Print

PrintThe following post comes to us from Katie Galley, senior vice president at Cornerstone Research. This post is based on a Cornerstone Research publication by Ms. Galley, Abe Chernin, Yesim C. Richardson, and Joseph T. Schertler.

This is the fourth in a series of reports that analyzes the characteristics of professional liability lawsuits filed by the Federal Deposit Insurance Corporation (FDIC) against directors and officers of failed financial institutions. Lawsuits may also be filed by the FDIC against other related parties, such as accounting firms, law firms, appraisal firms, or mortgage brokers, but we generally do not address such lawsuits here.

Overview of Litigation Activity

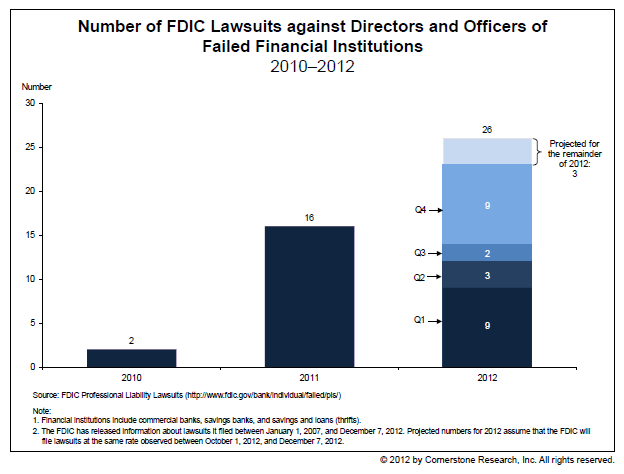

FDIC litigation against directors and officers (D&O) of failed financial institutions has increased markedly in the fourth quarter of 2012, after a lull during the second and third quarters. In October, November, and through December 7, the FDIC filed nine new lawsuits against directors and officers of failed institutions. If additional lawsuits are filed in the last few weeks of December, the number of filings in the fourth quarter will be higher than in the first quarter, when nine lawsuits were filed. Twenty-three lawsuits have been filed to date in 2012. If the recent pace of new filings persists for the balance of 2012, we expect 26 lawsuits will be filed by the end of the year. This reflects an increased level of filing activity compared with 16 in 2011 and two in 2010. In total, 41 lawsuits have been filed since 2010 against the directors and officers of 40 institutions (two separate lawsuits have been filed against various IndyMac directors and officers).

Damages Verdict of $169 Million against Three Former Officers of IndyMac Bank

On December 7, 2012, a jury in federal court in Los Angeles found three former officers of IndyMac Bank (IndyMac) liable for $169 million in damages in connection with 23 loans. This was the first D&O lawsuit filed by the FDIC after the 2008 financial crisis and the first case to go to trial. The case was brought against four former officers of IndyMac. At the time of trial, only three remained in the case. The fourth settled with the FDIC earlier in the year for $4.75 million (to be paid by D&O insurance). Trial began on November 6, 2012, and included 16 days of testimony, concluding on December 6.

IndyMac was seized in July 2008 and the lawsuit was filed two years later in July 2010. The FDIC’s most recent estimate of the cost of IndyMac’s failure was $13.0 billion, the highest among the 467 banks that have failed since 2007.

The FDIC’s damages claim stemmed from acquisition, development, and construction lending by the bank’s Homebuilder Division (HBD). The named defendants were all key HBD managers. The FDIC alleged “two significant departures from safety and soundness”: (1) HBD management ignored credit policies, in part because of compensation plans that rewarded loan volume rather than loan quality; and (2) management continued to increase lending volume at a time when a significant market downturn was “imminent” and despite internal warnings coupled with market signals.

In addition to liability issues regarding the prudence of management’s lending decisions and the underwriting of loans, loss causation was a central element of trial testimony. The conditions of, and expectations for, housing markets and the Office of Thrift Supervision’s (OTS’s) examination findings of IndyMac’s operations were discussed at length in testimony and in closing statements.

Counsel representing the FDIC began his closing statements to the jury by comparing the actions of the defendants to blowing a bubble using bubble gum that one knows is “going to pop” on one’s face. Counsel for the defendants responded citing testimony that no one foresaw the housing market crash and nothing like it had occurred since the Great Depression.

