Print

PrintNichol Garzon-Mitchell is Chief Legal Officer and Senior Vice President of Corporate Development at Glass, Lewis & Co. This post is based on her Glass Lewis memorandum. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance by Lucian A. Bebchuk and Roberto Tallarita (discussed on the Forum here); Companies Should Maximize Shareholder Welfare Not Market Value by Oliver Hart and Luigi Zingales (discussed on the Forum here); Reconciling Fiduciary Duty and Social Conscience: The Law and Economics of ESG Investing by a Trustee by Max M. Schanzenbach and Robert H. Sitkoff (discussed on the Forum here); and Exit vs. Voice by Eleonora Broccardo, Oliver Hart and Luigi Zingales (discussed on the Forum here).

With the growth of ESG investing has come heightened regulatory scrutiny. In the last Administration, the focus was on asset managers’ motives and particularly the dubious claim that ESG was a surreptitious effort to advance managers’ political preferences, rather than being used as a material risk-return characteristic. Now the focus has shifted to so-called “greenwashing”—the concern that some companies and funds overstate their ESG credentials.

In the wake of increased examination and enforcement activity on this issue, the U.S. Securities and Exchange Commission has now proposed its first rules and required disclosures for funds and investment advisers using ESG strategies. While the rules do not go as far as the European Union’s Sustainable Finance Disclosure Regulation (“SFDR”), if adopted they would substantially increase the disclosure obligations of funds and investment advisers that consider ESG factors. We encourage all interested parties to review the proposed rules and consider commenting on them. Given the priority the SEC has attached to this issue, funds and advisers may also want to consider planning a review of their ESG investment and stewardship approaches and disclosures in anticipation of some version of these rules being adopted in the coming year.

Background

The SEC’s proposal comes against the backdrop of remarkable growth in ESG investing. As the SEC notes, inflows of capital to ESG investment products have increased exponentially over the last two decades. In fact, U.S. domiciled assets integrating ESG strategies grew 42% between 2018 and the end of 2020. Today, about one in three dollars of total U.S. assets that are professionally managed, representing some $17.1 trillion, are in a strategy that considers ESG.

The SEC has responded to this growth in several ways. Signaling the issue’s importance, the SEC formed a climate and ESG task force last year to identify and pursue “ESG-related misconduct consistent with increased investor reliance on climate and ESG-related disclosure and investment.” This task force has already produced results. The SEC recently took enforcement action against an investment adviser that “did not always perform the ESG quality review that it disclosed using as part of its investment selection process for certain mutual funds it advised.” And the Commission’s 2022 examination priorities include “greenwashing” as one of its five significant focus areas for the year.

The Rule Proposals

On May 25, 2022, the SEC proposed two sets of rules to regulate funds’ use of names that refer to an ESG consideration and to require new disclosures from funds and advisers about their ESG strategies.

The “Names Rule”

The first set of proposed rules would amend the SEC’s “Names Rule” under the Investment Company Act of 1940. That rule requires funds with certain names to adopt a policy to invest 80% of their assets in the type of investments suggested by their name. The SEC proposes to subject funds whose name indicates that the fund’s investment decisions incorporate ESG factors (e.g., “Sustainable,” “Responsible,” “ESG,” “Climate,” or “Green”) to the Names Rule. As SEC Chair Gensler has put it, his goal is to give ESG fund investors the same certainty and transparency about what they are getting as when they buy “fat-free” milk in the grocery store. To that end, the proposed rules would also require funds to define the terms used in their name in their prospectus and prohibit “integration funds” (as defined below) from using ESG terminology in their name.

Although not directly related to greenwashing, the proposed rules would make other significant changes to the Names Rule, including extending the rule to fund names referring to other investment characteristics, such as “growth” or “value,” changing how derivatives are counted towards the 80%, and clarifying the limited circumstances and for how long a fund can depart from its 80% investment policy.

ESG Disclosure by Funds and Advisers

The second set of proposals would require additional disclosures from funds and advisers that consider ESG factors. To scale these disclosures, the proposed rules establish three categories of ESG funds based on how central ESG factors are to their strategy:

- ESG Integration. ESG Integration funds consider ESG factors alongside other non-ESG factors when selecting investments, but ESG factors are generally no more significant than non-ESG factors.

- ESG-Focused. ESG-Focused funds focus on one or more ESG factors as a “significant or main consideration” in selecting investments or in their engagement strategy (e.g., a fund that uses an inclusionary or exclusionary ESG factor screen or an index fund tracking an ESG-focused index).

- ESG Impact. ESG Impact funds are a subset of ESG-Focused funds that seek to achieve a specific ESG impact (e.g., a fund that seeks to advance the availability of clean water by investing in water treatment companies).

The proposal then would require different disclosures from funds and advisers falling in these categories in their prospectuses, annual reports, and adviser brochures. The proposed rules take what the SEC calls a “layered” approach, requiring key, high-level information earlier in the filing, with greater detail later on or in a supplemental filing. While there are a number of proposed new disclosures, some with complex details, key elements of them are summarized below.

Prospectus Disclosures

ESG Integration funds would be required to include a short narrative in their prospectus summarizing how the fund integrates ESG factors into its investment strategy. Later in the prospectus, such funds would provide more detail on how they consider ESG in their investment strategies and, if they consider GHG emissions, how and pursuant to what methodology they do so.

