The following post comes to us from Katie Galley, senior vice president at Cornerstone Research. This post is based on a Cornerstone Research publication by Ms. Galley, Abe Chernin, Yesim C. Richardson, and Joseph T. Schertler.

This is the fourth in a series of reports that analyzes the characteristics of professional liability lawsuits filed by the Federal Deposit Insurance Corporation (FDIC) against directors and officers of failed financial institutions. Lawsuits may also be filed by the FDIC against other related parties, such as accounting firms, law firms, appraisal firms, or mortgage brokers, but we generally do not address such lawsuits here.

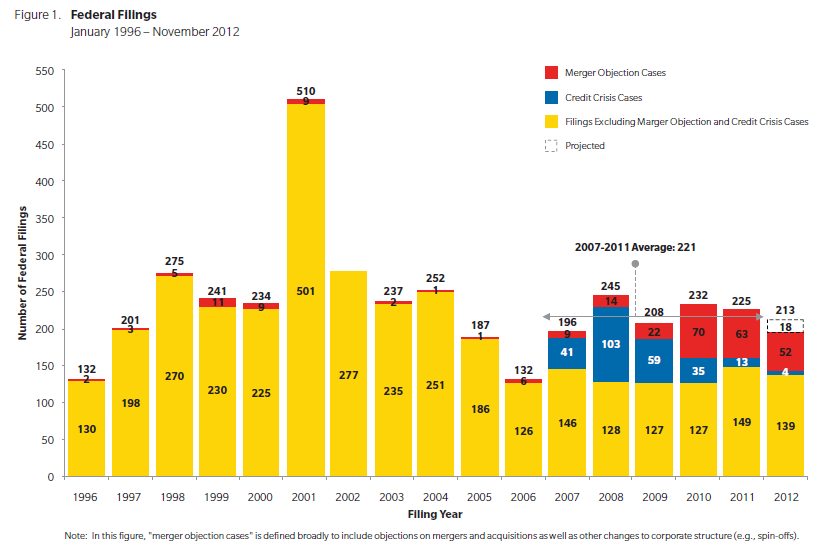

Overview of Litigation Activity

FDIC litigation against directors and officers (D&O) of failed financial institutions has increased markedly in the fourth quarter of 2012, after a lull during the second and third quarters. In October, November, and through December 7, the FDIC filed nine new lawsuits against directors and officers of failed institutions. If additional lawsuits are filed in the last few weeks of December, the number of filings in the fourth quarter will be higher than in the first quarter, when nine lawsuits were filed. Twenty-three lawsuits have been filed to date in 2012. If the recent pace of new filings persists for the balance of 2012, we expect 26 lawsuits will be filed by the end of the year. This reflects an increased level of filing activity compared with 16 in 2011 and two in 2010. In total, 41 lawsuits have been filed since 2010 against the directors and officers of 40 institutions (two separate lawsuits have been filed against various IndyMac directors and officers).