Print

PrintDavid H. Kistenbroker, Joni S. Jacobsen and Angela M. Liu are partners at Dechert LLP. This post is based on a Dechert memorandum by Mr. Kistenbroker, Ms. Jacobson, Ms. Liu, Julia Markham Cameron, and Melissa A. Vallejo. Related research from the Program on Corporate Governance includes Rethinking Basic by Lucian Bebchuk and Allen Ferrell (discussed on the Forum here); and Price Impact, Materiality, and Halliburton II by Allen Ferrell and Andrew Roper (discussed on the Forum here).

Introduction

In 2021, securities class action litigation on the whole remained at a steady high, and life sciences companies were, once again, popular targets of such lawsuits. [1] In this post, we analyze and discuss trends identified in last year’s filings and decisions so that prudent life sciences companies can continue to take heed of the results.

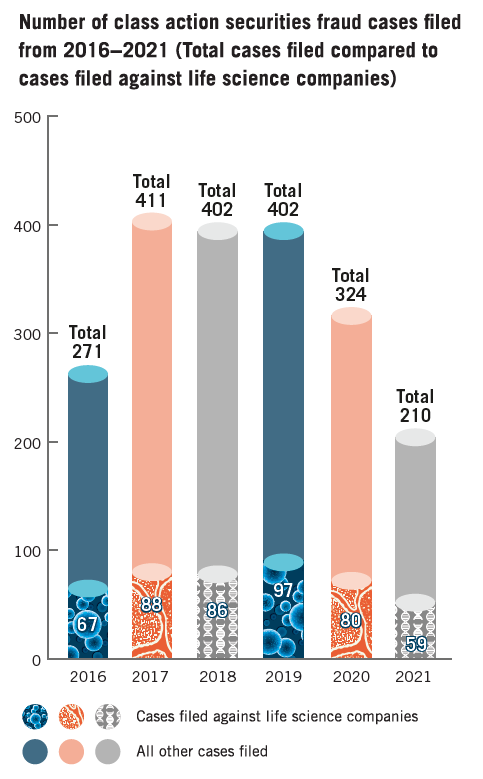

Plaintiffs filed a total of 59 securities class action lawsuits against life sciences companies in 2021. Filings against life sciences companies in 2021 represented a 17.5% decrease from the previous year, but a 19.4% increase from five years prior. Of these cases, the following trends emerged:

- Consistent with historic trends, the majority of suits were filed in the Second, Third and Ninth Circuits, with a 19.3% increase in suits filed in the Ninth Circuit. The Third Circuit, on the other hand, saw a 57.9% decrease in filings from the previous year—from 29 in 2020 to 9 in 2021. Within these circuits, the Northern District of California had the most filings, with 13 overall.

- A few plaintiff law firms were associated with about three-fourths of the filings against life sciences companies: Pomerantz LLP (27 complaints), Glancy Prongay & Murray LLP (11 complaints) and Bronstein, Gewirtz & Grossman, LLC (8 complaints).

- Slightly more claims were filed in the second half of 2021 than in the first half, with 29 complaints filed in the first and second quarters, and 30 complaints filed in the third and fourth quarters.

- 6 cases were filed against companies with COVID-19 related products.

An examination of the types of cases filed in 2021 reveals continuing trends from previous years.

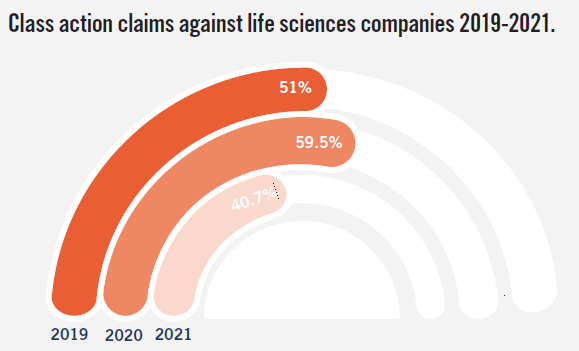

- About 40.7% of claims involved alleged misrepresentations regarding product efficacy and safety, with many of these cases involving alleged misrepresentations regarding negative side effects related to leading product candidates, which could at times impact the likelihood of Food and Drug Administration (“FDA”) approval.

- About 32.2% of the claims arose from alleged misrepresentations regarding regulatory hurdles, the timing of FDA approval or the sufficiency of applications submitted to the FDA.

- Approximately 22% of the claims alleged misrepresentations regarding purported unlawful conduct in both the United States and abroad, including (but not limited to) illegal kickback schemes, anticompetitive conduct, tax issues and inadequate internal controls in financial reporting.

- About 25.4% of the claims involved alleged misrepresentations of material information made in connection with proposed mergers, sales, IPOs, offerings and other transactions. [2]

Courts throughout the country issued decisions in 2021 involving securities fraud actions against life sciences companies, including:

- Claims that arose in the development phase, such as cases involving products failing clinical trials that are required for FDA approval, or products not approved by the FDA, where courts were more likely to grant motions to dismiss in full than to deny them, either in whole or in part.

- Claims that were independent of or arose after the development process, where courts were more likely to grant motions to dismiss in full than to deny them, either in whole or in part.

- Claims based on the financial management of life sciences companies, which generally split between plaintiff and defendant-friendly outcomes.

Given the numbers from this and recent years’ filings, and accounting for the COVID-19 pandemic, there is no indication that the filings of securities claims against life sciences companies is going to slow down any time soon. The decisions this year resulted in mixed outcomes, with 19 opinions decided in favor of defendants, [3] ten opinions denying motions to dismiss (including one reversal of dismissal on appeal), and eight opinions in which only partial dismissal was achieved. [4] In addition, appellate courts also rendered opinions. There was only one appellate court decision rendered, and in that case the Court of Appeals affirmed in part, vacated in part, and remanded for further proceedings. These numbers illustrate how life sciences companies remain attractive targets for class action securities fraud claims. Therefore, companies should continue to stay abreast of recent developments and implement best practices to reduce their risk of being sued.

Life Sciences Companies Remain Popular Targets for Securities Fraud Litigation

In recent years, life sciences companies have increasingly been targets of securities fraud lawsuits, and 2021 was no exception. This survey is intended to give an end-of-year overview of life sciences securities lawsuits in 2021.

First, we analyze the number of cases filed, including trends relating to the location, the types of companies targeted and the parallels between underlying claims. Next, we analyze the securities class action decisions rendered in 2021 and how they impact the legal landscape of life sciences claims. Finally, we set forth issues and best practices life sciences companies should consider to reduce the risk of being subject to such suits.

Almost One Of Three Securities Class Action Filings Are Against Life Sciences Companies

In general, the number of securities fraud class action lawsuits has been increasing steadily since 2012, peaking in 2017 before reaching a plateau in 2018. This trend has reversed since the coronavirus pandemic began: 324 securities fraud class action lawsuits were filed in 2020, and “only” 210 were filed in 2021. This total pales in comparison to the 402, 402 and 324 suits filed in 2018 through 2020, respectively, and marks the lowest number of filings since 2015 and thirteenth highest since 1996. [5] The average number of suits filed from 2018-2021 dropped to 333.5 per year, down from an average of 386 for in the period 2017-2020. [6]

Although the overall number of securities lawsuits filed has decreased since last year, the proportion of such actions brought against life sciences companies has remained unchanged. Indeed, a total of 59 class action securities lawsuits were filed against life sciences companies in 2021—more than one out of four of all securities fraud class action lawsuits. This percentage was slightly higher than 2020, where 80 out of 320 securities fraud class actions (or just under 25%) were filed against life sciences companies.

Figure 1

Filing Trends

Over the past year, the number of claims filed against life sciences companies decreased numerically but remained proportional relative to the past three years. The coronavirus pandemic—and the attendant disruptions to business—likely contributed to the decrease in total filings in 2021. The percentage of filings brought against life sciences companies, however, roughly remained the same, with a slight increase. In 2021, almost one out of every three securities fraud class action suits targeted a life sciences company, while 2020 and 2019 finished with 24.7% and 24.1%, respectively. [7] 2021 brought about new and noticeable variations within larger trends, particularly relating to when and where suits were filed, and the nature of the claims involved.

