Print

PrintElisa Mendoza is Vice President and Jeff Lubitz is Executive Director at ISS Securities Class Action Services LLC. This post is based on their ISS memorandum.

Social and environmental disasters, such as the #MeToo movement, the Deepwater Horizon oil spill, the opioid crisis, data privacy breaches with a vast number of companies such as Yahoo! Inc., Equifax, Inc., are well covered events in the news. These events impact peoples’ lives and many perceive a correlation between these events and civil litigation on the part of the injured or affected persons. However, it may not occur to the average person that these and other similar events have driven many securities class actions since 2016 onward. In fact, the trend of event-driven litigation is rising each year, while the more traditional accounting-based allegations are on the decline. No one can foresee a catastrophic event occurring or witness what goes on behind the closed doors of a publicly traded company or know that a data breach is occurring until after the event has occurred and been exposed. That exposure, sometimes a result of negligence or potentially outright fraud, can often lead to a sharp decline in the stock price and as such, impacts the investors in that stock negatively. Hence, the new trend of event-driven securities class action litigation is on the rise and resulting in more and more recoveries for shareholders, despite more tenuous arguments being the basis of the lawsuits.

When referencing securities litigation, it generally brings to mind well publicized accounting scandals, such as WorldCom, Inc. or Enron Corporation which delivered billions in investor recoveries. These cases hinged on schemes to inflate earnings or cooking up fake holdings and hiding debt through the use of special purpose vehicles or special purposes entities. The accounting fraud for both companies was eventually discovered by internal audits or SEC probes and are examples of the more traditional path leading to a securities class action being brought against any company. The nature of securities class actions for many decades has rested on traditional accounting-based allegations related to revenue recognition, improper allowance for losses, delayed asset impairment, or other violations of generally accepted accounting principles.

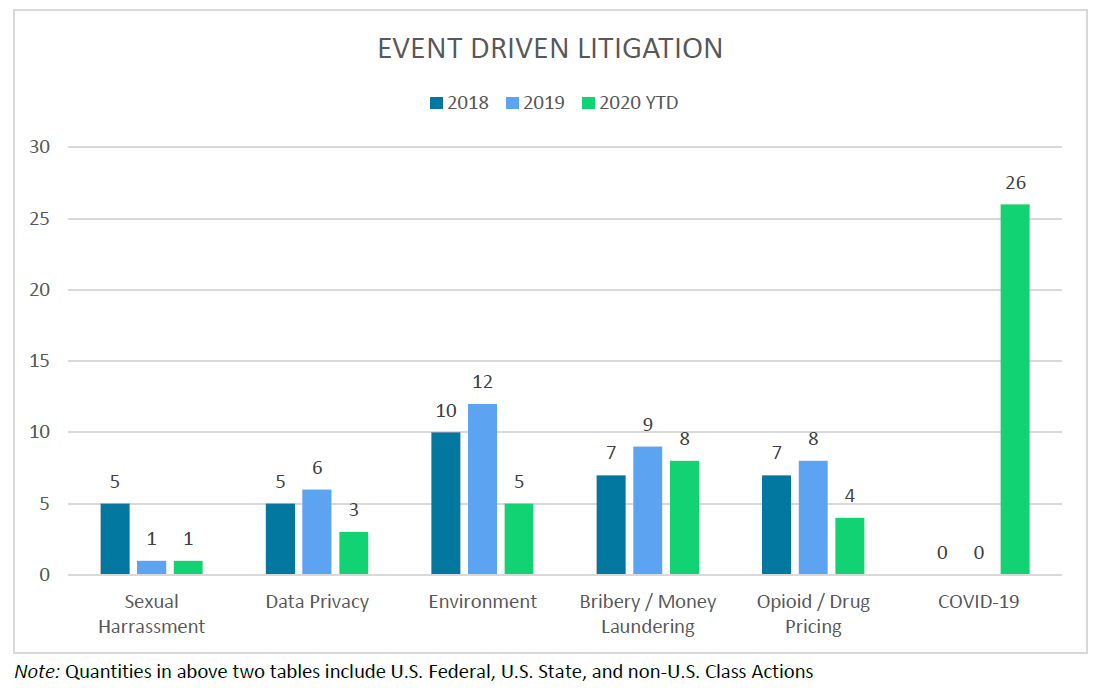

Note: Six growing categories of event-driven litigation.