FDIC counsel dismissed the relevance of the testimony surrounding the contemporary findings of the OTS in his closing statements: “[W]hy are we talking so much about the OTS? Are they a party? Like IndyMac they’re no longer in existence.” In contrast, defense counsel highlighted the OTS’s findings regarding IndyMac’s loan underwriting, including the following statement from OTS work papers: “Overall, we found the underwriting of the loans to be thorough with detailed analysis of the borrower’s financial capacity, feasibility of the project, and market conditions.” The jury ultimately awarded the FDIC the entire $169 million claimed in damages on the 23 loans in question, indicating that they were not persuaded by defense counsel’s damages arguments.

In July 2011, the FDIC filed a separate lawsuit against IndyMac’s former CEO. The lawsuit claimed $600 million in damages as a result of the CEO’s alleged negligence in preventing losses from a pool of more than $10 billion in residential loans. This case settled on December 14, 2012, with an agreement by the CEO to pay $1 million from his personal funds and for D&O insurance to pay $11 million. The insurers were not parties to the agreement. It is therefore unclear to what extent the FDIC will be successful collecting on the portion to be paid by insurance given numerous other claims to the limited insurance proceeds.

Financial Institution Failures

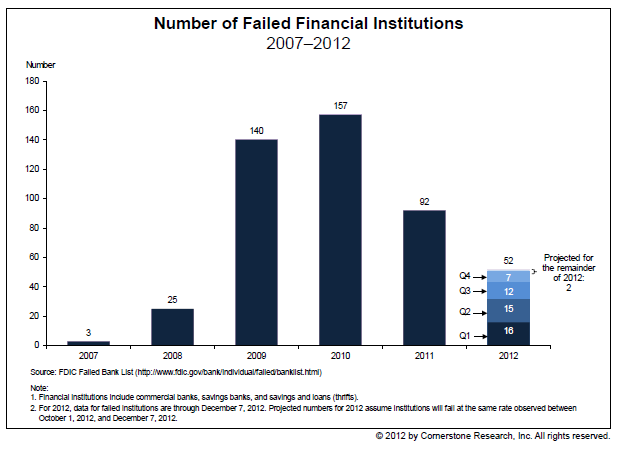

In prior reports, we observed a decline in the seizures of banks and thrifts by the FDIC in 2012 relative to 2011 and 2010 levels. This decline has continued during the second half of 2012. It appears that the pace of seizures has continued to slow in the final quarter of 2012. Thus far, only seven institutions have failed in the fourth quarter. In total 50 institutions have failed in 2012. If the rate of new failures continues during the remainder of the quarter, we expect that 52 institutions will fail in 2012 (fewer than in any year since 2008). Since the beginning of 2007, 467 financial institutions have failed.

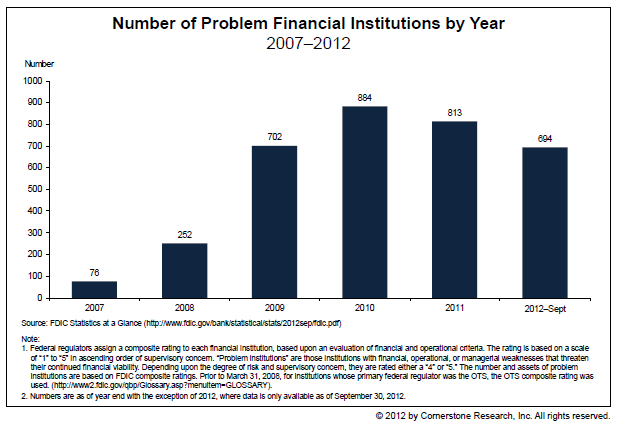

Despite the large decline in the number of failures in 2012 compared with 2009 through 2011, the number of institutions that the FDIC deems “problem institutions” has not declined as quickly. Problem institutions are defined as having weaknesses that threaten the continued viability of the institution. As of the most recent available figures at the end of September 2012, 694 financial institutions were so classified. This reflects a decline from year-end 2010, when 884 were considered problem institutions, but the decline is not as dramatic as the decline in the number of failures. The number of problem institutions has been declining consistently since the first quarter of 2011, when it peaked at 888. However, it still remains high, signifying continued regulatory concern.

