Print

PrintMatteo Tonello is Managing Director of ESG Research at The Conference Board, Inc. This post relates to Shareholder Voting Trends Live Dashboard, an online dashboard published by The Conference Board in partnership with ESG data analytics firm ESGAUGE and in collaboration with Russell Reynolds Associates and Rutgers Center for Corporate Law and Governance. Related research from the Program on Corporate Governance includes Social Responsibility Resolutions (discussed on the Forum here) by Scott Hirst.

This post provides an overview of shareholder resolutions filed at Russell 3000 and S&P 500 companies through mid-July 2022, including trends regarding the volume and topics of shareholder proposals, the level of support received by those proposals when put to a vote, and the types of proposal sponsors. The report is accompanied by a Live Dashboard, which contains the most current figures and enables data cuts by market index, business sectors, and company size groups. Please refer to the dashboard for the most recent data.

This commentary offers insights for what may lie ahead in the following areas:

- The continued increase in the number of shareholder proposals related to social and environmental policies of the company.

- Shareholder expectations regarding climate-related targets and disclosure.

- The success of many shareholder proposals on civil rights or racial equity audits.

- The alignment of corporate political activity and the firm’s stated values.

- The pressure on smaller public companies to endorse governance practices that are now widely used by their larger counterparts.

- The emerging link between softening support for director elections and company say-on-pay support levels, on the one hand, and investors’ dissatisfaction with corporate ESG performance, on the other.

The project is conducted by The Conference Board and ESG data analytics firm ESGAUGE, in collaboration with leadership advisory and search firm Russell Reynolds Associates and Rutgers University’s Center for Corporate Law and Governance (CCLG).

Shareholders filed a record number of shareholder proposals in 2022.

As of mid-July 2022, The Conference Board and ESGAUGE had recorded 813 filings in the Russell 3000 and 642 in the S&P 500—the highest volume reported in each index in the last five years. Collectively, Russell 3000 companies received 471 proposals on environmental and social policy (or 57.9 percent of the total), up from 403 in 2021 (50.9 percent), 339 in 2020 (45.9 percent), and 328 in 2018 (44.7 percent). By comparison, there were only 41 executive compensation proposals this year, compared to 42 in 2021 and 54 in 2020; corporate governance-related proposals declined from 305 in 2021 and 317 in 2020 to 258 this year.

- The rise in environmental and social proposals is primarily attributed to a higher number of requests for policy changes (including the disclosure of climate change risks, diversity and pay gap analyses, political contributions, and lobbying, among other issues) primarily submitted by individual investors and the investment vehicles of stakeholder groups (i.e., a heterogeneous category of organizations pursuing various social causes, including PETA, Oxfam America, not-for-profit As You Sow, and the National Center for Public Policy Research think tank). Directors can play an important role in the engagement with the company’s key shareholder base and have a constructive dialogue on issues that are increasingly viewed as critical to a company’s sustainable business strategy.

- As these new types of nonbinding resolutions in the environmental and social practice areas are introduced, investors tend to test them at larger companies: the S&P 500 reports an average number of proposals per company that is four times as high as the one of the Russell 3000. In fact, while the number of proposals per company has been constant in the Russell 3000 over the last few years (hovering in the 0.29–0.31 range), it has grown at larger companies in the S&P 500 (from the 1.14 of 2018 to 1.41 in 2022). Even in the Russell 3000, when one looks at the number of proposals on subjects of environmental and social policy, companies were receiving an average of 0.86 proposal in 2020; the number rose to 1.05 in 2021 and 1.28 in 2022. Even the most ardent advocates need to be selective about the companies they engage with. Their choice is therefore often dictated by the larger environmental and social impact of bigger companies as well as the consideration that a debate on ESG issues at prominent organizations is more likely to receive media attention and to extend its influence on the universe of smaller firms.

- It is also interesting to note that the consumer discretionary and materials industries are primarily responsible for the rise in resolution volume observed this year. Across other sectors, volume has in fact remained stable or slightly declined.

