Print

PrintVictoria Tellez is the Research Director at FCLTGlobal and Jonathan Ponder is the Vice President of Research & Development at MSCI Institute. This post is based on their FCLTGlobal memorandum.

Executive Summary

Boards with higher and more durable equity ownership are associated with stronger long-term shareholder returns, risk-adjusted returns (alpha), and differences in investment behavior, specifically higher R&D intensity based on FCLTGlobal analysis, in collaboration with MSCI Institute and leveraging data from MSCI Solutions, of 2,137 companies in the MSCI All Country World Index (ACWI) from 2020 to 2025.[a]

A sustained five percent average annual increase in independent director equity ownership over a five-year period is associated with:

- Total shareholder return (TSR): 35–40 percentage points higher cumulative 5-year TSR. Annually, a 1 percent increase in equity ownership led to ~8 percent increase in TSR.

- Risk-adjusted returns (alpha): Approximately 50 percentage points higher cumulative 5-year excess returns relative to a locally relevant equity market benchmark. Annually, a 1 percent increase in equity ownership led to an ~11 percent increase in alpha.

- R&D intensity: Roughly 3 percent higher aggregate R&D spend relative to revenue.

- Volatility: When independent directors held more equity than executives over a 5-year period, volatility was reduced by an average of 50.9 percent.

These relationships are particularly pronounced for independent directors and where board ownership is meaningful relative to executive ownership. The inverse was also found to be true. Directionality tests indicated that reduced director holdings across a five-year period correlated with a decrease in TSR and risk-adjusted returns.

For companies where independent directors decreased their holdings across the five-year period:

- TSR was reduced by an average of 9.7 percent.

- Risk-adjusted returns were reduced by 11 percent.

These findings reinforce a simple but often underappreciated insight: alongside other incentives, ownership can also play a meaningful role in shaping board behavior. When directors have a stake in long-term outcomes, boards appear better positioned to support durable strategy, disciplined capital allocation, and sustained investment.

Yet despite this evidence, board ownership remains uneven across public markets and is often designed in ways that limit its effectiveness. Short-term pressures, governance norms, independence concerns, and symbolic ownership practices frequently prevent boards from realizing the potential benefits suggested by the data.

This paper examines what the evidence shows about board equity ownership and long-term outcomes, why ownership is unevenly adopted, and how boards and investors can design ownership structures that reinforce a long-term ownership mindset.

| FCLTGlobal’s Research on Long-term Governance and Incentives

This study builds on FCLTGlobal’s research on long-term alignment between boards, executives, and investors. CEO Shareholder: Straightforward Rewards for Long-term Performance Explores how equity ownership and extended holding periods can strengthen accountability and long-term value creation at the executive level. The Board Playbook: Winning Strategies for Long-Term Value Creation Outlines practical steps boards can take to Together, these publications establish the foundation for this paper, extending the ownership lens from management to directors and examining how board equity can anchor long-term decision-making. |

Board Ownership Adds Long-Term Value

This joint analysis by FCLTGlobal and MSCI Institute finds that board equity ownership is associated with long-term value creation across global public markets. Companies in which directors hold higher and more durable equity stakes exhibit stronger long-term outcomes across several dimensions that matter to investors, boards, and other stakeholders.

Higher board ownership is associated with stronger five-year shareholder returns, improved risk-adjusted performance, lower volatility, and greater investment in innovation. These relationships are most pronounced where ownership is sustained over time, held by independent directors, and meaningful relative to executive ownership.

Taken together, these findings suggest that board ownership can shape board behavior and decision-making over long horizons.

| What Does “Meaningful” Equity Ownership Mean?

Throughout this paper, “meaningful” ownership refers to equity exposure that is:

|

What the Analysis Shows

The analysis evaluates the relationship between board equity ownership and long-term outcomes across a broad universe of global public companies. The results indicate that:

- Durable board equity ownership is linked to significantly stronger long-term returns. Companies in which director ownership increases and is sustained over time deliver approximately 35-40 percentage points higher TSR and 50 percentage points higher cumulative 5-year risk-adjusted returns. These relationships persist even after controlling for sector, geography, firm size, and ownership structure.