Figure 2

Life Science Companies

- Slight decrease in percentage of claims against large cap companies from previous year. In 2021, about 50.8% of the life sciences companies named in class action securities fraud complaints had a market capitalization of US$500 million or more. [8] This trend [9] represents a slight decrease from filings in 2020 [10] and 2019. [11] About 40.7% of the total cases filed in 2021 were against life sciences companies with a market capitalization of US$1 billion or more. [12] Of these complaints, about three in eight cases were filed against companies with a market capitalization of US$5 billion or more, [13] making up about one-sixth of the total cases filed. [14]

- The Ninth Circuit saw the highest number of filings, and among district courts, the Northern District of California saw the highest number of filings against life sciences companies. Breaking with historic trends, the Ninth Circuit saw the greatest number of filings in 2021, whereas in 2020 the greatest number of filings was seen in the Third Circuit. However, the majority of the 59 class action securities fraud suits brought against life sciences companies were again filed in courts in the same three federal circuits: the Ninth Circuit with 22; the Second Circuit with 13; and the Third Circuit with nine. There were some notable shifts, and these circuits experienced a decrease in filings: The Ninth Circuit saw a 12% decrease in complaints filed in its district courts. The Second Circuit saw a similar decrease of 18.75%.

The Third Circuit saw a 68.9% decrease in complaints filed in its district courts. Within these circuits, the Northern District of California had the most filings, with 13 overall. All 13 of these filings relate to topics ranging from mergers, product efficacy, Food and Drug Administration issues, among others. After California, district courts in New York were the second most popular with 13 total filings, with all filed in the Southern District of New York and the Eastern District of New York except one. In 2021, over half of all cases were brought in the federal district courts of two states. Unlike in 2020, California and New York accounted for the greatest number of filings. [15] The Third Circuit, which in previous years accounted for the most filings against life sciences companies, saw a shift in the distribution of filings among its federal district courts in 2021: Delaware with one (or 11.1%), New Jersey with five (55.6%), the Eastern District of Pennsylvania with three (33.3%) and the Western District of Pennsylvania with none. [16]

- Three law firms were associated with about three fourths of filings against life sciences companies. In 2021, the three firms with the most filings of securities fraud lawsuits against life sciences companies were Pomerantz LLP, Glancy Prongay & Murray LLP, and Bronstein, Gewirtz & Grossman, LLC. These firms were listed on 27, 11 [17] and eight complaints respectively, and Pomerantz LLP was selected as lead or co-lead counsel in ten cases thus far. Block & Leviton LLP had the fourth-most filings in 2021, accounting for four of the complaints filed, and serving as lead or co-lead counsel in one. Though the past two years saw a rise of filings initiated by RM Law, P.C. and Rigrodsky & Long, P.A. due to an increase in merger litigation in Delaware, in 2021, RM Law, P.C. was the only firm that initiated a filing.

- Slightly more claims were filed in the second half of 2021 than in the first half. Of the 59 complaints filed against life sciences companies in 2021, 29 were filed in the first half of the year, and 30 were filed in the second half. When broken down by quarter, 17 complaints were filed in the first quarter, 12 in the second, 14 in the third and 16 in the fourth. In 2019 and 2020, slightly more claims were also filed in the second half of 2020 than in the first half. [18]

These figures are generally consistent with historic trends overall, but there were some notable changes in 2021. Though companies with market capitalizations of more than US$500 million continued to be popular targets of class action complaints filed against life sciences companies, there was a slight decrease in these filings from previous years. The three federal circuits that dominated filings this year remained consistent with recent years, but it was the Northern District of California (not the District of Delaware) that led the pack at the district court level. This year, Pomerantz LLP filed more filings than any other firm. While in recent years, RM Law and Rigrodsky & Long filed the greatest number of securities fraud actions against life sciences companies, this year RM Law only filed one case, and Rigrodsky & Long did not file any cases.

Causes of Action

Although the total number of securities fraud class actions brought against life sciences companies decreased in 2021, the legal issues alleged in those complaints remained consistent with past years. As with other industries, deal litigation also continued to be at the forefront of securities fraud complaints filed against life sciences companies. However, the onset of the coronavirus pandemic has provided new allegations that are likely to continue into 2022.

Similar to previous years, one group of cases filed against life sciences companies in 2021 involved allegations unique to life sciences companies: misrepresentations regarding product efficacy and safety, especially negative side effects of leading product candidates, which could at times impact the likelihood of FDA approval. For example, FibroGen, Inc., a biopharmaceutical company, was sued in a securities class action alleging violations of Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 (“Exchange Act”) for making materially false and misleading statements. Specifically, the complaint alleged that: (1) FibroGen had manipulated clinical trial data for Roxadustat, an experimental pill designed to treat anemia in patients with chronic kidney disease (“CKD”), in order to make the drug appear significantly safer than it was; and that (2) consequently, the Phase 3 Roxadustat Trial was unlikely to meet its primary endpoint of demonstrating that Roxadustat was at least as effective

as Epogen, the standard of care in treating anemia in CKD patients, and so was unlikely to secure FDA approval. [19] In 2013, FibroGen secured an agreement with AstraZeneca to commercially develop Roxadustat, which was contingent on FibroGen achieving various milestones in the drug’s FDA new-drug application (“NDA”) approval process. The standard of care to treat anemia in CKD patients, Epogen, is only used in severe cases for patients already on dialysis because it leads to an increased risk of major adverse cardiac events. Accordingly, the goal of the Phase 3 Roxadustat trial was to demonstrate that Roxadustat was at least as effective as Epogen, while avoiding the safety issues that prevented Epogen from being used to treat a broader range of CKD patients. [20] From December 2018 through March 2021, FibroGen made numerous public statements promoting the safety and efficacy of Roxadustat as an anemia treatment for CKD patients. [21] However, the amended complaint alleges that in April 2021 the company announced in a press release that it had manipulated Roxadustat’s Phase 3 trial results, and that those manipulations had made the drug appear significantly safer than it really was. [22] Specifically, the defendants purportedly had manipulated the data to appear over 17% safer than it actually was under the FDA’s primary prespecified analysis. Rather, according to the amended complaint, as disclosed in April 2021, Roxadustat’s true FDA pre-specified data unequivocally demonstrated that there was no evidence whatsoever to support FibroGen’s assertions that Roxadustat was safer than Epogen, the standard of care in treating anemia in CKD patients. [23] Over the two days following FibroGen’s admissions, the company’s stock price purportedly fell US$15.83 per share, or 45% closing at US$18.81 per share—a US$1.45 billion decline in market capitalization. [24]

Another group of complaints unique to life sciences companies arose from misrepresentations regarding regulatory hurdles, the timing of FDA approval or the sufficiency of applications submitted to the FDA unrelated to safety. [25] Notably, two of these filings involved COVID. [26] For example, investors sued Novavax, Inc., a biotechnology company that focuses on the discovery, development and commercialization of vaccines to prevent serious infectious diseases and address health needs, and whose product candidates include, among others, NVX-CoV2373, which is in development as a vaccine for COVID-19, alleging violations of Sections 10(b) and 20(a) of the Exchange Act. [27] According to the complaint, Novavax, Inc. allegedly overstated its manufacturing capabilities and downplayed manufacturing issues that would impact its approval timeline for NVX-CoV2373 and as a result, Novavax was unlikely to meet its anticipated Emergency Use Authorization (“EUA”) regulatory timelines for NVX-CoV2373. [28] Accordingly, the company allegedly overstated the regulatory and commercial prospects for NVX-CoV2373. [29] Prior to the start of the class period, Novavax, Inc. announced that it planned to complete EUA submissions for NVX-CoV2373 with the FDA in the second quarter of 2021. [30] Through a series of news articles and the company’s own press releases, it was revealed that the company expected to file for NVX-CoV2373’s EUA in the fourth quarter of 2021, rather than what was initially disclosed, as a result of regulatory hurdles. [31] On the last set of news, Novavax’s stock price fell 14.76%. [32]