Characteristics of Director and Officer Lawsuits

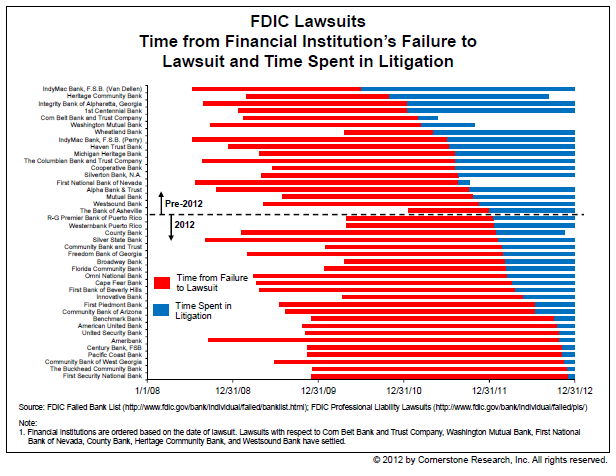

Timing of Lawsuits

Seven of the nine new D&O lawsuits in the current quarter were filed just prior to the expiration of the three-year statute of limitations for tort lawsuits. The FDIC’s lawsuits against the directors and officers of Ameribank and Community Bank of West Georgia were the two exceptions. Tolling agreements presumably allowed the FDIC to take 4.1 years after Ameribank’s failure and 3.4 years after Community Bank of West Georgia’s failure to file cases against the directors and officers of the two banks.

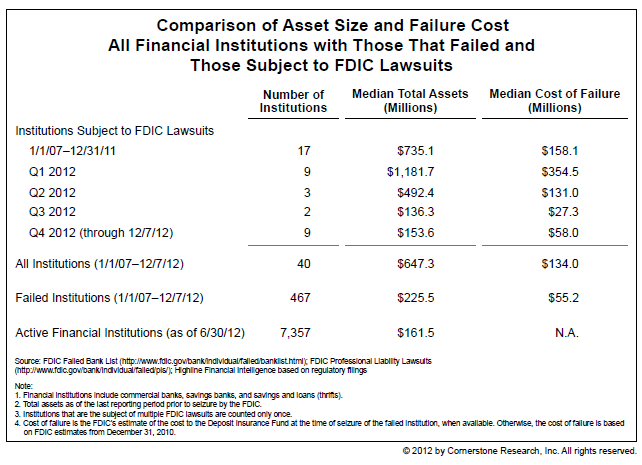

Size of Institutions Subject to Litigation

To date, 9 percent of financial institutions that have failed since 2007 have been the subject of FDIC lawsuits. These lawsuits generally have targeted larger failed institutions and those with a higher estimated cost of failure, although the lawsuits filed in the second half of 2012 have been against smaller and less costly failures. For example, the institutions targeted in the third and fourth quarters of 2012 had median total assets of $136 million and $154 million, respectively. In contrast, the institutions targeted in the first quarter of 2012 had median total assets of $1,182 million.

The 40 institutions that are the subject of D&O lawsuits had a median estimated cost to the FDIC of $134 million at the time of seizure. This compares with the median estimated cost of $55 million for all failed financial institutions. However, consistent with their smaller asset size, the institutions that were subject to the 11 FDIC lawsuits filed to date in the second half of 2012 had a lower median cost of failure than those subject to lawsuits in the first half of the year or prior to 2012.

Defendants and Claims

Defendants named in the 41 filed lawsuits included 324 former directors and officers. The number of cases in which only inside directors and officers were named as defendants increased to 11. Outside directors were named as defendants in addition to inside directors and officers in seven of the nine recent cases filed during the past four months, bringing the total number of such lawsuits since 2010 to 30. CEOs were named as defendants in 36 cases, including seven of the nine most recent cases. Other officers commonly named as defendants included:

- Chief credit officers (15 cases—4 additional cases in the last quarter of 2012)

- Chief loan officers (10 cases—1 additional case in the last quarter of 2012)

- Chief operating officers (8 cases—2 additional cases in the last quarter of 2012)

- Chief financial officers (7 cases—2 additional cases in the last quarter of 2012)

- Chief banking officers (2 cases—no change in the last quarter of 2012)

In addition, the number of lawsuits that named insurance companies as defendants remained at three, and the number of cases that identified a law firm as a defendant remained at one. The number of cases that also named spouses of the directors and officers as defendants remained at three.

All nine recent lawsuits included allegations of negligence and gross negligence, and three included allegations of breach of fiduciary duty. Overall, allegations of negligence, gross negligence, and breach of fiduciary duty were made in 38, 38, and 28 of the 41 lawsuits, respectively.

Regulatory Ratings of Financial Institutions Subject to Director and Officer Lawsuits

In the wake of a financial institution failure that imposes a loss on the FDIC’s Deposit Insurance Fund, the inspector general of the appropriate regulatory agency may conduct a review of the failed institution. Its findings are summarized in a Material Loss Review (MLR). One typical feature of MLRs is a short history of the failed financial institution’s examination ratings, which are otherwise unavailable to the public. The ratings provide an insight into regulators’ contemporary assessments of a financial institution and its management.

