, at the very least, representing a minor impact on the environment. (The EU Taxonomy Regulation itself provides for a review every three years.)

Sectors currently covered by the Taxonomy:

- Forestry

- Environmental protection and restoration activities

- Manufacturing

- Energy

- Water supply, sewerage, waste management and remediation

- Transport

- Construction and real estate

- Information and communication

- Professional, scientific and technical activities

- Financial and insurance activities

- Education

- Human health and social work activities

- Arts, entertainment and recreation

Given the high ambitions of the EU’s efforts—in one fell swoop to designate activities green or not—it’s not surprising that there are limitations to the current construct. For organisations undertaking activities not covered by the Taxonomy, the current state of the regulation provides little immediate motivation to transition towards more sustainable business activities or investments. Likewise, without a reach throughout the economy, it is doubtful that the regulation will face extensive uptake from investors beyond mandatory reporting requirements. With investors increasingly looking to funnel funds towards investments designated as sustainable, the limited coverage of the Taxonomy, as well as elements of confusion as to the designation of certain activities, increasingly limit hopes that it will provide a fundamental shift in investment decisions.

Having said that, the EU is considering an extension to open up the approach by recognising economic activities performing at an intermediate level (neither ‘green’ nor ‘brown’). These activities would be recognised as a credible pathway towards sustainability, provided they do not cause significant harm. The EU also plans to create a list of economic activities that do not have a significant impact on climate to prevent those activities from suffering financial pressure to be Taxonomy aligned. These evolutions could have a positive impact on the channelling of funds towards ‘soon-to-be-green’ investments and begin to extend the impact of the Taxonomy to other sectors and a larger proportion of the economy.

Where no technical screening criteria exist yet, companies are encouraged to use their own metrics and measurements and explain how these relate to the Taxonomy. However, such economic activities would not be considered Taxonomy aligned, a paradoxical situation given the aims of the underlying regulation. According to the Taxonomy, companies can nevertheless propose the inclusion of further economic activities in the Taxonomy.

While the current Taxonomy regulation is limited, the EU has been clear that the list of sustainable activities will be expanded over time to cover all industries. Indeed, despite not addressing a host of sectors and activities, importantly the current list covers industries responsible for over 80% of EU emissions. More significantly, the Taxonomy represents the start of regulatory labelling of activities as climate compliant or not. In a space where a host of stakeholders have clamoured for consistency and clarity, the Taxonomy may be the start of regulators displacing markets.

As appealing as it may seem to defer action until the Taxonomy is expanded—or the social taxonomy is confirmed—for those companies and industries not already covered, strategy, reporting and business decisions for any company within the EU should now be made against the backdrop of the Taxonomy. The ability to attract capital and companies’ licence to operate will be increasingly under threat by inaction against these regulatory developments. While the parameters of the Taxonomy may not capture activities now, the principles which the regulation is designed to achieve are clear. Ultimately every company within the EU will be assessed against its parameters.

Can reporting requirements drive meaningful change?

Responding to pressure from multiple directions, businesses are increasingly disclosing sustainability risks and opportunities. 240 of the world’s largest 250 companies currently report on their sustainability performance. As the EU looks to drive investment toward more sustainable activities, increasing transparency through corporate sustainability disclosure and data provision is an important step in the transition to a more sustainable economy. Over the past decade, however, market participants have—at times—seen enhanced reporting as a branding exercise. The latest shift in regulation necessitates a change in approach: to one whereby disclosure drives meaningful change within an organisation. The old adage that ‘what gets measured gets done’ can be repurposed. Activities that get reported on, force change within organisations.

Rather than viewing this as a resource intensive exercise in disclosure, organisations should use the requirement to inform their strategic objectives and support the transition towards a more environmentally sustainable business model. While reporting should flow from actions, reporting requirements also drive change.