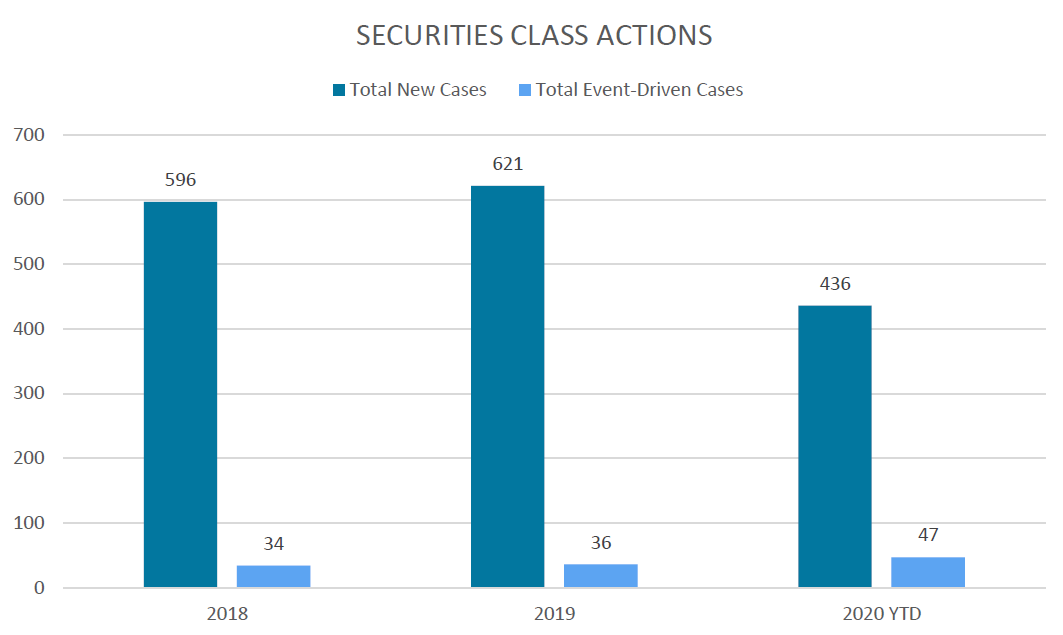

Class action filings over the last few years show a shift from these traditional accounting fraud allegations to more litigation driven by events. “2018 and 2019 both saw 433 cases filed, but the nature of these cases shifted considerably in the last year,” said NERA Managing Director Dr. David Tabak. During 2015 and 2016, the most common type of allegation related to accounting issues, with more than 30% of cases including this type of allegation. In 2018, cases revolving around consequences of the #MeToo movement and the opioid crisis increased, while 2019 saw an increase in filings alleging cyber security breaches and environmental disasters. 2020 has been no exception; now, amid a global pandemic, new filings are occurring based upon the fallout from the Coronavirus and its impact on certain economic industries, such as cruise lines and pharmaceutical companies.

The charts above depict the trends clearly through each of the last three years. In 2018, five cases arose from consequences of the #MeToo movement. Although one was ultimately dismissed, the other four are still active or allowed to progress through the courts in part, including Wynn Resorts Limited, CBS Corporation, and Papa John’s International, Inc. Also rising in 2018 were filings for data privacy breaches after the successful settlement of the Yahoo! litigation. The type of events which drove litigation in 2019 were environmental disasters, with 12 lawsuits being filed, including the BHP Billiton Limited, Vale S.A. and Volkswagen AG litigations that made international news. Only two cases were dismissed in 2019 relating to allegations of environmental causes. This year, 2020, perhaps not surprisingly as noted earlier, has seen a large number of securities class actions being filed based on consequences of the current Coronavirus pandemic, including Norwegian Cruise Line Holdings Ltd., Sorrento Therapeutics, Inc., and Carnival Corporation. Several coronavirus-related cases, those indirectly related to the pandemic, have also been filed by investors, including Eastman Kodak Company and Zoom Video Communications, Inc. To date, none of the Coronavirus related cases have been dismissed.