- Declines in director ownership are associated with weaker long-term performance. TSR declined by an average of 9.7 percent, and alpha were reduced by 11 percent for companies where independent directors decreased their holdings across the 5-year period. Boards in which director ownership falls over time tend to show weaker subsequent outcomes, suggesting that sustained ownership, rather than one-time grants or static holdings, is more closely linked to long-term performance.

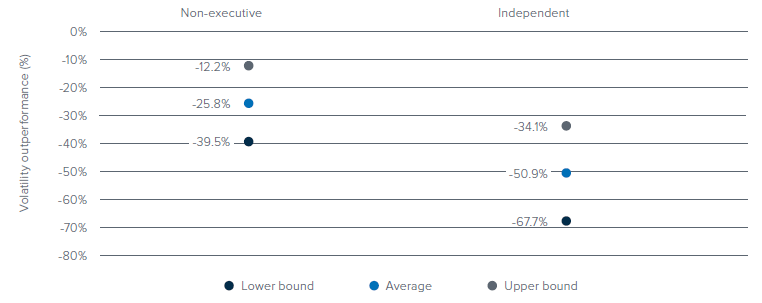

- Greater director ownership relative to executives is associated with lower volatility. Volatility was reduced by 50.9 percent on average when independent directors held more equity than

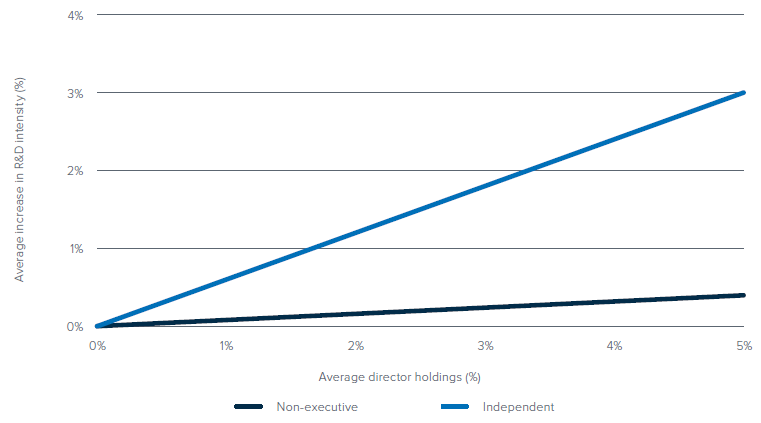

executives during a 5-year period. The strongest relationships appear when directors, particularly independent directors, hold meaningful equity stakes relative to executives, indicating that balanced ownership may strengthen the board’s capacity for effective oversight. - Higher independent director ownership is associated with greater investment in innovation. A sustained 5 percent increase in independent director equity ownership is associated with ~3 percent more aggregate R&D spend relative to revenue. This pattern suggests that board ownership may influence corporate behavior and long-term investment decisions, not only financial returns.

Director Definitions, Explained

|

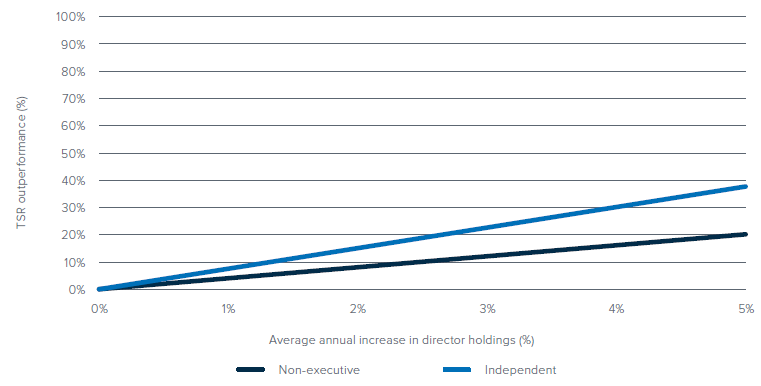

Figure 1a: Companies with increasing director equity holdings outperformed on 5-year TSR

