Print

PrintJason Frankl and Brian G. Kushner are Senior Managing Directors at FTI Consulting. This post is based on their FTI Consulting memorandum. Related research from the Program on Corporate Governance includes The Long-Term Effects of Hedge Fund Activism by Lucian A. Bebchuk, Alon Brav, and Wei Jiang (discussed on the Forum here); Dancing with Activists by Lucian A. Bebchuk, Alon Brav, Wei Jiang, and Thomas Keusch (discussed on the Forum here); and Who Bleeds When the Wolves Bite? A Flesh-and-Blood Perspective on Hedge Fund Activism and Our Strange Corporate Governance System by Frankl and Kushner Leo E. Strine, Jr. (discussed on the Forum here).

Introduction and Market Update

With summer just around the corner, FTI Consulting’s Activism and M&A Solutions team welcomes readers to our June 2023 Activism Vulnerability Report that highlights the findings from our Activism Vulnerability Screener for 1Q23 and discusses notable trends and themes observed in the world of shareholder activism during the 2023 proxy season.

Following the consecutive collapses of Silicon Valley Bank (“SVB”) and Signature Bank in March, other regional banks have been under pressure. Despite the U.S. Federal Reserve’s (“Fed”) efforts to prop up the banking sector, the high-profile failures coming in such close proximity undoubtedly contributed to depositors withdrawing more than $100 billion from First Republic Bank (“First Republic”) during 1Q23. This news, coupled with First Republic having a high percentage of uninsured deposits, triggered a run on the bank, causing a liquidity crisis that the bank could not quell. [1] On May 1, regulators seized First Republic, which had reported $232.9 billion in total assets on March 31, making it the largest U.S. bank failure since the 2008 financial crisis; JPMorgan Chase later agreed to buy the majority of its assets. [2] In the weeks following the First Republic Bank collapse, PacWest Bancorp, with shares down 66.2% year-to-date and deposits likewise hemorrhaging since SVB’s loss disclosure on March 8, announced it was exploring a potential sale. [3] [4]

The U.S. government’s battle over the debt ceiling, though resolved in early June, destabilized markets in May when it appeared lawmakers might not come to a resolution. [5] Despite the instability, investors were granted some breathing room in May as inflation continued to recede from its June 2022 peak. [6] The Fed issued its tenth consecutive interest rate hike in May, and although recent positive macroeconomic data has left the option open to future rate increases later this summer, analysts are expecting the Fed to pause tightening for at least one meeting to determine if additional rate hikes are warranted. [7] A pause may be more beneficial to investors than a direct rate cut would be; the S&P 500 has historically climbed 16.9% on average in the 12 months following a rate pause compared to a 1.0% drop in the 12 months following a rate cut. [8] At this point, market participants seem to believe the Fed will pause this month, but could resume rate tightening as early as July. However, additional rate hikes may carry consequences of their own, as the ever-present threat of a recession exposes risks to equity investors, just when it seemed the market was moving past a potential banking crisis. [9]

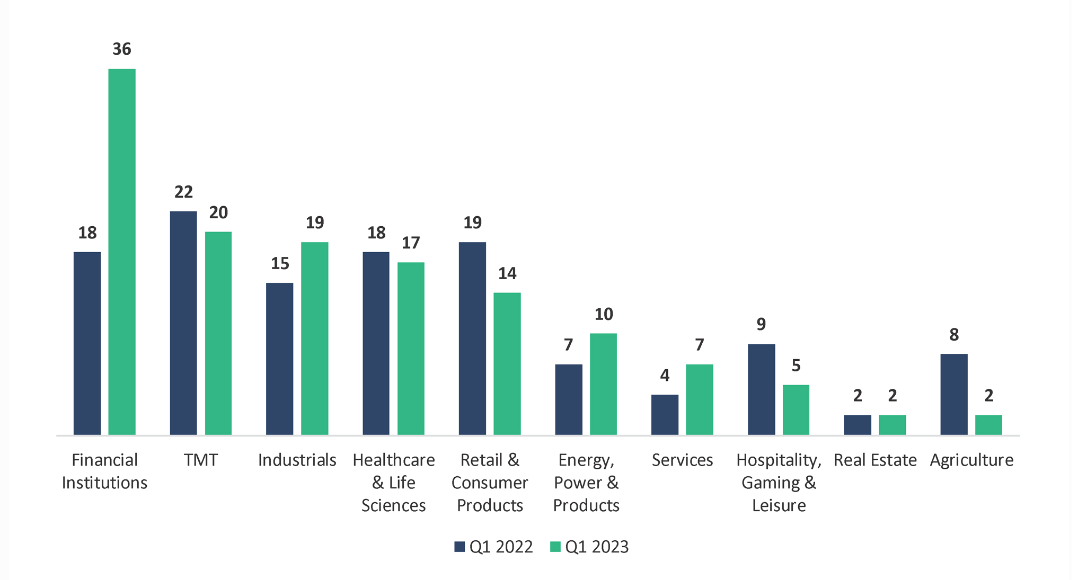

With share prices of financial institutions under pressure, shareholder activists began circling the sector. Campaigns focused on financial institutions doubled in 1Q23 relative to the same period last year. The Telecom, Media & Technology (“TMT”) and the Industrials sectors were also a focus for activists during the quarter.