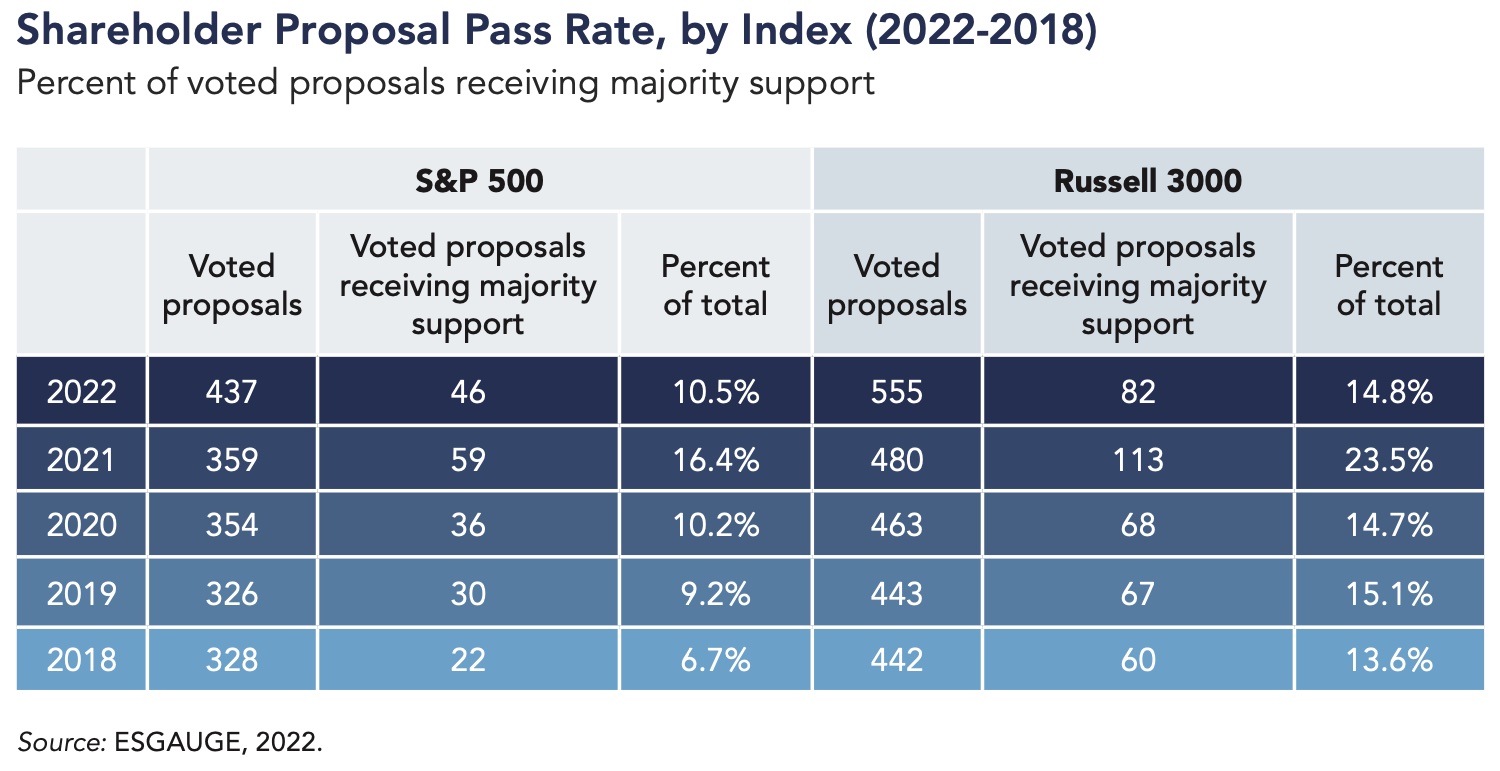

The number of voted proposals also rose in 2022. However, due to the higher filing volume and the low support of proposals submitted by organizations objecting to an expansionary corporate ESG policy, the pass rate has declined.

Average support levels and pass rates (i.e., percentage of shareholder proposals receiving majority support) appear to be down this year after peaking in 2021. Upon a closer look, however, this appears to be a function of the higher volume of filings and the emergence of a new type of formulations—those submitted by investment funds affiliated with conservative organizations (in particular, the National Legal and Policy Center and National Center for Public Policy Research’s Free Enterprise Project) to counter what they consider an increasingly progressive institutional investor agenda in the ESG area. [1]

We counted 49 filings from those two organizations alone in 2022. Their explicit goal is to provide an alternative viewpoint to the argument used by more traditional proponents. For example, the resolution submitted by the National Center for Public Policy Research at Johnson & Johnson uses terminology that closely resembles other requests for companies to commission a racial equity audit. However, the resolution’s supporting statement clarifies that what motivates the proponent is the concern that anti-racism training in companies’ racial equity programs is itself “deeply racist” and that employees deemed “non-diverse” could be discriminated against; and it goes as far as accusing Bank of America, American Express, Verizon, Pfizer, and CVS of “sponsoring and promoting overtly and implicitly discriminatory employee-training programs.” [2]

While such resolutions had little traction (in fact, most of those that went to a vote received single-digit support levels, with the J&J proposal scoring only 2.7 percent of for votes), the overall number of submissions increased so much that it affected the average voting results and pass rate of all shareholder resolutions across subject areas. Specifically, in the S&P 500, when “conservative” submissions are counted, 10.5 percent of all shareholder resolutions that went to a vote as of mid-July 2022 received majority support and passed—a share like the one recorded in 2020 but significantly lower than the 16.4 percent reported last year. Similarly, in the Russell 3000, when “conservative” submissions are counted, 14.8 percent of the shareholder resolutions voted in the 2022 proxy season passed—a share like the one recorded in 2020 but significantly lower than the 23.5 percent reported last year.

- While smaller companies are less likely to receive shareholder proposals than larger ones, the shareholder resolution average pass rate is higher in the Russell 3000 than in the larger companies that comprise the S&P 500. In fact, the analysis by company size of the entire Russell 3000 index shows an inverse correlation between the annual revenue of the company and the average shareholder resolution pass rate.

- Russell 3000 companies in the materials sector reported the highest percentage of proposals that won majority support in 2022, whereas the pass rate for shareholder proposals in the energy sector declined to 15.4 percent from the record 51.7 percent recorded in 2021.

- Despite their impressive volume growth in 2022, shareholder proposals on topics of environmental and social policy registered the highest year-on-year pass rate decline. In fact, the rise in numbers helps explain the pass rate decline, as several of the newly submitted proposals this year were considered of lesser quality or too prescriptive to gain wide support. This was the case, for example, for the proposals described above by the National Center for Public Policy Research or by the National Legal and Policy Center. It was also the case for requests to ban the financing or underwriting of projects that could lead to an increase in fossil fuel consumption (which some institutional investors such as BlackRock were reluctant to support given the current uncertainties in the global energy market). [3] In 2022, 11.4 percent of proposals in this thematic category received majority support. The rate is down from the record 20.4 percent of 2021 but remains in line with the percentage reported in 2020 and well above the 4.3 percent and 4.1 percent found in 2019 and 2018, respectively.

On Investors’ Scrutiny of Corporate Environmental and Social PerformanceWhile endowment funds of religious orders and the investment vehicles of special stakeholder groups were the first to call attention to them, corporate environmental and social policies have now moved to the front and center of proxy seasons for more mainstream investors too. Executives should ensure their boards are apprised of the growing prominence of these proposal types, especially given that they would rarely pass only a few years ago but now may have more uptake. Directors can play an important role in engaging with the company’s key shareholder base and have a constructive dialogue on these issues now that they are increasingly viewed as critical to a company’s business strategy. Proponents may be pursuing different agendas. In some cases, they may in fact want the company to fully adopt the proposed organizational change or to undertake practical actions to advance toward that goal. In other cases, they may use the proposal to seek the board’s attention on a more ample range of issues. Finally, there may be proponents who are more interested in the public attention they can raise on the issue of the proposal (i.e., climate change) than in the outcome of the proposal at that specific company. The company should try to appreciate the proponents’ motivations when developing its proposal response strategy. At least in some of these cases, engagement can help to reassure investors that the company is taking sustainability seriously and aligning it with the company’s business. Providing additional environmental and social disclosure can also be an opportunity to proactively win investor support and control the company’s message on key stakeholder concerns. When legal considerations suggest a prudent approach to disclosure, companies should consider mapping their disclosures to key stakeholder concerns and being prepared in situations where the concerns are publicly escalated. |