Another group of complaints alleged other unlawful conduct, including (but not limited to) illegal kickback schemes, anticompetitive conduct, tax issues and other forms of financial malfeasance. [33] In one case, investors sued Emergent BioSolutions Inc., a specialty biopharmaceutical company that develops vaccines and antibody therapeutics for infectious diseases. [34] Plaintiffs alleged that Emergent, which contracted with Johnson & Johnson and AstraZeneca to provide contract development and manufacturing organization services to produce the companies’ COVID-19 vaccine candidates, engaged in a fraudulent scheme to artificially inflate its stock price by repeatedly assuring investors of its ability to mass manufacture the vaccines at its Baltimore facility while failing to disclose deficiencies at this facility that detrimentally affected its ability to manufacture the vaccines. [35] These deficiencies came to light in March 2021, when media reports revealed that employees at Emergent’s Baltimore manufacturing facility “mixed up” ingredients for the J&J and AstraZeneca vaccines, contaminating up to 15 million doses of the J&J vaccine. [36] It was further reported that by December 2020, Emergent was forced to discard the equivalent of millions of AstraZeneca vaccine doses after they were spoiled by bacterial contamination of equipment at the same Baltimore facility. [37] Plaintiffs alleged that in response to this news, shares of Emergent’s stock price fell US$14.29 per share, or over 15% over the next two trading days, from a close of US$92.91 per share on March 31, 2021, to close at US$78.62 on April 5, 2021. [38]

Another group of the class action securities fraud claims filed against life sciences companies in 2021 alleged misrepresentations and omissions related to proposed mergers, sales, IPOs, offerings and other transactions. [39] Many of the complaints arising from transactions contain similar allegations. [40] For example, investor sued Longeveron Inc., a clinical stage biotechnology company, alleging that the company made materially false and misleading statements regarding the company’s business, operations and compliance policies. [41] Specifically, the plaintiff alleges that the defendants made false and/ or misleading statements and/or failed to disclose that Lomecel-B was not as effective in treating aging frailty as defendants had led investors to believe in the IPO offering documents. [42] On August 13, 2021, Longeveron issued two press releases disclosing that Lomecel-B had “not achiev[ed] . . . statistical significance for the pairwise comparison to placebo” with respect to the primary efficacy endpoint. [43] Thus, plaintiff alleges that Lomecel-B’s clinical and commercial prospects with respect to aging frailty were overstated in the offering documents. [44] Accordingly, Longeveron Inc. was alleged to have violated Sections 10(b) and 20(a) of the Exchange Act and Rule 10b-5 as well as Sections 11 and 15 of the Securities Act. [45]

The COVID-19 pandemic has upended daily business across the world, forcing many companies, especially life sciences companies, to consider new litigation risks. Although fewer securities class actions were filed in 2020, there were at least six complaints alleging issues with a company’s COVID-19 antibody or vaccine development. [46] For example, investors alleged that AstraZeneca PLC misrepresented facts regarding its clinical trials for its COVID-19 vaccine, AZD1222. [47] In November 2020, AstraZeneca issued a press release announcing the results of an interim analysis of its ongoing AZD1222 trials involving two smaller-scale trials that employed two different dosing regimens, one providing patients a half dose of AZD1222 followed by a full dose, and the other trial provided two full doses. [48] AstraZeneca allegedly claimed that the half-dosing regimen was “substantially more effective at preventing [COVID-19]—at 90% efficacy—than the full-dosing regimen.” [49] In the following days, it was allegedly revealed that the different dosing regimens were due to a manufacturing error rather than trial design, AstraZeneca acknowledged knowing about the dosing error by June 2020, the half-dose strength had not been tested in people over the age of 55 and some trial participants received their second doses later than expected. [50] The complaint alleges that “in response to these and other partial disclosures of truth to investors,” the price of AstraZeneca’s American Depository Shares fell from US$55.30 on November 20, 2020, to US$52.60 by market close on November 25, 2020, a 5% decline allegedly “in response to developing adverse news, on abnormally high volume.” [51]

Last, another noteworthy trend in 2021 has been the number of life sciences companies that are incorporated abroad but have still been subject to securities lawsuits in the United States, which is in line with general securities litigation trends across all industries. [52] While many of the allegations seem to cover topics similar to those discussed above, the two suits that involve cannabis companies were both related to mergers and acquisitions. Neptune, a Canadian integrated health and wellness company focused in part in producing cannabis products, was sued for allegedly failing to disclose to investors that the cost of Neptune’s integration of the assets and operations acquired from SugarLeaf Labs, LLC and Forest Remedies LLC would be larger than the Company had acknowledged, placing significant strain on the Company’s capital reserves. [53] Once Neptune announced subpar financial results for the third quarter of the Company’s fiscal year 2021, thus needing to conduct additional stock offerings to raise more capital, the stock dropped. [54] GW Pharmaceuticals, PLC, a biopharmaceutical company focused on discovering, developing and commercializing novel therapeutics from their proprietary cannabinoid product platform, was sued for allegedly characterizing the merger consideration for Jazz Pharmaceuticals, PLC to acquire it as “fair” when in reality, the merger consideration undercompensated GW shareholders providing them with substantially less than the intrinsic fair value of their shares. [55]

Similar to years past, the common themes of these complaints show the unique challenges life sciences companies face as issuers, but also commonalities with securities litigation filings on the whole. First, these filings continue to show that negative side effects in clinical trials can create a claim for securities fraud when management attempts to conceal or downplay these effects, subsequently overstating the trial’s results and prospects of FDA approval. The filings also continue to indicate that companies cannot inflate investors’ expectations of FDA approval—they must ensure that the company’s risk disclosures and cautionary warnings are robust, and executives’ statements regarding the likelihood of approval must be measured and in no way misleading. Moreover, the filings show life sciences companies also face challenges similar to those faced by other non-life sciences issuers, particularly challenges relating to disclosures in the sale or merger of life sciences companies. In addition, similar to other non-U.S. issuers, those life sciences companies with headquarters located outside of the U.S. may still be targets of securities class actions in the U.S. While these filings show that life sciences companies face unique challenges when it comes to securities fraud, they also reveal how these companies are still at risk from more common forms of securities fraud claims as well.

2021 Class Action Securities Fraud Decisions in the Life Sciences Sector

There was a slight decline in securities fraud decisions by courts involving life sciences companies in 2021, especially in light of the coronavirus pandemic and resulting court closures. Compared to 2020, where Dechert identified 43 such decisions, Dechert identified 38 decisions using the same criteria. These decisions fall under three broad categories: (i) cases involving claims that arose in the development phase, such as cases involving a drop in stock price after the failure of a clinical trial, and cases involving overly optimistic statements regarding FDA approval of a drug or device; (ii) cases involving claims arising independent of or after the development process; and (iii) cases involving the financial management of life sciences companies (e.g., alleged market manipulation or improper accounting). As in the previous two years, the majority of these decisions address alleged violations of Sections 10(b) and 20(a) of the Exchange Act.

Court Decisions Regarding Alleged Misrepresentations During Product Development

Life sciences companies face significant risk during the developmental stage of a drug or device. Companies naturally want to promote new products and ensure that potential investors are aware of attractive opportunities. When those products perform well during trials and are ultimately approved by the FDA, they may then succeed in the market and reward the company and its investors. However, when products in development underperform or outright fail during clinical trials, plaintiffs’ firms around the country pursue securities fraud class actions to recover for the purported harm to investors, arguing that the defendants somehow misled the public. Thus, when new products fail clinical trials, or if the FDA declines to approve the new product, life sciences companies can (and should) expect plaintiffs’ firms to mine public filings in order to piece together a story that the life science company mischaracterized or exaggerated trial results and/or failed to warn investors of significant risks that the product would not be approved.

In 2021, courts issued 39 opinions—a slight decline from 43 decisions identified using similar criteria in 2020. Of those 39 opinions, 14 include allegations of misrepresentations during product development. In some cases, stock prices fell after a drug or device did not meet efficacy or safety expectations, resulting in claims that the company misrepresented test results in order to improperly bolster stock prices. In others, plaintiffs alleged that defendants made false or misleading misrepresentations regarding the likelihood of a product’s FDA approval, including that the companies withheld or mischaracterized FDA advice or warnings during development.