The subject of whether the event-driven cases have been dismissed is important because the theory these types of cases are based on is very different from the typical securities class action pleadings. Event-driven suits are based on a more tenuous argument than core accounting arguments. The main theory in the event-driven cases is that the occurrence or event upon which the case is based was the materialization of an under-disclosed or downplayed risk. The bulk of the event driven litigation rests on Section 10(b) of the Securities Exchange Act and Rule 10b-5 of the Code of Federal Rules. Section 10(b) makes it unlawful to “use or employ, in connection with the purchase or sale of any security … any manipulative or deceptive device or contrivance in contravention of such rules and regulations as the Commission may prescribe.” Rule 10b-5 makes it unlawful to “make any untrue statement of a material fact” or “omit to state a material fact necessary in order to make the statements made, in light of the circumstances under which they were made, not misleading.”. In addition, a “complaint alleging securities fraud must satisfy the heightened pleading requirements” of Federal Rules of Civil Procedure 9(b). These are the key elements of a claim arising out of an event-driven litigation.1

Taking a closer look at the inner workings of the event-driven litigation, the case against CBS filed August 27, 2018 is one example of a case arising out of the #MeToo movement and the types of allegations being made to connect bad events to a claim that shareholders have been impacted negatively because of the corporation’s conduct or failure to act. In this case, CBS’s proxy statements from 2016 to 2018 incorporated the Company’s Business Conduct Statement which sets forth the ethical conduct expected of all directors and employees. The proxies also stated that the Ethics Code was applicable to the Company’s Chief Executive Officer. When allegations against Les Moonves came out in July 2018, the stock price dropped about six percent and when the exposé was published by the New York Times in December 2018, the stock dropped by an additional four percent. Interestingly, the law firms bringing these tenuous cases in recent years are smaller players in the securities class actions arena that do not have relationships with major institutional investors. As explained by Willis Towers Watson, these firms have little chance of controlling larger cases involving financial irregularities and they therefore focus on cases involving adverse events that institutional investors do not typically bring. (Jeffery A. Dailey)

In the complaint filed in federal court, the Plaintiffs alleged “Moonves and other managers sexually harassed and threatened female employees, fostering a crude and hostile workplace culture.” This behavior and culture created a risk that CBS would lose Moonves, its star executive. Plaintiffs argued that with the advent of the #MeToo movement, the risk of losing Moonves increased because of his behavior, yet Defendants failed to disclose the risk. Meanwhile they were touting to the public the ethical standards of the company and its officers to swiftly act when they learn of unacceptable behavior and to remove that type of behavior from the workplace. The Court denied Plaintiff’s motion in part by explaining that rules of business conduct can be aspirational and therefore are not statements of fact that can then be shown to be misleading, i.e. they are mere puffery. They did uphold the statement made by Moonves himself at an industry event hosted by Variety as misleading and creating the basis of the Plaintiff’s only claim allowed to continue through litigation. The Court upheld this argument because Moonves stated at the Variety event that they were just learning of these (sexual harassment and misconduct) problems, when in fact he was at the time actively seeking to conceal his own past sexual misconduct. Therefore, although not strong (the court even points out that the allegation is “barely” adequate to show a misleading statement of material fact), the court upheld the tenuous argument the plaintiffs made to survive in the securities class action arena and the case progresses partially with no ultimate verdict at this time.