Until now, the absence of an agreed classification framework has allowed for enhanced perception of green credentials without objective assessments. In 2022, we will not just move towards mandatory reporting, we will move to labelling and designations, meaning companies can no longer rely on policies and disclosure to attract positive ESG ratings or investment. Instead, businesses will need to differentiate by fundamentally gravitating toward more sustainable business practices that are either covered by the Taxonomy; or that will allow access to capital as a means of achieving one of the EU’s environmental objectives, driving progress and reflecting this effectively in reporting.

How regulation can drive meaningful change

The EU hopes that the Taxonomy regulation will be a first step in creating the change required to transition to a more sustainable economy. While this seems highly ambitious, there are many existing examples of how increased guidance and scrutiny have helped create meaningful change:

Sarbanes Oxley

One such example would be the Sarbanes-Oxley Act (‘SOX’) that was passed by US Congress in 2002, with the objective of restoring investor confidence, combating fraud and improving risk and reporting processes, in the wake of a series of gross corporate abuses. The key focus was to make governance more rigorous, financial practices more transparent, and management criminally liable for lapses. A subsequent study published in the Harvard Business Review, showed that the first year of implementation was costly and onerous. However, in the second year of compliance, some companies saw the benefit of this additional legislation as a source of valuable insights into its operations. Strengthening the control environment, improving documentation, increasing audit committee involvement, standardisation of processes, reducing complexity, and minimising human error have been some of the key improvements. This additional information on operations helped companies protect their stakeholders and provided a shield against potential lawsuits, but equally important, it helped protect companies from making ‘bad decisions’, the ultimate goal of any robust legislation.

Shareholder Rights Directive II

Another example is the EU Shareholder Rights Directive, implemented in 2009. This focused on the rights of shareholders to improve the governance of companies listed in the EU public markets, through improved transparency and disclosure; and to enhance shareholder rights by imposing certain minimum standards on the exercise of shareholder voting rights at EU listed companies. This amended directive, the Shareholder Rights Directive II, was published in 2018 and became effective in all member states from June 2020. It requests more transparency from companies and investors, to ensure decisions are made in line with the long-term stability of a company. Some of the key topics relate to improving the oversight of directors’ remuneration, and the opportunity for shareholders to vote both ex ante and ex post; refining regulation and policies on related party disclosures; facilitate the flow of information between shareholders and the company; and to increase transparency for institutional investors, proxy advisors and asset managers.

How to make the Taxonomy meaningful to your business

The Taxonomy should not be perceived as disclosure for disclosure’s sake—instead it should be viewed as an opportunity to pivot towards a more sustainable business model; reduce the risk of redundant business activities and stranded assets; and improve stakeholder perceptions of the sustainability of the organisation. Organisations should view the Taxonomy as a classification system that can drive strategy development, data collection and investor communications to create value from newly mandated disclosure. In a world where a range of stakeholders—customers, suppliers, financiers, investors among others—are increasingly concerned about the genuine sustainability profile of a business and its products/services, the ‘Taxonomy’ should be seen as an opportunity. Businesses can differentiate themselves while also ensuring they are effectively managing risk and protecting their licence to operate. Some of those who have pointed to an “alphabet soup” [5] as hampering their sustainability efforts will have their arguments blunted by clearer guidance.

External benefits of demonstrating alignment to the Taxonomy

Attracting investment

While it is not mandatory for companies to ensure their economic activities meet the criteria of the Taxonomy, it provides a motivation for companies to strive to reach a level of environmental performance that financial markets recognise as ‘green’. ESG focused investment is a growing market with more than $649 billion flowing into ESG-focused funds worldwide in 2021, up from the $542 billion and $285 billion in 2020 and 2019, respectively. ESG investment will be funnelled into organisations that can demonstrate alignment to the Taxonomy. The full suite of sustainable reporting criteria under development from the EU, including the Taxonomy, the SFDR, CSRD, the EU Ecolabel for retail financial products [6] and the EU Green Bond Standard, [7] will ensure that Taxonomy-aligned activities are visible and recognised in investment decisions.