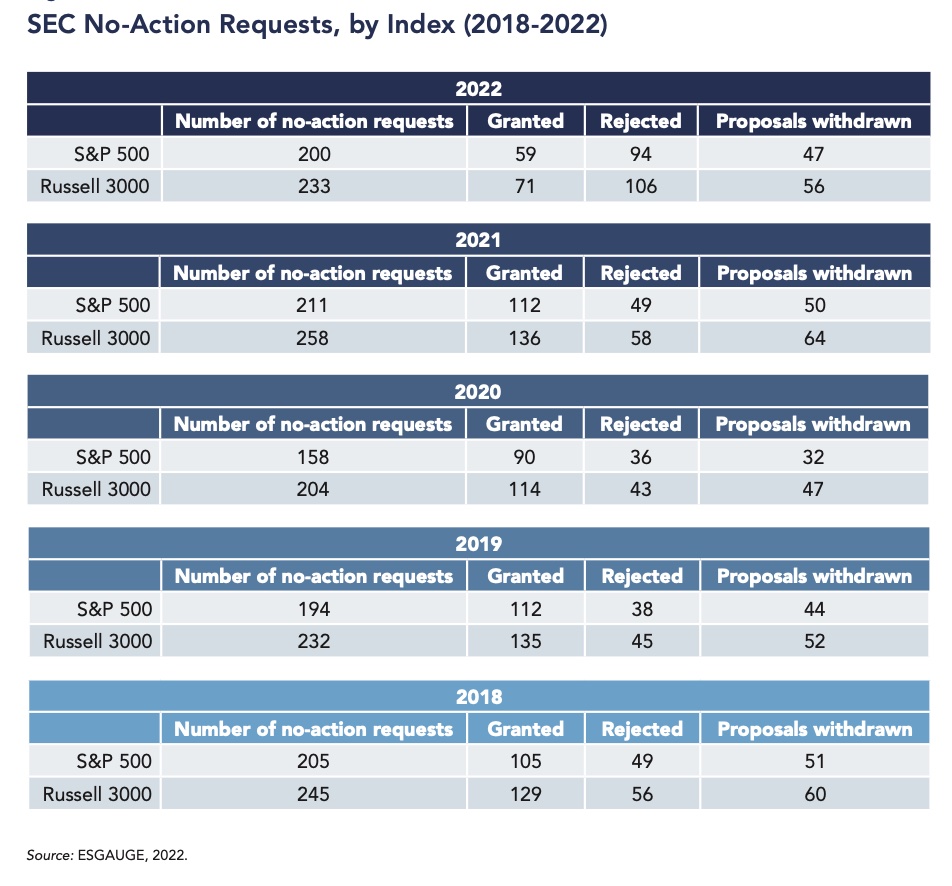

A recent SEC staff policy change has reduced management’s ability to omit shareholder resolutions from the voting ballot, while the steady number of negotiated withdrawals of proposals may speak to the effectiveness of corporate-investor dialogue—whether because proponents become apprised of (and are satisfied with) the company’s commitment to a proposal issue or because of a negotiated compromise.

The SEC staff had long adhered to a policy that allowed companies to exclude shareholder proposals from their proxy statements if they dealt “with a matter relating to the company’s ordinary business operations,” unless the proposal also dealt with a “significant policy issue.” Companies could succeed in excluding a proposal if there was not a sufficient nexus between the company’s business and the policy issue. With Staff Legal Bulletin No. 14L in November 2021, however, the staff stated it would “no longer focus on determining the nexus between a policy issue and the company but will instead focus on the social policy significance of the issue that is the subject of the shareholder proposal.” [4]

Following this policy change and the diminishing grounds for no-action relief, the SEC staff rejected many more no-action requests during the 2022 proxy season (in the Russell 3000, 106 rejections out of 233 requests) than in 2021 (58 rejections out of 258 requests), and the number of shareholder proposals that management omitted from the proxy ballot after obtaining no-action relief was cut in half—from 136 in 2021 to 71 this year. By contrast, voted proposals jumped 15 percent, from 480 to 555.

Of the 13 omitted proposals submitted by stakeholder groups, nine were filed by either the National Legal and Policy Center or National Center for Public Policy Research. Just as in prior years, many other omissions were related to proposals submitted by individual investors. The highest number of granted no-action requests were obtained for climate-related resolutions that the SEC staff considered so prescriptive that they would impede the day-to-day management of the company. This was the case for a proposal at Tesla that tried to impose a five-business-day period for the company to liquidate newly acquired cryptocurrency assets deemed to have a high environmental impact.

In the Russell 3000, 187 proposals were withdrawn in 2022, up from 168 in 2021 and 148 in 2020. Of all withdrawn proposals, 32.1 percent were submitted by stakeholder groups, 20.3 percent by large investment advisory firms, 16.0 percent by individuals, and 15.5 percent by religious groups. Generally, figures on withdrawals illustrate the importance of corporate-investor engagement as a means of addressing shareholder concerns outside of the formal voting process that takes place at an annual meeting. For example, a resolution filed by As You Sow at Dominion Energy was withdrawn after the company announced its commitment to a net-zero carbon emission strategy meant to align its footprint with the milestones of the Paris Agreement. [5]

Demands for climate-related disclosure dominated the 2022 proxy season, with 1 out of 4 voted resolutions gaining majority support at this year’s AGMs.

In 2022, shareholders filed a record number of environmental proposals, in most cases related to climate change. Typically, requests for disclosure on climate-related issues range from the company’s current carbon footprint to the mitigation targets it set to align with the standards of the Paris Agreement; and from the impact that rising temperatures can have on business operations to the risks resulting from maintaining the current levels of greenhouse gas emissions. Companies that have not yet done so should consider the benefits of a process to gather and disclose information on their carbon footprint and emission-reduction strategy.