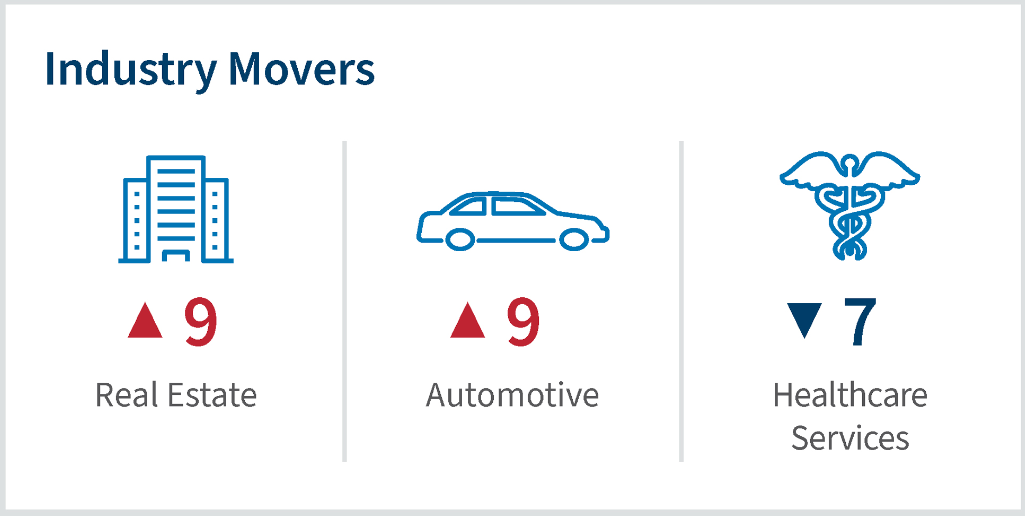

Industries that saw the greatest increase in vulnerability in 1Q23 were the Real Estate and Automotive, both industries with considerable interest rate sensitivity, each increasing nine spots in vulnerability according to our Activism Vulnerability Screener. The Healthcare Services industry experienced the largest decline in vulnerability, dropping seven positions in the rankings.

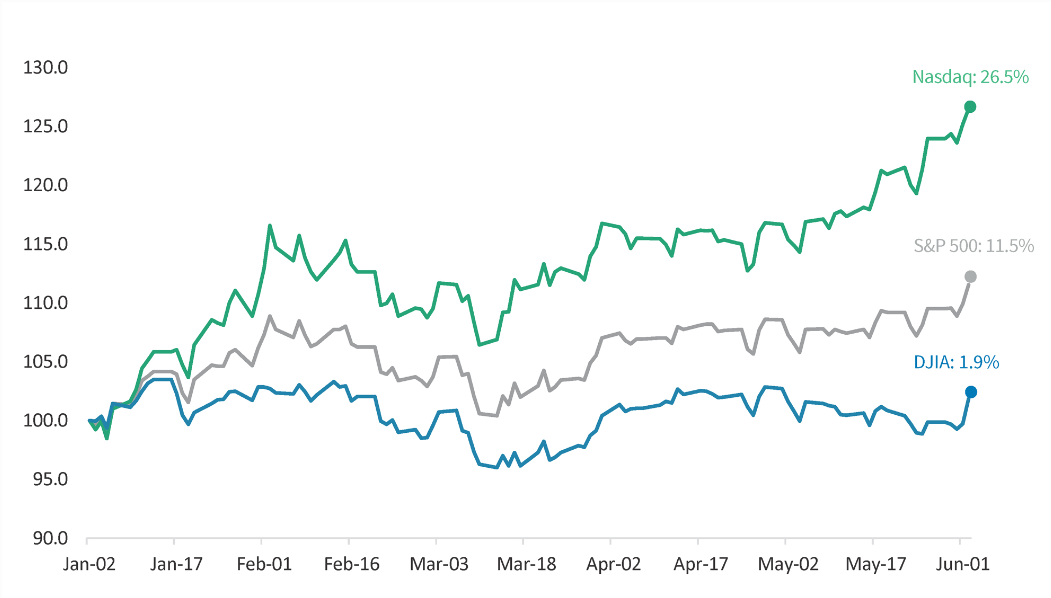

As of June 2, 2023, the Nasdaq Composite was higher by 26.5% year-to-date, the S&P 500 increased by 11.5% and the Dow Jones Industrial Average (“DJIA”) was up by 1.9% (see graphic below). Over the same period, the CBOE Volatility Index (“VIX”) was down 26.6%. [10]

Year-to-Date Performance (2023) [11]