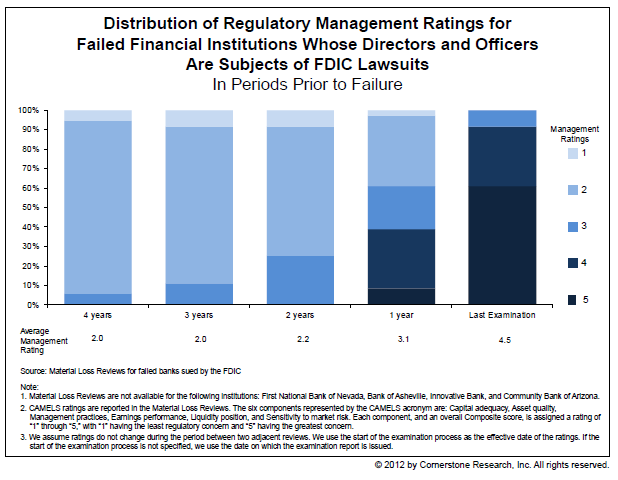

We have identified MLRs for 36 of the 40 institutions that have been subject to FDIC lawsuits and examined the management component of the CAMELS ratings, as well as the composite (i.e., overall) rating, for each institution. The chart below shows the distribution of the management ratings for these institutions in the four years prior to failure. On a scale with “1” as the best rating and “5” as the worst, management ratings generally remained strong (i.e., “1” or “2”) until two years prior to failure.

The average management rating was 2.2 two years prior to failure and no institution had a management rating of “4” or “5.” Seventy-five percent were rated “1” or “2.” Ratings of “1” and “2” were viewed as a favorable assessment of management ability. An Office of the Comptroller of the Currency (OCC) handbook defined a “1” as indicating

strong performance by management and the board of directors and strong risk management practices…. Management and the board have demonstrated the ability to promptly and successfully address existing and potential problems and risks.

A rating of “2” was less positive, but still a favorable assessment of management’s ability. A “2” was defined as indicating

satisfactory management and board performance and risk management practices…. In general, significant risks and problems are effectively identified, measured, monitored, and controlled.

Management ratings started deteriorating substantially between one to two years prior to failure. Sixty-one percent of the institutions had management ratings of “3,” “4,” or “5” one year prior to failure, but 39 percent still retained a “1” or “2” rating.

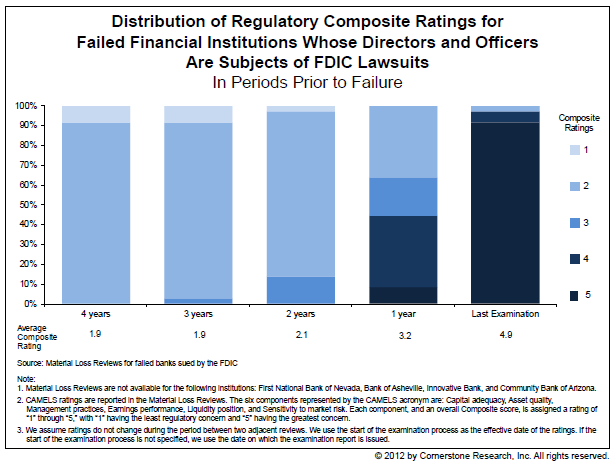

The composite rating that assessed the safety and soundness of these institutions displayed a similar pattern. The following chart shows the distribution of the composite rating for institutions subject to FDIC lawsuits in the four years prior to failure.

As with management ratings, composite ratings generally remained strong until two years prior to failure. The average composite rating was 2.1 two years prior to failure and no institution had a composite rating of a “4” or “5.” According to the OCC handbook, a composite rating of “1” signified that

[f]inancial institutions in this group are sound in every respect…. Any weaknesses are minor and can be handled in a routine manner by the board of directors and management…. These financial institutions are in substantial compliance with laws and regulations. As a result, these financial institutions exhibit the strongest performance and risk management practices relative to the institution’s size, complexity, and risk profile, and give no cause for supervisory concern.

A composite rating of “2” signified that

[f]inancial institutions in this group are fundamentally sound.… Only moderate weaknesses are present and are well within the board of directors’ and management’s capabilities and willingness to correct.… These financial institutions are in substantial compliance with laws and regulations. Overall risk management practices are satisfactory relative to the institution’s size, complexity, and risk profile. There are no material supervisory concerns and, as a result, the supervisory response is informal and limited.

