Print

PrintJackie Cook is Director of Manager Research and Jon Hale is head of sustainability research for Morningstar, Inc. This post is based on their Morningstar memorandum. Related research from the Program on Corporate Governance includes Social Responsibility Resolutions by Scott Hirst (discussed on the Forum here) and Reconciling Fiduciary Duty and Social Conscience: The Law and Economics of ESG Investing by a Trustee by Robert H. Sitkoff and Max M. Schanzenbach (discussed on the Forum here).

Key Takeaways

- Asset-manager proxy voting support for ESG-related shareholder resolutions has increased considerably over the past five years, with average support across 50 large fund families rising to 46% from 27%.

- Funds offered by Allianz Global Investors, Blackstone, Eaton Vance, and PIMCO were the most likely to support shareholder-proposed ESG resolutions in 2019, voting for these resolutions more than 87% of the time.

- Five of the 10 largest fund families—Vanguard, BlackRock, American Funds, T. Rowe Price, and DFA Funds offered by Dimensional Fund Advisors—voted against more than 88% of ESG-related shareholder resolutions.

- Large fund groups voting against ESG-related shareholder resolutions kept many of these initiatives from achieving majority support. Nineteen of 23 resolutions earning more than 40% support would have passed if supported by just one of the largest two asset managers.

Fund Proxy Votes Reflect Asset Managers’ ESG Stewardship

Since 2004, U.S.-domiciled open-end and exchange-traded mutual funds have been required to report their annual proxy voting records in SEC filings. Each year at the end of August, asset managers must disclose—fund by fund, item by item—how they voted on portfolio company ballots for meetings held in the preceding proxy calendar year, which runs from July through June.

These records shine a light on how investment fiduciaries, managing trillions of dollars of assets on behalf of fund investors, exercise stewardship. Investors can use their votes on individual ballot items to strengthen investee company governance of emerging ESG risks with votes that shape board oversight, incentive structures, transparency, and company policies. Investors concerned about ESG risks often put forward requests for greater transparency and stronger policies on how companies are overseeing and addressing risks.

Voting is executed by funds based on proxy voting guidelines set by fund advisors—the asset managers offering the funds. Generally, passive fund providers maintain a more centralized system of proxy voting administration, leveraging the resources required for researching and executing votes across multiple funds in a family of funds. Actively managed funds may be voted independently by fund managers. However, in practice, voting may be administered by asset managers in a variety of ways across the funds offered.

How Asset Managers Operationalize Proxy Voting Strategies

Vanguard’s Investment Stewardship team currently administers proxy votes on behalf of the entire suite of Vanguard funds. However, starting in 2020, Vanguard’s actively managed funds, accounting for approximately 10% of assets under management, will be voted independently by their respective managers. [1]

The Proxy Committee of T. Rowe Price, provider of mainly actively managed funds, develops a set of positions on all major proxy voting issues, but leaves the ultimate discretion for proxy voting up to individual portfolio managers. In practice, this results in a high degree of voting consensus across shareholder-sponsored ballot items. [2]

Invesco’s mutual funds and PowerShares’ ETFs take guidance from a Global Proxy Advisory Committee which “provides a forum for investment teams to monitor, understand and discuss key proxy issues and voting trends within the Invesco complex” and assumes responsibility for voting proxies unless explicitly delegated to the respective investment management team. All investment teams track voting via Invesco’s proprietary Fund Manager Portal. [3]

BlackRock’s stewardship team, with members in various international offices, directs proxy voting across BlackRock’s global offering of non-ESG mutual funds and ETFs, which includes all iShares ETFs. BlackRock’s ESG funds vote independently. [4]

State Street’s full suite of funds—including its SPDR ETF offerings as well as its ESG funds—vote in unison according to a strategy administered by the asset manager’s Global Stewardship Team. [5]

Using Morningstar’s multiyear-fund voting data, we examine votes by large asset managers on shareholder-sustainability proposals voted at public-company annual general meetings (AGMs) over the past five proxy seasons, along with a more-detailed analysis of the 2019 proxy season.

Resolutions addressing sustainability risks are filed by shareholders under conditions regulated by the U.S. Securities and Exchange Commission. They request target companies’ management to make disclosures or implement policies or governance arrangements that address issues such as climate risk, environmental stewardship, diversity and inclusiveness, human and worker rights, corporate political influence, public health and product safety, animal welfare, ethical business conduct, cyber security, and online content governance.

Five Years of Asset-Manager Voting on ESG Resolutions

Between 2015 and 2019, 1,033 shareholder-initiated ESG resolutions were voted at U.S. company AGMs, an average of 207 per year. In this section we examine the five-year voting record of 50 of the largest fund families that offer funds to investors in the U.S.