Shareholder Activism Update

Activist campaigns increased 8.2% in 1Q23 (132 campaigns) compared to 1Q22 (122 campaigns). [12] The Financial Institutions sector was the most targeted sector during the quarter by a large margin, as 36 campaigns were initiated in 1Q23 compared to 18 campaigns in 1Q22. The heightened activist activity observed in the Financial Institutions sector was largely driven by depressed stock prices and underperformance, as interest rates hikes continue to expose fundamental weaknesses in participants of the sector (e.g., Dow Jones U.S. Select Regional Bank Index fell 27.5% YTD.) [13] [14] Blue Foundry Bancorp, AmeriServ Financial, Inc. and Genworth Financial, Inc. were just some of targets pursued by activists in 1Q23, and the financial sector continues to be top-of-mind for activists into the second quarter. [15] Other noteworthy contributors to the campaigns total include the TMT sector and the Industrials sector, tallying 20 and 19 campaigns in 1Q23 compared to 22 and 15 campaigns in 1Q22, respectively. Together, the three sectors accounted for 56.8% of total campaigns initiated during the quarter. [16]

Since the conclusion of 1Q23, campaigns have been launched against Aimia, Inc. and Sound Financial Bancorp, Inc. (“Sound Financial”). [17] Of the more recent campaigns, Stilwell Value LLC (“Stilwell”) is seeking board representation at Sound Financial, citing the belief that the assets of the entity are not adequately reflected in its current share price. [18] The pursuit by Stilwell came just two weeks after the activist unsuccessfully bid for board representation at Peoples Financial Services Corp. [19]

Activist Targets by Sector – Q1 2023 Year-Over-Year Change [20]

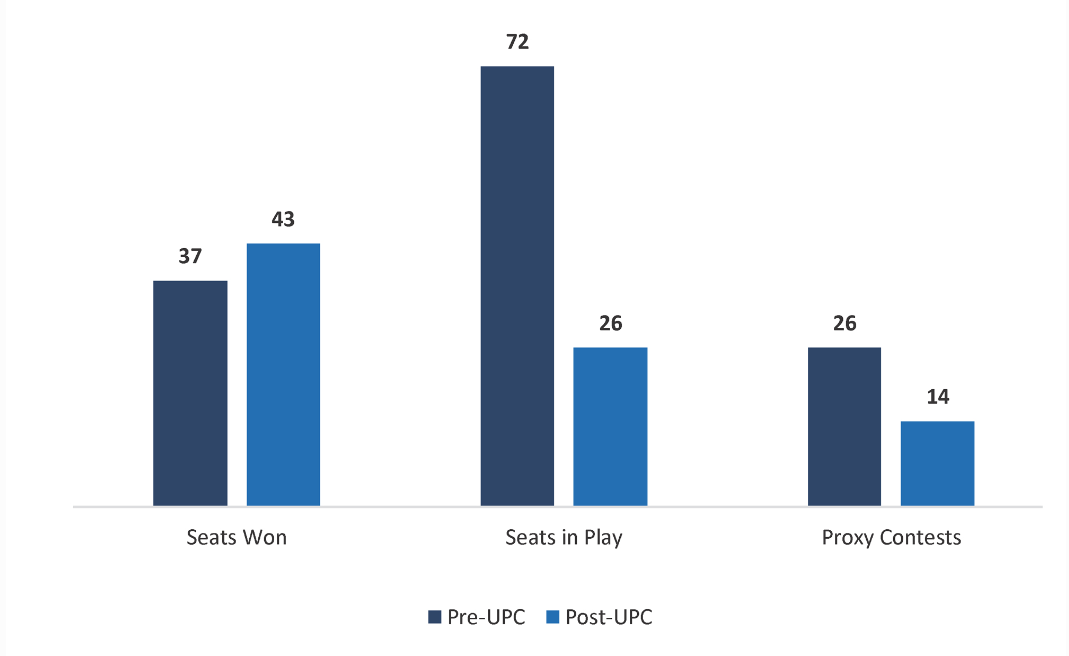

In the United States, total seats won, including seats won via settlement, increased 11.1% in 1Q23 compared to the same prior year quarter. Since the adoption of the Universal Proxy Card (“UPC”) on September 1, 2022, through the end of 1Q23, the number of seats won in the U.S. increased 16.2%. The number of seats remaining in play for upcoming votes decreased 63.9% compared to the same time period last year. [21] Further, significantly fewer proxy contests have been launched (14 vs. 26 in the prior year). [22] These statistics may suggest that UPC’s implementation, so far, has led to a higher volume of seats won, while decreasing the occurrence of proxy fights between activist investors and target companies.

The Effects of UPC on Board Seats and Proxy Contests [23]

The demand data suggests this as well. Settlements accounted for 12.5% of all closed campaign demands from September 1, 2022 through June 2, 2023, relative to 8.5% during the four-year period from August 31, 2018 to August 31, 2022, the cutoff date for the new regulation. The percentage of demands that went to a vote also decreased from the pre-UPC era: 2.9% went to a vote in the four years prior to the new regulation, compared to just 1.1% in the eight months following enactment. [24] Preliminary data of campaign results thus far points to the accuracy of the previous forecast mentioned in FTI Consulting’s Q4 2022 Vulnerability Report, that settlements will likely increase in the 2023 proxy season due to UPC. While this initial data seems to support this prediction, outcomes of ongoing campaigns and future proxy seasons need to be evaluated to validate such a trend.