For organisations with activities which are not currently covered by the Taxonomy, demonstrating the alignment of activities with the Taxonomy definition criteria will also prove an effective way to appeal to ESG focused investors. If your activities are not covered now, they are likely to be soon through the expansion of the Taxonomy or under the social taxonomy. Early action will help companies establish a leadership position and potentially highlight a commitment to sustainability ahead of peers.

Preferential financing

A four-year long MSCI study found that companies with high ESG scores, on average, had a lower cost of capital compared to companies with poor ESG scores, with cost of equity and debt following the same relationship. This same relationship is likely to extend to organisations with a high proportion of Taxonomy aligned activities who may be able to avail of preferential financing. Additionally, organisations may be offered lower rate loans if they are to be used to finance Taxonomy-aligned activities or investments.

Workforce

Strong, demonstrable ESG strategies can be used to attract talent. According to a 2021 Deloitte survey, 47% of companies saw a positive impact on employee recruitment and retention through their environmental sustainability efforts. The Taxonomy provides a clear and tangible way to demonstrate commitment to sustainable activities and the ability to transparently compare between competing employers.

Supply chain

Up to 90% of the environment footprint of an organisation lies within in the value chain. In order to achieve environmental goals, organisations are increasing requirements on suppliers to improve their environmental performance. This includes selecting suppliers (or customers) who can demonstrate sustainability, with increasing requests for ESG information in RFPs. Taxonomy alignment is a simple way to demonstrate that an activity or organisation is pursuing a sustainable strategy and a way for purchasing organisations to objectively compare the performance of competing suppliers. This aspect will be considerably strengthened by the EU since Brussels is planning to adopt rules aiming at improving companies’ management of sustainability-related matters in their own operations and value chains to promote long-term sustainable value creation.

The Taxonomy provides the ability to compare competing organisations against a common framework for the first time. This presents an opportunity for investors to transparently compare investments and objectively quantify alignment to the EU’s climate goals. It also presents an opportunity for organisations with sustainable activities to be rewarded by attracting investment, availing of lower finance costs, and potentially supporting business development. For those that are not pivoting towards sustainable activities, the Taxonomy presents the risk of highlighting areas where organisations lag peers and which could draw scrutiny from investors, NGOs, and civil society.

