Print

PrintAlyson Clabaugh is a Senior Product Marketing Manager and Rob Peters is a Senior Director at Intelligize, Inc. This post is based on their Intelligize memorandum.

In the process of assembling our inaugural Unicorn IPO Report, we discovered something surprising. We set out to investigate “unicorn” companies, the modern reference to private companies with valuations exceeding $1 billion (our full criteria for what constitutes a unicorn company may be found in the Methodology section of this report). While the number of unicorns has been growing over time, they are named for their scarcity. And they remain rare indeed. As 2019 began, just over 300 of them existed in the world. [1]

There’s no question, then, that these are standout operations. Which is what makes our findings—drawn from data in the Intelligize SEC compliance platform—somewhat counterintuitive. One would expect the technology unicorns, like the unicorns of myth, to be wild and independent creatures. You could say that in resisting the IPO process for so long, many of them have embodied the unicorn’s mythological ability to resist capture or taming. And yet, our examination of unicorns that went public in recent years reveals that to an unexpected degree, these singular corporations demonstrate something of a herd mentality.

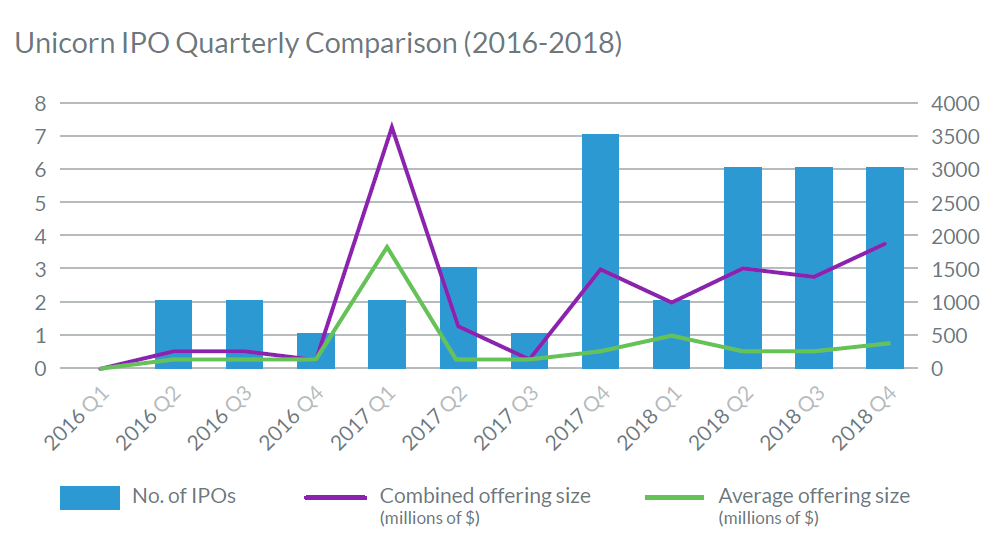

We witness this dynamic most dramatically in the rate at which unicorns have gone public in the last eight quarters. In that period, two IPOs loom large: those of Snapchat parent, Snap, Inc. (in Q1 2017), which was perceived as a major disappointment after a downward slide in its stock, and Dropbox (in Q1 2018), which was well-received by comparison. Snap’s experience scared away fellow unicorns, and in the following three quarters only 12 went public. By contrast, Dropbox’s success drew a crowd. The three quarters following its IPO saw an increase of 50 percent—18— public market debuts. Will we see a continuation of this upward trend through 2019, or will more unicorns elect to remain private? A recent Goldman Sachs report concluded that due in part to the availability of private investment, during the last two years the biggest new public companies would have created more value by staying private.

We can discern the herd mentality in other data points as well. In the following pages, we will see:

- That unicorns almost uniformly go to market more quickly than other companies going through the IPO process;

- That a large number of unicorns lack gender diversity on their boards; and

- That only one of 20 unicorns disclosed executive compensation figures beyond the minimum required by law.

Of course, we should not overstate this phenomenon. Our report also demonstrates diversity of thought among unicorns on decisions like CEO duality (trusting their CEO and chairperson roles to a single individual), and on the choice between issuing single or multiple classes of stock.