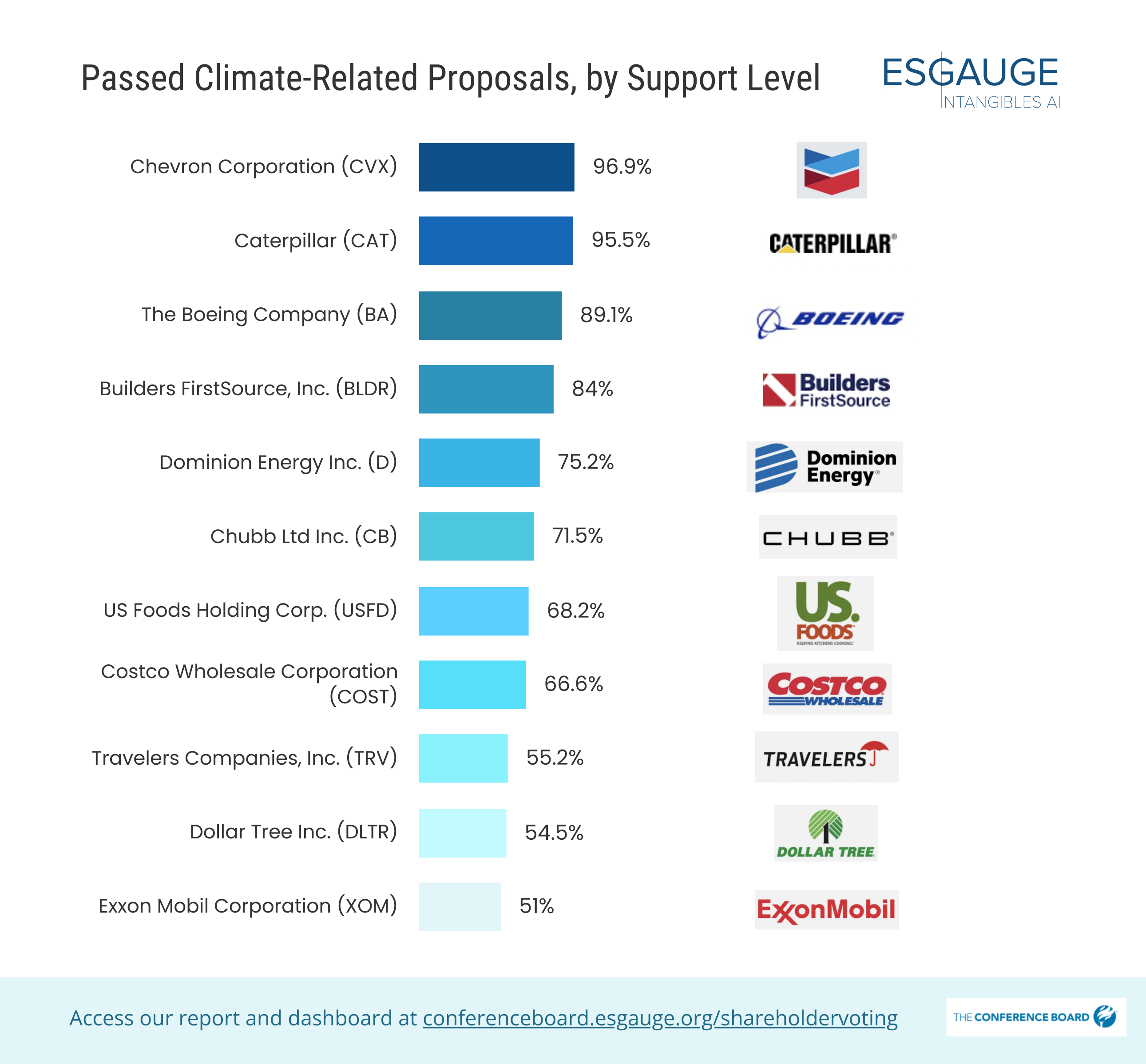

- The Conference Board and ESGAUGE recorded 101 climate-related filings in the Russell 3000 in the period from January 1 to July 15, 2022, up from 60 resolutions in the same period of 2021 and 50 in 2020. Of the climate-related proposals filed in 2022—mostly by the investment vehicles of nonprofit As You Sow or of religious groups such as Mercy Investment Services—11 obtained majority support and passed. Their recipients include large companies such as Boeing, Caterpillar, Chevron, Chubb, Costco, and Exxon Mobil. It’s the highest number ever reported: by comparison, eight climate-related proposals passed in 2021, three in 2020, zero in 2019, and one in 2018.

- This year, shareholders also approved one plastic pollution proposal, requesting that fast-food chain Jack in the Box disclose how the company intends to develop comprehensive sustainable packaging practices that include transitioning from single-use plastic to reusable containers, eliminating black plastic and toxic substances, and adopting Forest Stewardship Council-certified materials. Of the 7 proposals of this type that went to a vote, it was the only that passed during the examined period.

- Another notable development of the 2022 proxy season is that there were no say-on-climate proposals. Spearheaded by London-based hedge fund The Children’s Investment Fund Management (TCI), this type of proposal appeared in 2021 but failed to gain traction in the broader investment community. It requested that shareholders be given the opportunity in the annual proxy statement to provide an advisory vote on whether, in consideration of global climate benchmarks, they approve of the company’s publicly available climate policies and strategies. None of the four say-on-climate resolutions that went to a vote in the Russell 3000 in 2021 passed (two were filed by TCI and two by US-based As You Sow).

On the Demand for Emission-Reduction Goals and Climate Change DisclosureCompanies that have not yet done so should consider gathering information on the costs and benefits of designing an emission-reduction strategy that includes targets and timelines, and addressing the business risks resulting from global warming. Especially if their business is conducive to emitting significant levels of greenhouse gases, companies should be forthcoming about their approach to the problem as investors, proxy advisors, and regulators continue to intensify their focus on climate change and the transition to a net-zero economy. For example, while expressing concerns about proposals with unduly prescriptive formulations that may constrain the decision-making of boards and management, BlackRock has also been vocal about its intention to continue to demand more disclosure of companies’ emission-reduction plans and climate-related strategy. [6] Proxy advisor ISS, reacting to findings from the last edition of its Climate Policy Survey [7] —where a vast percentage of investor respondents supported establishing more stringent forms of board accountability for companies that are “significant greenhouse gas emitters” (through their operations or value chain)—introduced for 2022 the policy of recommending voting against the incumbent chair of the responsible board committee in situations where corporate disclosure appears lacking or unpersuasive. [8]

Last but not least, in March 2022, the SEC proposed climate-related disclosure rules that, if approved, will require a publicly traded company to publish information about:

|

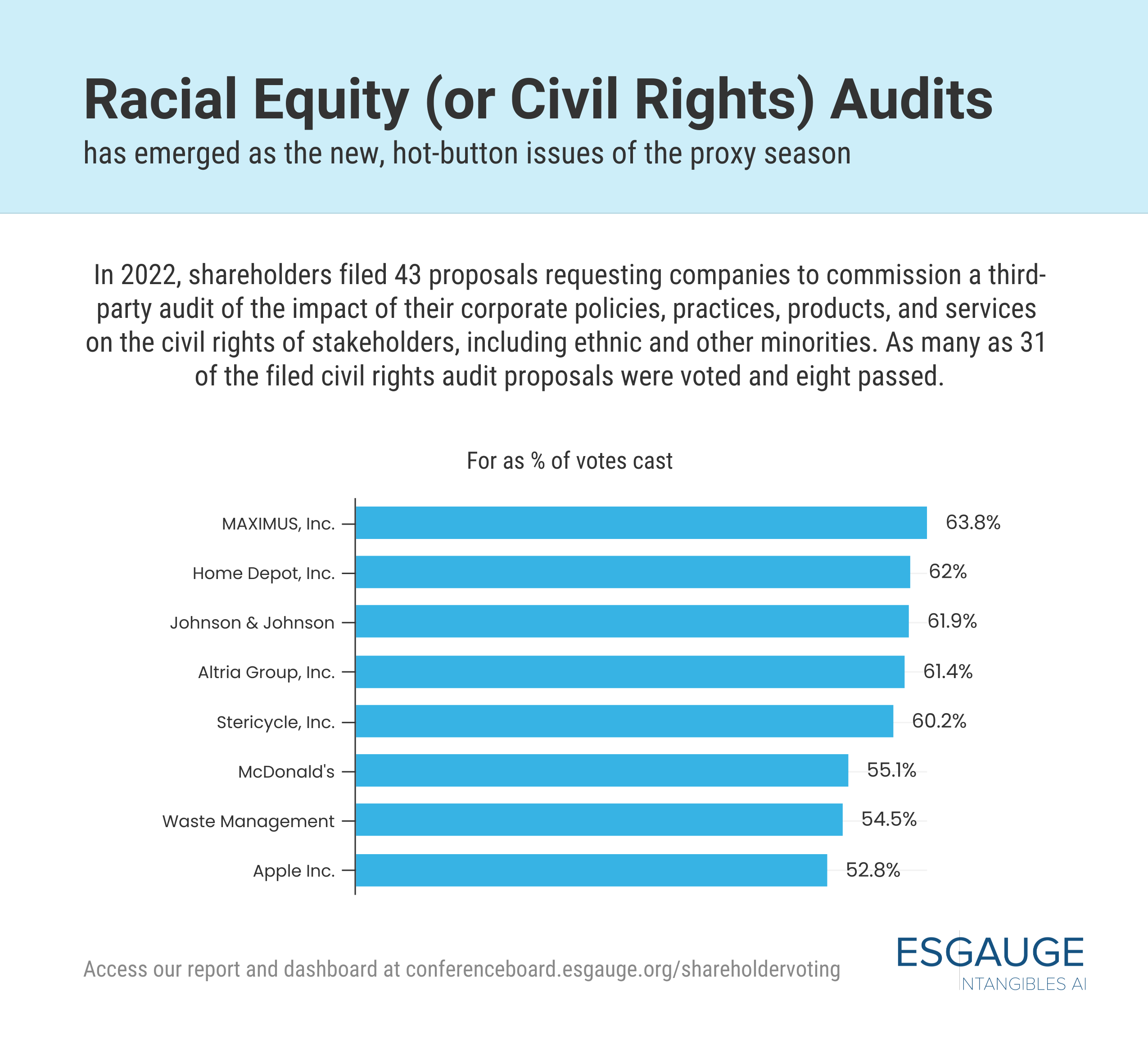

Racial equity or civil rights audits emerged as the new, hot-button human capital management (HCM) issue of the 2022 proxy season, with several proposals receiving a majority of for votes at large companies.

Human capital management has moved to the front and center of the proxy season since the onset of the COVID-19 pandemic. In 2022, just as in the environmental area, shareholders filed a record number of HCM-related proposals (155, up from 136 in 2021) on issues ranging from board and workplace diversity to the concealment of sexual harassment and from workforce pay gaps to the audit of racial equity and/or civil rights. A total of 14 resolutions across these topics passed at Russell 3000 annual shareholder meetings held in the period from January 1 to July 15, 2022, compared to 13 in the same period of 2021, five in 2020, three in 2019, and none in 2018. Companies should evaluate the circumstances that warrant commissioning a civil rights or racial equity audit.

- In the examined 2022 period, shareholders at Russell 3000 companies filed 43 proposals requesting companies to commission a third-party audit of the impact of their corporate policies, practices, products, and services on the civil rights of stakeholders, including ethnic and other minorities. The text of most of these resolutions clarifies that the audit is meant to extend beyond legal and regulatory matters and recommends that the process include soliciting input from civil rights organizations, employees, customers, and communities where the companies operate. This proposal type was first introduced last year, when all nine of the filed proposals went to a vote but none received majority support. This year, 31 of those 43 civil rights audit proposals were voted and eight passed—among them, those filed at Altria, Home Depot, Johnson & Johnson, McDonald’s, and Waste Management. Proponents often view the notion of civil rights broadly; for example, the request at Altria focuses specifically on the impact that the company’s investment in e-cigarette maker Juul may have on the civil rights of youth.

- Four shareholder proposals on employee arbitration policies also passed this year, up from only one in each of the last two proxy seasons. These requests raise concerns about the application of nondisclosure clauses often included in employee agreements to prevent employees from speaking openly about instances of harassment or discrimination they might have experienced during their tenure—requiring instead that any such claim be subject to a confidential arbitration procedure. This year, proposals requesting that the company report on this practice were approved by shareholders at Apple, IBM, Sunrun, and Twitter. Two proposals, filed at Lowe’s and The Walt Disney Company, to report on median and adjusted employee pay gaps across race and gender also won majority support in 2022.

- In 2022, shareholders also voted on 11 proposals on board diversity (down from 12 in 2021), five on workplace diversity (down from 14 last year), and two on divulging EEO-1 data on workforce demographics and its breakdown by gender and race (down from three in 2021). While 10 proposals in those categories were successful last year, none of the 2022 proposals passed.

On Civil Rights Audits and the Role of Corporations in Addressing Societal DisparitiesProponents of civil rights or racial equity audits argue that business organizations should understand whether they inadvertently play a role in creating or sustaining societal disparities. In the last few years, several companies have chosen to commission an internal audit of this type, whether in response to a specific demand from shareholders or because of the publicity that a certain corporate practice had received. In 2016, Airbnb was the first major US corporation to investigate its practices after data showed that its hosts were less likely to accept reservations from Black guests. [10] In another example, in 2018, Starbucks agreed to investigate its racial equity practices after national headlines about an incident where a store manager called the police on two African American patrons who were waiting in the coffee shop for a business meeting. [11] And, as mentioned earlier, investors at Altria, Johnson & Johnson, and McDonald’s, among other companies, voted in favor of a civil rights/racial equity audit during the most recent proxy season.

Many boards may hesitate to endorse this practice. Civil rights and racial equity audits can be costly, lengthy, and quite complex to conduct. Their scope may be questioned, and their results disputed, which would ultimately amplify the magnitude of the problem they were meant to address. A tangible commitment to promote equality, accompanied by specific targets and milestones (e.g., a financial institution that introduces a program to increase the number of home purchase mortgages it underwrites for racial minorities), might be seen as a much more pragmatic and effective way for a business to contribute to the making of a more equal society. Having said that, there may be situations where a company would benefit from a civil rights or racial equity audit. For example:

When a company determines that an internal civil rights or racial equity audit is desired or appropriate, it should consider the following aspects:

|

In 2022, shareholders supported requests for political spending disclosure and, at one company, human rights: a proposal at a gun manufacturer linking firearm sales and reputational risk passed with a large majority.

This proxy season witnessed a remarkable rise in the volume of voted resolutions pertaining to corporate social policies (outside of the HCM and civil rights audit area). Shareholders filed a total of 177, of which 131 went to a vote (compared to 99 voted social proposals in 2021). Almost all topics in this category—from animal welfare to human rights and from political spending to public health—saw a higher number of voted proposals compared to last year. Nonetheless, the category was the most underperforming of the season, and almost all these requests received limited voting support—with average support level generally declining from 2021.

- In the examined 2022 period, shareholders in the Russell 3000 voted on 53 political spending proposals—including requests for disclosure on monetary contributions offered to political campaigns and on lobbying activities. Of those, four passed (two per category, down from six and four, respectively, in 2021). They were on the voting ballot at Dollar General, Netflix, Travelers Companies, and Twitter. Last year, shareholders also supported five proposals for the disclosure of lobbying activities that proponents contend may be misaligned with the company’s carbon emission reduction plans and public stance on issues of global warming; by contrast, none of the four climate-related lobbying resolutions filed in the examined period of 2022 passed.