Internal implications

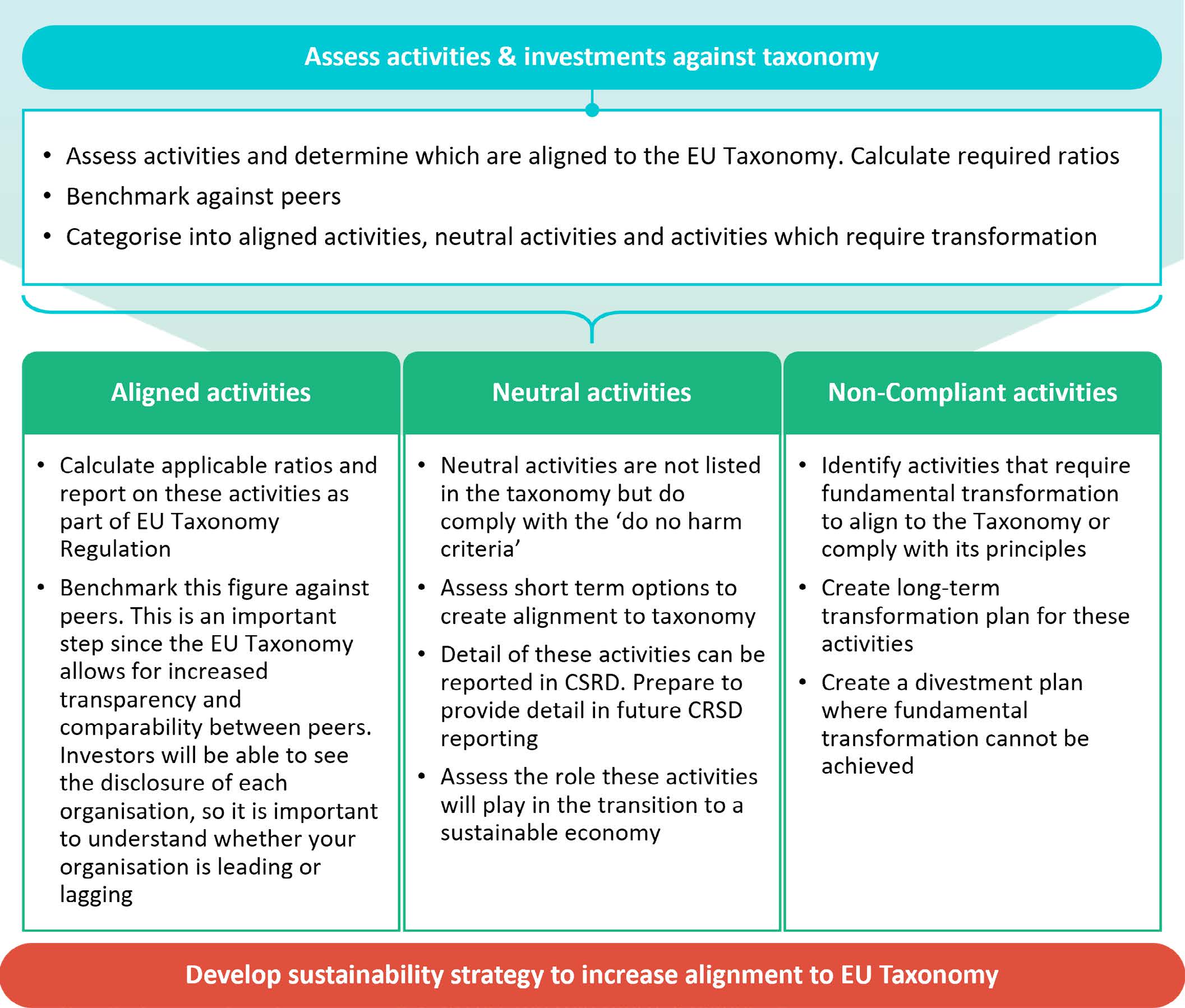

Sustainability can often be a mix of art and science. When asked if an activity is sustainable, an organisation can have different viewpoints depending on the specific scenario or lens through which an activity is viewed. Currently, the Taxonomy provides a ‘black and white’ answer to these questions. Now organisations have a classification system that provides an answer to whether a specific activity or investment is environmentally sustainable. This provides a strong foundation for sustainability strategy development.

The EU is committed to all 17 of the UN’s Sustainable Development Goals, committing to ‘eradicate poverty and achieve a sustainable world by 2030 and beyond, with human well-being and a healthy planet at its core’. In 2021, we saw increasing legislation from the EU to encourage improved sustainability and to align with the bloc’s goal to achieve Net Zero greenhouse gas emissions by 2050.

As we progress towards the EU’s 2030 and 2050 deadlines, we are likely to see increasing legislation that discourages environmentally harmful business practices and may even make these practices non-viable financially.

The Taxonomy provides clear goal posts for a selection of economic activities that must be achieved to enable climate neutrality by 2050. For organisations with activities not yet covered by the Taxonomy, the environmental objectives and criteria included in the Taxonomy definition can be used to give a clear direction of travel. Taking the Taxonomy beyond a disclosure requirement, it should be used as an input for transition strategies, to attract investors and to perform due diligence and screening for sustainable investment opportunities.

The Taxonomy can be used to increase resilience and drive the transition towards more environmentally sustainable activities and investments.

Figure 3.