Unlike in 2020, when courts “dismissed nearly all of the claims related to alleged misrepresentations during product development,” [56] courts in 2021 took a slightly more moderate approach. Of the 14 identified opinions, courts dismissed nine of such matters in whole [57] and one in part [58] (including appellate decisions affirming lower courts’ dismissal orders).

Defendants frequently challenge and defeat securities class action claims by arguing that they did not act with scienter when making statements during product development. One of the more notable cases from 2021, Carr v. Zosano Pharma Corp., [59] affirmed a dismissal under Federal Rule of Civil Procedure 12(b)(6) focusing in depth on the “critical element of scienter.” [60] In Carr, the United States District Court for the Northern District of California addressed allegations that Zosano Pharma Corporation, a clinical stage pharmaceutical company that focuses on “administering drugs to patients using its proprietary intracutaneous delivery system, known as the Adhesive Dermally Applied Microarray (“ADAM”),” misled investors regarding the likelihood that one of its new products would receive FDA approval. [61] The product in question was Qtrypta, which was designed to deliver a proprietary formulation of zolmitriptan (a drug previously approved by the FDA to treat migraines) through Zosano’s ADAM patch. In March 2016, Zosano announced that it was restructuring its operations to focus on Qtrypta following positive Phase 1 data and FDA feedback. The FDA had “indicated that a single positive pivotal efficacy study and a long-term safety study could support approval” of Qtrypta via a streamlined approval process for products that incorporate previously approved drugs. [62] In February 2017, Zosano issued a press release announcing “positive top line results from its pivotal efficacy study,” stating that Qtrypta had “achieved both co-primary endpoints of pain freedom and most bothersome symptom freedom at 2 hours” in its Phase 2/3 studies, and that the drug was “not associated with any Serious Adverse Events.” [63] Throughout 2017, 2018 and 2019, Zosano continued to express optimism about the likelihood that Qtrypta would be approved by the FDA, and filed a new drug application (NDA) for the drug in December 2019. [64]

But in September 2020, Zosano disclosed that it had received a Discipline Review Letter from the FDA, in which the FDA raised questions regarding “unexpected high plasma concentrations of zolmitriptan observed in five study subjects from two pharmacokinetic studies and how the data from these subjects affect the overall clinical pharmacology section of the [NDA],” and “differences in zolmitriptan exposures observed between subjects receiving different lots of Qtrypta in the company’s clinical trials.” [65] Then, in October 2020, Zosano disclosed that the FDA had rejected the Qtrypta NDA due to “inconsistent zolmitriptan exposure levels observed across clinical pharmacology studies,” specifically “differences in zolmitriptan exposures observed between subjects receiving different lots of Qtrypta in the company’s trials and inadequate pharmacokinetic bridging between the lots that made interpretation of some safety data unclear.” [66] The FDA admonished Zosano that it would need to conduct additional studies before resubmitting an application. [67] Following this announcement, plaintiffs filed a complaint alleging that Zosano and its officers knew of the issues raised in the Qtrypta trials and failed to disclose them. The plaintiffs continued that, as a result of such knowledge, defendants also knew that the FDA was likely to require further studies to support approval, and thus regulatory approval was at risk or was likely to be delayed. [68] Plaintiffs also alleged that, because it had incurred several years of net losses, Zosano was “motivated to issue misstatements” regarding FDA approval for Qtrypta in order to “stem the flow of losses, boost cash on hand, and provide funding for the development and trials of Qtrypta.” [69]

In ruling on Zosano’s motion to dismiss for failure to state a claim, the court found that the plaintiffs had failed to plead scienter. Analogizing to Nguyen v. Endologix, Inc., 962 F.3d 405 (9th Cir. 2020)—an opinion profiled in Dechert’s 2020 edition of this survey—the court reasoned that “[t]here is no logical reason why Defendants would tell investors that they believed FDA approval was likely if they secretly knew the FDA was going to delay or reject the application,” especially as the plaintiffs did not allege that Zosano or its officers engaged in “insider stock sales” or other suspicious financial activity before disclosing that the FDA had rejected the Qtrypta NDA, nor did plaintiffs include any allegations against the defendants from any confidential witnesses or former Zosano employees. [70] The court further rejected plaintiffs’ contention that Zosano was incentivized to issue misstatements about Qtrypta’s FDA approval process in order to bolster its sagging finances, as “the Ninth Circuit has rejected the proposition that ‘allegations of routine corporate objectives such as the desire to obtain good financing and expand’” are “insufficient to allege scienter.” The court explained that holding otherwise “would support a finding of scienter for any company that seeks to enhance its business prospects.” [71] The court dismissed the complaint without prejudice, noting that any amended complaint must set forth “considerably” stronger allegations of scienter. [72]

In the context of alleged misrepresentations during product development, courts also dismissed cases on grounds that the alleged misrepresentations were protected by the PSLRA’s safe harbor for forward-looking statements. The PSLRA prevents statements from being actionable by applying a safe harbor for forward-looking statements when those statements are identified as forward-looking and “accompanied by meaningful cautionary language.” [73] For example, in Villare v. Abiomed, Inc., plaintiffs brought allegations against Abiomed, Inc., a company that develops, manufactures and markets devices designed to improve blood flow to the coronary arteries and to temporarily assist the pumping function of the heart. In the complaint, plaintiffs alleged that the company made misleadingly optimistic statements about its growth rate, its ability to grow sustainably and the ability of its Impella line of percutaneous heart pumps to penetrate the market. [74] The defendants argued that the statements they made about Abiomed’s potential growth were “quintessentially forward-looking” because they concerned the company’s growth goal. [75]

In response, plaintiffs argued that the defendants’ statements “reflected Abiomed’s then-current ability to grow sustainably—not a projection that it will.” [76] The court disagreed with the plaintiffs, reasoning that “by [plaintiffs’] logic, a statement that a company ‘will grow’ is protected under the safe harbor provision, while a statement that a company ‘thinks it will grow’ is not. Such a distinction would be meaningless, especially because a company’s current ability to grow is necessarily implicit in every future projection.” [77] Consistent with this reasoning, the court cited additional New York cases for the positions that statements that a company was “tracking in line with its internal deleveraging targets,” and that officers “believe[d] that [the company] will continue to achieve new sales and profit records” were forward-looking as a whole even though they contained some present-tense portions. [78] The court found the other alleged misstatements to be immaterial and/or corporate puffery, and dismissed the case without prejudice. [79] Oftentimes, courts will dispose of cases on grounds that the alleged misrepresentations were not material. Section 10(b) of the Exchange Act and its related Rule 10b-5 require a plaintiff to plead “a material misrepresentation or omission.” [80] Aside from the nonactionable forward-looking statements in Villare v. Abiomed, Inc. discussed above, the court also disposed of certain claims due to materiality. Specifically, the court addressed allegations that Abiomed failed to disclose that its growth rate had allegedly stalled and that it was allegedly unable to convince doctors to regularly use Abiomed’s products. [81] The court found that, while the plaintiffs had offered the subjective views of confidential witnesses regarding Abiomed’s alleged inability to sustain its growth rates, the views were insufficient to demonstrate that any defendants believed these statements to be inaccurate when they were made. [82] Because the plaintiffs were, in essence, “seek[ing] to hold Defendants liable simply for failing the unsustainability of their business model, [they] failed to allege an actionable omission.” [83] In another case, In re Karyopharm Therapeutics, Inc. Securities Litigation, the court rejected a similar argument advanced by plaintiffs. [84] In Karyopharm Therapeutics, the court addressed a claim that defendants knowingly misrepresented data by not disclosing that its drug candidate for the treatment of certain advanced cancer did not show a statistically significant overall survival rate in patients. [85] However, the court rebutted this assertion by pointing out that the defendants did state that it was cancelling trials of the drug because it would not reach statistical significance for overall survival. [86] The court denied the plaintiffs’ further arguments that the defendants were liable for failing to disclose that the median overall survival rate for patients receiving the drug was lower than the rate for patients receiving standard care and/or that 100% of evaluable patients who received the drug experienced adverse effects. The court explained that “Karyopharm has no affirmative duty to disclose every piece of information in its possession in which an investor may have an interest,” and the defendants had adequately apprised investors with an overall picture of the efficacy of the drug. [87] While the court found that defendants disclosure that the drug was a “success” was “arguably incomplete” without also disclosing data regarding the drug’s toxicity, it held that plaintiffs failed to allege defendants acted with scienter. Accordingly, the court granted the motion to dismiss without prejudice.