Data as of November 4, 2025. 5-year TSR analysis is based on a universe of 2,137 companies that were continuous constituents of the MSCI ACWI Index between 2020 and 2025. Full variable definitions and model specifications are provided in Appendix 1. Outperformance factor was approximately 4.1% and 7.6% per 1% average annual increase in holdings for non-executive and independent directors, respectively. Holdings growth chart capped by the maximum 5-year average growth value observed for independent directors (4.38%). Correlation does not imply causation.

Source: MSCI Sustainability & Climate Research, FactSet.

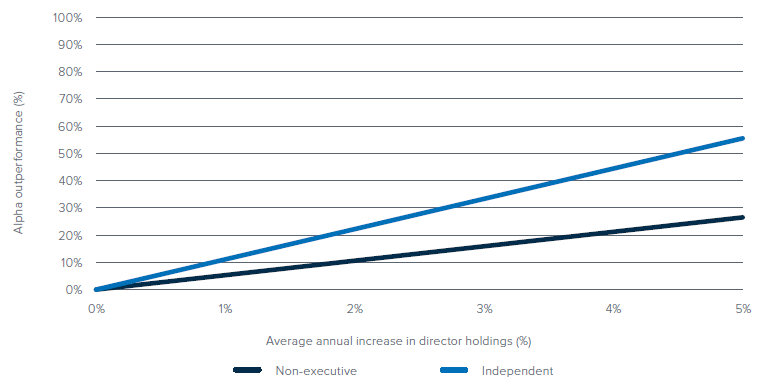

Figure 1b: Companies with increasing director equity holdings outperformed on 5-year risk-adjusted returns

Data as of November 4, 2025. 5-year risk-adjusted returns (alpha) analysis is based on a universe of 2,137 companies that were continuous constituents of the MSCI ACWI Index between 2020 and 2025. Full variable definitions and model specifications are provided in Appendix 1. Outperformance factor was approximately 5.3% and 11.1% per 1% average annual increase in holdings for non-executive and independent directors, respectively. Holdings growth chart capped by the maximum 5-year average growth value observed for independent directors (4.38%). Correlation does not imply causation.

Source: MSCI Sustainability & Climate Research, FactSet.

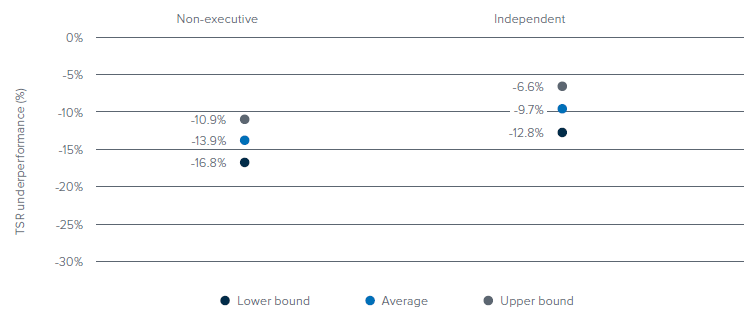

Figure 2a: Companies with decreasing director equity holdings underperformed on average 5-year TSR

Data as of November 4, 2025. 5-year TSR analysis is based on a universe of 2,137 companies that were continuous constituents of the MSCI ACWI

Index between 2020 and 2025. Full variable definitions and model specifications are provided in Appendix 1. The reduced holdings indicator is a

binary factor, whereby the 5-year average percentage change in non-executive and independent director ownership is below 0. Lower and upper

bounds are defined by +/- one standard error (non-executive = 2.99%; independent = 3.06%). Correlation does not imply causation.