The chart on the previous page shows that 86 percent of the institutions subject to FDIC lawsuits had a “1” or “2” composite rating two years prior to failure. The remaining 14 percent were rated “3.” Not until one to two years prior to failure were any of the institutions rated “4” or “5.” Sixty-four percent were rated “3,” “4,” or “5” one year prior to failure, but 36 percent still had a “2” rating.

In short, weak ratings were not a persistent historical problem for this group of institutions. The decline in ratings occurred near the end of their independent existence.

Other Recent FDIC Litigation Activity

FDIC as Receiver for Colonial Bank v. Auditors

On October 31, 2012, the FDIC, as receiver for Colonial Bank of Montgomery, Alabama (Colonial), brought a lawsuit against PricewaterhouseCoopers (PwC), the bank’s external auditor, and Crowe Horwath (Crowe), which provided internal audit services. This is the first FDIC lawsuit since the 2008 financial crisis targeting the auditors of a failed financial institution. The claims include professional malpractice, gross negligence, breach of contract, and negligent misrepresentation, with claimed damages in excess of $1 billion.

The FDIC alleges that Colonial’s failure in August 2009 was triggered by massive fraud perpetrated against the bank by the bank’s largest mortgage banking customer, Taylor Bean & Whitaker (Taylor Bean). Following the conviction in April 2011 of the ex-chairman of Taylor Bean (which was upheld in June 2012), as well as guilty pleas by other Taylor Bean officials and employees of Colonial complicit in the fraud, PwC and Crowe are now charged with failures to detect fraud and prevent losses suffered by the bank.

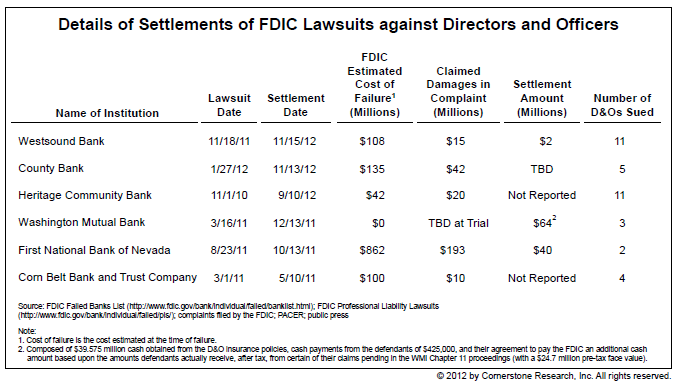

Settlements

Three settlements of D&O lawsuits have been publicly announced in the three months since our previous report. Six lawsuits in total had settled as of November 20, 2012, and two others related to IndyMac were resolved in the intervening weeks. Settlement details are listed below.

Future Director and Officer Lawsuits

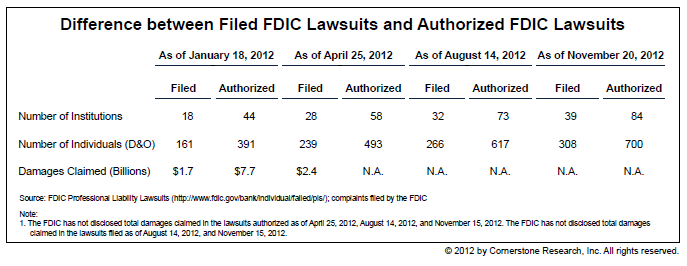

These findings do not include the many negotiations and mediations the FDIC has undertaken with directors and officers of failed institutions, as statistics for these activities are unavailable. The number of lawsuits filed has continued to lag behind the number authorized by the FDIC. As of November 20, 2012, the FDIC had authorized lawsuits against 700 individuals in connection with 84 failed institutions. At that time 308 individuals had been sued in connection with the 39 filed lawsuits, suggesting that as many as 392 former directors and officers were still awaiting a decision on whether the FDIC would file a lawsuit against them. The difference between the number of lawsuits authorized and the number filed increased in 2012. There were 45 cases that the FDIC had authorized but not filed as of November 20, 2012. This backlog of authorized lawsuits, the FDIC’s recent success in the IndyMac trial, and the approaching end of the statute of limitations for making a claim against the numerous institutions that failed in 2009 and 2010 suggest that substantially more FDIC cases may be filed in upcoming months.