Court Decisions Regarding Alleged Misrepresentations After Product Development

Life sciences companies can still face liability after a product is developed. Recalling the slight drop from 43 opinions in 2020 to 38 in 2021, Dechert identified only seven instances of a court addressing fraud claims that arose after a drug or device’s development process. Of the seven cases, four were dismissed in whole [88] and three were dismissed in part. [89]

One of the cases, Industriens Pensionsforsikring A/S v. Becton, Dickinson & Co. (“Becton”), concerned alleged misstatements in press releases, earnings calls, SEC filings and conferences related to a 510(k) application required by the FDA. [90] The Becton case includes claims under Sections 10(b) and 20(a) of the Exchange Act and Rule 10b-5. The claims in this case stemmed from Becton’s software-based medical device, Alaris, that delivers medication or other fluids to patients intravenously. According to the plaintiffs, Alaris has been a primary revenue driver for Becton’s largest business segment and Becton as a whole. [91] It is also subject to substantial FDA regulation and oversight to oversee safety and compliance. According to the complaint, although Alaris had already received FDA approval to market the product, in light of new FDA guidance and certain product-related issues, Becton determined it needed to seek approval for infusion pump changes that could significantly affect device safety or effectiveness through the FDA’s Premarket Notification 510(k) program. [92] The plaintiffs alleged that the company did not disclose that it believed such approval was necessary because it knew that certain of Becton’s Alaris infusion pumps experienced software errors and alarm prioritization issues. Instead, Becton actively assured the market that Alaris was poised to anchor Becton’s impressive guided FY20 revenue growth. Although Becton’s sales were temporarily delayed because it was making “enhancements” to Alaris, Becton allegedly disclosed that it expected to promptly resolve to the FDA’s satisfaction any technical issues. [93] However, Alaris was recalled several times and the expected growth did not occur. [94]

After the defendants filed their second motion to dismiss, the court dismissed the complaint, but the plaintiffs were granted leave to amend. In granting the motion to dismiss, the court held that the defendants did not unlawfully fail to disclose that the FDA would need to approve a 510(k) application before the business could continue selling Alaris products. [95] The court reasoned that since the FDA ultimately set forth that requirement in February 2020, Becton and current and former company executives were neither obligated to predict that move nor reveal such a prediction since “the mere possibility of administrative action is not enough to require disclosure.” [96] The allegations also lacked the requisite scienter because, although the plaintiffs presented confidential witnesses, the court did not find them compelling in part because the witnesses were “not alleged to have had any communication with either the individual defendants or representatives of the FDA.” [97]

The court also rejected the plaintiffs’ assertion that Becton had mischaracterized the software changes as “upgrades,” “enhancements” and “improvements.” [98] The court explained that it viewed the modifications in question as “‘upgrades,’ ‘enhancements,’ and ‘improvements,’ whether or not they were also implemented to ‘remediate’ or ‘fix’ previously identified issues.” [99] Ultimately, the court dismissed the action without prejudice, holding that when considering the available mix of information, no reasonable investor could bury their head in the sand and ignore the potential risks of regulatory action against the Alaris products. [100]

Court Decisions Regarding Financial Management

Though life sciences companies must obviously navigate the risks associated with development of new drugs and devices, they also encounter securities-law risks common to all public companies. In 2021, courts issued eight opinions in cases involving allegations of financial management, including: improper accounting, price fixing and disclosures relating to mergers or spin-offs, among other claims. Of the cases Dechert identified, the outcomes varied, with three being dismissed in whole in favor of defendants, [101] three more being dismissed in part, [102] one in which summary judgment for defendants was denied, [103] and one in which plaintiffs prevailed on their motion for summary judgment. [104]

Many of the opinions issued in 2021 in this category concern allegations of illicit sales tactics or market manipulation. [105] In one of those cases, In re Vaxart, Inc. Securities Litigation, formerly known as Himmelberg v. Vaxart, Inc., the complaint was previously discussed in Dechert’s 2019 edition of this report and has now reached a disposition. [106] In this case, the plaintiffs alleged that the defendants, a vaccine development company, the hedge fund that financed it and its officers, engaged in a fraudulent scheme to profit from artificially inflating the company’s stock price by announcing misleadingly that Vaxart’s oral COVID-19 vaccine candidate had been chosen for funding by U.S. “Operation Warp Speed.” [107] However, according to plaintiffs, that disclosure was incorrect as it was merely selected to participate in preliminary government studies to determine potential areas for possible partnership and support. [108] The court found that the complaint “adequately” alleged that two statements Vaxart had made were materially misleading. The first statement, that Vaxart had entered a partnership with a manufacturer that would enable the production of one billion Vaxart vaccine doses per year, was materially misleading because the manufacturer Vaxart allegedly partnered with was plausibly alleged to lack “the regulatory capacity, personnel, and wherewithal to produce even one dose, never mind one billion.” [109] Also found to be materially misleading was Vaxart’s statement that it had been “selected” for Operation Warp Speed when it had not been selected by the federal government as one of its leading vaccine developers or to receive federal funding. [110] Rather, Vaxart had been selected “to participate in a non-human primate (NHP) challenge study, organized and funded by Operation Warp Speed.” [111] As such, the court found that the plaintiffs had adequately alleged that Vaxart had made materially misleading statements, and denied Vaxart’s motion to dismiss. [112] However, the court did dismiss the case with respect to Vaxart’s co-defendant Armistice, a hedge fund that had acquired a majority stake in Vaxart in 2019. [113] Plaintiffs alleged that Armistice was engaged in a scheme to sell its remaining shares in Vaxart and exercise warrants after “popping” Vaxart’s share price by misleading the public about its vaccine development, so as to realize even greater profits. [114] But the court reasoned that even if this were true, the complaint did not plausibly allege that Armistice disseminated (or assisted Vaxart in disseminating) any of the misstatements at issue. [115] As such, the court dismissed the case as to Armistice, but with leave to amend. [116]

Another issue apparent in financial management opinions this year was alleged marketing campaigns for off-label drug uses. For example, Ferraro Family Foundation, Inc. v. Corcept Therapeutics Inc. concerned allegations that Corcept, the manufacturer of an orphan drug called Korlym approved to treat Endogenous Cushing’s Syndrome, was pushing physicians to prescribe off-label uses of Korlym to sustain Corcept’s business until its next drug could be developed. [117] Plaintiffs further alleged that due to Korlym’s designation as an orphan drug, Corcept had seven years of market exclusivity—a period that would soon be coming to an end. [118] The complaint alleged that, in the face of the loss of exclusivity, the defendants began to aggressively market Korlym to endocrinologists who had little knowledge of Endogenous Cushing’s Syndrome and thus “would be more susceptible to prescribing Korlym as a first-line therapy.” [119] In addition, the complaint cited ten confidential witnesses to support allegations that Corcept aggressively marketed Korlym for off-label use. [120] The plaintiffs brought suit under the PSLRA, alleging that the defendants made materially false and misleading statements regarding (1) Corcept’s speaker and education programs about Endogenous Cushing’s Syndrome, (2) Corcept’s marketing and promotional materials, (3) Corcept’s compliance with FDA regulations, (4) Korlym revenue and sales growth, and (5) on-label use of Korlym. [121] The court found that, at the motion to dismiss stage, the plaintiffs had adequately alleged that Corcept was engaged in an off-label marketing scheme of Korlym. [122] Next, the court reviewed the categories of allegedly false and misleading statements made by Corcept and found that only the statements made regarding Corcept’s marketing and promotion materials, compliance with FDA regulations, and on-label use of Korlym were actionable. [123] Finally, the court addressed scienter, agreeing with the plaintiffs that, “given that Korlym represented 100% of Corcept’s revenue and Corcept allegedly employed a widespread off-label marketing scheme to promote Korlym, it would be absurd to suggest that management was without knowledge of the off-label marketing scheme.” [124]

Minimizing Securities Fraud Litigation Risks

Life sciences companies continue to be a popular target for class action securities fraud claims. While many of the companies discussed above were successful in defending against these claims, companies should take steps to reduce the risk of being targeted in a securities fraud class action. Below is a list of practices that life sciences companies should consider:

- Companies should develop a long-term response plan to potential triggering events. Companies should strive to avoid inconsistency in public statements and fight the urge to respond reflexively. Companies should consistently evaluate and update their plans to respond to market conditions.