The development of a strategy that is both effective and cohesive will rely on the development of a suitable data framework. Data collection should be undertaken in line with the Taxonomy to understand the extent of alignment between the business and the EU’s goals on an ongoing basis.

Data will need to be gathered on a yearly basis for mandatory reporting but monitoring this data on an ongoing basis will allow an organisation to create greater value from the data.

Investors will also require data on their investee companies. All corporates will need to ensure they have a data framework that not only tracks meaningful KPIs for their own sustainability strategy, but now also looks at economic activities, corresponding financial information, and alignment to the environmental (and later, social) Taxonomy.

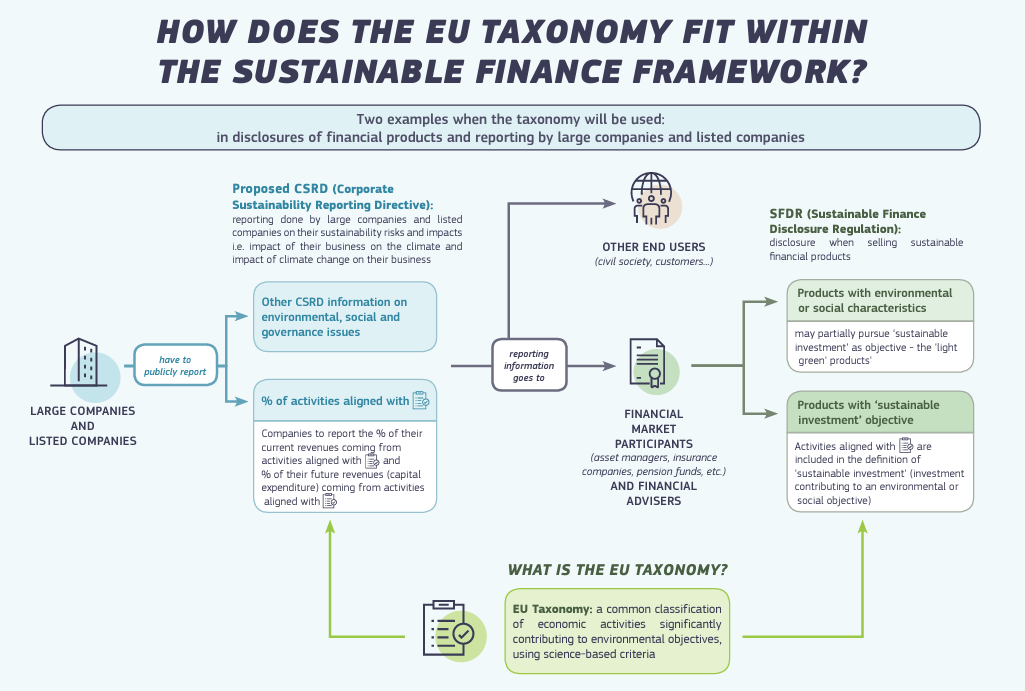

The full suite of regulation

The EU Taxonomy is the fundamental cornerstone of a suite of regulation to be launched by the EU to improve and standardise sustainability reporting. In particular, the Taxonomy will support the Sustainable Finance Disclosure Regulation (SFDR) and the upcoming Corporate Sustainability Reporting Directive (CSRD). During 2021, the impact of the SFDR already hit home—through pushback from asset managers seeking increased clarity and from companies attempting to ensure they would fit into the sustainable bucket to maintain their ability to attract capital. While the SFDR puts pressure on investors, the CSRD puts it on reporting companies.

The CSRD will require organisations to:

- Disclose sustainability risks, including climate change risks

- Detail the organisation’s impact on society and environment

- Identify material sustainability topics for stakeholders

- Include targets and progress

- Report in line with Sustainable Finance Disclosure Regulation (SFDR) and the EU Taxonomy Regulation

The CSRD will likely be adopted in mid-2022 with mandatory reporting from 2024.