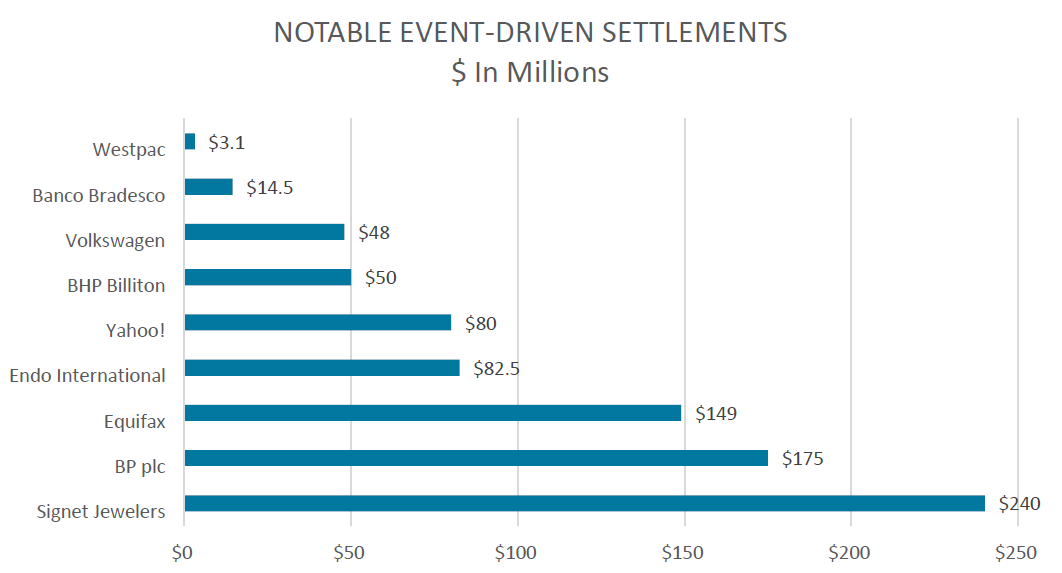

Similarly, Signet Jewelers Limited, one of the largest settlements to date ($240 million) related to #MeToo factors, based its theory of culpability on the same line of reasoning. It alleged that Signet’s culture was rife with sexual harassment of female employees, including the highest levels of the Company. The Plaintiffs further allege that publicity of the “Jock” arbitration by Cohen Milstein posting redacted Declarations in February 2017 that revealed this rampant culture led to the stock price dropping dramatically, by 8.3%. (The “Jock” arbitration had been an earlier legal proceeding brought by Signet’s employees alleging Signet officials engaged in sexual harassment.)ix The nexus connecting the inappropriate behavior to a securities class action again hinges on Section 10(b) and Rule 10b-5 in that the plaintiffs alleged that the Defendant failed to disclose material and relevant information. In denying Defendant’s Motion to Dismiss, Judge McMahon specifically noted that the company had said in its SEC reports that the Jock litigation involved store-level alleged misconduct whereas the allegations in Jock were about pervasive sexual harassment that reached the highest offices in the company. “These allegations,” Judge McMahon said, “suffice to state a claim that Signet’s public disclosures regarding the Jock litigation were false or misleading.” This case includes many allegations not connected to sexual harassment and settled pursuant to mediation, not a court ruling. Therefore, it is difficult to conjecture that the claims would have ultimately been successful if tried by a jury or judge, but one can gather from it that these arguments, even if tenuous, do survive motions to dismiss.

Turning to environmental events, one can see the same theories being asserted. Take for example, BHP Billiton Ltd, which concerns the catastrophic collapse of the Fundao Dam which caused a toxic mudslide that swept away an entire village and killed nineteen people in Brazil, wreaking environmental damage along its path through rivers before finally spilling into the Atlantic Ocean. As news of the devastating event spread across the world, the stock price fell substantially. Again, the Plaintiffs pled under Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 and Rule 10b-5 against BHP (this specific action occurred in the U.S., as BHP has American Depository Receipts on the NYSE). Again, the Court granted Defendant’s Motion to Dismiss in part and denied in part. Plaintiffs alleged that warning signs about the structural integrity of the dam were repeatedly disregarded while BHP officials made various types of actionable misrepresentations and omissions relating to safety, BHP’s financial performance and the incident. The Plaintiffs further claimed that the defendants signed and filed misleading certifications in the Company’s 2014 and 2015 Forms 20-F. Therefore, they argued that had the risks been disclosed, the stock price would not have fallen so dramatically once the event occurred because stockholders would have been apprised of the risks at stake. This case settled after the Judge denied in part the Defendants’ Motion to Dismiss for $50 million and the claim submission process wrapped up in 2019, with recovery payments still pending to affected shareholders.