- Life sciences companies in particular deal with regulatory setbacks, negative side effects in clinical trials, clinical trial failures, etc. that, when disclosed, may trigger a stock drop. Be particularly cognizant when making disclosures or statements to disclose both positive and negative results, including after preliminary results are issued. Ensure that a disclosure regimen and processes are well documented and consistently followed.

- Smaller life sciences companies have been particularly susceptible to securities class actions and should work with counsel to ensure that they adopt a disclosure plan. Disclosure plans should not only cover written disclosures made in press releases or SEC filings, but also any statements made by executives during analyst calls. Websites should also be continually updated.

- Life sciences companies are not immune to issues that may cut across all industries and should be prepared to make appropriate disclosures relating to transactions, consolidated financials, internal controls, conflicts of interest, anticompetitive conduct, quality control, etc.

- Courts often have the benefit of hindsight to determine whether a product is defective by considering what defendants could or should have done differently. For example, courts often consider the existence of safer alternatives and the ability of the defendant to eliminate a product’s dangerous characteristics. Companies should consider not only whether a given product is defective on its own, but how it compares to potential alternative designs or formulations and how its benefits balance the risks.

- Because deal litigation has been at the forefront in filings against life sciences and other companies, materials to investors relating to the transaction should contain detailed explanations about the history of the transaction, alternatives to the transaction, reasons for recommendation, the terms of the transaction, fairness opinions, conflicts of interest, among other issues.

- Even if incorporated abroad, life sciences companies that are also non-U.S. issuers may be targeted in the U.S. despite events occurring that may not be U.S. specific.

- Regarding statements made in public filings, courts continue to weigh in on opinion statements, and the law is continuing to evolve. Be aware that opinion statements should not conflict with information that would render the statements misleading.

- Forward-looking information about a drug or device should be clearly identified as such and distinguished from historical fact. Analyst calls and webcasts should also identify disclosures as a forward-looking statement.

- Risk disclosures that are current, relevant and upfront help to ward off securities class actions. Ensure that public statements and filings contain not only general disclaimers relating to forward-looking statements, but also appropriate “cautionary language” or “risk factors” that are specific and meaningful, and cover the gamut of risks throughout the entire drug product life cycle—from development to commercialization.

- Be aware that former employees in all departments, not just those relating to clinical trials, may become confidential witnesses for shareholder plaintiffs. Educate employees about not sharing confidential information with others and limiting social media about the company.

- Develop and publish an insider trading policy to minimize the risk of inside trades, including 10b5-1 trading plans and trading Class action lawyers aggressively monitor trades by insiders to develop allegations that a company’s executives knew “the truth” and unloaded their shares before it was disclosed to the public and the stock plummeted.

- Work with insurers to hire experienced counsel with experience defending securities class action litigation on a full-time basis.

Endnotes

12017 saw a record increase of class action securities litigation overall with 411 cases, up from the 271 securities class actions filed in 2016. In 2020, 324 securities class actions were filed while 210 were filed in 2021.(go back)

2It should be noted that 21 of all 2021 filings fell in more than one category.(go back)

3Throughout this post, the terms “company” or “defendants” may be used to also include individual officers or directors.(go back)

4The cases were compiled through Westlaw searches of dispositive orders involving the Private Securities Litigation Reform Act (“PSLRA”) between January 1 and December 31, 2021, and cross-referencing them against filters in the Securities Class Action Clearinghouse filings by “Healthcare.” In many cases, the court dismissed the operative complaint without prejudice and amended complaints are anticipated.(go back)

5Throughout this survey, data from prior years is derived from Dechert LLP’s 2020 survey on the same topic. David Kistenbroker, Joni Jacobsen, Angela Liu, Dechert Survey: Developments in U.S. Securities Fraud Class Actions Against Life Sciences Companies, Dechert LLP (Jan. 28, 2021). The number of securities fraud class actions filed and decided in 2020, as well as the number of those brought against life sciences companies, are based on information reported by the Securities Class Action Clearinghouse in collaboration with Cornerstone Research, Stanford Univ., Securities Class Action Clearinghouse: Filings Database, SECURITIES CLASS ACTION CLEARING HOUSE (last visited Feb. 12, 2022). This survey includes litigation and cases involving drugs, devices, deal litigation and hospital management. As of February 12, 2022, the Securities Class Action Clearinghouse has reported a change in securities class action filing totals since Dechert published its previous survey in January 2021. In the 2020 Dechert survey, the Clearinghouse had listed the following totals for the years 2016-2020, respectively: 270, 412, 403 and 404.(go back)

6See id.(go back)

7In 2021, 59 out of a total of 210 lawsuits were brought against a life sciences company, or 1%. In 2020, 80 out of a total of 324 lawsuits were brought against a life sciences company, or 24.7%. In 2019, 97 out of a total of 402 lawsuits were brought against a life sciences company, or 24.1%. In 2018, 86 out of a total of 402 lawsuits were brought against a life sciences company, or 21.4%. These filings were tallied by filtering all Securities Class Action Clearinghouse filings by Healthcare, then sorting them by life sciences company named as defendant. See Securities Class Action Clearinghouse in collaboration with Cornerstone Research, Stanford Univ., Securities Class Action Clearinghouse: Filings Database, SECURITIES CLASS ACTION CLEARINGHOUSE (last visited Feb. 12, 2022) (these figures are based on information publicly available through February 12, 2022). The filings include litigation and cases involving drugs, devices, financial management, deal litigation and hospital management. Cases that were subsequently consolidated or amended were only counted once, unless the subsequent filing received a new docket number, in which case both filings were counted separately.(go back)

8In 2021, of these 59 different life sciences companies that were named in class action securities fraud complaints, 30 had a market capitalization of US$500 million or more, or 50.8%. Market capitalization figures are current as of the filing date and were compiled with Yahoo! Finance and Bloomberg. Yahoo! Finance, YAHOO.COM (last visited 16, 2021); Bloomberg, BLOOMBERG (last visited Dec. 16, 2021).(go back)

9In contrast, 3% of filings, or 45 of 59, were against life sciences companies with a market capitalization of US$2 billion or less. Of these 59 companies, 16 had a market capitalization of less than US$250 million.(go back)

10In 2020, about 5% of life sciences companies named in class action securities fraud complaints had a market capitalization of US$500 million or more.(go back)

11In 2019, 51% of life sciences companies named in class action securities fraud complaints had a market capitalization of US$500 million or more.(go back)

12In 2021, 24 of 59 cases were filed against these companies. In 2020, this number was 34 of 80, or 42.7%. In 2019, this number was 37 of 96, or 38.5%.(go back)

13In 2021, 9 of 24 complaints were filed against life sciences companies with a market capitalization of US$5 billion or more, or 37.5%. In 2020, that number was 14 of 34, or 41.2%.(go back)

149 of 53 is 15.3%.(go back)

15In 2016, 36 of 67 cases were filed in district courts in California and New York, or 7%. In 2017, this number was 35 out of 88, or 39.8%. In 2018, this number was 39 of 86, or 45.3%. In 2019, 53 of 97 cases were filed in district courts in Delaware and New York, or 54.6%. In 2020, 45 of 80 cases were filed in district courts in California and Delaware, or 56.3%. In 2021, 31 of 59 cases were filed in district courts in California and New York, or 52.5%.(go back)

