Print

PrintJason Frankl and Brian G. Kushner are Senior Managing Directors at FTI Consulting. This post is based on their FTI Consulting memorandum. Related research from the Program on Corporate Governance includes The Long-Term Effects of Hedge Fund Activism (discussed on the Forum here) by Lucian A. Bebchuk, Alon Brav, and Wei Jiang; Dancing with Activists (discussed on the Forum here) by Lucian A. Bebchuk, Alon Brav, Wei Jiang, and Thomas Keusch; and Who Bleeds When the Wolves Bite? A Flesh-and-Blood Perspective on Hedge Fund Activism and Our Strange Corporate Governance System (discussed on the Forum here) by Frankl and Kushner Leo E. Strine, Jr.

Introduction

R-E-S-P-E-C-T … One year down in UPC!

UPC, also known as Universal Proxy Card, has surely garnered “respect” from both issuers and activists alike. FTI Consulting’s Activism and M&A Solutions team touches on this, as well as how a culture change in Japan is igniting a surge of activism, in our September 2023 Activism Vulnerability Report. This iteration presents our 2Q23 Activism Vulnerability Screener results, as well as our commentary on notable trends in the world of shareholder activism.

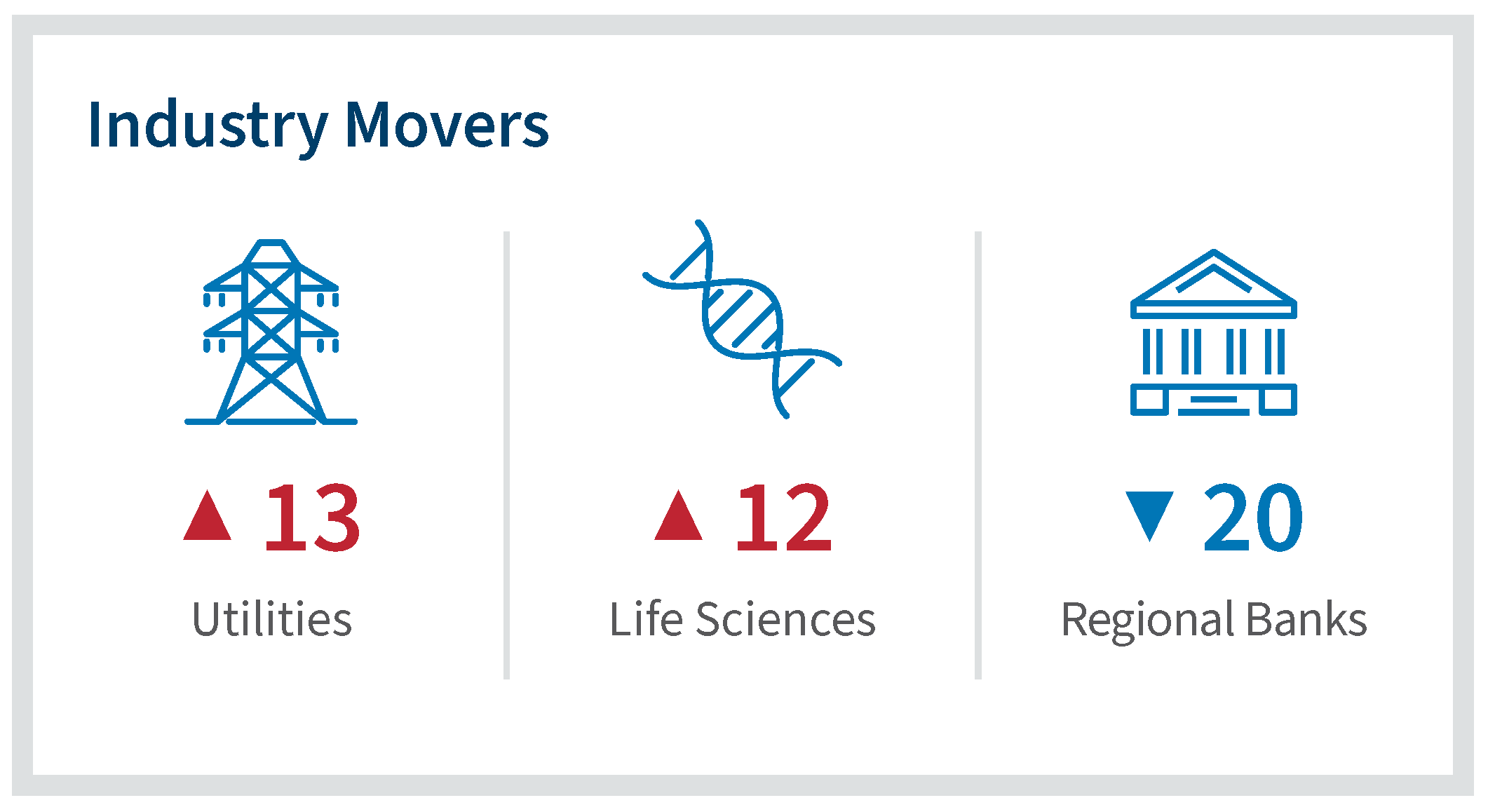

During the first half of 2023, financial institutions faced their most challenging period in more than a decade, even calling into question the viability of the regional banking model. At the same time, activist campaigns targeting financial institutions increased by more than 60% year-over-year during the first half of the year. By the end of 2Q23, fundamental concerns for the sector waned with the Regional Banks and Savings Banks industries appearing substantially less vulnerable in our rankings. By contrast, Utilities’ vulnerability increased dramatically, moving from number 14 last quarter (out of 36 industries) to the industry most vulnerable to activism. Additionally, industries in the Healthcare Services sector, including the Life Sciences, Pharmaceuticals and Health Services industries, all increased in vulnerability during 2Q23.

Click here to download the report

Market Update

Coming off the midst of the banking crisis in March, consensus opinion regarding the near-term health of the economy was looking less than favorable; however, as inflation started to cool in the summer, so too did the fear and pessimism in the market.1 Moderating inflation, higher consumer confidence and spending, and favorable labor markets have caused economists and banks to dial back their calls for a near-term recession, something the equity markets welcomed with open arms. Whispers of soft landings are on the rise once again, but the risk of a recession is still very relevant, mainly due to the Fed potentially increasing rates further in the future.2,3