The CSRD will enable organisations whose activities are not covered by the Taxonomy to provide further information on the sustainability of their activities and investments. Where no technical screening criteria for specific economic activities exist, companies should use their own metrics and measurements and explain how these relate to the Taxonomy ahead of the implementation of the CSRD. While the Taxonomy sets the baseline for the direction of investment to enable Europe to achieve its goal of being the first ‘carbon neutral continent’, the CSRD provides transparency over the sustainability risks and opportunities for the remainder of the economy and sectors which are not directly covered by the Taxonomy.

The Sustainable Finance Disclosure Regulation (SFDR) aims to increase transparency on sustainability among financial market participants and financial advisers operating within the EU toward end-investors. It requires firms to disclose how they integrate sustainability risks and objectives in their policies as well as how they integrate sustainability in financial products—in particular, firms are required to classify the investments they offer based on their ESG Credentials. This is needed to improve industry-wide comparability and prevent greenwashing. The SFDR divides the products into three categories:

- Funds which do not integrate any kind of sustainability into the investment process

- Financial products promoting ESG characteristics, and which follow good governance practices (Art. 8 products)

- Financial products with sustainable investment as their objective and indices designated as reference benchmarks (Art. 9 products)

The SFDR directly interlinks with Taxonomy Regulation which requires specific disclosure obligations—for example, whether and to what extent, products qualify as sustainable under the Taxonomy. The SFDR has been in force since 10 March 2021, however, specific disclosures have been delayed (in particular those relating to Taxonomy alignment) and have been postponed until 1 January 2023.

The intention of these regulations is to standardise reporting requirements and increase transparency. In turn, the EU hopes that this will reduce ‘greenwashing’; promote greater accountability; and encourage investment towards the promotion of environmentally sustainable activities.

Figure 4.

Conclusion

Since the EU Taxonomy came into force, it has faced criticism due to its limitations, the designation of certain activities, and even whether legislation should play a role in accelerating the transition of capital markets towards a sustainable economy. While aspects of these criticisms may be valid, it would be naïve to ignore the importance of the Taxonomy in signally the beginning of far-reaching mandatory sustainability disclosure. As the suite of sustainability regulation builds, businesses and investors will have nowhere to hide and must transition towards activities and investments that play a role in mitigating the climate crisis.

The regulation will be fundamental in providing guiding principles which allow the EU to achieve its environmental objectives. Even the fierce infighting between nations on the designation of certain activities points to a recognition of how impactful regulation will be. By determinedly fighting the corner for the inclusion of energy sources which are fundamental to their energy mix, member states are demonstrating their belief that those activities which are not included in the Taxonomy will struggle to survive.

The Taxonomy cannot be ignored, and business should leverage the Taxonomy to drive sustainable transformation and underpin long-term strategy. The comparability and transparency brought about through the Taxonomy mean that sustainability disclosure can no longer be viewed as a branding exercise, instead it must drive meaningful change within the organisation. Those that tune in to the Taxonomy and leverage it to pivot towards a more sustainable business model will reap the rewards of alignment with the EU’s priorities. All companies have been put on notice that—either now or over the near term—their businesses and activities will be labelled sustainable or not by the regulator of the world’s second largest economy.

Endnotes

1https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal_en(go back)

2https://ec.europa.eu/info/business-economy-euro/banking-and-finance/sustainable-finance/eu-taxonomy-sustainable-activities_en(go back)

3https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A32019R2088(go back)

4https://ec.europa.eu/info/business-economy-euro/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en(go back)

5https://www.accountancyeurope.eu/wp-content/uploads/Unpuzzling-the-Sustainability-Reporting-Alphabet-Soup.pdf(go back)

6https://susproc.jrc.ec.europa.eu/product-bureau/product-groups/432/documents(go back)

7https://ec.europa.eu/info/business-economy-euro/banking-and-finance/sustainable-finance/european-green-bond-standard_en(go back)