16In 2020, filings in the Third Circuit were as follows: Delaware with 21 or 72.4%; the District of New Jersey with four or 13.8%; the Eastern District of Pennsylvania with three or 3%; and the Western District of Pennsylvania with one or 3.5%. In 2019, filings in the Third Circuit were as follows: the District of Delaware with 29, or 72.5%; the District of New Jersey with nine, or 22.5%; and the Western and Eastern Districts of Pennsylvania with one each, or 5% collectively. In 2018, eight of 18 filings brought in the Third Circuit were filed in the District of New Jersey, or 44%, and seven of those 18 were brought in the District of Delaware, or 38.9%.(go back)

17Pomerantz LLP appeared together with Bronstein, Gewirtz & Grossman, LLC as co-counsel on eight cases.(go back)

18In 2019, 46 of 97 securities fraud class action complaints filed against life sciences companies were filed in the first two quarters, or 47.4%. In 2020, 36 of 80 securities fraud class action complaints filed against life sciences companies were filed in the first two quarters, or 45%.(go back)

19See Am. Compl., In re FibroGen Inc.., No. 3-21-cv-02623-EMC 4-5 (N.D. Cal. Nov. 19, 2021).(go back)

20See id. at 4.(go back)

21Id. at 50-76.(go back)

22Id. at 77.(go back)

23Id. at 81.(go back)

24Id. at 88; see also, g., Am. Compl., Sanchez v. Decision Diagnostics Corp., No. 3:21-cv-00418-JAK-JPR 3-4 (C.D. Cal. Oct. 14, 2021) (alleging that Decision Diagnostics misled investors by falsely claiming that it had developed a finger-prick blood test that could detect COVID-19 in less than one minute, when, in actuality, it had failed to develop any viable COVID-19 test); Compl., Williams v. Penumbra, Inc., No. 3:21-cv-00420 3-7 (N.D. Cal.Jan. 15, 2021) (alleging that Penumbra failed to disclose to investors: (1) that the Jet 7 Xtra Flex, an aspiration catheter used to remove blood clots from arteries and veins in stroke patients developed, manufactured and sold by Penumbra, had known design defects that made it unsafe for its normal use; (2) that Penumbra did not adequately address the risk of the Jet 7 Xtra Flex causing serious injury and deaths, which had in fact already occurred; (3) that the Jet 7 Xtra Flex was likely to be recalled due to its safety issues); Am. Compl., In re Sesen Bio, Inc. Securities Litigation, No. 1:21-cv-07025-AKH 2-6 (S.D.N.Y. Dec. 6, 2021) (alleging that Sesen Bio, the developer of a treatment for non-muscle invasive bladder cancer called Vicineum, failed to disclose to investors that: (1) its clinical trials showed that Vicineum leaked out from the bladder into the body, interacting with non-cancerous cells and leading to side effects including potentially fatal drug-induced liver injury; (2) another clinical trial for Vicineum had more than 2,000 violations of trial protocol, including 215 classified as “major”; (3) three of its clinical investigators were found guilty of “serious noncompliance,” including “back dating data”; (4) it had submitted the tainted data in connection with applications for regulatory approval to market Vicineum; and (5) the European Medicines Agency had identified and raised serious concerns about Vicineum and its trials and conveyed such concerns to Sesen Bio.).(go back)

25Such suits comprised 19 of the 59 cases filed, or 2%.(go back)

26See Compl., Roberto Nicanor, et al. v. Ocugen, Inc., et al., No. 21-CV-02725 (E.D. Pa. June 17, 2021); Compl., Sothinathan Sinnathurai, et al. v. Novavax, Inc., et al., No. 21-CV-02910 (D. Md. Nov. 12, 2021).(go back)

27Compl. 66-81, Novavax, No. 21-CV-02910.(go back)

28Id. at 2.(go back)

29Id. at 3.(go back)

30Id. at 2.(go back)

31Id. at 9.(go back)

32Id.; see also, e.g., Compl., Jose Chung Luo, et al. v. Spectrum Pharmaceuticals, Inc., et al., No. 21-CV-01612 (D. Nev. Aug. 31, 2021) (alleging that problems in Neovasc’s clinical study meant that the FDA would require additional premarket clinical data before approving its cardiovascular treatment, and alleging that statements the company made about submitting its pre-market application without needing to gather further evidence was materially false and/or misleading); Compl., Marc Richfield, et al. v. PolarityTE, Inc., et al., No. 21-CV-00561 (D. Utah Sept. 24, 2021) (alleging that defendants failed to disclose to investors that the manufacturing facilities for the company’s sole product candidate did not comply with current good manufacturing practices; and that as a result, regulatory approval for the candidate was reasonably likely to be delayed; when defendants disclosed that it had received a Complete Response Letter from the FDA identifying deficiencies in a list of conditions or practices that are required to be resolved prior to the approval of Fennec’s product candidate); Compl., Daniel P. McLaughlin, et al. v. Nano-X Imaging Ltd., et al., No. 21-CV-05517 8-11 (E.D.N.Y. Oct. 5, 2021) (alleging that defendant engaged in a fraudulent scheme to profit from artificially inflating the Company’s stock price by announcing misleadingly that Vaxart’s oral COVID-19 vaccine candidate had been chosen for funding by U.S. “Operation Warp Speed” when it was merely selected to participate in preliminary government studies to determine potential areas for possible partnership and support).(go back)

33Such complaints comprised 13 of the 59 filings reviewed, or 22%.(go back)

34See Compl., Palm Tran, Inc. – Amalgamated Transit Union Local 1577 Pension Plan v. Emergent BioSolutions Inc., 8:21-cv-00955-PWG 1-2 (Dist. Md. Apr. 19, 2021).(go back)

35See id. at 1-4.(go back)

36See id. at 5.(go back)

37See id. at 7.(go back)

38See id. at 8.(go back)

39Such suits comprised 15 of 59 of the cases filed, or 4%.(go back)

40See, e.g., Compl., Marko Busic, et al. v. Orphazyme A/S, et al., 21-CV-03640 (N.D. Ill. July 9, 2021) (alleging that Orphazyme A/S issued offering documents that contained untrue statements of material fact because its product, arimoclomol, was not as effective in treating IBM as Defendants had represented and thus its commercial prospects, were significantly overstated); Compl., Benjamin Dresner, et al. v. Silverback Therapeutics, Inc., et al., No. 21-CV-01499 (W. D. Wash. May 29, 2020) (alleging the same violations as in Orphazyme but for its product candidate SBT6050).(go back)

41Compl., Jerald Vargas Malespin, et al. v. Longeveron Inc., et al., No. 21-CV-23303 7 (S.D. Fl. Sept. 13, 2021).(go back)

42See id. at 7-11(go back)

43See id. at 8.(go back)

44Id.(go back)

45See id. at 68-97(go back)

46See, e.g., Compl., Lewis v. CytoDyn Inc., No. 3:21-cv-05190-BHS 2-6 (W.D. Wa. Mar. 17, 2021) (alleging that CytoDyn engaged in a fraudulent scheme to artificially inflate its stock price by aggressively touting Leronlimab, a drug formerly promoted as a potential therapy for patients with HIV, as a treatment for COVID-19 while defendant investors dumped millions of shares).(go back)

47See Am. Compl., In re AstraZeneca PLC Sec. Litig., No. 1:21-cv- 00722-JPO (S.D.N.Y. Jul. 12, 2021).(go back)

48Id. at 4.(go back)

49Id.(go back)

50Id. at 5.(go back)

51Id. at 7, 92.(go back)

52Approximately 16.9%, or 9 of 53 cases, filed in 2021 were against non-U.S. issuers incorporated across nine countries. In 2020, 19 of 80 cases, or 24%, were filed against non-U.S. issuers.(go back)

53See Compl., Marvin Gong, et al. v. Neptune Wellness Solutions Inc., et al., No. 21-CV-01386 7-9 (E.D.N.Y Mar. 16, 2021).(go back)

54See id.(go back)