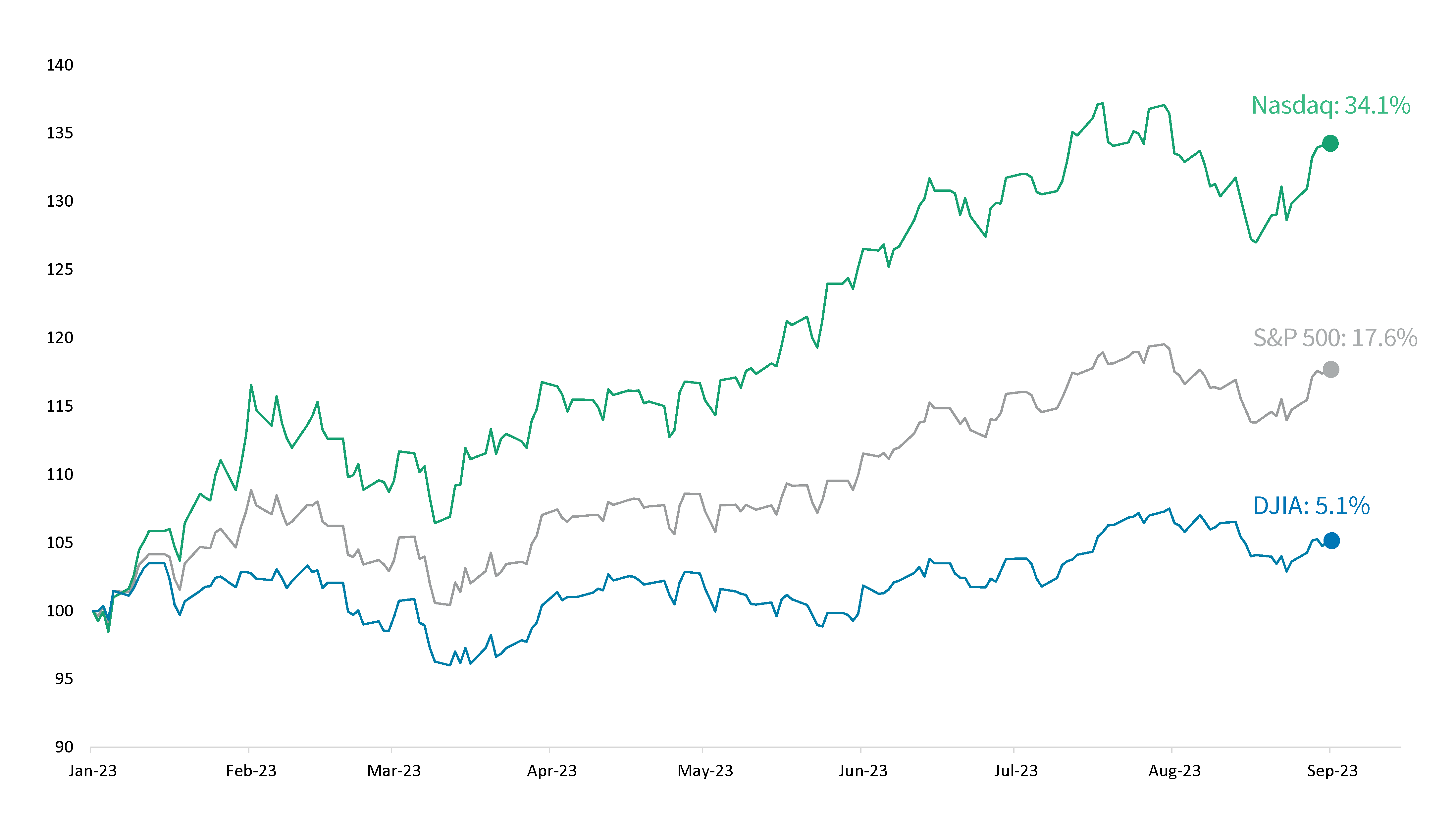

The credit markets are far from convinced, regardless of Wall Street’s optimism, as a New York Federal Reserve indicator, which tracks the difference between the three-month and 10-year Treasury yields, points to a 66% chance of a contraction within the next 12 months.4 Unlike its more mature older brother, the equity markets are signaling a different story seemingly sharing in the optimism, as markets have performed well year-to-date. The S&P 500 has returned 17.6%, while the Dow Jones Industrial Average and NASDAQ were in the green by 5.1% and 34.1%, respectively.5

While the Fed paused rate hikes at its June meeting, it raised rates by 25 basis points in July, bringing the target rate range to 5.25%-5.50%, the highest rates have been in 22 years.6,7 Fed Chairman Jerome Powell signaled that future rate hikes are still on the table.8

In recent months, long-term interest rates have also been rising. The U.S. Treasury 10-year bond yielded 4.2% as of September 1, 2023, remaining at elevated levels.9 This has pressured demand for interestrate-sensitive sectors. For example, sales of previously owned homes in July 2023 were lower than during any July since 2010.10 Delinquency rates for automobile loans in June 2023 were higher than during any June since at least 2013.11

Year-to-Date Performance (2023)12

While the equity markets have rebounded from last year’s lows, mergers and acquisitions have remained sluggish year-to-date. Globally, M&A activity declined in both transaction volume and value during 2Q23. The number of transactions dropped by 27.5% year-over-year to 8,364, while the value of transactions fell by more than 44% year-over-year to $501 billion in 2Q23.13 The situation in the U.S. and Canada has not fared any better. Transactions by value fell by nearly 40% year-over-year in 2Q23 to $267.1 billion.14 Notably, 2Q23 weakened sequentially from 1Q23 and there are limited signs of this reversing in the near term.

