Print

PrintRobert Main is COO, Marc Lindsay is Director of Research, and Amy Hernandez is Associate Director of Research at Sustainable Governance Partners. This post is based on a SGP memorandum by Mr. Main, Mr. Lindsay, Ms. Hernandez, and Jessica Strine. Related research from the Program on Corporate Governance includes Socially Responsible Firms by Alan Ferrell, Hao Liang, and Luc Renneboog (discussed on the Forum here) and The Illusory Promise of Stakeholder Governance by Lucian A. Bebchuk and Roberto Tallarita (discussed on the Forum here).

A familiar refrain has emerged as the COVID-19 pandemic continues: companies will be judged for years based on the actions they take today. Perhaps no other issue will generate such long-lasting implications—to a company’s reputation, brand, and resiliency—as how a company treats its people during these trying weeks and months.

It would be naïve to suggest that there is a single right path to manage workforce size, employee health and safety, and the many other human capital issues amplified by the crisis; there are simply too many sector-and company-specific variables. What is clear, however, is the need for companies to proactively communicate their chosen path forward to their stakeholders, and to do so in a transparent, context-rich manner that goes beyond what is disclosed in calmer times. Indeed, the dialogues that companies have today with their investors will impact those relationships—for good and bad—in years to come.

The “S” Moves to the Forefront

Scrutiny of the “S” or social elements of “ESG” is not new, and has tended to fall in two categories: social capital and human capital. The human capital emphasis of the “S” focuses on a company’s labor force and the efforts required to build, maintain, and oversee that labor force’s productive capacity. Executives commonly count their employee base as among their companies’ most important assets, and the Business Roundtable’s 2019 reframing of corporate purpose placed special emphasis on investing in employees. Simultaneously, shareholders—recognizing the investment case for companies that excel in attracting, retaining, and motivating their workforce—have clamored for enhanced human capital disclosure, giving rise to the Workforce Disclosure Initiative, related standards from the Sustainability Accounting Standards Board, and other disclosure frameworks.

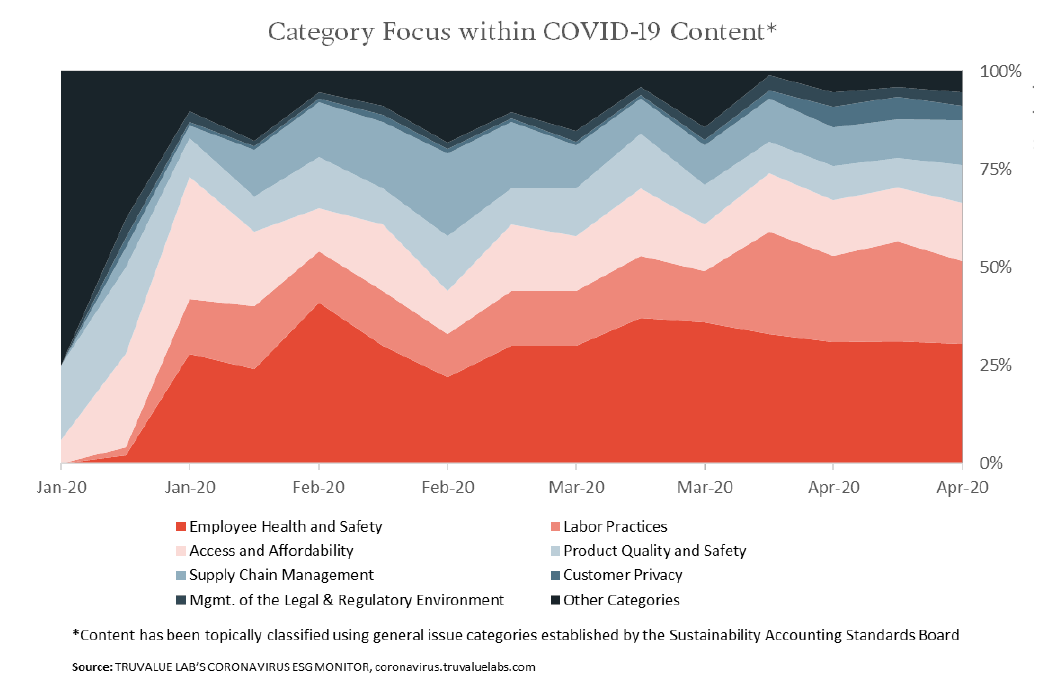

The COVID-19 crisis has accelerated these trends, and we anticipate the pandemic will drive long-lasting attention on the “S” similar to the Great Financial Crisis’ impact upon governance (the “G”). Based on research by the data firm TruValue Labs, labor practices and employee health and safety have quickly become the dominant sustainability topics within public content related to the crisis:

Amidst the crisis, long-term investors have been particularly vocal that companies must not lose sight of employee welfare. Among these sentiments:

- A coalition of 195 institutional investors, representing nearly $5 trillion in assets under management (AUM), signed a public letter urging companies to provide paid leave to all workers (including temporary and contracted workers), prioritize employee health and safety, and take every measure to avoid layoffs.

- State Street Global Advisors, which manages over $3 trillion, indicated that engagement conversations would shift to more immediate ESG issues such as employee health, while urging companies to refrain from taking short-term actions that harm their longer-term sustainability.

- Glass Lewis signaled that boards should proactively seek changes to executive compensation that align with employee and shareholder experiences stemming from the crisis, suggesting that “executives might need to take a pay cut.”

Transparency—and Frank Discussions—are Key

Earlier this month, Securities and Exchange Commission leadership issued a groundbreaking statement noting that upcoming earnings calls will not be routine, and requesting that companies provide as much information as practicable regarding their plans to address the pandemic’s effects. [1] They stated specifically that forthcoming disclosures should respond to investor interest in “how the company’s COVID-19 response, including its efforts to protect the health and well-being of its workforce and its customers, is progressing.”

This statement parallels investors’ demands for more information than normal. Investors are broadly aware that companies’ responses to the crisis are bound by many factors now outside of their control, yet additional context will help investors appreciate this background, how it impacts long-term prospects, and whether the management team has a handle on the situation. To this end, companies should aim to address:

1. Layoffs and reductions

Management teams in some of the hardest hit sectors, such as retail and airlines, have taken the difficult step of laying off or furloughing hundreds of thousands of employees, leading to an unprecedented rise in unemployment. Against this backdrop, some companies, such as Bank of America, Citigroup, and Morgan Stanley, have pledged to suspend layoffs until 2021, while others, such as GM and Ford, are retraining or repurposing their workers to address the pandemic’s immediate needs. However, not all companies—whether due to sector-specific headwinds, historic strategic decisions, or a combination of both—are positioned to maintain their workforce at pre-crisis levels. Difficult decisions—including reductions in workforce, pay cuts, and hiring freezes—will be inevitable.

For this reason, context is essential. In discussions with investors, companies should be prepared to explain how employee costs are being balanced with other capital priorities—debt obligations, capex, dividends, buybacks, etc.—and when and how capital allocation decisions could be expected to normalize. Through engagement, companies will also be able to hear directly from their shareholders, including their long-term investors, on how they consider these trade-offs. As Peter Harrison, CEO of Schroders, an asset manager of nearly $700 billion, has written about the crisis, “all stakeholders will inevitably face pain… Our responsibility today is to ensure industries are supported, that they aren’t engulfed by short-term turbulence. Long-termism must win out.” [2]

2. Employee health & safety

Context is likewise important when it comes to discussing the health and safety of employees. For front-line companies facing heightened exposure to the virus, employee safety will never be guaranteed, but explaining safety measures in the context of broader business imperatives is a message that investors need to hear.

On this topic, investors will want to understand the impact of the virus on companies’ health and safety budgets, and how workers are being protected through such means as: remote work, protections for those who cannot work from home, rotating shifts, and closing locations if necessary. Given that many of the most exposed workers are also part-time employees or contractors, companies should also explain how the company is considering hazard pay, sick leave, or other steps to protect their employees (such as assistance in accessing government support programs or employer-paid health insurance for laid-off workers). Finally, companies should explain their contingencies for leadership succession should senior executives contract the virus.