There are many additional, different, and perhaps even contrary interpretations of unicorns to be drawn from the data in the following pages. In that way, corporate unicorns may indeed be very much like the mythical beasts: something upon which we all impose our own imaginations.

Unicorn IPO Year-Over-Year Comparison

Without much fanfare, 2018 saw a significant increase in unicorn IPOs compared to 2017. Twenty unicorns went public in 2018, a 54 percent increase over the 13 IPOs in 2017. Since 2016, the number of unicorn IPOs has grown by 300 percent.

Despite seven more unicorn IPOs in 2018 than in 2017, the combined offering size of more than $6 billion in 2017, led by Snap Inc.’s $3.4 billion IPO, still eclipsed the $5.8 billion total offering size of 2018. Likewise, the Snap offering skewed 2017’s average offering size higher, coming in at $462.5 million compared to less than $290 million in 2018.

Looking Back

To provide context for these trends and those illustrated below in “Unicorn IPO Quarterly Comparison (2016-2018)”, it is worth examining the news and events surrounding them. In 2016, more than 70 percent of investors surveyed by Sharepost believed that private tech company valuations would either remain flat or increase over the following 12 months. Many venture capital investors opted for an M&A exit during this timeframe. AppDynamics was just days away from its IPO when it was acquired by Cisco for $3.7 billion. Battery Ventures’s Neeraj Agrawal, estimated that similar cloud technology acquisitions totaled $63 billion in 2016.

Then came the IPO of Snap in March 2017, and its much-heralded decline that saw shares fall by 48 percent over the next six months. The chilling effect of the Snap fiasco caused some unicorns to abandon IPO plans over the next year. For example, eviCore Healthcare reportedly pursued a dual-track exit in May 2017, and perhaps taking its cue from the public market performances of Snap and Blue Apron, opted to find a home with Express Scripts rather than proceed with an IPO.

Unicorn IPO activity rebounded after Dropbox’s well-received IPO in March 2018, with the 18 unicorn public offerings over the following three quarters equaling the total number of IPOs in the previous eight quarters combined.

Looking Forward

Despite the government shutdown in December 2018 and January 2019, which virtually froze operations at the SEC and countless other federal agencies, many industry insiders still predict a strong 2019 IPO market, driven largely by unicorns. While such rosy predictions have proved unfounded in past years, several high-profile companies—Lyft and Slack most prominently—have bolstered market outlooks by filing confidential draft registration statements with the SEC.