- In 2022, shareholders at firearm manufacturer Sturm, Ruger & Company also approved a proposal requesting that the company conduct and disclose the outcome of a third-party assessment of the impact of corporate policies and products or services on human rights around the globe. The formulation of the request is similar to those on civil rights audits. In this case, the proponent, an investment fund affiliated with Catholic health system CommonSpirit Health, argued that, given the lethality of firearms and the possibility of their misuse, the company was exposing itself to a human rights risk that “can be a bellwether for a company’s long-term viability.” The proposal passed, winning 68 percent of for

- In 2022, shareholders of Russell 3000 companies filed and voted on 13 resolutions on charitable giving—the highest on record. By way of comparison, there was only one voted proposal of this type in each of the 2021 and 2020 proxy seasons. The typical formulation calls for publishing and maintaining a semiannual report that itemizes and quantifies all (monetary and in-kind) charitable donations made by the company and/or any of its managed or controlled foundations, aggregated by the name and address of each recipient of more than $999 annually and including information on the rationale for each contribution as well as the policy and procedures followed to grant it. Despite the rise in volume, all of the 13 voted proposals failed the annual shareholder meeting vote; in fact, they all received only single-digit support.

On the Demand for Transparency in Corporate Political SpendingCorporate lobbying, political contributions, and other forms of corporate influence on the public discourse on policy issues have been increasingly scrutinized in recent years. Investors and other stakeholders have focused on situations where investors and other stakeholders perceive a company’s public stance on social and environmental matters to be out of alignment with its—often less publicly promoted—political activities, including lobbying and political contributions.

When the company does engage in political activities or chooses to be vocal on issues of public policy, the board should:

|

Resolutions demanding shareholders’ right to call special meetings tripled in 2022. A few other proposals passed at smaller companies that have not yet endorsed widely accepted governance practices.

Over the last few years, the focus of the proxy season has gradually shifted from issues of corporate governance to environmental, human capital, and social issues. The 2022 season confirmed this trend. In the period from January 1 to July 15, 2022, shareholders of Russell 3000 companies filed 258 proposals related to corporate governance matters (or 31.7 percent of the total number of filings), compared to 303 proposals in the same period of 2021 (38.6 percent of the total) and 316 in 2020 (43 percent). Moreover, shareholders gave majority support to only 30 corporate governance–related proposals, a sharp decline from the 50 recorded in the same period in 2021. Passed resolutions requested bylaws amendments to allow for shareholders to call special meetings, eliminate supermajority requirements, declassify the board, and transition from a plurality to a majority voting standard in uncontested director elections.

- In the examined 2022 period, investors filed 114 resolutions requesting their right to call special meetings of shareholders, or three times as many as those recorded in 2021 proxy statement filings. This proposal topic alone represented almost half (44.2 percent) of all governance-related proposal submissions in the season. Almost all special meeting proposals went to a vote (109 proposals), and nine (or 8.3 percent of the 109) passed. They were filed by individual shareholders (namely, John Chevedden, Kenneth Steiner, and Myra K. Young) at health care/medical equipment firm Becton, Dickinson; energy giant ConocoPhillips; and aerospace and defense technology company Northrop Grumman, among others.

- In 2022, investors also approved nine of the 11 voted proposals, filed by John Chevedden and Kenneth Steiner, to eliminate supermajority vote requirements and apply a simple majority voting standard to any shareholder voting matter. Prominent firms where the resolutions were successful include The Southern Company, Goodyear, Netflix, and Fortinet.

- This season, shareholders also approved five resolutions to declassify the board structure and four to change the standard for director elections from plurality to majority voting. Both practices are now widely adopted, and smaller firms are now the likeliest targets for these resolutions; see “On the Choice of Departing from Widely Adopted Governance and Compensation Practices” on page X. For many years, requests for board declassification have been receiving the highest average support level of all nonbinding shareholder proposals: in 2022 it was the highest on record—or 84.7 percent of votes cast, up from 82.5 percent of 2021 and 73.8 percent of 2019. Their major proponent, CorpGov.net publisher James McRitchie, was successful at health care companies Invitae and NanoString Technologies, while Kenneth Steiner introduced the proposals that passed at financial firms Carlyle Group and New York Community Bancorp. Resolutions on the change from plurality to majority voting received majority support at smaller materials company Warrior Met Coal and information technology companies 2U and Ncino (all with annual revenue of about $500 million or less), but also at a larger health care technology company, IQVIA ($13 billion).

In the last decade, following the adoption of say on pay, shareholder resolutions on executive compensation issues have declined in volume and rarely reached the majority support level. This year, however, four such resolutions, regarding golden parachutes in severance agreements, passed. [15]

The proposals were introduced by individual investors John Chevedden and Kenneth Steiner at airlines Alaska Air Group and Spirit AeroSystems Holdings, and at biotech AbbVie and information technology company Fiserv. They all used the same formulation, where “shareholders request that the board seek shareholder approval of any senior manager’s new or renewed pay package that provides for severance or termination payments with an estimated value exceeding 2.99 times the sum of the executive’s base salary plus target short-term bonus.” The four successful proposals are part of a record number of proposal filings of this type in 2022 (16 in total, compared to only four in each of the 2021 and 2020 periods). In 2021, there was only one successful proposal on this topic, and none in each of the prior three years.

Just as in prior years, shareholders also voted on handfuls of proposals related to CEO pay ratio, the use of “clawback” provisions to recoup incentive pay, enhanced disclosure of the link between pay and performance, and equity retention period requirements. However, none of them reached majority support.

On the Choice of Departing from Widely Adopted Governance and Compensation PracticesGovernance and executive compensation practices that were the focus of the proxy season only a decade ago are now commonly adopted, at least among larger public companies. This is certainly the case for board declassification, majority voting, and the policy of seeking shareholder approval of termination pay included in severance agreements with senior executives. Current data from The Conference Board and ESGAUGE’s Corporate Board Practices Live Dashboard show that, in the S&P 500 Index, only 13.7 percent of companies still stagger the terms of their director service. Even in the Russell 3000, where board classifications are much more common, almost 60 percent of companies have transitioned to annual elections for all their board members (though the percentage drops to 30 for companies with annual revenue under $100 million). Similarly, less than 10 percent of S&P 500 companies continue to use a system of plurality voting in their director elections, which was the norm for all publicly traded companies just over 10 years ago and remains prevalent today at smaller organizations in the Russell 3000. Directors and executives should be aware that some investors are now specifically targeting those governance and compensation issues at smaller firms. While many companies in that cohort have thus far remained immune to changes in their director election system, things may change. In particular, boards should take a careful and holistic look at changing their director election practices. While plurality voting and staggered boards can be seen as protections against activism, they can also invite activism. As for staggered boards, they are increasingly perceived as an impediment to board turnover, and companies may wish to consider shifting to annual elections if it helps them to adjust the composition of the board in a way that keeps pace with strategic needs. As for golden parachutes, The Conference Board Task Force on Executive Compensation placed them on a list of “contentious” pay practices as far back as 2009, recommending that companies review them through the pay-for-performance lens and “avoid them except in limited circumstances,” given the risk that they could “erode credibility and trust of key constituencies.” [16] Today, proxy advisor ISS has a policy for investors to vote in favor of any shareholder proposals requiring that executive severance agreements be submitted for shareholder ratification, unless the proposal requires shareholder approval prior to entering into employment contracts. Per ISS guidance:

|

The analysis of the last four years of say-on-pay resolutions shows a decline in average support level, higher failure rates, and a rising number of Russell 3000 companies receiving less than 70 percent for votes, a threshold that may attract additional scrutiny from proxy advisors and investors.