The universe that we considered for inclusion consists of those ranked in the Morningstar Fund Family 150 as of July 2019. [6] These are the largest 150 fund families by fund assets under management in the U.S. To identify the most influential fund groups, we selected the 30 largest fund families from the list, plus others on the list that also ranked among the world’s largest 100 asset managers according to the Investment & Pensions Europe, or IPE, Global 400 Asset Manager Ranking. [7] Based on these criteria we identified 53 fund families. Three were screened out of the final list as they voted on fewer than 25 ESG resolutions in one or more years of the survey: AXA, Aberdeen, and Dodge & Cox.

Wellington Management ranks 13th on the IPE list. The funds it subadvises for Hartford are considered under the Hartford fund family. For two of the 50 fund families we split the votes into two subgroups. Fidelity’s index funds, subadvised by Geode Capital Management, are considered separately because Geode votes the proxies of the funds it subadvises and is itself ranked 55th in the IPE ranking of asset managers. Nuveen funds are considered separately from TIAA Funds as they continue to vote independently following the acquisition of Nuveen Investors by TIAA-CREF in 2014. The analysis is therefore based on the votes of funds belonging to one of 52 fund groups derived from 50 fund families.

Within fund complexes where voting is delegated to portfolio managers, and particularly within multimanager-fund complexes, votes on one resolution can differ from manager to manager. Of the 52 fund groups, 10 had mixed votes, on 10% or more of the resolutions voted where no consensus vote could be identified. There were no natural groupings in any of these cases (like TIAA versus Nuveen or Fidelity actively managed versus Geode) that would eliminate the variance.

The proxy voting decisions of the fund families selected for the survey reflect the voting preferences of large asset managers. The mutual funds offered to U.S. investors by these asset managers collectively control $16.9 trillion—or 88% of all U.S.-domiciled fund assets. [8]

The analysis is based on 516,788 votes cast (for, against, or abstain) across 1,033 individual ESG resolutions by more than 2,000 funds offered within the 52 fund groups. Funds with ESG mandates are excluded from the analysis because, in many cases, they follow a separate proxy voting strategy from the rest of the family of funds to which they belong. The five-year analysis includes ballots voted from July 2014 through June 2019 and reported in fund companies’ N-PX filings.

Growing Asset-Manager Support for ESG Resolutions

Over the past five years, we observe growing asset-manager support for ESG-shareholder proposals reflected in aggregated votes across fund families. In fact, asset-manager support has increased every year since 2015. Average support across the 52 fund groups increased by 19 percentage points, to 46% in 2019 from 27% in 2015, and jumped by more than six percentage points in each of the two most recent proxy years. Appendix B shows support by each of the 52 fund groups for resolutions voted across the five-year survey period.