3. Executive compensation

Not surprisingly, there have been a range of calls from investors—as well as politicians, the employee base, and other stakeholders—for executive pay to be sharply reduced and executives at affected companies to “share the pain.” In response, executives at companies such as Disney, Marriott, and Royal Caribbean, have taken significant pay cuts, sometimes reducing their salaries to zero. At the same time, prudent voices have recognized the need to retain and motivate top management at this trying time. As Sascha Sadan, director of investment stewardship at Legal & General Investment Management has said, “We do need leadership at the moment. We need good people. The best leaders could end up saving their companies a lot more.” [3]

Faced with this balancing act, boards should be mindful that the decisions they make today will be assessed by investors with the benefit of hindsight in future Say-on-Pay votes. Again, there is no one-size-fits-all solution, but boards should be mindful of the broader picture: if shareholder returns drop significantly, if employees face lay-offs or other reductions in pay, the default expectation will be that the executive team’s pay is meaningfully reduced as well. Likewise, pay should be structured so that executives are incentivized to drive long-term business results, and share in the benefits of the recovery.

4. Employee engagement

For years before the crisis, the importance of an ‘engaged’ employee base has been touted, with research reports showing positive relationships with overall productivity. `[4] Particularly for companies who have had to lay-off or furlough a portion of their workforce, investors will want to know what actions—such as additional training or benefits, or monitoring of workforce morale and wellness—are being put in place to retain their loyalty and satisfaction. Investors will also want to understand how companies will resume operations as quickly and safely as possible once the crisis has subsided, particularly if this necessitates a hiring ramp-up of new employees.

5. Role of Executive Leadership

Closely related, companies should elaborate on what actions their leadership teams are taking to keep company culture strong through the crisis, and how they are ensuring continuity of collaboration. Leadership is being tested right now, and culture is a strategic asset overseen by the executive team, and particularly the CEO—not a set of employee policies administered by a human resources department.

Companies that fortify their culture—and double down on their corporate purpose—may be best-positioned to push through these dark times. Research suggests that purposeful employees are more likely to be net promoters of their organization, to stay longer, and to have strong relationships with their colleagues. [5] Likewise, on the other side of the crisis, purpose-driven companies will be well-positioned to recruit talent given millennials’ oft-cited preference to work for purpose-driven firms. [6] It may feel counterintuitive, as management’s every moment is absorbed by the real-time needs of the crisis, but now may be precisely the right time for executives and their boards to revisit, clarify, and communicate their corporation’s purpose.

6. Role of the Board

Underlying each of these issues, governance and the role of the board in overseeing a company’s human capital strategy—the ‘G’ of ESG—is essential for companies to articulate to their investors. Shareholders will expect that the board is playing a significant role in questioning and appropriately challenging management decisions, particularly if they require drastic actions such as layoffs or broad pay reductions. As difficult as these times may be, boards should also be using this crisis to assess the strength of their management teams and succession pipeline; some executives will rise to the challenge, and some will not. Many investors will want to speak directly with a board member, given the importance of these issues.

A (Cautious) Look Forward

No one yet knows the depth or duration of this crisis, but it is reasonable to predict that attention on how well companies treat their employees will persist. Moreover, companies should expect investors to return focus to other human capital issues that were gaining strength before the crisis began, such as diversity among executives and the broader work force, gender and racial pay gaps, and employee development. In future months and years, companies should likewise expect to be asked how the actions they took in connection with the current crisis have impacted those longer-term focus areas.

Every company is facing difficult decisions that will result in difficult conversations with all stakeholders, investors included. But if companies can communicate in a transparent and context-rich manner, those conversations can be the foundation to building a strong relationship that will last for years to come.

Endnotes

1SEC Chairman Jay Clayton and William Hinman Director, Division of Corporation Finance, “The Importance of Disclosure—For Investors, Markets and Our Fight Against COVID-19” (April 8, 2020). The statement emphasized that forward-looking disclosure would be particularly important for investors. Mindful of companies’ concerns about legal risk if such statements prove to be inaccurate, the statement reassured companies that the SEC would not expect to second guess good faith attempts to provide appropriately framed forward-looking information.(go back)

2Peter Harrison, “Strong companies must be supported—but not unconditionally,” Financial Times (March 24, 2020).(go back)

3“The CEO’s coronavirus conundrum: how much pay to sacrifice?,” Financial Times (April 7, 2020).(go back)

4For example, Gallup’s series of Q12 Meta-Analysis Reports has consistently illustrated the connections between highly engaged teams and increases in business outcomes.(go back)

5For example, Imperative’s Workforce Purpose Index: Purpose at Work (2016).(go back)

6For example, The Deloitte Global Millennial Survey (2019) and PwC’s Workforce of the Future (2018).(go back)