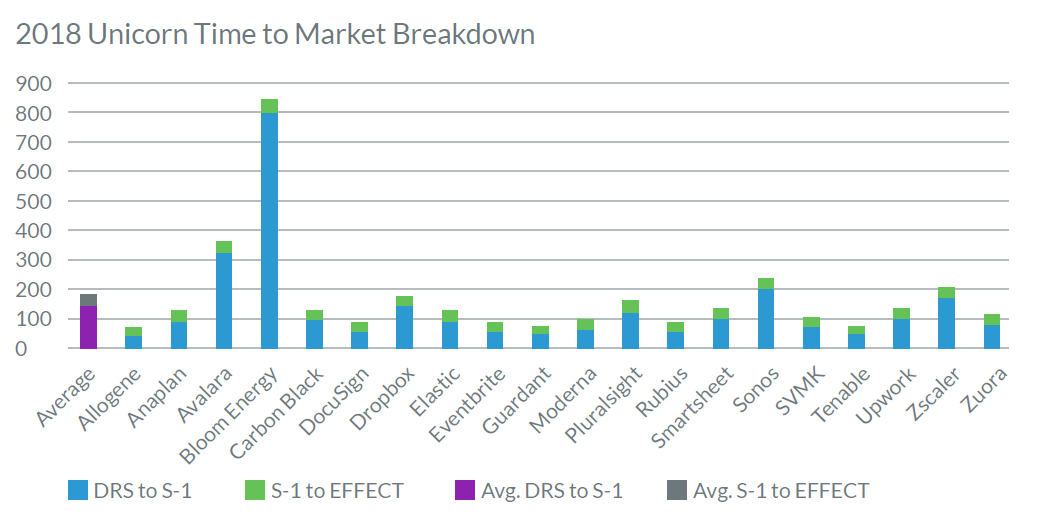

Time to Market

Of the 20 unicorn IPOs in 2018, the average time from draft registration statement (DRS) filing to IPO was 168 days. Even removing the nearly two and a half years between Bloom Energy Corporation’s DRS and IPO (851 days), the average was 132 days, still a surprisingly generous cushion from process start to finish. At the other end of the spectrum, Allogene Inc., a developer of cell therapies for treating cancer, took only 61 days, by far the shortest of any company, filing its DRS on August 10, 2018 and its S-1 on September 14. The SEC filed Allogene’s EFFECT on October 10.

As expected, the majority of time (140 days on average) was spent between the filing of the DRS and S-1, while companies took an average of just 28.15 days from S-1 to EFFECT. For comparison, our data shows that for the broader market, the average time from S-1 to trading for 2018 U.S. IPOs registering common stock was 48.54 days.

There is clearly urgency on the part of unicorns to move to trading as quickly as possible.

As discussed above and illustrated in the “Time to Market Breakdown” chart, Bloom Energy, the developer, manufacturer and installer of solid oxide fuel cell power generators, was an outlier, its 851 days to market more than doubling the time of next highest issuer (Avalara, Inc at 318 days). This uncharacteristically long lag time was certainly eventful, as during that period, Bloom Energy:

- Received 13 SEC comment letters;

- Opted to create a dual-class common stock structure;

- Was forced to address issues from its previous VC funding rounds; and

- Temporarily put its IPO plans on hold after a federal subsidy for alternative energy systems was allowed to expire.

This highlights the need to for companies to consider the eventual effect of politically-motivated tax maneuvers, governance structures, and seed-stage VC rounds on a future IPO.