U.S. activists’ demands involving M&A mimicked the global trend of M&A deal volume continuing to fall throughout early 2023. [25] In 1Q23, the number of demands by activists involving M&A decreased by 47.4% quarter-over-quarter (20 in 1Q23 vs. 38 in 1Q22). [26] M&A-related activist demands continue to be modest as interest rate hikes, inflation and recessionary fears hinder companies’ dealmaking enthusiasm. [27] Though weakening valuations may continue to invigorate activists in some areas, the pressure in M&A markets may prove a bigger counterweight than previously thought.

Large-cap companies continue to be highly targeted, as the percentage of campaigns involving large-cap companies remained consistent from 1Q22 (41.8% in 1Q23 vs. 41.7% in 1Q22). [28] A trend predominately targeting large-cap companies has emerged, commonly known as “swarming,” or when multiple activists are pursuing the same target. [29] We observed this trend start to show up in the data, as 36% of 1Q23 campaigns were initiated at a target company already navigating activist pressures. [30] A potential driver of this new trend may be the depressed stock prices of large corporations whose shares were once richly valued, thus allowing activists to capitalize on low valuations by acquiring larger stakes. However, swarming could also be a byproduct of a scarcity of promising targets. [31] A potential issue with swarming is that activists often have opposing views on key topics, presenting several conflicting narratives simultaneously to the company and other shareholders and obstructing efforts to create value-additive change. [32]

One example, beginning in late 2022, Ritchie Bros Auctioneers Inc. (“Ritchie Bros.”), an industrial auctioneer, announced plans to acquire IAA, Inc. (“IAA”), an online automobile auctioneer. Shortly after this announcement, activists and Ritchie Bros. shareholders Luxor Capital (“Luxor”), Starboard Value (“Starboard”) and Ancora Advisors began commenting on the situation. In December 2022, Luxor publicly opposed the merger. [33] The next month, Starboard offered a $500 million investment if its CEO, Jeff Smith, was appointed to Ritchie Bros.’ Board and if the IAA acquisition was completed. [34] In February 2023, Ancora Advisors supported the acquisition and criticized funds who opposed the merger. [35] On March 12, 2023, despite the many conflicting voices and interests, along with a lack of support from ISS and Glass Lewis, Ritchie Bros. received shareholder approval for the merger. [36]

We also recently observed a trend of activists seeking change at companies listed in foreign markets. In 1Q23, despite a slight increase in campaign volume, the U.S. accounted for 54.1% of campaign activity, compared to 60.0% in 1Q22. This proportion change was due to the number of target companies in foreign markets increasing 29.3%, to 106 in 1Q23 from 82 in 1Q22. [37] In 1Q23, Elliott Management initiated a campaign in Japan against Dai Nippon Co. Ltd. (“Dai Nippon”). [38] Following this, in March, Dai Nippon announced its largest share buyback in the company’s history, promising to repurchase approximately 30% of its market capitalization. [39] Likewise, in April, ValueAct Capital Partners (“ValueAct”) initiated a campaign against Japanese retail giant Seven & i Holdings Co. Ltd. (“Seven & i”), demanding the company spin off its 7-Eleven convenience store chain. The activist was seeking to replace four board members, but recent news from the Japanese company unveils a successful defense against ValueAct, as all 15 proposed directors by the company were elected. [40] [41] Meanwhile, Jeff Ubben’s Inclusive Capital Partners made its largest investment to date in German pharmaceutical giant, Bayer AG (“Bayer”). [42] This stands in contrast to 1Q22, when established activist funds initiated fewer campaigns overseas. [43] Looking to the future, as the U.S. markets evolve and the activism landscape becomes potentially more crowded, we will continue to monitor where U.S. activists allocate money overseas and how campaigns run their course as shareholder activism in foreign markets increases in popularity.

With the activist asset class expanding, and a limited appetite to pursue M&A initiatives in the current U.S. market, the question becomes “how will activists evolve their strategies to differentiate themselves?” [44] The increased interest in foreign markets and swarming could be a forced reaction as activists jockey for position and opportunities, as the large field of activists continues to grow. As markets evolve and regulation adapts, we will be keeping an eye out for savvy activists looking to innovate and differentiate in response to these changes in the market and regulations.

The Importance of Company Directors

Over the past two decades as the number of activists and assets under management of existing activists have grown, corporate directors are accumulating experience sitting across the table from activists. As of 2022, 38% of directors in Russell 3000 companies have experienced being targeted by an activist campaign. [1] Finding success when approached by an activist starts with understanding how to address them proactively, and potentially welcoming individuals on the board if it provides a strategic opportunity. [46]

Activists derive power in their ability to persuade shareholders. If a company wants to work proactively to avoid shareholder activism or minimize the distraction of a campaign, they must understand shareholder sentiment and operate to maintain shareholder support. [47]