Source: MSCI Sustainability & Climate Research, FactSet.

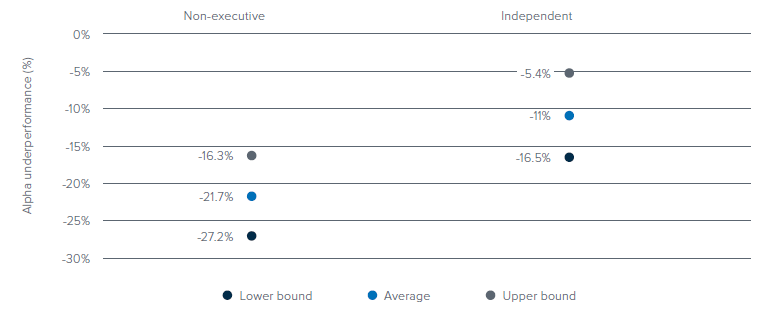

Figure 2b: Companies with decreasing director equity holdings underperformed on average 5-year risk-adjusted returns

Data as of November 4, 2025. 5-year risk-adjusted returns (alpha) analysis is based on a universe of 2,137 companies that were continuous constituents of the MSCI ACWI Index between 2020 and 2025. Full variable definitions and model specifications are provided in Appendix 1. The reduced holdings indicator is a binary factor, whereby the 5-year average percentage change in non-executive and independent director ownership is below 0. Lower and upper bounds are defined by +/- one standard error (non-executive = 5.44%; independent = 5.58%). Correlation does not imply causation.

Source: MSCI Sustainability & Climate Research, FactSet.

Figure 3: Companies where directors hold more equity than executives were less volatile on average over 5 years

Data as of November 4, 2025. 5-year volatility analysis is based on a universe of 2,137 companies that were continuous constituents of the MSCI ACWI Index between 2020 and 2025. Full variable definitions and model specifications are provided in Appendix 1. The relative ownership indicator is a binary variable, where total equity ownership held by directors exceeds that held by executives within the same company. Lower and upper bounds are defined by +/- one standard error (non-executive = 13.62%; independent = 16.83%). Correlation does not imply causation.

Source: MSCI Sustainability & Climate Research, FactSet.

Figure 4: Companies with higher director equity holdings are associated with higher 5-year R&D intensity

Data as of November 4, 2025. 5-year R&D intensity analysis is based on a universe of 2,137 companies that were continuous constituents of the MSCI ACWI Index between 2020 and 2025. Full variable definitions and model specifications are provided in Appendix 1. R&D intensity was found to rise by 0.1%and 0.6% per 1% increase in holdings for non-executive and independent directors across the period, respectively. Holdings chart capped at the 99th percentile of observed average independent director holdings, and for consistency with prior charts. Correlation does not imply causation.

Source: MSCI Sustainability & Climate Research, FactSet.

What the Results Imply

Taken together, the results suggest that board ownership is most closely associated with long-term outcomes when it is sustained over time, rather than granted on a one-off or easily reversible basis. Patterns in the data indicate that increases in board ownership are associated with stronger outcomes over the same five-year period, while declining ownership is associated

with weaker outcomes, underscoring the importance of durability and continued exposure.

The findings also highlight the role of independent directors and the balance of ownership between boards and executives. Performance relationships are strongest where independent directors hold meaningful equity stakes and where board ownership is comparable to or exceeds that of executives. This suggests that ownership may be particularly relevant for board oversight and risk governance.

In addition, the association between independent director ownership and higher investment in innovation points to a potential link between board ownership and corporate behavior. Beyond financial returns, ownership appears to be connected to how boards support long-term investment decisions and strategic posture.