Other examples of environment related-events that led to securities class actions were the Deepwater Horizon oil spill by BP plc (complaint alleges that BP was misleading the investing public by touting the growth potential of its Gulf of Mexico operations while cutting corners and reducing its spending on safety measures; investor class action settled for $175 million; similar allegations settled with the SEC for $525 million); the Volkswagen emissions scandal that settled for $48 million and disbursed this last July 2020; and Mitsubishi, which similarly revolved around an emissions test scandal but had only been litigated in Japan and remains an active case.

The event-driven trend extends across several other topics such as the Opioid Crisis, Data Privacy, Money Laundering, and now in 2020, Coronavirus. These cases include:

Opioid Crisis

- Endo International plc—Endo International plc manufactures and sells generic and branded pharmaceuticals including both generic and branded opioid products. Plaintiffs alleged that Defendants made false and/or misleading statements and/or failed to disclose that Reformulated Opana ER, an opioid, was not resistant to crushing, was not abuse-deterrent and that its use carried an inherent risk of abuse and that the Reformulated Opana was contributing to the opioid public health crisis by publishing and disseminating false information to health care providers regarding the risks and benefits of opioids. The foregoing, once revealed, was likely to subject Endo International to increased regulatory scrutiny and to financial and/or regulatory harm. Furthermore, they alleged that the Registration Statement filed with the SEC contained untrue statements of material fact and omitted material facts. On June 10, 2020, New York Governor Andrew Cuomo announced that the New York Department of Financial Services had filed administrative charges and thereafter, Endo International’s share price fell nearly 15%. The Defendants filed a Motion to Dismiss which was denied in part and granted in part. Thereafter the parties entered mediation and the parties settled for $82.5 million dollars. The claim deadline was February 7, 2020 and claims are pending payment to all eligible investors.

Data Privacy

- Yahoo!—In January 2017, a securities class action lawsuit was initiated against Yahoo! alleging that the Defendants had failed to disclose the two largest data breaches in U.S. history, in which hackers stole the records of three billion users in 2013 and compromised the accounts of 500 million users in 2014, thereby causing financial harm to its investors. The Plaintiffs further alleged that Yahoo! continued to fraudulently reassure the public that it had safeguards in place to protect personal information and that it would disclose security vulnerabilities within 90 days of discovery. The data breaches included users’ names, e-mail addresses, telephone number, birth dates, passwords, social security numbers, security questions linked to users’ accounts and credit/debit card information. The complaint goes on to allege that Yahoo! sat on the data privacy breach even while negotiating and finalizing a sale of its core business to Verizon in 2016. Due to the data breach coming to light, Verizon renegotiated a $350 million price reduction. When the market learned of the data breach, the value of Yahoo shares plummeted by over 31%, the hook whereby Plaintiffs allege that investors were financially harmed and thus initiated the securities class action. The statutory grounds for the allegations were Section 10b and Rule 10b-5 of the Federal Rules of Civil Procedure. Yahoo! settled with investors in March 2018 for $80 million. As Kevin Lacroix from The D&O Diary points out this settlement is significant at the time, not because it is one of the Top 100 securities suit settlements, but because it is the first substantial data breach-related shareholder lawsuit recovery. It was a milestone development that opened the door for similar data breach lawsuits such as Equifax and Facebook. Interesting to note, and a possible cause of this case settling quickly, the stipulation of settlement was reached on the defendant’s behalf by Altaba, an investment company that held certain former assets of Yahoo! as a result of the Verizon acquisition. If the company had not been acquired shortly before the lawsuits were initiated, one can speculate that the outcome might have been different, i.e. the acquiring company most likely brought pressure to settle the pending lawsuits quickly.

- Equifax—In 2017, Equifax, a consumer credit reporting agency, announced a “cybersecurity incident” potentially impacting 143 million U.S. customers. The information breach included names, Social Security numbers, birth dates, addresses, and credit card numbers. This was easily the largest news story of the week, appearing on front pages across all major newspapers and the lead story of all newscasts. The first trading day after the release of the data breach news, Equifax’s stock price dropped nearly 15%. Plaintiffs’ lawyers filed a securities class action lawsuit alleging that defendants made misleading statements and omissions around the sensitive information in Equifax’s custody, the vulnerability of the company to cyberattack, and the company’s compliance with data protection laws. Ultimately, shareholders alleged that the stock price was artificially inflated based on these misleading statements and omissions and that it ultimately fell when “the truth was revealed.” Defendants filed a motion to dismiss and the judge granted the motion in part and denied it in part. The parties entered mediation and the parties settled for $149 million dollars. The claim deadline was July 22, 2020 and claims are pending payment to all eligible investors.