After being quite stable for almost a decade following the adoption of SEC rules governing advisory votes on executive compensation, average support level for say-on-pay (SOP) proposals has been declining in the last four years. Of the Russell 3000 SOP proposals voted in the examined 2022 period, 96.8 percent passed, down from an average of 97.6 percent in the prior three years. Of the S&P 500 SOP proposals voted in the examined 2022 period, 95.8 percent passed, down from an average of 97.4 percent in the prior three years.

- In 2022, in the Russell 3000, the SOP failure rate (i.e., vote support below 50 percent) was 3.2 percent, up from an average of 2.5 percent in the prior three years. In the S&P 500, it was 4.2 percent in 2022, up from an average of 2.4 percent in the prior three years. As of July 15, 2022, the list of Russell 3000 failed SOP votes in this proxy season contains 67 companies (up from 61 last year, 45 in 2022, and 50 in 2019), including JP Morgan, Intel, The TJX Corporation, Halliburton, and Netflix. Average support level for companies on the failed SOP list was 35.5 percent of votes cast.

- Other companies reported passing SOP proposals with support of less than 70 percent of votes cast, the level at which proxy advisory firms may scrutinize more closely their compensation plans and consider issuing a future negative recommendation. In 2022, the share of Russell 3000 companies in this category was 6.8 percent, up from an average of 5.2 percent in the prior three years. In the S&P 500, it was 6.3 percent in 2022, up from an average of 5.5 percent in the prior three years. As of July 15, 2022, the list of Russell 3000 SOP votes with support level of 70 percent or lower contains 143 companies (up from 102 last year, 109 in 2020, and 124 in 2019), including Amazon, Apple, First Republic Bank, CSX Corporation, Coca-Cola, Virgin Galactic, and Twitter. Average support level for companies on this list of SOP underperformers was 60.9 percent of votes cast.

- There was also a notable decline in the percentage of companies that received the support of 90 percent or more of the votes cast for their SOP management proposal. In the Russell 3000, 70.5 percent of the companies were in this category in 2022, down from an average of 74.9 percent in the prior three years. In the S&P 500, 66.1 percent of the companies were in this category in 2022, down from an average of 73.3 percent in the prior three years.

Compensation experts have suggested that there may be a link between these recent trends regarding the SOP vote and the increasing scrutiny of corporate ESG performance by large institutional investors.

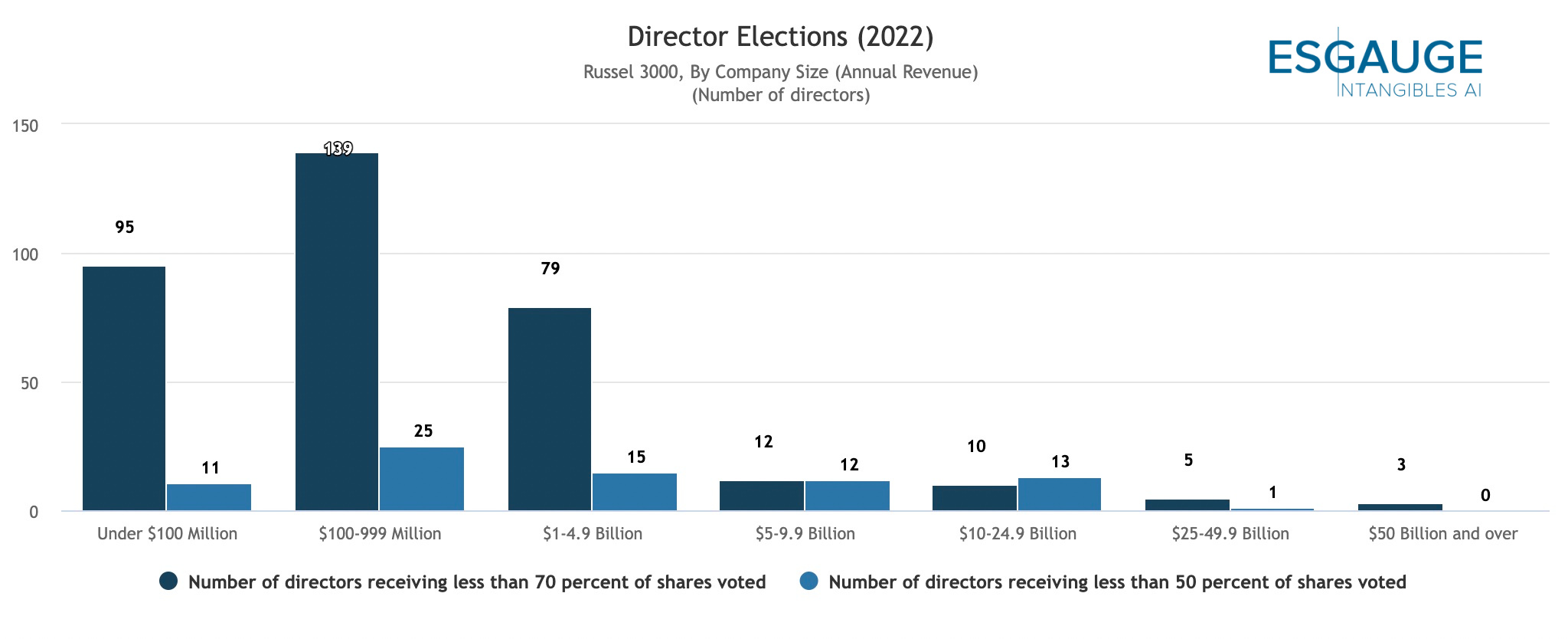

Average support levels for board-endorsed candidates in director elections have been declining in recent years. In 2022, 75 directors nominated by management did not get elected—a multiple of the number recorded only a few years ago.