Despite these implications, structured and durable board ownership remains uncommon across public markets. As the next section explores, a combination of short-term pressure, governance norms, incentive design, and investor dynamics has limited the extent to which the evidence on board ownership has translated into practice.

| Independent Directors and Long-Term Outcomes

Independent directors play a central role in oversight, challenge, and long-term strategy. The evidence shows that ownership held by independent directors is particularly associated with stronger long-term performance, lower volatility, and greater investment in innovation. |

Why Evidence has Not Translated into Practice

A long-term orientation is widely recognized as a driver of sustained corporate performance.[1] Prior research shows that companies focused on long-term value creation grew revenue 47 percent faster and earnings 36 percent faster than short-term peers over a 14-year period.[2]

Boards should be natural champions of this long-term perspective: as stewards of strategy, risk, and capital allocation, directors play a central role in shaping how companies balance near-term pressures against long-term value creation.

Yet evidence linking board ownership to long-term outcomes has not translated into consistent practice.

Short-Term Pressure and Boards

Boards operate in an environment shaped by quarterly reporting cycles, activist scrutiny, and market volatility. These pressures can narrow decision horizons, even when boards recognize the importance of long-term orientation.

Boards do not only experience short-term pressure — they can also reinforce it. Survey evidence shows that three in four directors say market demands have compromised their company’s strategic focus, and management teams cite boards themselves as a direct source of short-term pressure.[3] In this context, incentives that provide limited long-term exposure may weaken the board’s ability to counterbalance near-term demands.

Incentive Design and Limited Long-Term Exposure

One key contributing factor may be the limited extent to which director incentives are aligned with long-term performance. Across global markets, independent directors typically receive fixed cash fees and modest equity awards, often with limited or no holding requirements, with the U.S. as a notable exception.[4] In many jurisdictions, relatively low levels of director

compensation also limit the scale of equity ownership that can reasonably be expected, making it difficult for boards to establish stakes that create meaningful financial exposure. While practices vary by jurisdiction, many directors hold only small or easily liquidated stakes, providing limited personal exposure to the long-term consequences of board decisions and

corporate performance.

Global data reflects this pattern. Nearly one-fifth of companies in the MSCI ACWI had zero director ownership, and 94 percent of companies did not have a formal equity ownership policy for directors, underscoring how unevenly adopted long-term board ownership remains across public markets.[5]

Figure 5: Board Incentives and Norms Vary Across Markets[6]

| Country | Approach |

| Brazil | Cash pay dominates; roughly 15% of companies offer variable components such as equity. |

| France | Cash pay dominates; governance codes recommend that directors purchase shares. |

| Germany | Fixed fees are most common; equity grants are rare. |

| Japan | About 12% of large companies award equity to outside directors. |

| Sweden | A mix of cash and equity, with strong encouragement for directors to purchase shares. |

| United Kingdom | Mostly fixed fees; around 29% of listed companies use equity pay, often at symbolic levels; recent changes underway. |

| United States | Base (cash) and equity; over 90% of S&P companies grant equity to directors. |

These differences in incentive structures reflect broader governance norms across markets, including varying expectations around director independence and the role of equity ownership in board compensation.

Regulatory and Governance Norms

In many markets, regulatory frameworks and governance codes emphasize director independence and have historically approached equity-based compensation with caution. These norms are well-intentioned, reflecting concerns about conflicts of interest, entrenchment, and the integrity of board oversight.

Recent developments suggest these views are evolving. For example, updated UK guidance clarifies that share-based remuneration for non-executive directors may be appropriate where it supports long-term alignment, provided independence is preserved, and conflicts are carefully managed.[7]

Even so, in practice, these norms can still constrain boards’ ability to adopt ownership structures that provide meaningful long-term exposure. In some jurisdictions, directors who hold significant equity stakes may face heightened scrutiny or risk being reclassified as non-independent, discouraging ownership even where it could strengthen alignment with long-term

value creation. Proxy advisor policies and investor voting guidelines can also reinforce these norms, as boards often seek to avoid governance structures that may trigger negative recommendations or heightened scrutiny during proxy reviews.