For companies targeted in the current proxy season, just over 70% of cases involved SG&A costs above their peer group, leaving room for activists to create value by streamlining operations and cutting excessive costs. [48] In October 2022, Meta Platforms, Inc. (“Meta”) received a letter from Altimeter Capital Management demanding headcount reductions and reduced capital expenditures.[49] Months later, CEO Mark Zuckerberg opened the February 2023 (4Q22) earnings call by stating, “I want to discuss my management theme for 2023, which is the year of efficiency.” [50] In the April 2023 (1Q23) earnings call, Mr. Zuckerberg followed up with an immediate reference to the progress being made regarding efficiency and the improvement of its financial position. [51] Meta provides an excellent example of quickly taking action and communicating with shareholders to maintain support. Since the original conference call in February, the stock is up 78.0%. [52]

In the current proxy season, 67% of targeted companies had lower returns on capital employed than peers. [53] On May 5, 2023, Bradley Radoff filed a Schedule 13D disclosing a 5.7% stake in LifeVantage. In the filing, Mr. Radoff stated his intention to hold management accountable to a double-digit EBITDA margin and to implement a value-enhancing capital allocation framework. Mr. Radoff is also pushing for an enhancement of the company’s directors. Investors seemed to agree, as the stock has risen 27.8% since the date of filing. [54]

As shareholder activism continues to grow, experienced directors are a strong asset for any company, especially if their approach to oversight mimics the mindset of an activist investor. Such a mindset enables them to preempt a possible activist attack and, if they have experience working through a playbook of activist defense tactics, understand how to govern shareholder support. Will companies add board members based on previous experience with shareholder activists? And will this experience prove to be valuable in future engagements?

Observations & Insights

The 2023 proxy season has largely kept pace with the strong momentum built during the breakout year for shareholder activism we saw in 2022, resulting from “pent up” interest among activists eager to deploy war chests of capital once the pandemic subsided. While we are still in the final innings of the 2023 proxy season, there have already been over 360 companies in the U.S. that were subject to activist demands, robust by historical standards yet slightly below trend compared to last season, as some activists have taken a “wait and see” approach to how the SEC’s new universal proxy card (UPC) rules play out. Things are also getting busier in Canada, Europe and Asia – measured by volume, market cap and publicity – with over 260 non-U.S. companies finding themselves in the crosshairs of an activist this season, including high profile engagements at Bayer, Alibaba, Airbus and Seven & i.

The 2023 proxy season most notably ushered in the new UPC rules that took effect in the U.S. on September 1, 2022. Leading up to the 2023 season, UPC was our industry’s shiny new object that unleashed a tsunami of spirited discourse and debate on how the “mix-and-match” capability of UPCs would impact shareholder activism.

This is what we have seen in the activism trenches under UPC – settlements, settlements . . . and more settlements. The UPC format has made many shareholder activists think twice about going for board control and has resulted in more focused campaigns seeking to replace only the most vulnerable incumbent directors. As a result, boards have been more willing to settle on one or two seats held by their weakest-link directors rather than taking their chances at an annual meeting. The numbers speak for themselves – during the 2023 season in the U.S., ~50 situations have settled, resulting in ~90 dissident nominees being seated on boards – less than 20 campaigns have gone to a vote or are scheduled to go to a vote.

Since prior to the UPC rollout, we have been pounding the table for people to ignore narratives advanced by company-side advisors that UPC would open up the floodgates for first-time activists because the rules would purportedly make it easier and cheaper for them to run proxy fights. Woven into these narratives were patently false and irresponsible assertions that any shareholder would be able to free-ride the company’s proxy card without conducting its own solicitation under the new rules.

Recent data clearly dispels these claims – during the 2023 proxy season, the rate of U.S. campaigns commenced by first-time activists as a percentage of all campaigns has stayed almost exactly in line with past years (low 20% range since 2020). In addition, these proxy fights did not get any cheaper for activists under the new rules – the dissidents waging UPC campaigns that already went to a vote or are scheduled to go the distance expected to spend on average ~$1.15 million per campaign, according to their proxy statements. Ironically, the same company advisors who claimed that UPC would make proxy fights cheaper and more accessible to shareholders have actually driven up the cost of running a dissident campaign by advising companies to expand their advance notice bylaw procedures under the guise that they must be aligned with the new UPC rules.

— Andrew Freedman, Chair, Shareholder Activism Practice Group, Olshan Frome Wolosky LLP

