Print

PrintSzu Ho is a Principal, Ira Kay is a Managing Partner, and Joadi Oglesby is a Consultant at Pay Governance LLC. This post is based on their Pay Governance memorandum.

Introduction

Thousands of companies, including more than 70% of the S&P 500 companies, grant performance stock units (PSUs) with relative total shareholder return (TSR) or stock price performance-vesting conditions. These incentives can be very motivational, help align management rewards with shareholder returns, and are strongly favored by some investors and proxy advisors. Nevertheless, differing perspectives on the value of these awards, affecting the sizing of grants, may impact the motivational power of these grants.

Companies granting relative TSR-PSUs are faced with the dilemma of how to determine the number of shares being granted. This question comes up often as compensation committees and/or management wonder if the grant date value being delivered is aligned with the intended grant value. Choosing market stock price (either as of the grant date or average toward the grant date) or a Monte Carlo valuation to determine the number of shares being granted can be more complex than one would think, given each calibration approach typically results in a different number of shares. This Viewpoint is intended to help inform companies of the various trade-offs, and it can be used as a general guide to help companies decide which approach makes the most sense for their circumstances.

The Case for Relative TSR Plans

The increasing prevalence of relative TSR performance metrics in performance-based equity awards is driven by multiple factors, with a principal factor being the preferences of major institutional investors and proxy advisors when evaluating alignment between executive pay and performance. For example, Vanguard considers a company’s “three-year total shareholder return and realized pay over the same period vs. a relevant set of peer companies” for evidence of pay and performance alignment. [1] Both Institutional Shareholder Services (ISS) and Glass Lewis use various relative financial and/or TSR performance metrics in their pay-for-performance evaluations to support their recommendations to companies’ say-on-pay proposals. In this context, many companies perceive TSR awards as a means to simultaneously align their compensation with an investors’ perspective on performance and conform to known pay-for-performance evaluation frameworks. Further, the introduction of TSR awards has also become a common action taken in response to unfavorable say-on-pay results.

From the Board’s perspective, TSR plans can create strong alignment with shareholder interests while mitigating challenges with setting multi-year financial or operational goals (particularly within volatile industry sectors) or achieving “apples-to-apples” relative performance comparisons among peers arising from differences in the timing and comparability of reporting.

These factors have contributed to making relative TSR the most prevalent relative performance metric companies use to determine PSU award payouts. TSR is often used as a standalone weighted performance metric but may also be used as a payout modifier. Most often, the subject company’s TSR performance is compared to constituents of a general stock index (e.g., S&P 500), an industry specific stock index, or a custom TSR performance peer group selected by the company.

Valuation and Disclosure of TSR and Other Market-Conditioned Awards

Central to the question of the calibration and motivational effect of TSR awards is their valuation. These valuations — and ultimately the proxy-reported values of these awards — are dictated by accounting guidance, which treats awards subject to market conditions (e.g., TSR, stock price) fundamentally differently from those tied to absolute financial and operational metrics.

For restricted shares, or performance shares subject to financial or operational metrics, the valuation of these awards is generally equal to the stock price on the grant date. Other aspects of the design, including the performance measurement period and minimum/maximum award payout opportunities generally have no bearing on the valuation of the award. Assuming a $10 stock price, in this case all awards and plan variations are valued equally. If you make the goal harder/easier: $10. If you increase/decrease the payout opportunity: $10. If you shorten/lengthen the performance period: $10. As a result, there is little friction when revising incentive designs or shifting between restricted stock and PSUs.

By comparison, the valuation of awards subject to market conditions must consider the effect of those conditions when determining the award value for accounting/disclosure purposes, which is often accomplished using a Monte Carlo valuation methodology. In contrast with financial/operational PSU awards which are valued based on the grant date stock price, market-conditioned awards are valued based on their expected payout value. This results in valuations which are often higher than the stock price on the date of grant (e.g., $12 valuation relative to $10 grant date stock price).[2] Importantly, as plan provisions change, so may the valuation. If you make the goal easier or increase the payout opportunity, the valuation may increase (e.g., $13). Conversely, if you make the goals harder, or reduce the payout opportunities, the valuation may decrease (e.g., $11). This can significantly impact the proxy-reported value of these awards and may significantly change the motivational impact of awards when transitioning to/from market-conditioned awards.