Director Risk Appetite and Investor Buy-In

Both personal and external constraints shape board ownership decisions.

From a director’s perspective, equity ownership introduces concentration risk that some directors may be unwilling or unable to bear. From an investor perspective, new or expanded ownership structures may face skepticism, particularly where proxy advisor policies or voting guidelines prioritize formal independence over long-term exposure.[8]

Without clear investor buy-in and shared understanding, boards may default to familiar incentive structures, even where evidence suggests that alternative ownership designs could better support long-term outcomes.

How Board Ownership Can Align with Long-Term Value Creation

The evidence shows that board ownership is associated with long-term value creation. It also shows why ownership, in practice, has often failed to deliver that alignment. Ownership does not work automatically. Its impact depends on how it is designed, sustained, and understood within the broader governance system. This section examines how board ownership can align with long-term value creation by identifying common pitfalls and the conditions under which ownership reinforces, rather than undermines, effective board oversight.

Common Pitfalls of Board Ownership

Drawing on the empirical analysis in this study, complemented by interviews with subject matter experts, discussions with FCLTGlobal members, and insights from practitioner forums, two pitfalls consistently emerge as the most consequential:

- Symbolic ownership

- Insufficient duration of exposure

The most common pitfall is symbolic ownership. Directors may receive equity, but hold stakes that are too small, too liquid, or too easily reduced to meaningfully influence behavior. In many cases, equity ownership guidelines are calibrated at levels that fail to create material exposure, particularly relative to directors’ overall compensation and responsibilities. When combined with flexible selling provisions, ownership exists largely in form rather than substance, signaling alignment without creating sustained exposure to long-term outcomes. As a result, its ability to shape board deliberations, risk tolerance, or strategic resolve is limited.

Closely related is the issue of duration. Ownership that can be reduced or eliminated once minimum guidelines are met weakens the link between board decisions and long-term consequences. Where directors are free to sell shares after short holding periods, equity exposure may heighten attention to near-term share price movements rather than reinforce long-term performance. Across interviews and practitioner forums, short or easily reversible holding periods emerged as one of the most common reasons board ownership failed to influence behavior in practice.

At the other extreme, overexposure can also distort decision-making. Excessive personal financial concentration may introduce risk aversion, particularly during periods of volatility or strategic transition, when oversight and judgment are most critical. While less frequently observed than symbolic ownership or short duration, this risk underscores the importance of

balance in ownership design.

Taken together, these dynamics help explain why board ownership, despite its association with long-term outcomes, has not consistently translated into durable alignment across public markets. Where ownership is symbolic or short-lived, its governance impact is limited, regardless of intent.

Guardrails That Support Alignment

The same evidence and practitioner insights that highlight the risks of symbolic or short-lived ownership also point to concrete design features that appear more consistent with long-term alignment.

- Meaningful and sustained equity ownership, typically reflected in holding periods of 5 years or more

- Ownership aligned with the full arc of board service, including expectations that extend through tenure and, in some cases, beyond departure

- Meaningful ownership held by independent directors, supporting effective oversight and long-term perspective relative to executive ownership

- Ownership that is broadly understood and accepted by long-term investors, reinforcing good judgment without undermining independence

First, alignment is reinforced when ownership provides meaningful and sustained exposure over time. In practice, this has most often meant holding periods that extend for at least five years, rather than ownership that can be accumulated and unwound over shorter horizons. Longer holding periods strengthen the connection between board decisions and the long-term outcomes those decisions are intended to influence.

Second, alignment is supported when ownership expectations are tied to the full arc of board service. Holding expectations that extend through board tenure, and in some cases for a period following departure, reinforce continuity. Post-departure holding reduces incentives to prioritize short-term outcomes near the end of a director’s term. It helps ensure that decisions

taken late in tenure remain aligned with long-term value creation.