The most active sectors involved in M&A were Financial Institutions, Healthcare & Life Sciences, Industrials, Energy, Power & Products and Real Estate.15 Rising interest rates and continued uncertainty surrounding Fed rate hikes appear to have deterred would-be suitors from actively pursuing opportunities. Overall, we believe that M&A activity is likely to remain tepid over the near-term for most companies. As issuers adjust to the higher interest rate environment and increased costs of capital, transaction activity will likely be muted with the exception of interest rate-sensitive industries.

Shareholder Activism Update

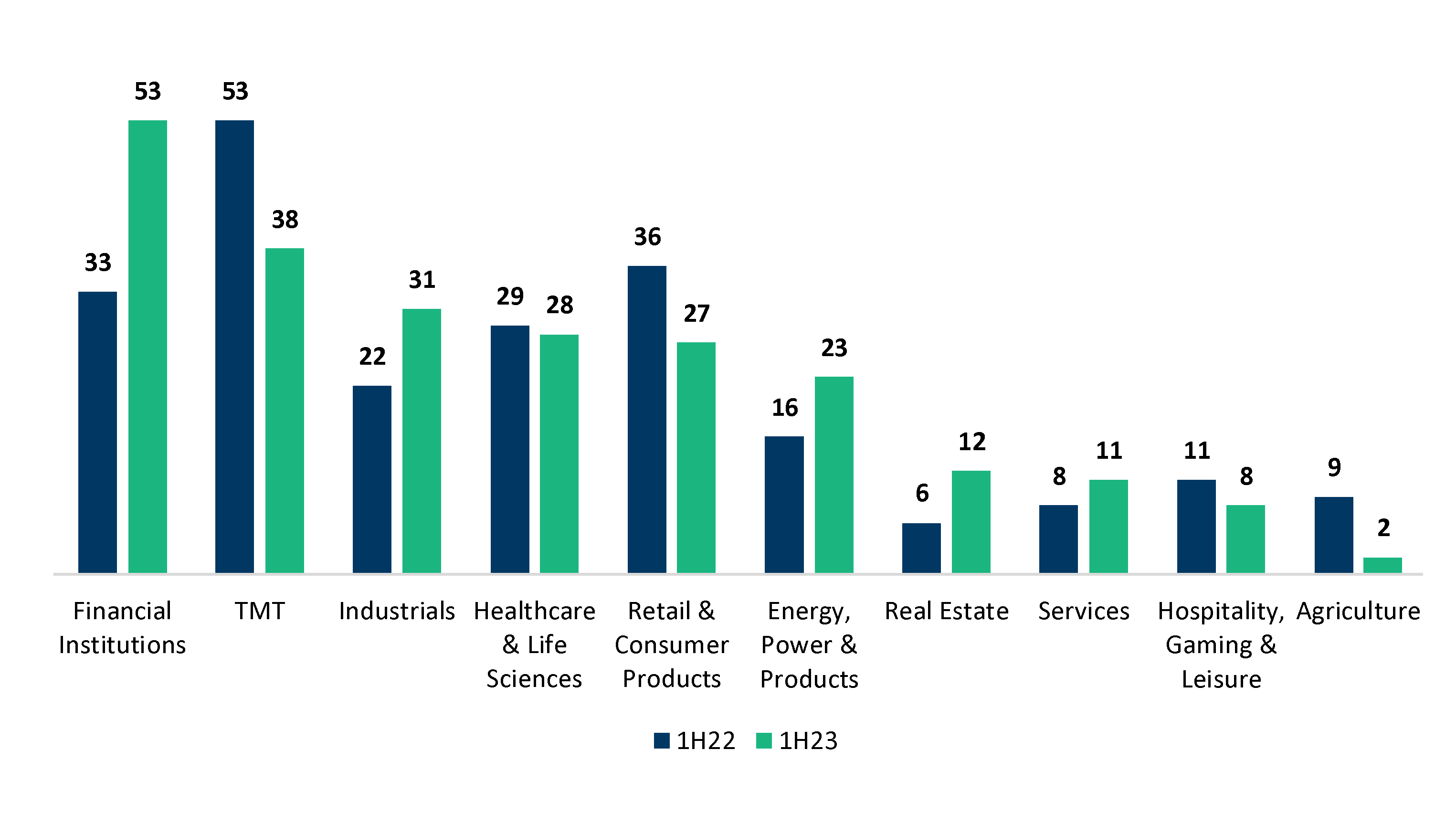

A total of 233 campaigns involving U.S. and Canadian-based companies were launched in 1H23.16 The number of campaigns in 1H23 was up 4.5% compared to 1H22.17 The Financial Institutions sector was the sector most targeted by shareholder activists in 1H23, representing 23% of all U.S. and Canadian campaigns in the first half of the year, followed by the TMT sector (16%) and the Industrials sector (13%).18 The increase in activist campaigns against the Financial Institutions sector may be attributed to the sector’s sustained underperformance, as the KBW Regional Bank Index is down 16.1% year-to-date and has underperformed the Russell 2000 by 25.2% since the year began.19 Recent threats of increased capital regulation and downgraded credit ratings across 10 small and midsize institutions may have contributed to this campaign surge.20,21 Although there were a number of campaigns in the sector, the overall vulnerability has gone down due to favorable increase in short-term total shareholder return (“TSR”) and operating performance metrics. Notably, TSR is still a concern for the sector, but underperformance has lessened slightly since the previous quarter’s data was released.

When compared to 1H22, the Real Estate sector witnessed the biggest percentage jump in campaigns initiated, while the Agriculture sector experienced the largest decrease in campaigns, dropping 78% from nine campaigns in 1H22 to only two in 1H23.22 Rising interest rates and increased construction costs have tempered investor expectations for shareholder returns in the Real Estate sector. Commercial real estate in particular has fared poorly, with office vacancy rates creeping to record highs, as companies manage employees’ increasing demands for remote work.23 With more than 67% of all outstanding commercial real estate loans being held by small and midsized domestic banks, industry weakness and heightened loan defaults could further impact regional banks.24