Further, proxy advisors ISS and Glass Lewis both use grant date stock price for performance-based full-value stock awards (i.e., PSUs or performance stock awards). When measuring compensation and conducting quantitative pay-for-performance assessments:

- ISS values all performance-based awards using the grant date stock price and the target payout opportunity . This results in parity between the valuation of PSUs with financial/operational metrics and market-based metrics (e.g., TSR). Under this framework, this may result in lower valuations for TSR awards than is reported by companies in their proxy statements. [3]

- Glass Lewis uses the same approach as ISS when valuing performance-based stock awards. [4] In addition, Glass Lewis considers a measure of realized pay in their evaluations, which emphasizes the value of awards when earned rather than when granted (as is generally reflected in the proxy).

Tradeoffs When Calibrating Awards

Relative TSR PSUs are often granted to top executives, with a pre-determined $ target or intended $ grant value. Given differing views on the “value” of TSR awards, companies often debate the proper method to deliver as they seek to balance the views of award recipients with disclosure requirements and investor perspectives.

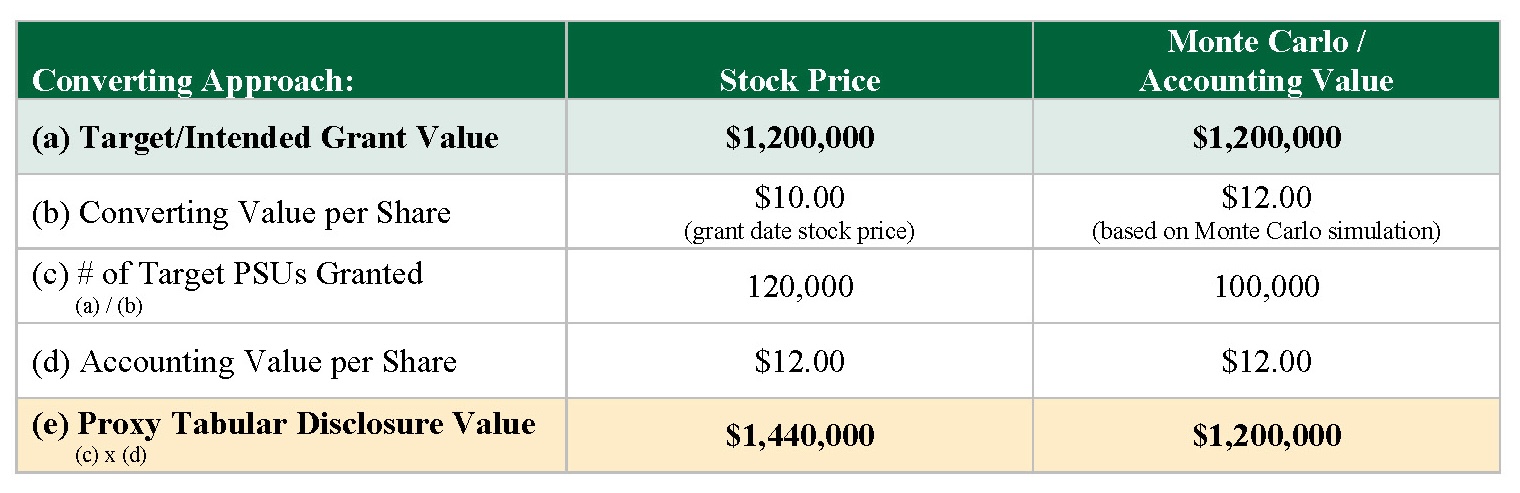

Our experience and research suggest market practice is roughly evenly split between those which convert target grant values to a number of PSU using either (i) the stock price approach or (ii) the accounting / Monte Carlo approach. The following exhibit illustrates the financial differences between these two approaches.