Third, alignment benefits from balance across the governance system. Ownership appears most relevant for oversight when directors — particularly independent directors — hold meaningful stakes relative to executives. This balance supports the board’s ability to challenge management, oversee risk, and maintain a long-term perspective.

Finally, alignment depends on legitimacy and trust. Ownership is more likely to support effective governance when it is broadly understood and accepted by long-term investors and other stakeholders as reinforcing rather than compromising independence. Where ownership is perceived as credible and appropriately bounded, it can strengthen accountability and oversight without raising concerns about conflicts or entrenchment.

Taken together, these guardrails suggest that board ownership aligns with long-term value creation when it is durable in duration, sustained through service, balanced relative to executive ownership, and supported by legitimacy and trust within the governance system.

The table below summarizes common ways in which board ownership can fall short of its intended purpose, alongside design features that appear more consistent with long-term alignment.[b]

Figure 6: Pitfalls and Guardrails in Board Ownership Design

| Instead of… | Consider… | Why it matters |

| Small, symbolic equity stakes with flexible exit provisions | Equity stakes that are meaningful in scale and held for at least 5 years | Meaningful, sustained exposure reinforces long-term and reduces the risk that ownership remains symbolic |

| Equity that can be sold once the minimum ownership guidelines are met | Ownership aligned with the full arc of board service, including expectations that may extend beyond departure | Durability reinforces long-term decision-making and reduces short-term incentives late in tenure |

| Board ownership that is concentrated primarily with executives | Meaningful ownership held by independent directors, relative to executive ownership |

Ownership balance supports effective oversight, challenge, and risk governance |

| Ownership structures that raise independence concerns | Ownership that is appropriately bounded and broadly accepted by long-term investors |

Legitimacy and trust shape whether ownership strengthens governance or creates friction |

Conclusion

Board ownership is associated with stronger long-term outcomes when it is meaningful, sustained, and embedded within effective governance. The evidence suggests that ownership can shape board behavior, not only incentives, when directors share material exposure to the long-term consequences of their decisions. At the same time, ownership remains unevenly adopted and often designed in ways that limit its impact. The frameworks in this paper provide a structured way for boards and investors to examine how equity ownership fits within their governance context and long-term objectives, as a design choice that reflects how boards steward value over time.

The complete publication is available here.

aThroughout this paper, ‘alpha’ or ‘risk-adjusted returns’ refer to excess return compared to a benchmark index (FactSet). FactSet has an alpha value for each company, calculated based on a company-specific index (P_Alpha_Pr) (P_Local_Index).(go back)

bThese distinctions are recurring patterns observed across markets and governance contexts, informed by the empirical findings in this study and reinforced through discussions with subject matter experts, FCLTGlobal member interviews, and practitioner forums.(go back)

1McKinsey Global Institute, Where companies with a long-term view outperform their peers, 2017.(go back)

2FCLTGlobal, McKinsey & Co. Measuring the Economic Impact of Short-Termism, 2017; Rising to the Challenge of Short-Termism, 2016.(go back)

3FCLTGlobal, The Long-Term Habits of a Highly Effective Corporate Board, 2019.(go back)

4WTW. The non-executive director pay landscape in Japan, the U.S., and Europe, 2025.(go back)

5MSCI Sustainability and Climate Research, 2025.(go back)

6Pay Governance. Trends in S&P 500 Board of Director Compensation, 2024. WTW. The nonexecutive director pay landscape in Japan, the U.S., and Europe, 2024. Forbes Brazil, 2025. AFEP: Corporate Governance Code of Listed Corporations, 2022.(go back)

7White & Case, FRC revises guidance on non-executive directors’ remuneration, 2025.(go back)

8FCLTGlobal, Voting for Value: Reforming Proxy Systems for Lasting Impact, 2025; US Congress, Proxy Advisor Regulation: Recent Litigation, State Law Developments, and Federal Legislation, 2024.(go back)