Activist Targets by Sector – Q1 2023 Year-Over-Year Change25

Though total seats won in the United States in 1H23 is down 15.9% compared to 1H22, total seats won in Canada increased a robust 31.6% from 1H22, with seats won by Starboard Value, Legion Partners and K2 & Associates, among others.26 The increase in seats gained up North is not terribly surprising, as we continued to observe heightened activist activity in Canada quarter-over-quarter, likely due to its favorable regulatory environment for shareholders.27,28

Since the implementation of UPC on September 1, 2022, there has been extensive debate about how impactful the rule would be on proxy contests moving forward. After one full proxy cycle, we observed some interesting developments. Anecdotally, we saw more early-stage settlements during the year. While this could be attributed to a number of factors, it appears that companies are more eager to settle with activists quickly to avoid the frustrations of a public, and costly, proxy battle under this new process. As an example, only about 48 hours after Engaged Capital reported a position in the burger chain Shake Shack, Inc. in May, the company quickly added a mutually agreed-upon independent director to its Board.29 While this is only one instance, we also observed quick settlements in other activist situations this year, perhaps suggesting that activists are either using the threat of UPC to their advantage when negotiating a settlement or are being more conservative with their capital in these uncertain economic times.30 In response to UPC, Glass Lewis reported that 685 companies amended advance notice bylaws. The proxy advisor recommended against nine companies this proxy season who implemented the defense mechanism.31 And despite all the anticipation that UPC would make campaigns easier and cheaper to run, thus provoking record numbers of first-time activists, results show it to be a misapprehension.32