Screener Results

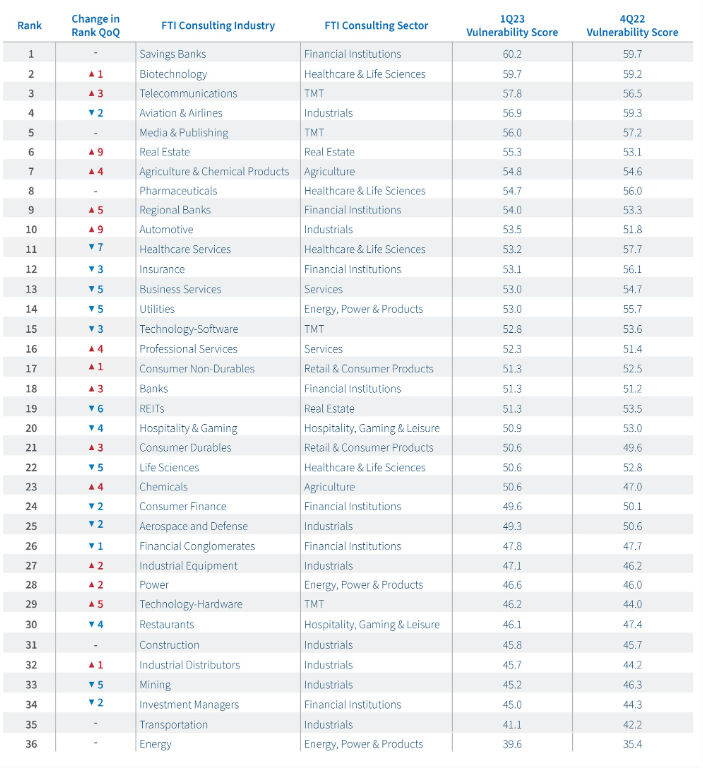

Few industries experienced substantial changes in their vulnerability rankings, tracking with what we observed in 2H22. We did not observe any industries that moved 10 or more spots in our 1Q23 data. The Savings Bank industry held steady from 4Q22 and continued to rank as the most vulnerable industry to activism. We would be remiss not to mention the Real Estate industry, which jumped nine spots into the top six industries most vulnerable to activism. Following a period of rapid home sales and home-price appreciation, the housing market in the U.S. has recently cooled, as home affordability is becoming more stressed (the average 30-year fixed mortgage rate surpassed 6%) [55] Commercial real estate has fared even worse, as office and property valuations took a nosedive since the onset of the COVID-19 pandemic. [56] Recent banking stressors from small- and mid-size banks are exacerbating these concerns, as about 80% of bank loans for commercial properties come from regional banks. [57]

Similarly, the Automotive industry jumped nine spots during the quarter, entering the top 10 most vulnerable industries for the first time since 2Q22, primarily driven by low total shareholder returns. The pandemic-fueled disruption of global supply chains forced automakers to slash production of new vehicles and resulted in higher car prices. Although new vehicle supply is now beginning to improve, demand has subsequently weakened, which, coupled with stubbornly high interest rates, may continue to challenge the industry in 2023. [58]

What This Means

With most indicators suggesting the credit cycle is veering toward a downturn, it seems activists are capitalizing on discounted valuations by initiating a multi-year record-high number of campaigns during the year so far. [59] The current macroeconomic environment and changing regulatory landscape may provide activists further opportunities to focus their demands on profitability and cost-cutting measures. Investors will be keeping a close eye on the Fed to determine if its tightening cycle will end soon and navigate a so-called soft landing. In the background, although the debt ceiling debate was resolved and a catastrophic default was avoided until at least January 1, 2025, now that Pandora’s Box is open, the issue could become a recurring battle in the future. [60]

FTI Consulting’s Activism Vulnerability Screener Methodology

The Activism Vulnerability Screener is a proprietary model that measures the vulnerability of public companies in the United States and Canada to shareholder activism by collecting criteria relevant to activist investors and benchmarking to sector peers.

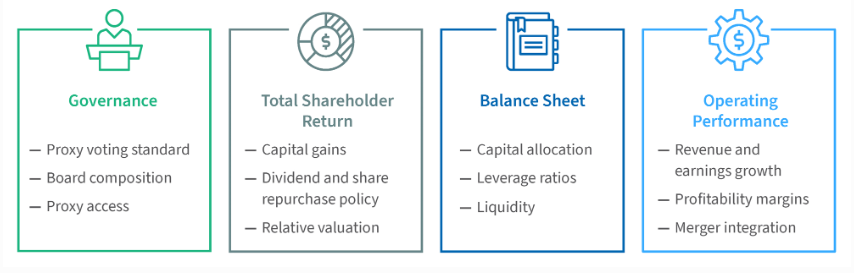

The criteria are sorted into four categories, scored on a scale of 0-25, (1) Governance, (2) Total Shareholder Return, (3) Balance Sheet and (4) Operating Performance, which are aggregated to a final Composite Vulnerability Score, scored on a scale of 0-100.

- By classifying the relevant attributes and performance metrics into broader categories, experts at FTI Consulting can quickly uncover where vulnerabilities are found, allowing for a more targeted response. FTI Consulting’s Activism and M&A Solutions team determined these criteria through research of historical activist campaigns in order to locate themes and characteristics frequently targeted by activist investors.

The following is a selection of themes that are included for each category:

The Activism and M&A Solutions team closely follows the latest trends and developments in the world of shareholder activism. Due to the constantly evolving activism landscape, FTI Consulting’s Activism and M&A Solutions team consistently reviews the criteria and their respective weightings to ensure the utmost accuracy and efficacy of Activism Screener.