55Compl., Kurt Ziegler, et al. v. GW Pharmaceuticals, PLC, et al. No. 21-CV-01019 3-9 (C.D. Cal. May 27, 2021).(go back)

56Kistenbroker, et al., supra note 5 at 11.(go back)

57See Carr v. Zosano Pharma Corp., 2021 WL 3913509 (N.D. Cal. Sept. 1, 2021) (dismissal with leave to amend); Employees’ Ret. Sys. of City of Baton Rouge & Par. of E. Baton Rouge v. MacroGenics, Inc., 2021 WL 4459218 (D. Md. Sept. 29, 2021) (dismissal without leave to amend); In re Alkermes Pub. Ltd. Co. Sec. Litig., 523 F. Supp. 3d 283 (E.D.N.Y. 2021), aff’d sub nom. Midwest Operating Engineers Pension Tr. Fund v. Alkermes Pub. Ltd. Co., 2021 WL 5782079 (2d Cir. Dec. 7, 2021) (granting dismissal); In re Amarin Corp. PLC Sec. Litig., 2021 WL 1171669 (D.N.J. Mar. 29, 2021) (granting dismissal without prejudice); In re AnaptysBio, Inc., 2021 WL 4267413 (S.D. Cal. Sept. 20, 2021) (granting dismissal with leave to amend); In re Sona Nanotech, Inc. Sec. Litig., 2021 WL 5504758 (C.D. Cal. Oct. 28, 2021) (granting dismissal with leave to amend); In re Sorrento Therapeutics, Inc. Sec. Litig., 2021 WL 6062943 (S.D. Cal. Nov. 18, 2021) (granting dismissal with leave to amend); Smith v. Antares Pharma, Inc., 2021 WL 754091 (D.N.J. Feb. 26, 2021); Villare v. Abiomed, Inc., 2021 WL 4311749 (S.D.N.Y. Sept. 21, 2021) (granting dismissal with leave to amend).(go back)

58Kuhne v. Gossamer Bio, Inc., No. 20-CV-649-DMS-DEB, 2021 WL 1529934 (S.D. Cal. Apr. 19, 2021).(go back)

592021 WL 3913509 (N.D. Cal. Sept. 1, 2021).(go back)

60Id. at 414.(go back)

61Id. at *1.(go back)

62Id. at *2.(go back)

63Id.(go back)

64Id. at *3-4.(go back)

65Id. at *4.(go back)

66Id.(go back)

67Id.(go back)

68Id. at 5.(go back)

69Id.(go back)

70Id. at *10.(go back)

71Id. at *11 (citing In re Rigel Pharms., Inc. Sec. Litig., 697 F.3d 869, 884 (9th Cir. 2012)).(go back)

72Id.(go back)

7315 U.S.C. § 78u-5.(go back)

742021 WL 4311749, at *1-3 (S.D.N.Y. Sept. 21, 2021).(go back)

75Id. at *11.(go back)

76Id. at *16.(go back)

77Id. at *17.(go back)

78Id. (citing In re Anheuser-Busch InBev SA/NV Sec. Litig., 2020 WL 5819558, at *4 (S.D.N.Y. Sept. 29, 2020) and Steamfitters Loc. 449 Pension Plan v. Skechers U.S.A., Inc., 412 F. Supp. 3d 353, 361 (S.D.N.Y. 2019), aff’d sub nom. Cavalier Fundamental Growth Fund v. Skechers U.S.A., Inc., 826 F. App’x 111 (2d Cir. 2020)).(go back)

79Id. at *15, *20.(go back)

80Dura Pharms., Inc. v. Broudo, 544 U.S. 336, 341 (2005).(go back)

81See Abiomed, Inc., 2021 WL 4311749, at *11.(go back)

82Id. at *12.(go back)

83Id.(go back)

842021 WL 3079878 (D. Mass. July 21, 2021).(go back)

85Id. at *1, *7.(go back)

86Id. at *7.(go back)

87Id.(go back)

88See Industriens Pensionsforsikring A/S v. Becton, Dickinson & Co., No. 220CV02155SRCCLW, 2021 WL 4191467 (D.N.J. Sept. 15, 2021) (dismissal without prejudice); Turnofsky v. electroCore, Inc., No. CV 19-18400, 2021 WL 3579057 (D.N.J. Aug. 13, 2021) (dismissal without prejudice); In re Align Tech., Inc. Sec. Litig., No. 20-CV-02897-MMC, 2021 WL 1176642 (N.D. Cal. Mar. 29, 2021) (dismissal without prejudice); In re Curaleaf Holdings, Inc. Sec. Litig., 519 F. Supp. 3d 99 (E.D.N.Y. 2021) (dismissal with prejudice).(go back)

89See Rosi v. Aclaris Therapeutics, Inc., 19-CV-7118 (LJL), 2021 WL 1177505 (S.D.N.Y. Mar. 29, 2021); Bos. Ret. Sys. v. Alexion Pharms., Inc., No. 3:16-CV-2127(AWT), 2021 WL 3675180 (D. Conn. Aug. 19, 2021); Ferraro Fam. Found., Inc. v. Corcept Therapeutics Inc., No. 19-CV-01372-LHK, 2021 WL 3748325 (N.D. Cal. Aug. 24, 2021).(go back)

90No. 220CV02155SRCCLW, 2021 WL 4191467 (D.N.J. Sept. 15, 2021).(go back)

91Id. at 2-9.(go back)

92Id.(go back)

93Id.(go back)

94Id.(go back)

95Id. at 12.(go back)

96Id. at 13.(go back)

97Id. at 18.(go back)

98Id. at 12.(go back)

99Id.(go back)

100Id.(go back)

101See In re Baxter Int’l Inc. Sec. Litig., 2021 WL 100457 (N.D. Ill. Jan. 12, 2021); In re Galena Biopharma, Inc. Sec. Litig., 2021 WL 50227 (D.N.J. 5, 2021); In re Karyopharm Therapeutics Inc., Sec. Litig., 2021 WL 3079878 (D. Mass. July 21, 2021).(go back)

102See City of Hollywood Police Officers’ Ret. Sys. v. Henry Schein, Inc., 2021 WL 3434875 (E.D.N.Y. 3, 2021); In re Vaxart, Inc. Sec. Litig., 2021 WL 6061518 (N.D. Cal. Dec. 22, 2021); Derr v. Ra Med. Sys., Inc., 2021 WL 1117309 (S.D. Cal. Mar. 24, 2021).(go back)

103In re Merit Med. Sys., Inc. Sec. Litig., 2021 WL 1192133 (C.D. Cal. Mar. 29, 2021).(go back)

104In re Perrigo Co. PLC Sec. Litig., 2021 WL 3005657 (S.D.N.Y. July 15, 2021), reconsideration denied, 2021 WL 3773461 (S.D.N.Y. Aug. 24, 2021).(go back)

105Inchen Huang v. Higgins, 443 F. Supp. 3d 1031 (N.D. Cal. 2020); In re Mylan N.V. Sec. Litig., No. 16-CV-7926 (JPO), 2020 WL 1673811 (S.D.N.Y. Apr. 6, 2020); Pelletier v. Endo International, 439 F. Supp. 3d 450 (E.D. Pa. 2020).(go back)

106Kistenbroker, et al., supra note 5 at 8 n.32; In re Vaxart, Inc. Sec. , 2021 WL 6061518 (N.D. Cal. Dec. 22, 2021).(go back)

107Vaxart, 2021 WL 6061518, at *1.(go back)

108Id. at *1-*2.(go back)

109Id. at *2, *4.(go back)

110Id. at *2, *4.(go back)

111Id. at *2.(go back)

112Id. at *8.(go back)

113Id. at *1, *8.(go back)

114Id. at *8.(go back)

115Id. at *9.(go back)

116Id.(go back)

1172021 WL 3748325, at *1-*2 (N.D. Cal. Aug. 24, 2021).(go back)

118Id. at *2.(go back)

119Id.(go back)

120Id. at *3.(go back)

121Id. at *7.(go back)

122Id. at *16.(go back)

123Id. at *17-*22.(go back)

124Id. at *24.(go back)