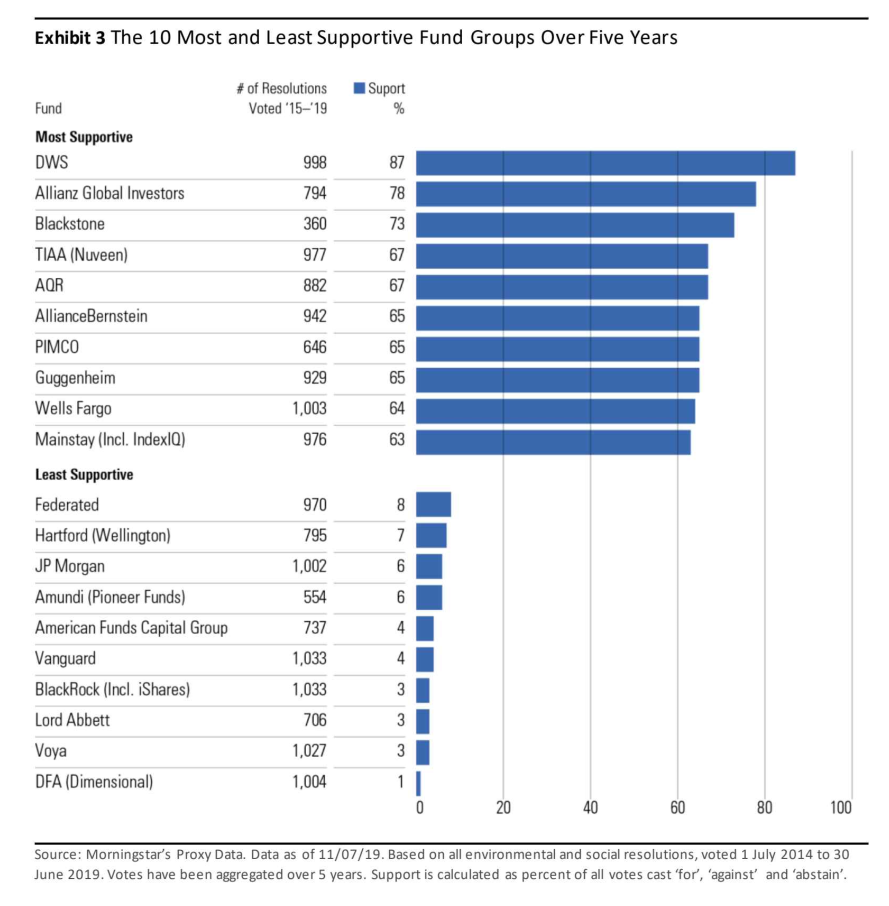

DWS, Allianz Global Investors, Blackstone, Nuveen and AQR Funds supported ESG-shareholder proposals most often over the full five-year period. Fund group DWS led the way, supporting 89% of all 998 items voted. DFA, Voya, Lord Abbett, BlackRock, and Vanguard supported shareholder proposals least often. DFA only supported nine out of 1,004 ESG resolutions voted over the five years.

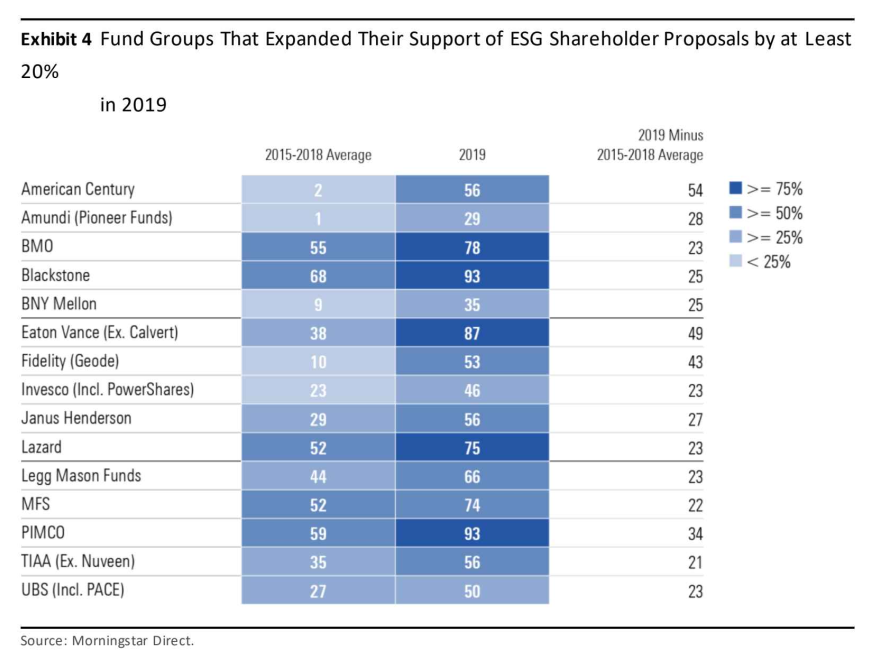

Some asset managers significantly increased their support for ESG-related shareholder proposals in 2019. American Century had the biggest increase. After supporting only 2% (13 of 720) of ESG resolutions voted from 2015 through 2018, the fund group supported 56% (76 of the 135) of ESG resolutions voted in 2019.

Eaton Vance, which acquired responsible investment asset manager Calvert Research and Management in 2016, went from supporting 20% of ESG resolutions in 2015 to supporting 87% of resolutions in 2019. Calvert’s funds themselves are not represented in Eaton Vance’s votes in this analysis because they follow explicit ESG-investing mandates and a separate set of voting guidelines. [9]

Pioneer supported only 1% of resolutions it voted from 2015 to 2018 and then jumped to supporting 28% in 2019. Pioneer Investments was acquired by Amundi, the largest European asset manager in IPE’s 2019 ranking, in July 2017. Full integration of Pioneer Investments into Amundi was completed early in 2019. The increase in support for ESG-shareholder resolutions by Pioneer-branded funds is consistent with Amundi’s strong focus on ESG investing. In addition to offering a range of specialized ESG-investment products, in 2018 Amundi embarked on a three-year plan to incorporate ESG criteria into all funds by 2021, including its ETFs. [10]

Fifteen of the 52 fund groups expanded their support for ESG-related shareholder resolutions in 2019 by more than 20 percentage points over their respective previous four-year averages. Fidelity’s index funds (managed by Geode) unanimously abstained on all 431 resolutions voted in 2015 and 2016, before inching up to 7% of votes “for” in 2017 and then jumping to 30% and 53% votes “for” in 2018 and 2019.