- Facebook—In 2018, the New York Times published an investigative report that revealed that Cambridge Analytica used the data of 50 million people obtained from Facebook without proper disclosures or permission. After the news broke, the stock price fell 6.76%. A day later, Bloomberg published an article disclosing that the Federal Trade Commission was probing whether Facebook had violated terms of a consent decree for its handling of user data. After this article circulated, the stock price fell another 4.48%. The Plaintiffs’ lawyers filed a securities class action lawsuit alleging that the defendants made false and/or misleading statements and failed to disclose that Facebook violated its own purported data privacy policies by allowing third parties to access the personal data of millions of Facebook users. The Defendants filed a Motion to Dismiss. The Court found that the Plaintiffs failed to prove falsity for the statements it asserted as being misleading except for one statement, Statement 22, but ultimately rejected the argument because they ruled that the Plaintiffs failed to plead scienter as to this Statement, and thus they granted Defendants’ Motion to Dismiss with leave to amend. The Plaintiffs filed an amended complaint. The Court again granted Defendants’ Motion to Dismiss with leave to amend until September 23, 2020. There is no record of the Plaintiffs amending their complaint again. Thus, this case will be dismissed with prejudice.

Money Laundering

- Danske Bank—Danske Bank’s central management were alleged to have knowledge of its Estonian branch’s money laundering activities since late 2013. The central management took nearly two years to mitigate these activities and engaged in a cover-up to keep the truth from financial regulators in Estonia and Denmark, and from its investors. An independent investigation uncovered that an exorbitant $234 billion flowed through the bank as part of the money laundering scheme from 2007 to 2016. Once the fraud was publicly disclosed, Danske’s stock lost over $12.8 billion in value. Plaintiffs’ lawyers filed a securities class action lawsuit alleging that the Defendants had made materially false and/or misleading statements. The Defendants filed a Motion to Dismiss and the Court granted the Motion stating that the Plaintiffs had failed to plead fraud with specificity. After giving leave to amend the complaint three times, the Court ultimately dismissed the action with prejudice. Although the action was dismissed in the United States for failure to state a claim, investors continue to pursue numerous ongoing securities class action litigations in Denmark and at least six criminal and regulatory investigations are pending in Estonia, Denmark, France, the United Kingdom, and the United States.

- Wirecard—Wirecard was formed in Germany in 1999 as a payment system company. In 2015, the Financial Times reported suspicious growth for Wirecard and its un-transparent accounting. In 2020, Wirecard delayed the publication of its 2019 annual report because its auditor, Ernst & Young Gmbh Wirtschafsprufungsgesellschaft, was unable to confirm an amount of €1.9 million on Wirecard’s balance sheet. Later, Wirecard confirmed that the €1.9 million allegedly held in a trust account with banks in the Philippines did not exist, retracting earlier statements regarding its TPA business and preliminary 2019/2020 results. Wirecard also informed the market that it was facing immediate debt payment obligations and that it had fired COO Jan Marsalek and CEO Dr. Markus Braun had resigned. The stock dropped 99% from January 29, 2019 to August 4, 2020. The Plaintiffs’ lawyers alleged that Wirecard employed devices, schemes and artifices to defraud, made untrue statements of material facts or omitted material relevant facts. The company announced it had filed for bankruptcy on June 25, 2020. There are currently two litigations pending against Wirecard in the United States, and several more litigations pending in Germany against Wirecard through an insolvency proceeding and against Wirecard’s auditor, Ernst & Young, in Germany as well.