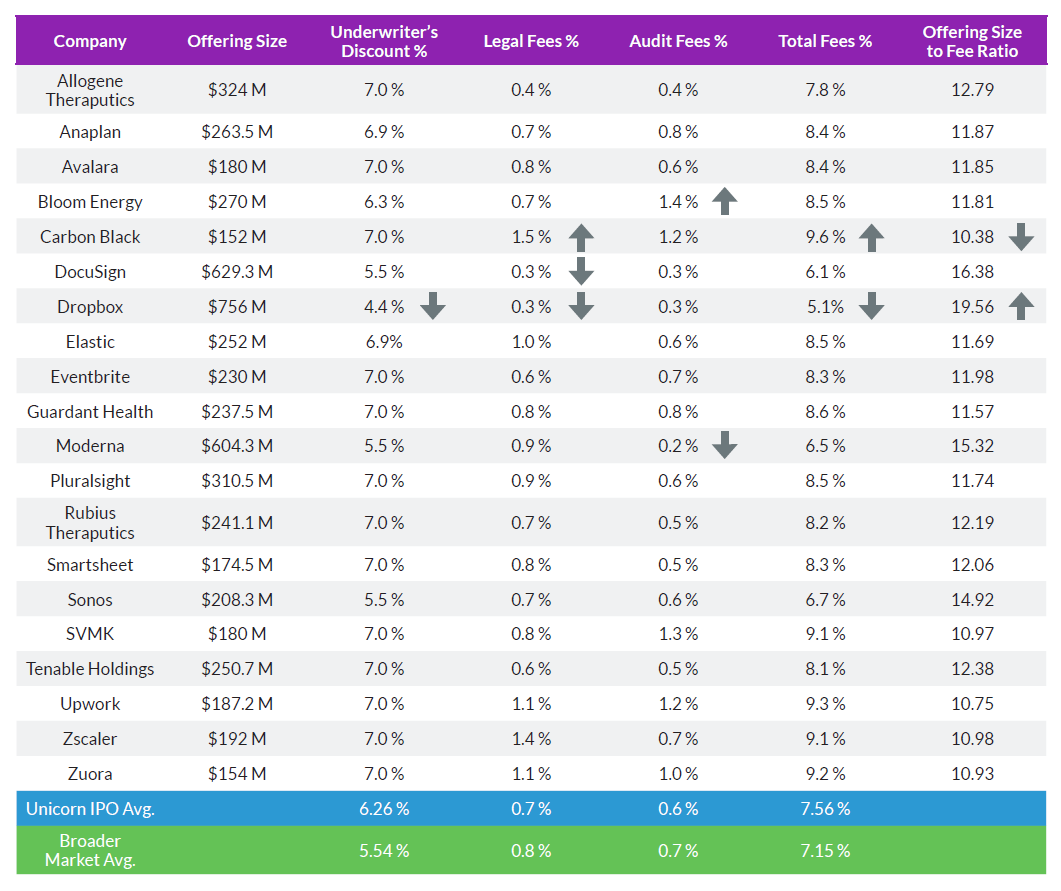

Offering Size-to-Fee Ratio

The average offering size of 2018 unicorn IPOs was $289.4 million, with combined fees for underwriting, legal and audit averaging $21.9 million (7.56%). This put average offering size-to-fee ratio at 13:1. Perhaps not unexpectedly, the largest, highest profile IPOs paid less in fees on average, with Dropbox (20:1), DocuSign (16:1), Moderna (15:1) and Sonos (15:1) leading the way. Those four unicorns had an average offering size of $549.5 million. At the other end of the spectrum, SVMK, Upwork, Zscaler and Zuora all had offering size-to-fee ratios of less than 11:1. Their average offering size was $178.3 million. This stark difference in fee ratio is illustrative of the fierce competition among underwriters, law firms and accounting firms for marquee IPOs.

The average underwriter’s discount among unicorns in 2018 was 6.26%, compared to 5.54% for the broader market, putting unicorns above average in this category. Average legal and audit fees for unicorns trended slightly below the broader market average (0.7% vs. 0.8% for legal and 0.6% vs. 0.7% for audit). This is likely due to the complex nature of unicorn public offerings meriting additional underwriting fees. Legal and auditing teams, on the other hand, typically have long-established relationships with unicorn companies formed during their VC rounds and auditors and attorneys may be looking to preserve longer-term relationships by offering lower IPO fees.

Unicorn Corporate Governance

Unicorn Board Composition

Board composition is already a hot topic in public companies, with Facebook taking public heat last year for a lack of diversity on its board, and California having already enacted law (Cal. Corp. Code §§ 301.3 and 2115.5) mandating that companies incorporated or headquartered in California have women on their boards of directors. All companies must have at least one woman on their board of directors by December 31, 2019. That requirement will increase to at least two female board members for companies with five directors and at least three female board members for companies with six or more directors by December 31, 2021. It is a near certainty that other states will eventually follow suit.