Endnotes

1Rachel Louise Ensign, Eliot Brown, AnnaMaria Andriotis, Gina Heeb, Why First Republic Bank Collapsed, The Wall Street Journal (May 1, 2023), https://www.wsj.com/articles/first-republic-bank-collapse-why-banking-crisis-61660d96.(go back)

2Lora Kelley, First Republic is Sold: What to Know, The New York Times, (May 3, 2023), https://www.nytimes.com/2023/05/01/business/first-republic-stock-deposits-sale.html(go back)

3Candice Choi, The Banking Crisis: A Timeline of Key Events, The Wall Street Journal (May 11, 2023), https://www.wsj.com/articles/bank-collapse-crisis-timeline-724f6458.(go back)

4FTI Consulting analysis. Data provided by FactSet as of June 2, 2023.(go back)

5Alexandra Hutzler, Senate passes debt ceiling deal, staving off default, ABC News (June 1, 2023), https://abcnews.go.com/Politics/senate-passes-debt-ceiling-deal/story?id=99758031.(go back)

6Greg Iacurci, Here’s the inflation breakdown for April 2023, in one chart, CNBC (May 10, 2023), https://www.cnbc.com/2023/05/10/april-2023-cpi-inflation-report.html.(go back)

7Howard Schneider, Fed rate-hike pause still likely despite strong data, Reuters (June 2, 2023), https://www.reuters.com/markets/us/feds-new-projections-may-fill-void-interest-rate-guidance-2023-06-02/.(go back)

8Krystal Hur, The Fed probably won’t cut rates anytime soon. Why that’s good news for markets, CNN Business (May 15, 2023), https://www.cnn.com/2023/05/14/business/fed-rate-cut-markets/index.html.(go back)

9Wayne Duggan, June 2023 Stock Market Forecast, Forbes (last visited May 26, 2023), https://www.forbes.com/advisor/investing/stock-market-outlook-and-forecast/.(go back)

10FTI Consulting analysis. Data provided by FactSet as of June 2, 2023.(go back)

11Ibid.(go back)

12FTI Consulting analysis of activist campaigns. Data provided by Insightia as of March 31, 2023(go back)

13Enda Curran & Eric Martin, IMF Chief Says Rising Rates Exposed Banking Vulnerabilities, Bloomberg (May 1, 2023), https://www.bloomberg.com/news/articles/2023-05-01/imf-chief-says-rising-rates-exposed-banking-vulnerabilities.(go back)

14FTI Consulting analysis. Data provided by FactSet as of June 2, 2023.(go back)

15FTI Consulting analysis of activist campaigns. Data provided by Insightia as of March 31, 2023.(go back)

16Ibid.(go back)

17Ibid.(go back)

18Securities and Exchange Commission, Sound Financial Bancorp, Inc. – Schedule 13D (May 8, 2023), https://www.sec.gov/Archives/edgar/data/1113303/000110465923059877/tm2315658d1_sc13da.htm.(go back)

19Securities and Exchange Commission, Peoples Financial Corporation – Form 8-K (April 26, 2023), https://www.sec.gov/ix?doc=/Archives/edgar/data/770460/000143774923011927/pfbx20230501_8k.htm.(go back)

20FTI Consulting analysis of activist campaigns. Data provided by Insightia as of March 31, 2023.(go back)

21Shareholder Activism Update: Early Look at 2023 Trends, Lazard (April 18, 2023), https://www.lazard.com/research-insights/shareholder-activism-update-early-look-at-2023-trends/.(go back)

22Ibid.(go back)

23Ibid.(go back)

24FTI Consulting analysis of activist campaigns. Data provided by Insightia as of June 2, 2023.(go back)

25Emily Rouleau, ANALYSIS: There Was No Sign of an M&A Market Rebound in Q1 2023, Bloomberg Law (April 6, 2023), https://news.bloomberglaw.com/bloomberg-law-analysis/analysis-there-was-no-sign-of-an-m-a-market-rebound-in-q1-2023.(go back)

26FTI Consulting analysis of activist campaigns. Data provided by Insightia as of March 31, 2023.(go back)

27Anirban Sen & Andres Gonzalez, Global dealmaking sinks to lowest level in over a decade, Reuters (March 31, 2023), https://www.reuters.com/markets/deals/global-dealmaking-sinks-lowest-level-over-decade-2023-03-31/#:~:text=NEW%20YORK%2FLONDON%2C%20March%2031,appetite%20of%20companies%20for%20dealmaking.(go back)

28FTI Consulting analysis of activist campaigns. Data provided by Insightia as of March 31, 2023.(go back)

29Ed Hammond, Scary Activist Investors Aren’t That Scary Anymore, Bloomberg (April 21, 2023), https://www.bloomberg.com/opinion/articles/2023-04-21/scary-activist-investors-aren-t-that-scary-anymore.(go back)

30Shareholder Activism Update: Early Look at 2023 Trends, Lazard (April 18, 2023), https://www.lazard.com/research-insights/shareholder-activism-update-early-look-at-2023-trends/.(go back)

31Ibid.(go back)

32Ibid.(go back)

33Ritchie Bros. Takeover of ‘Inferior’ IAA Opposed by Luxor, Bloomberg (December 16, 2022), https://www.bloomberg.com/news/articles/2022-12-16/ritchie-bros-takeover-of-inferior-iaa-opposed-by-luxor?sref=p5QwRxCz.(go back)