Coronavirus

- Sorrento Therapeutics—Sorrento Therapeutics is a biopharmaceutical company that researches human therapeutic antibodies for the treatment of infectious diseases. In May of this year, Sorrento announced that it would work to generate antibody products that would act as a “protective shield” against SARS-CoV-2 coronavirus infection. On May 15, 2020, Sorrento announced that it had discovered an antibody that had “demonstrated 100% inhibition of the SARSCoV-2 virus infection. Founder and CEO of the company both referred to the breakthrough as a “cure.” Stock value increased by 281.7% from the date of the announcement to May 18, 2020. On May 20, 2020, Hindenburg Research issued a report rebutting Sorrento’s claims. The stock then declined 43%. The founder then proceeded to walk back their previous statements in their announcement by saying it could potentially be a cure after certain checks on the efficacy of the medication were followed. The Plaintiffs’ lawyers allege that Defendants misrepresented and/or failed to disclose that: (i) the Company’s initial finding of “100% inhibition” in an in vitro virus infection will not necessarily translate to success in a person; (ii) the Company’s finding was not a “cure” for COVID-19; and (iii) as a result of the foregoing, Defendant’s positive statements were materially misleading. As a result of these materially misleading statements and omissions, the shareholders suffered significant losses and damages. The case is presently pending before the United States District Court of Southern California.

- Kodak—Eastman Kodak is another Coronavirus related litigation that is also based on violations of Sections 10(b) of the Securities Exchange Act of 1934 and Rule 10b-5 of the Federal Rules of Civil Procedure. The company announced on July 27, 2020 that it was entering a “new manufacturing initiative” involving the US International Development Finance Corporation (“DFC”) to assist in creating drugs for the treatment of Coronavirus. The Plaintiffs allege that the defendants, using material non-public information, granted its CEO and Executive Chairman 1.75 million stock options and awarded 45,000 stock options each to its CFO, Vice-President and General Counsel before publicizing the “new manufacturing initiative.” The next day, upon announcement of the government loan from the DFC to produce pharmaceutical materials, including Covid-19 drugs, share prices surged by over 200%. The massive stock price increase, Plaintiffs allege, allowed the Defendants to enrich themselves off of the insider information and the compensation scheme they created. Senator Elizabeth Warren wrote a letter to the SEC asking it to investigate the deal between the DFC and the company for alleged violations of the insider trading laws. Additionally, news came to light that a religious institution received a generous charitable contribution of 3 million Kodak shares but that the religious institution was controlled exclusively by one Kodak board member. These developments caused the stock price to drop, adversely impacting investors and shareholders. The DFC, due to increasing public awareness and Congressional and regulatory scrutiny paused the deal with Eastman Kodak, causing the stock price to decline again. The action was filed on August 13, 2020 and is currently pending before the United States District Court of New Jersey.

- Carnival Cruise Lines—Carnival Cruise Lines has also been sued in the wake of the pandemic. In February 2020, 3,700 passengers and crew were quarantined aboard the Diamond Princess, a ship operated by Princess Cruises, a cruise line owned by Carnival. On February 20, the ship docked in San Francisco and at least one known COVID infected person disembarked. By March 2020, seven Company ships accounted for 49 of the 70 cruise ship fatalities. An article published in April 2020 suggested that Carnival may have failed to adequately protect passengers from COVID-19 on a series of cruise voyages and even continued to operate new cruise departures. After this news article was circulated, the share price dropped; a second article was published, and the share price fell again. In May 2020, Plaintiffs filed a securities class action litigation alleging that specifically, Defendants failed to disclose to investors that: (1) the Company’s medics were reporting increasing events of COVID-19 illness on the Company’s ships; (2) Carnival was violating port of call regulations by concealing the amount and severity of COVID-19 infections on board its ships; (3) in responding to the outbreak of COVID-19, Carnival failed to follow the Company’s own health and safety protocols developed in the wake of other communicable disease outbreaks; (4) by continuing to operate, Carnival ships were responsible for continuing to spread COVID-19 at various ports throughout the world; and (5) as a result of the foregoing, Defendants’ positive statements about the Company’s business, operations, and prospects, were materially misleading and/or lacked a reasonable basis. This case is currently pending before the United States District Court of Southern Florida.