One campaign that did go all the way to a vote this season was Carl Icahn’s crusade against life sciences company Illumina, Inc., which manufactures tools and systems used in gene research. This campaign ended in the removal the company’s Chairman, as well as the installation of one of Mr. Icahn’s nominees.33 This victory came at an opportunistic time for Mr. Icahn; only weeks before Illumina’s annual meeting, Hindenburg Research issued a short report on Icahn Enterprises, accusing the company of operating a “Ponzi-like” structure to pay dividends.34 This situation has unveiled a rare moment of weakness for the formidable investor, as Icahn Enterprises recently cut its dividend in half, and its stock is down 53.9% year-to-date.35 This is another example demonstrating that activists themselves are not immune to shareholder activism, a topic we explored in our September 2022 Activism Vulnerability Report.

Screener Results

In stark contrast to what we witnessed last quarter, where no industries moved 10 or more spots in our rankings, we saw substantial changes in 2Q23; six industries moved 10 or more spots. The most vulnerable industry in 1Q23 had been the Savings Banks industry, which fell 19 spots from last quarter as fundamental concerns eased despite further interest rate increases.

The Utilities industry climbed 13 spots to the top of the list as the most vulnerable industry to activism. Utilities historically have been viewed as a relatively stable equity investment. However, rising fuel costs, supply chain problems and rising inflation and interest rates have challenged the Utilities industry this year, with the S&P 500 Utilities Sector ETF underperforming the S&P 500 by 28.8% year-to-date.36 Utilities’ dividends are struggling to compete with higher U.S. Treasury yields at the same time as the industry has tried to manage rising costs along with growing demand for innovation in renewables and distributed energy.37

Two notable situations in the Utilities industry this year include Starboard’s campaign against Algonquin Power & Utilities Corp. and Elliott’s campaign against NRG Energy Inc. Starboard sent a letter to Algonquin’s Board urging it to divest its renewable assets to reduce debt and improve earnings.38 Following this letter, CEO Arun Banskota resigned and the company indicated that it was considering a sale of its renewable energy unit.39 Elliott issued a public letter that called for a new CEO at NRG, as well as for a potential sale of the home security business, Vivint, that NRG purchased earlier in the year.40

The Life Sciences, Pharmaceuticals and Healthcare Services industries each climbed up the rankings in vulnerability, increasing 12 spots, four spots and three spots, respectively, in 2Q23. As older adults have begun to catch up on elective surgeries that were delayed during the COVID-19 pandemic, health insurers that once benefitted from this delay have witnessed their stocks tumble.41 The Health Care Select Sector SPDR Fund is down 1.7% year-to-date, compared to the broader S&P 500 performance of 17.6%.42 In one healthcare campaign during the year, AREX Capital Management urged Enhabit, Inc., a home health and hospice company, to consider exploring a sale and refreshing its board with its two director candidates.43 Another situation involved Elliott Management buying shares at Catalent, Inc., which manufactures pharmaceuticals, and pushing for changes to the company’s Board.44 Corvex Management and Sachem Head Capital Management, two other well-known activists, disclosed having bought Catalent in 2Q23 before Elliott’s stake became public in July.45

Endnotes:

1: Harriet Torry, Anthony DeBarros, “Economists Are Cutting Back Their Recession Expectations,” The Wall Street Journal, (July 15, 2023)

2: Katherine Doherty, “Bank of America Reversed Recession Call on Strong Jobs and Spending, CEO Says,” Bloomberg, (August 3, 2023)

3: Jeff Cox, “JPMorgan backs off recession call even with ‘very elevated’ risks,” CNBC, (August 4, 2023)

4: Ibid.

5: FTI Consulting analysis. Data provided by FactSet as of September 1, 2023.

6: Lauren Aratani, “Federal Reserve officials announce pause in US interest-rate hikes,” The Guardian, (June 14, 2023)

7: Jeff Cox, “Fed approves hike that takes interest rates to highest level in more than 22 years,” CNBC, (July 26, 2023)

8: Ibid.