In the Russell 3000, for example, average support level went from 98.2 percent of votes cast in 2017 [17] to 95.1 percent in 2020 and 94.1 percent in 2022. Only seven directors in the entire index had failed to receive majority support in 2017, while the number climbed to 50 in 2020 and 75 in 2022. Similarly, the number of directors who received less than 70 percent of votes cast was only 83 in 2017 and rose to 290 in 2020 and 442 in 2022. While these numbers are relatively small when compared to the full director population in the examined index (almost 17,500 directors were up for reelection in the Russell 3000 in 2022), they were never observed in earlier years.

Just as in other recent proxy seasons, the health care sector reported the lowest average support level in director elections in 2022, at 90.6 percent of votes cast; it was 92.8 percent in 2020 and 97.4 percent in 2018. Utilities companies reported the highest, or 96.8 percent; it was 97.3 percent in 2018. The company size analysis shows significantly lower average director election support levels among smaller companies; for example, those with annual revenue under $100 million showed a support level of 88 percent, down from 92 percent in 2018; there were only two failed director elections in 2018, and the number grew to 10 in 2022. By way of comparison, larger companies with annual revenue reported a director election support level of 95.5 percent this year and no failed election.

On Business Leaders Being Held Accountable for Perceived Poor ESG PerformanceA link is emerging between softening director election support levels, on the one hand, and investors’ perceived dissatisfaction about corporate ESG performance. [18] Some commentators have also speculated that the recent decline in SOP support may be attributable not only to excessive compensation but also to the lack of pay-for-sustainability performance. [19] Major asset managers have become quite explicit about the intention of holding individual board members and senior executives accountable for their lack of leadership regarding ESG issues within their purview. These are just a few examples of their expansionary policy, and for now the focus seems to be on larger companies:

Board members and C-suite executives should remain educated about ESG issues of concerns to the investment community and the proxy advisors that often influence institutional votes. They can do so by maintaining year-round lines of communication with their largest shareholders, by monitoring voting policies and stewardship reports, by benchmarking their company’s ESG disclosure practices against those of its peers, and by tracking the outcome of resolutions submitted during the proxy season (including those that were withdrawn from the voting ballot after private engagements). At least for now, the new accountability voting policies described above seem to be confined to the most serious cases of perceived ESG shortcomings; if a company is not yet prepared to endorse a certain ESG practice, the engagement process is the channel to persuade investors of its rationale for a more measured approach. |

Endnotes

1Andrew Edgecliffe-Johnson and Brooke Masters, Political Proxies: Conservative Activists File Record Shareholder Proposals, Financial Times, March 28, 2022, cites data and analysis by The Conference Board and ESGAUGE.(go back)

2Johnson & Johnson, 2022 Proxy Statement, p. 126.(go back)

3BlackRock, 2022 Climate-Related Shareholder Proposals More Prescriptive Than 2021, May 2022. Also see Merel Spierings, 70% of Environmental Shareholder Proposals Going to Vote, The Conference Board ESG Blog, May 20, 2022.(go back)

4US Securities and Exchange Commission (SEC), Shareholder Proposals: Staff Legal Bulletin No. 14L, November 3, 2021.(go back)

5Dominion Energy, Dominion Energy Broadens Net-Zero Commitments, press release, February 11, 2022.(go back)

6BlackRock, BlackRock Investment Stewardship. Proxy Voting Guidelines for US Securities, January 2022, p. 17.(go back)

7Institutional Shareholder Services (ISS), 2021 Global Policy Survey—Climate. Summary of Results, October 1, 2021.(go back)

8ISS, United States Climate Proxy Voting Guidelines. 2022 Policy Recommendations, January 19, 2022, p. 14. For 2022, ISS applied the policy to “significant GHG emitters,” which it defined as those on the Climate Action 100+ Focus Group list.(go back)

9SEC, The Enhancement and Standardization of Climate-Related Disclosures for Investors, Release Nos. 33-11042, 34-94478, March 21, 2022. Also see SEC, SEC Proposes Rules to Enhance and Standardize Climate-Related Disclosures for Investors, press release, March 21, 2022.(go back)

10Ray Fisman and Michael Luca, Fixing Discrimination in Online Marketplaces, Harvard Business Review, December 2016.(go back)

11Jill Disis, Starbucks Advisers Say the Company Needs to Do More to End Racial Bias, CNN Business, July 2, 2018.(go back)

12Amazon.com, Inc., Notice of 2022 Annual Meeting of Shareholders & Proxy Statement, May 25, 2022.(go back)

13Edward Skyler, Citi Will Conduct a Racial Equity Audit, press release, October 22, 2021. A major investor that filed a successful shareholder resolution requesting the audit in 2021 argued that most of the resources from the initiative were in fact allocated to instruments such as loans and other market-priced investments that would ultimately benefit the bank rather than the disadvantaged communities.(go back)

14Starbucks Corporation, Starbucks to Close All Stores Nationwide for Racial-Bias Education on May 29, press release, April 17, 2018; Airbnb, Inc., Elevating Our Commitment to Non-Discrimination and Human Rights, press release, July 9, 2021.(go back)

15Golden parachutes are lucrative severance arrangements offered to certain executives in case of mergers or other change-in-control events that would lead to their termination. See Peer Fiss, A Short History of Golden Parachutes, Harvard Business Review, October 3, 2016. The SEC adopted rules on the approval of golden parachutes, under the Dodd-Frank Act, in 2011: see SEC, Shareholder Approval of Executive Compensation and Golden Parachute Compensation, Release No. 33-9178; 34-63768, January 25, 2011.(go back)

16The Conference Board, The Conference Board Task Force on Executive Compensation, September 21, 2009.(go back)

17See Matteo Tonello, 2021 Proxy Season Preview and Shareholder Voting Trends (2017-2020), The Conference Board, January 26, 2021, p. 17.(go back)

18For a recent investigation of the consequences of ESG failures for the business leadership, see Richard Walton, What Do the Consequences of Environmental, Social and Governance Failures Tell Us About the Motivations for Corporate Social Responsibility?, International Journal of Financial Studies 10, no. 1 (2022): 17.(go back)

19See Todd Sirras et al., What Do Elevated Shareholder Expectations Mean for Large Company Boards and Compensation Programs?, Harvard Law School Forum on Corporate Governance, July 31, 2022.(go back)

20ISS, United States Climate Proxy Voting Guidelines. 2022 Policy Recommendations, January 19, 2022, p. 14.(go back)

21ISS, US Climate Proxy Voting Guidelines, p. 14.(go back)

22BlackRock, BlackRock Investment Stewardship. Proxy Voting Guidelines for US Securities, January 2022, pp. 5, 6, and 4, respectively.(go back)

23State Street Global Advisors, Proxy Voting and Engagement Guidelines—North America (United States & Canada), March 2022, p. 6.(go back)

24AllianceBernstein, Proxy Voting and Governance Policy, March 2022, p. 9.(go back)