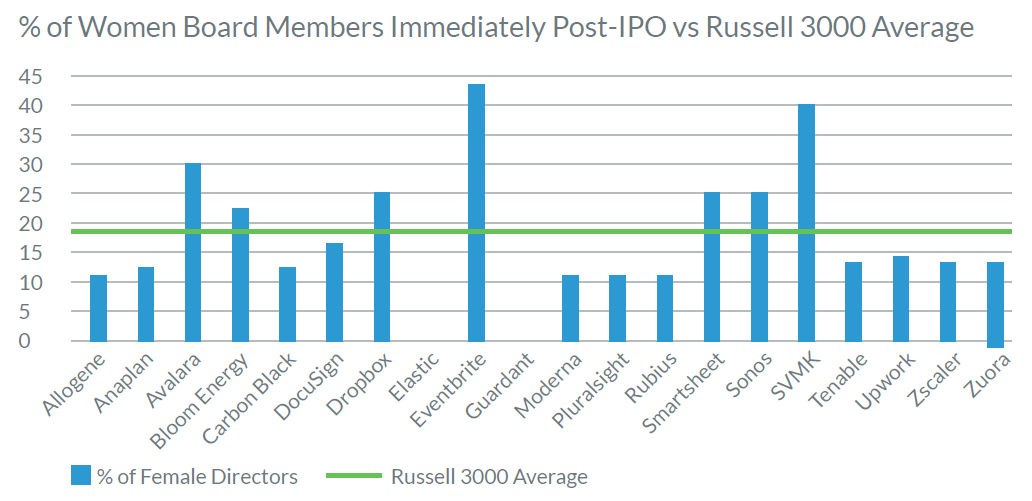

Among the 2018 unicorn IPOs—13 of which are headquartered in California—board gender diversity varied widely immediately after IPO. The boards of Eventbrite and SVMK (the parent of SurveyMonkey) were 44 percent and 40 percent female, respectively. SVMK noted in its IPO prospectus: “Across our board and management team we are proud of the progress we have made with respect to diversity and inclusion, gender equality and providing a path for our people to achieve their full potential. We believe there is a strong correlation between the health of our business and the health of our culture.”

Eventbrite, a ticketing and event platform that helps people find and attend events, was also one of the few unicorns in 2018 to debut on the public markets with a female CEO, Julia Hartz. Hartz, in an interview with TechCrunch last year, said, “The makeup of our board and executive team is the outcome of carefully and thoughtfully cultivating the right group of people based on values, experience and expertise.”

At the opposite end of the spectrum, a surprising number of companies (12 out of 20, or 60 percent) had either one or zero female directors. Guardant Health and Elastic, two companies with zero female directors, are both based in California and will therefore presumably need to make changes soon. No matter their geographic location, activist investors and other shareholders will certainly have much to say about board composition moving forward.

In comparing these statistics to the broader market, the Equilar Gender Diversity Index, shows the percentage of women on Russell 3000 corporate boards at 18 percent as of Q3 2018. Importantly, that was the fourth consecutive quarter in which this percentage increased. That’s the positive news. On the down side, the same report indicates that nearly 17 percent (504) of Russell 3000 boards still lack a female director. This compares to 10 percent (2) of unicorns that went public in 2018.

For unicorn companies going through the IPO process, they must contend not only with board gender composition requirements, but also a host of other board changes that accompany the transition from private to public company. One such issue is that of the classified or “staggered” board of directors.

In 2018, 19 out of 20 unicorns that went public installed a classified board immediately after IPO. By contrast, the tide of opinion is turning toward board declassification in the broader market, where classified boards are no longer considered a corporate governance best practice.

Between management and shareholders in 2018, there were 95 proposals for board declassification (85 management and 10 shareholder), up markedly from the 67 such proposals in 2017 and 76 in 2016, according to a Proxy Insight memorandum.

Among unicorns the only declassified board immediately following IPO was Dropbox, which said that it will elect directors annually until its Class B shareholders lose control of the company:

“Until the outstanding shares of our Class B common stock represent less than a majority of the combined voting power of common stock, we will have a single class of directors who are each elected for one-year terms and until their successors are duly elected and qualified. When the outstanding shares of our Class B common stock represent less than a majority of the combined voting power of common stock, we will have a classified Board of Directors consisting of three classes of approximately equal size, each serving staggered three-year terms. Our directors will be assigned by the then-current Board of Directors to a class.”

Capital Structure

Perhaps unsurprisingly, unicorns that go through the IPO process also often struggle with the idea of ceding company control to shareholders. Issuing multi-class common stock can, of course, restrict voting privileges to company founders, venture capital backers or other early stakeholders, helping those parties maintain additional control over a public company. Snap was one of the most extreme examples of this approach when in 2017, it gave zero voting rights to investors in a $3.4 billion IPO. Among unicorns that went public in 2018, Dropbox was the largest issuer (in terms of offering size) to do this. Pluralsight and Bloom Energy Corp. were also among the 10 largest IPOs, which issued multi-class common stock.

Something of a resistance is beginning to form against the multi-class stock approach, however. S&P Dow Jones Indices and FTSE Russell, for instance, now exclude some dual-class shares, including Snap, meaning that passive funds tracking that index are not obligated to buy its stock—a potentially huge loss.