- Securities class actions have also been filed against Norwegian Cruise Line and most recently, Royal Caribbean Cruises Ltd for similar allegations this current year due to consequences from the Coronavirus pandemic.

Conclusion

As explored above, event-driven litigation hinges on allegations around misleading or fraudulent statements or the omission of materially relevant information that had the investor known the true or omitted information, the investor would have possibly made different investment decisions. These U.S. based cases hinge on pleadings based upon Section 10 of the Securities Exchange Act of 1934 and Rule 10b-5 of the Federal Rules of Civil Procedure. Securities fraud claims have pleading challenges. Claims under Rule 10b-5 must be pled with particularity under Rule 9(b) and the PSLRA’s heightened pleading standard. In the examples above, the pleadings of the Plaintiff are not always successful. Cases such as Danske Bank and Facebook were not successful because they were not plead with specificity. Other causes of action were dismissed, such as in the CBS litigation, because the Court ruled that some company statements are aspirational or puffery and do not create actionable guidelines by which the Company must act, or else be accused of publishing a misleading statement. In all cases though, the framework has been laid for others to mimic in creating securities class actions based upon events in real-time instead of accounting errors or accounting fraud. Because a higher and higher number of these litigations are reaching successful settlements, ISS Securities Class Action Services believes the trend will most likely continue to rise in the years to come and will continue to track and report on these critical developments.

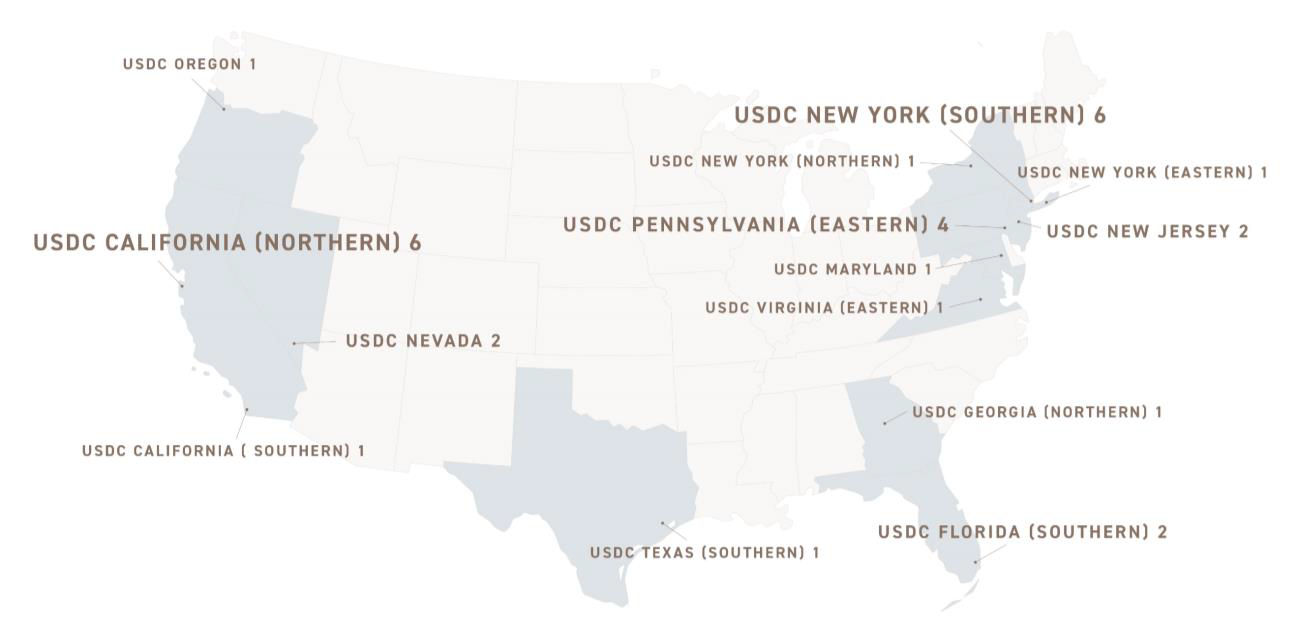

Note: Frequent U.S. District Court venues for event-driven litigation.

The complete publication, including footnotes, is available here.