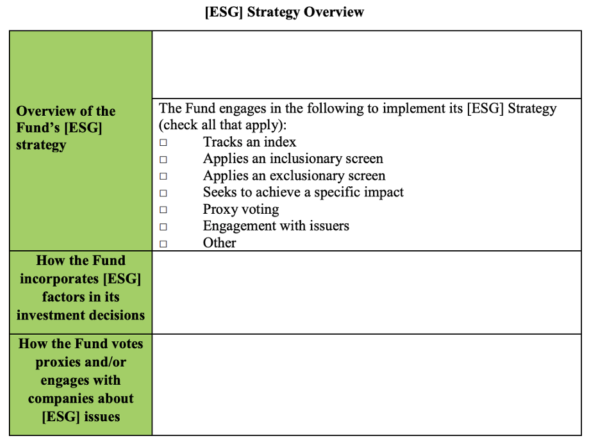

ESG-Focused funds would have to disclose a new “ESG Strategy Overview” table in a specified format, as shown in the SEC’s release:

As a subset of ESG-Focused funds, ESG Impact funds would make the same disclosures as ESG-Focused funds, as well as additional disclosures about the impact the fund is seeking to achieve, including:

- how it will achieve this impact,

- how the fund measures progress toward the specific impact the fund seeks to achieve, including the key performance indicators the fund analyzes,

- the time horizon the fund uses to analyze progress, and

- the relationship between the impact the fund is seeking to achieve and financial returns.

Annual Reports

Certain ESG-Focused funds would have to disclose additional information in their annual reports:

- Proxy Voting Records. ESG-Focused funds that use proxy voting as a significant means of implementing their ESG strategy would have to disclose “the percentage of ESG voting matters [involving ESG factors the fund considers in its investment decisions] during the reporting period for which the Fund voted in furtherance of the initiative,” as well as provide a link to their full voting record (Form N-PX);

- Engagement Meeting Metrics. ESG-Focused funds that use engagement as a significant means of implementing their ESG strategy would have to disclose progress on any key performance indicators of such engagement, as well as “the number or percentage of issuers with which the Fund held ESG engagement meetings and total number of ESG engagement meetings”;

- Impact Progress. ESG Impact funds would have to make qualitative and quantitative disclosures about their progress during the year in achieving their impact; and

- GHG Emissions. ESG-Focused funds that consider environmental factors in their investment strategies would have to disclose specific, quantitative information regarding the GHG emissions associated with their investments.

Finally, investment advisers that consider ESG factors would be required to make generally similar disclosures in their brochures and report certain other ESG information annually. If adopted, the SEC proposes a one-year transition period for most of the new disclosures, with funds’ follow-up information in their annual reports being required 18 months after the final rules’ effective date.

Takeaways

The proposed rules would significantly expand the scope of information and detail expected from funds and advisers on their ESG strategies. If adopted in anything like their current form, putting in place the necessary compliance processes and making the new disclosures will require substantial work from such funds and investment advisers. While not as granular and extensive as what is required by the EU’s SFDR, the required disclosure of portfolio companies’ GHG emissions for ESG-Focused funds that consider environmental factors has drawn particular early fire, with critics calling it a “real challenge” or even “unworkable” due to data limitations.

The proposed rules also reflect the importance of proxy voting and engagement, and seek to ensure that funds’ use of those strategies is disclosed and aligned with their stated ESG objectives. To that end, the new Strategy Overview table for ESG-Focused funds shown above would call for such funds that check either the “Proxy Voting” or “Engagement with Issuers” boxes to explain “[h]ow the Fund votes proxies and/or engages with companies about [ESG] issues.” The SEC explains that this disclosure should include whether the fund has specific or supplemental proxy voting policies and procedures that include one or more ESG considerations and, if so, which ESG considerations those policies and procedures address. Likewise, if an ESG-Focused fund seeks to engage with issuers on ESG matters, the fund must disclose an overview of the objectives it seeks to achieve through its engagement.

These disclosures would be supplemented by quantitative disclosures in the funds’ annual reports. As noted above, ESG-Focused funds that use proxy voting as a significant strategy would have to disclose the percentage of the fund’s votes in favor of relevant ESG voting matters. The SEC does not explain in detail how the fund’s relevant “ESG voting matters” would be determined for these purposes, but it does seek comment on whether a narrative discussion of the fund’s proxy voting should be allowed in addition to, or even instead of, this quantitative disclosure.

Likewise, ESG-Focused funds that use engagement as a significant strategy would annually report the number of ESG engagement meetings held. For these purposes, the SEC has proposed a prescriptive and circumscribed definition of an “ESG engagement meeting.” The SEC release explains that a “‘meet and greet’ between a fund’s adviser and the management of an issuer in the fossil fuel industry where the topic is mentioned, but only at a high level would be unlikely to meet the definition, even if the adviser and the issuer’s management do discuss transitioning away from fossil fuels.” On the other hand, the SEC notes that:

[I]f a fund adviser met with management of an issuer in the fossil fuel industry to urge the issuer to divest carbon intensive assets by the year 2030 due to their impact on the environment, with a list of measurable interim steps that could be made in each period and a follow-up meeting scheduled with management in six months to discuss progress toward that goal, the each such meeting would be an ESG engagement meeting under the proposed definition.

The discussion of this proposed definition also does not seem to account for collective engagement. Engagement, of course, is still an evolving practice and there is no one model for effective engagement. While the SEC’s goals of enhanced transparency and accountability in this context are laudable, commenters may want to focus on whether the proposed definition of an “ESG engagement meeting” is workable and adequately reflects the range of activities shareholders and their representatives undertake to substantively and meaningfully engage with companies on relevant ESG issues.

Next Steps

The SEC will take comments for 60 days after the proposed rules appear in the Federal Register. We encourage all interested parties to weigh in with the SEC. While the timing and content of any final rules is unknowable at this time, funds and advisers may also want to consider planning to review their ESG strategies to ensure that their investment and stewardship practices meet the SEC’s current and potential future expectations.