Unicorns as Emerging Growth Companies

Aside from Dropbox, all other 2018 Unicorn companies that went public classified themselves as “emerging growth companies” (EGC). In 2012, the JOBS Act created a new category of securities issuer, the EGC, that included those with revenues under $1 billion which had either not gone public or just had their IPO.

Dropbox noted in its prospectus that: “We ceased to be an ‘emerging growth company,’ as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, on December 31, 2017. However, because we ceased to be an ‘emerging growth company’ after we confidentially submitted our registration statement related to this offering to the SEC, we will continue to be treated as an “emerging growth company” for certain purposes until the earlier of the date on which we complete this offering or December 31, 2018.”

EGCs are not subject to the same SEC reporting requirements as other public companies. Specifically, Title I provides scaled disclosure provisions for EGCs, including two years of audited financial statements in the Securities Act registration statement for an IPO of common equity securities, the smaller reporting company version of Item 402 of Regulation S-K, and no requirement for Sarbanes-Oxley Act Section 404(b) auditor attestations of internal control over financial reporting. In addition, EGCs need only disclose the compensation of their three top executives (as opposed to four for other public companies) and are not required to disclose pay ratio for their principal named executive officer.

Indeed, all 20 unicorns (Dropbox included) in our analysis took advantage of these EGC benefits, with very few outliers. Allogene Therapeutics had only one named executive officer for which to disclose compensation, while cybersecurity solutions provider Tenable Holdings elected to disclose compensation for its top four named executive officers.

Unicorns and Accounting

Unicorns that issue public offerings also benefit from several accounting-related rules meant to ease their transitions. A relaxation of GAAP compliance, for example, allows unicorns to adopt new GAAP standards on the less-aggressive private company schedule. Underscoring the challenge of the transition, however, half of 2018’s unicorns still received SEC comment letters addressing issues of GAAP compliance.

The story was similar for revenue recognition, which has already offered public company CFOs and CAOs many a sleepless night.

Fifty-five percent of the 2018 unicorn IPOs elected to early adopt the revenue recognition standards. Of those early adopters, 45 percent drew a SEC comment letter about their implementation.

Comparatively, in our November analysis of 32 public companies that adopted the new standards early, we found that nearly one-third had received SEC comment letters questioning their application of the new rules to company revenues.

Methodology

This report is based on information contained in the Intelligize platform as of February 1, 2019.

There is no one universally accepted definition of a “unicorn” company. This means that research produced on the topic is often inconsistent based on the criteria used to classify a unicorn. For the purposes of this report, a Unicorn is defined as a company:

- Valued at $1 billion or greater at the time of IPO

- That is venture-capital backed

- Listing common stock or a class of common stock (not ADRs)

- Listing on the NYSE or NASDAQ, with more than 50 percent of outstanding voting securities held by U.S. residents

- With registration effective from January 1, 2016 through December 31, 2018

The companies included in this analysis with IPOs between 2016-2018 are:

- Moderna, Inc.

- Anaplan, Inc.

- Allogene Therapeutics, Inc.

- Elastic N.V.

- Guardant Health, Inc.

- Upwork Inc.

- SVMK Inc.

- Eventbrite, Inc.

- Sonos, Inc.

- Tenable Holdings, Inc.

- Bloom Energy Corporation

- Rubius Therapeutics, Inc.

- Avalara, Inc.

- Pluralsight, Inc.

- Carbon Black, Inc.

- DocuSign, Inc.

- Smartsheet Inc.

- Zuora, Inc.

- Dropbox, Inc.

- Zscaler, Inc.

- Casa Systems, Inc.

- Denali Therapeutics Inc.

- Stitch Fix, Inc.

- MongoDB, Inc.

- Roku, Inc.

- CarGurus, Inc.

- Switch, Inc.

- Redfin Corporation

- Blue Apron Holdings, Inc.

- Cloudera, Inc.

- Okta, Inc.

- MuleSoft, Inc.

- Snap Inc.

- Coupa Software Incorporated

- Nutanix, Inc.

- Trade Desk, Inc., The

- Twilio Inc.

- NantHealth, Inc.

Endnotes

1https://www.cbinsights.com/research/unicorn-startup-market-map/(go back)