Exhibit I: Relative TSR PSU Conversion Illustrative Example

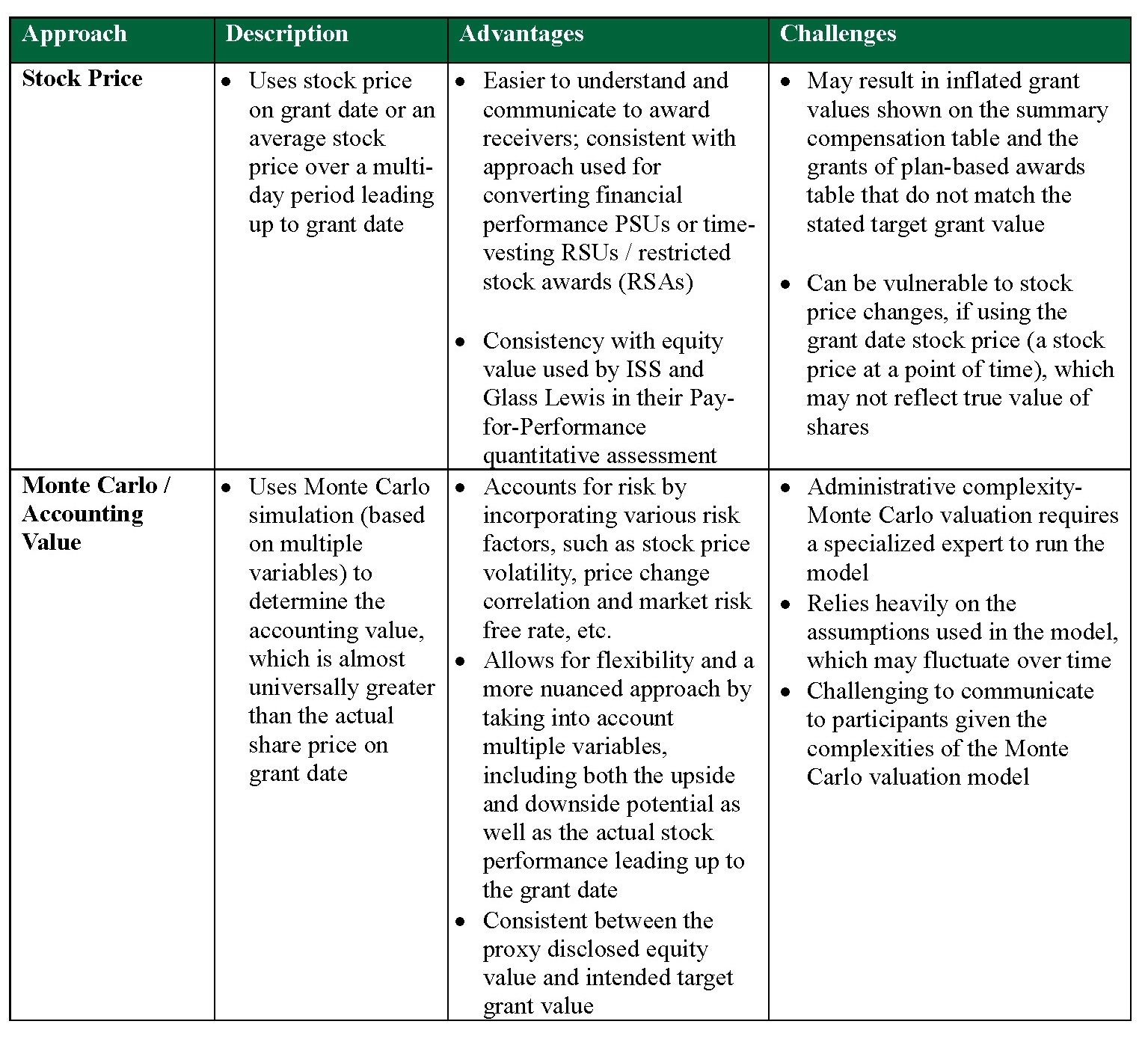

There are advantages and challenges in using each granting approach which should be considered based on each Company’s priorities, valuation objectives, and resources available. Below we summarize several of these key advantages and challenges.

Exhibit II: Relative TSR Awards Granting Approach Comparison Summary

Given the advantages and challenges of each granting approach, there is no singular or correct method. For companies that currently grant relative TSR PSUs, there may not be a compelling reason for change in the near term.

For companies considering adding relative TSR as a PSU performance metric, management and compensation committees should decide which conversion approach best suits the objectives of the Company.

For example, if a company emphasizes communication and value perception with PSU to participants, the stock price approach may be the preferred choice. This most likely will result in a higher proxy-reported value for the award than the value that may have been communicated to the participant as their intended target opportunity.

In contrast, if a company emphasizes consistency between the intended target opportunity and its accounting and proxy reported values, the Monte Carlo approach may be the preferred choice.

1From 2024 Vanguard Proxy Voting Policy for U.S. Portfolio Companies.(go back)

2Similarly, option valuation relies on expected payout value. For example, an option with the exercise price set at the current market price would have $0 intrinsic value at grant but still have a positive grant date value based on expected value in the future.(go back)

3For stock options, ISS also has a different approach than what most companies use to value their options. ISS uses a full-life / term approach and price volatility within a shorter period of time compared to an expected life approach and price volatility over a longer period adopted by most companies when calculating option value. This often results in a higher option value than what is reported by companies in proxy statements.(go back)

4Glass Lewis typically uses company disclosed values for options / stock appreciation rights, which differs from the ISS approach stated above.(go back)