9: FTI Consulting analysis. Data provided by FactSet as of September 1, 2023.

10: Dani Romero, “Housing activity in July withered to slowest pace since 2010,” Yahoo! Finance, (August 22, 2023)

11: Ben Foldy, “Car Prices Might Be Unsustainable for Buyers,” The Wall Street Journal, (August 21, 2023)

12: FTI Consulting analysis. Data provided by FactSet as of September 1, 2023.

13: “Global M&A by the Numbers: Q2 2023,” S&P Global Market Intelligence, (August 11, 2023)

14: Ibid

15: Ibid

16: FTI Consulting analysis of activist campaigns. Data provided by Diligent as of June 30, 2023

17: Ibid

18: Ibid

19: FTI Consulting analysis. Data provided by FactSet as of September 1, 2023.

20: Hugh Son, “Fitch warns it may be forced to downgrade dozens of banks, including JPMorgan Chase,” CNBC, (August 15, 2023)

21: Jeff Cox, “Regional banks slide after Fed’s Kashkari advocates ‘significantly further’ capital regulation,” CNBC, (August 15, 2023)

22: FTI Consulting analysis of activist campaigns. Data provided by Diligent as of June 30, 2023.

23: Evelyn Jozsa, “U.S. Office Sales Total $14.8B Halfway Through 2023,” CommercialEdge, (July 19, 2023)

24: Emily Peck, “Small bank struggles could hit the real estate market hard,” Axios, (March 21, 2023)

25: FTI Consulting analysis of activist campaigns. Data provided by Diligent as of June 30, 2023.

26: “Shareholder Activism in H1 2023,” Diligent.

27: Jameson Berkow, “Activists advancing: Why boardroom battles are accelerating across Canada,” The Globe and Mail, (April 24, 2023),

28: Alex Moore, Jennifer Crawford, “A general introduction to shareholder rights an activism in Canada,” Lexology, (August 21, 2023),

29: Crystal Tse, “Activist Fights Tick Up, Along With Settlements,” Bloomberg, (July 10, 2023)

30: Bruce Goldfarb, “Shareholder Activists Should Be Careful About Quick Settlements,” Forbes, (May 15, 2023)

31: “US 2023 Proxy Season Briefing,” Glass Lewis, (2023)

32: FTI Consulting analysis of activist campaigns. Data provided by Diligent as of June 30, 2023.

33: Annika Kim Constantino, “Illumina shareholders oust board chair, CEO survives Carl Icahn proxy battle,” CNBC, (May 25, 2023)

34: Niket Nishant, “Carl Icahn’s firm cuts dividends in half after short-seller attack, shares slump,” Reuters, (August 4, 2023)

35: FTI Consulting analysis. Data provided by FactSet as of September 1, 2023.

36: FTI Consulting analysis. Data provided by FactSet as of September 1, 2023.

37: Matt Phillips, “Chart: Utilities stocks are the worst place to be in 2023,” Axios, (August 22, 2023)

38: “Hedge fund Starboard urges Algonquin Power to sell renewable assets,” Reuters, (July 6, 2023)

39: Tanay Dhumal, “Canada’s Algonquin mulls sale of renewable energy unit,” CEO exits, Reuters, (August 10, 2023)

40: Sourasis Bose, “Activist investor Elliott calls for new CEO at NRG Energy,” Reuters, (June 27, 2023)

41: Annika Kim Constantino, “Health insurance stocks slide after UnitedHealth warns more surgeries will drive up medical costs,” CNBC, (June 14, 2023)

42: FTI Consulting analysis. Data provided by FactSet as of September 1, 2023.

43: “AREX Capital Issues Letter to Board of Directors of Enhabit, Inc.,” GlobeNewswire, (June 13, 2023)

44: Svea Herbst-Bayliss, “Catalent, facing pressure from Elliott, had other activists in stock,” Reuters, (August 14, 2023)

45: Ibid.