We also observe more asset managers casting a majority of their votes “for” ESG-shareholder proposals. In 2015, only 12 fund groups supported most of the resolutions voted. In 2019, 25 fund groups supported more than half of the ESG resolutions on which they voted. Those numbers include 11 fund groups that voted in support of more than 75% of ESG proposals in 2019. In 2015 only DWS voted in support of more than 75% of ESG resolutions.

Comparing votes across the largest five, the largest 10, and the remainder of the fund groups in our analysis shows that support has increased for each group over the past five years. However, funds offered by the largest asset managers continue to lag those of their smaller peers by a wide margin. As a group, the largest of the asset managers are the least likely to support ESG shareholder-sponsored ballot initiatives.

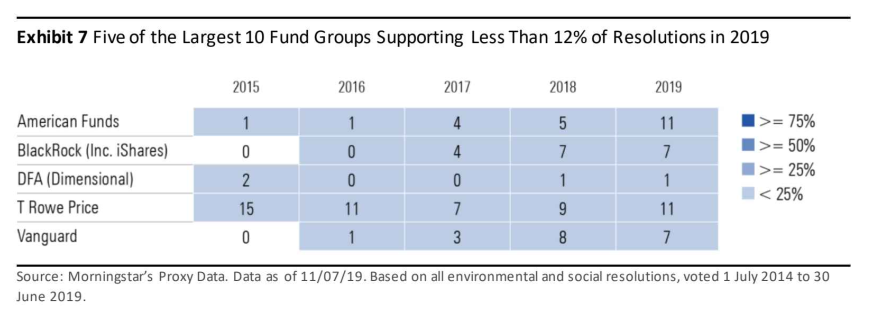

American Funds, BlackRock, DFA, T. Rowe Price, and Vanguard are all among the 10 largest fund managers in Morningstar’s Fund Family 150 ranking, and all but DFA also ranked in the largest 15 asset managers in IPE’s 2019 global ranking. Each supported fewer than 12% of ESG resolutions voted in 2019, bringing average support across the largest five and largest 10 asset managers to below that of the remainder of the fund groups in the study.

In almost all cases, a vote in support of a shareholder resolution is opposed to management’s recommended vote, as corporate boards typically recommend that shareholders vote down the measure proposed. As a group, large asset managers have historically been reluctant to vote against management both on shareholder- and management-sponsored ballot items. The upward trend in asset-manager support for shareholder-initiated ESG resolutions reflects rapidly changing investor attitudes toward the materiality of the sustainability issues that these resolutions address. It shows that asset managers, as a group, are becoming increasingly willing to use their proxy votes to support transparency and better governance of sustainability concerns.

* * *

The complete publication is available here.

Endnotes

1Vanguard Investment Stewardship 2019. “Vanguard funds plan to grant proxy voting responsibilities to external managers.” https://about.vanguard.com/investment-stewardship/perspectives-and-commentary/proxy_ext_mgrs.pdf(go back)

2T. Rowe Price Proxy Voting Guidelines. https://www.troweprice.com/content/dam/trowecorp/Pdfs/C35H15KRK_Final.pdf(go back)

3Invesco’s Policy Statement on Global Corporate Governance and Proxy Voting. December 2019. https://www.invesco.com/corporate/dam/jcr:472ccfeb-b3cc-411e-9996-afd238caa7ad/Invesco-Global-Proxy-Policy-Statement-June-2019.pdf(go back)

4BlackRock Investment Stewardship 2019. https://www.BlackRock.com/corporate/literature/publication/blk-profile-of-BlackRock-investment-stewardship-team-work.pdf(go back)

5State Street 2018 Corporate Responsibility Report. http://www.statestreet.com/content/dam/statestreet/documents/values/2018_STT_CR_Report.pdf(go back)

6Laske, M. 2019. “Morningstar Fund Family 150.” Morningstar Research Services. July 2019 https://www.morningstar.com/lp/fund-family-150 (go back)

7Moreolo, C.S. 2019. “Top 400 Asset Managers: AUM grows 1% amid market volatility.” Investments & Pensions Europe. June 5, 2019. https://www.ipe.com/top-400-asset-managers-aum-grows-1-amid-market-volatility/10031518.article(go back)

8Calculated to be $19.3 trillion according to Morningstar’s Fund Family 150 ranking.(go back)

9Securities and Exchange Commission. 2018. Calvert Funds Proxy Voting Policy and Procedures. Adopted Oct. 10, 2017, as revised April 5, 2018. https://www.sec.gov/Archives/edgar/data/319676/000094039418001332/calvertcomplexsupp.htm(go back)

10Fitzpatrick, N. 2019. “Executive Interview: Amundi Plans to “Stigmatise” ESG Laggards.” Funds-Europe. December 2019. https://www.funds-europe.com/dec-2019-jan-2020/executive-interview-amundi-plans-to-stigmatise-esg-laggards(go back)