34Ritchie Bros. Announces $500 Million Strategic Investment from Starboard Value, PR Newswire (January 23, 2023), https://www.prnewswire.com/news-releases/ritchie-bros-announces-500-million-strategic-investment-from-starboard-value-301727989.html.(go back)

35Response to Luxor’s Apparent “Short and Distort” Campaign Against IAA & Ritchie Bros, Ancora Alternatives (last visited May 17, 2023), https://mms.businesswire.com/media/20230223005447/en/1721440/1/Response_to_Luxor_s_Apparent_Short_and_Distort_Campaign_Against_IAA_and_Ritchie_Bros_February_23_2023.pdf?download=1.(go back)

36Securities and Exchange Commission, Ritchie Bros. Auctioneers Incorporated – Form 8-K (March 12, 2023), https://www.sec.gov/ix?doc=/Archives/edgar/data/1046102/000110465923032513/tm238171d1_8k.htm.(go back)

37FTI Consulting analysis of activist campaigns. Data provided by Insightia as of March 31, 2023.(go back)

38Ibid.(go back)

39Elliott Statement on Dai Nippon Printing, PR Newswire (March 9, 2023), https://www.prnewswire.com/news-releases/elliott-statement-on-dai-nippon-printing-301768540.html.(go back)

40Svea Herbst-Bayliss, ValueAct questions Seven & i strategy, pushed 7-Eleven spin-off, Reuters (April 3, 2023), https://www.reuters.com/business/retail-consumer/valueact-questions-seven-i-strategy-pushes-7-eleven-spin-off-2023-04-02/.(go back)

41Notice of the Results of the 18th Annual Shareholders’ Meeting. Seven & I Holdings Co., Ltd. (May 25, 2023).(go back)

42Hannah Kuchler & Olaf Storbeck, Bayer embraces activist Ubeen with place on its sustainability council, Financial Times (February 26, 2023), https://www.ft.com/content/0b4b2908-3f19-46d4-8574-c3d831ad3868.(go back)

43FTI Consulting analysis of activist campaigns. Data provided by Insightia as of March 31, 2023.(go back)

44Hannah Kuchler & Olaf Storbeck, Bayer embraces activist Ubeen with place on its sustainability council, Financial Times (February 26, 2023), https://www.ft.com/content/0b4b2908-3f19-46d4-8574-c3d831ad3868.(go back)

45Andrew Baker, David Larcker, Brian Tayan & Derek Zaba, The Evolving Battlefronts of Shareholder Activism, Hoover Institution (March 6, 2023), https://www.sidley.com/en/insights/publications/2023/03/the-evolving-battlefronts-of-shareholder-activism.(go back)

46Erin Essenmacher, Think Like an Activist, Directors & Boards, https://www.directorsandboards.com/articles/singlethink-activist.(go back)

47Brian Tayan, The Evolving Battlefronts of Shareholder Activism, Harvard Law School Forum on Corporate Governance (March 28, 2023), https://corpgov.law.harvard.edu/2023/03/28/the-evolving-battlefronts-of-shareholder-activism/#more-155437.(go back)

48What activists want in 2023, Insightia (May 16, 2023), https://one.insightia.com/news/activism/latest?newsID=49400.(go back)

49Meta shareholder wants Facebook parent to cut jobs, spending, Reuters (October 24, 2022), https://www.reuters.com/article/meta-platforms-shareholders-altimeter-ca-idCAKBN2RJ17X.(go back)

50Q4 2022 Earnings Call. Meta Platforms, Inc.(go back)

51Q4 2022 Earnings Call. Meta Platforms, Inc.(go back)

52FTI Consulting analysis. Data provided by FactSet as of June 2, 2023.(go back)

53What activists want in 2023, Insightia (May 16, 2023), https://one.insightia.com/news/activism/latest?newsID=49400.(go back)

54“Treasury Announces Marketable Borrowing Estimates,” U.S. Treasury Department press release, Aug. 1, 2022, https://home.treasury.gov/news/press-releases/jy0902.(go back)

55Matt Tracy, Analysis: Overexposed US regional banks could sell commercial property loans, Reuters (May 17, 2023), https://www.reuters.com/business/finance/overexposed-us-regional-banks-could-sell-commercial-property-loans-2023-05-17/.(go back)

56Nicole Goodkind, Commercial real estate is in trouble. Why you should be paying attention, CNN Business (March 27, 2023) https://www.cnn.com/2023/03/27/investing/premarket-stocks-trading/index.html.(go back)

57Ibid.(go back)

58John Rosevear & Michael Wayland, 2023 could be another difficult year for the auto industry – here’s why, CNBC (December 27, 2022), https://www.cnbc.com/2022/12/27/why-2023-could-be-another-difficult-year-for-the-auto-industry.html.(go back)

59What’s Next for the Credit Cycle? Loomis, Sayles & Company (last visited May 17, 2023), https://info.loomissayles.com/whats-next-for-the-credit-cycle.(go back)

60Cami Mondeaux, Biden signs debt limit deal, avoiding catastrophic default just two days before deadline, Washington Examiner (June 3, 2023), https://www.washingtonexaminer.com/news/white-house/biden-signs-debt-limit-deal-avoiding-catastrophic-default(go back)